|

市場調查報告書

商品編碼

2066699

北美緩釋肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Controlled Release Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

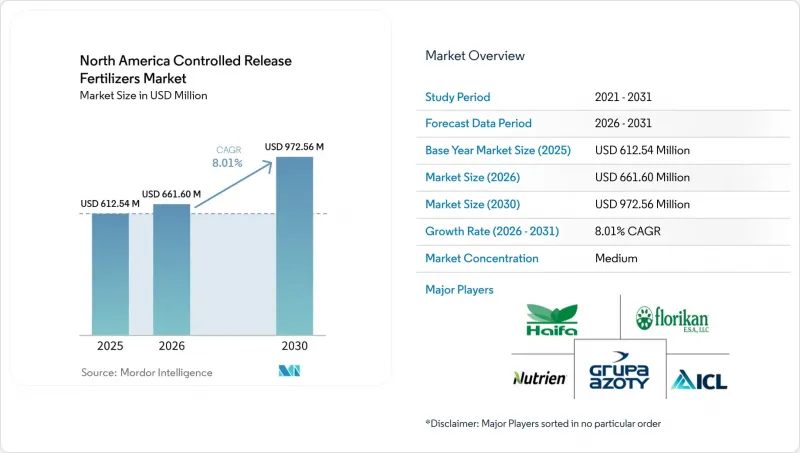

根據 Mordor Intelligence 預測,北美緩釋肥料市場規模將從 2025 年的 6.1254 億美元和 2026 年的 6.616 億美元成長到 2031 年的 9.7256 億美元,2026 年至 2031 年的年複合成長率(CAGR)。

本報告按塗層類型(聚合物塗層、聚合物-硫塗層、硫塗層及其他塗層技術)、作物類型(田間作物、園藝作物、草坪草和觀賞作物)以及地區(加拿大、墨西哥、美國、北美及其他地區)進行細分。市場預測以價值(美元)和數量(公噸)表示。

北美緩釋肥料市場趨勢與洞察

引進精密農業及施肥灌溉

由於商業農場擴大採用變數施肥(VAT)和綜合養分管理技術,北美緩效肥料市場正在成長。在美國,變數施肥技術已廣泛應用於農田,這表明許多生產者已經在使用需要精準施肥的系統。這種方法減少了施肥次數,從而降低了田間成本。同樣,加拿大農場也採用了變數施肥技術,而緩釋肥料的使用已經為進一步推廣奠定了堅實的技術基礎。一次施用緩效肥料即可滿足特定區域的養分需求,無需多次田間作業。在勞動力持續短缺和農業機械擁有成本高昂的背景下,能夠提高作業效率並保持農藥有效性的解決方案為北美緩釋肥料市場提供了支撐。

關於營養物質徑流的監管壓力

北美緩效肥市場也受惠於更嚴格的營養物徑流和水質法規結構。美國環保署 (EPA) 持續支持水質惡化流域的營養物減量工作。其中包括2025年6月宣布的一項370萬美元的津貼計劃,用於資助在伊利湖西部流域開展工作的密西根州和俄亥俄州機構。這種流域層面的支持表明,營養物管理正成為更廣泛的水質改善行動計畫的重要組成部分,尤其是在那些特別脆弱或正在經歷水質劣化的流域。加拿大也提供了類似的政策支援;例如,魁北克省正在透過其永續農業舉措實施一項計劃,以支持聚合物包膜尿素的推廣應用。這些監管和政策趨勢將繼續進一步增強北美對緩效性肥料的長期需求。

與傳統肥料相比的價格差異

北美緩釋肥市場最明顯的商業性障礙仍然是包膜產品相對於傳統氮肥更高的成本。這種價格差異既反映了包膜成本,也反映了為實現更可預測的養分釋放而增加的生產過程複雜性。對於大規模糧食農場,尤其是那些採用低利潤種植系統的農場而言,採用緩釋肥的可行性往往並非取決於單季的成本節約,而是取決於能否在多個種植季獲得明確的投資回報。佛羅裡達大學食品與農業科學研究所於2025年2月發表的一項研究表明,儘管區域成本分攤計畫可以減輕負擔,但高昂的材料成本仍然是田間作物採用緩釋肥的主要障礙。在價格差距進一步縮小之前,北美緩釋肥市場將繼續在那些收益(例如養分控制、符合法規要求或節省勞動力)足以抵消初始成本差異的地區快速擴張。

細分市場分析

到2025年,聚合物包衣配方將佔據77.2%的市場佔有率,成為北美緩效肥料市場中按包衣類型分類的最大佔有率。這一主導地位反映了其在作物種植、保護性耕作和人工草坪等領域的廣泛應用,在這些領域,可預測的釋放特性比低初始投資成本更為重要。此外,該細分市場還受益於其在玉米和草坪系統中的長期商業應用,從而增強了人們對施用方法和作物反應的信心。成熟的供應鏈以及與標準混合和噴灑設備的兼容性進一步推動了其在北美緩釋肥料行業的普及。這些成功經驗使得聚合物包衣產品在種植者尋求商業規模的穩定性時,比硫基肥料和一些特殊用途的包衣產品更具優勢。

聚合物包衣配方是成長最快的包衣類型,預計2026年至2031年將以8.1%的複合年成長率成長,顯示該技術不僅沒有失去發展勢頭,反而持續獲得支持。 2025年,Parcel 農業技術和Wastek集團簽署了一項合資協議,將在馬來西亞建立一座用於緩釋肥料的聚合物包衣工廠。據報道,該項目投資超過8,000萬馬幣(約1,800萬美元)。該工廠預計將利用Parcel的包衣技術服務於東南亞市場。聚合物硫包衣產品和硫包衣產品在成本敏感市場中繼續發揮重要作用,因為它們提供了一種低成本的提高利用效率的方法。其他包衣技術在某些細分市場仍然很重要,但它們在北美緩效肥料市場的核心規模和成長趨勢方面仍無法與聚合物包衣相提並論。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章:主要產業趨勢

- 主要農作物種植面積

- 田間作物

- 園藝作物

- 草坪和觀賞植物

- 平均施肥量

- 主要營養素

- 田間作物

- 園藝作物

- 草坪和觀賞植物

- 主要營養素

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 引進精密農業及施肥灌溉

- 遵守有關營養物徑流法規的壓力

- 田間作物氮肥利用效率的需求

- 擴大保護性栽培

- 在美國農業部的支持下,擴大國內生產能力

- 生物分解塗料的創新

- 市場限制因素

- 與傳統肥料相比的價格差異

- 經銷商和生產商之間在應用方面的知識差距

- 聚合物殼中微塑膠的詳細檢測

- 原物料價格波動劇烈

第5章 市場規模與成長預測

- 按塗層類型

- 聚合物塗層

- 聚氨酯和樹脂塗料

- 可生物分解聚合物塗層

- 聚合物硫塗層

- 硫塗層

- 其他塗層技術

- 聚合物塗層

- 作物處理

- 田間作物

- 穀類和穀類食品

- 油籽/豆類

- 棉花和其他纖維作物

- 園藝作物

- 水果

- 蔬菜

- 果樹和葡萄藤

- 草坪和觀賞植物

- 高爾夫球場和運動草坪

- 專業庭園綠化

- 溫室中種植的幼苗與觀賞植物

- 田間作物

- 按地區

- 加拿大

- 墨西哥

- 美國

- 其他北美國家

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介

- Nutrien Ltd.

- ICL Group Ltd.

- Koch Industries Inc.

- Haifa Group

- Grupa Azoty SA(Compo Expert)

- Yara International ASA

- Profile Products LLC

- The Andersons, Inc.

- JR Simplot Company

- Pursell Agri-Tech, LLC

- EuroChem Group AG

- New Mountain Capital(Florikan)

- The Scotts Miracle-Gro Company

- Helena Agri-Enterprises, LLC(Marubeni Corporation)

- Timac Agro USA, Inc.(Groupe Roullier)

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america controlled release fertilizer market size is projected to expand from USD 612.54 million in 2025 and USD 661.60 million in 2026 to USD 972.56 million by 2031, registering a CAGR of 8.01% between 2026 to 2031.

This report is Segmented by Coating Type (Polymer Coated, Polymer-Sulfur Coated, Sulfur Coated, and Other Coated Technologies), Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and Geography (Canada, Mexico, United States, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

North America Controlled Release Fertilizers Market Trends and Insights

Precision Agriculture and Fertigation Adoption

The North America controlled release fertilizer market is growing due to the increased use of variable-rate technology and integrated nutrient management practices on commercial farms. In the United States, variable-rate technology is extensively applied to cropland, highlighting that many growers already operate within systems requiring precise nutrient placement. This approach reduces the number of fertilizer applications, thereby lowering field costs. Similarly, Canadian farms have adopted variable-rate input application and are already utilizing slow-release fertilizers, demonstrating a strong technical foundation for the wider adoption of controlled release fertilizers. A single application of controlled release fertilizer can align with zone-based nutrient prescriptions, reducing the need for multiple field passes. With ongoing labor shortages and high equipment ownership costs, the North America controlled release fertilizer market is supported by solutions that enhance operational efficiency while maintaining agronomic effectiveness.

Nutrient-Runoff Compliance Pressure

The North America controlled release fertilizer market is also supported by a more stringent regulatory framework for nutrient runoff and water quality. The United States Environmental Protection Agency has continued to support nutrient-reduction efforts in impaired watersheds. This includes a USD 3.7 million grant package announced for June 2025, aimed at organizations in Michigan and Ohio working within the Western Lake Erie Basin. This type of basin-level support demonstrates how nutrient management is becoming an integral part of broader water-quality action plans, particularly in sensitive or impaired watersheds. Similar policy support exists in Canada, including Quebec programs that support the adoption of polymer-coated urea through sustainable agriculture initiatives. These regulatory and policy developments continue strengthening long-term demand for controlled release fertilizers across North America.

Premium Price Versus Conventional Fertilizers

The clearest commercial barrier in the North America controlled release fertilizer market remains the price premium of coated products over conventional nitrogen materials. That premium reflects both coating cost and the added manufacturing complexity needed to deliver more predictable nutrient release. For large grain farms, especially in lower-margin cropping systems, the decision often depends on whether the product can show a clear multi-season return rather than a one-season saving. A University of Florida Institute of Food and Agricultural Sciences study published in February 2025 identified high material costs as the main barrier to wider field-crop use, even though local cost-share programs can soften the burden in some cases. Until price gaps narrow further, the North America controlled release fertilizer market will continue to expand fastest where nutrient control, compliance, or labor savings are valuable enough to offset the initial cost difference.

Other drivers and restraints analyzed in the detailed report include:

- Field-Crop Nitrogen-Use Efficiency Needs

- Protected Horticulture Expansion

- Dealer And Grower Application-Learning Gap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer-coated formulations held 77.2% market share in 2025, giving them the largest share in the North America controlled release fertilizer market by coating type. That lead reflects broad acceptance across row crops, protected horticulture, and managed turf, where predictable release behavior is valued more than the lowest upfront input cost. The segment has also benefited from long commercial use in corn and turf systems, which has built confidence around application methods and crop response. Mature supply chains and compatibility with standard blending and spreading equipment have further strengthened adoption across the North America controlled release fertilizer industry. This installed base gives polymer-coated products a clear advantage over sulfur-based and niche coating alternatives when growers want consistency at a commercial scale.

Polymer-coated formulations are the fastest-growing coating type, with a CAGR of 8.1% projected from 2026 to 2031, demonstrating that this technology continues to gain traction rather than losing momentum. Pursell Agri-Tech and Wastech Group entered into a joint venture agreement in 2025 to establish a controlled release fertilizer polymer coating facility in Malaysia. The reported capital expenditure for the project exceeded RM80 million (approximately USD18 million). This facility is projected to serve Southeast Asian markets utilizing Pursell's coating technology. Polymer-sulfur coated and sulfur coated products still matter in more cost-sensitive settings because they provide a lower-cost path into enhanced efficiency use. Other coated technologies remain relevant in specialty niches, but they do not yet challenge the scale or growth profile of the polymer coated core within the North America controlled release fertilizer market.

List of Companies Covered in this Report:

- Nutrien Ltd.

- ICL Group Ltd.

- Koch Industries Inc.

- Haifa Group

- Grupa Azoty S.A. (Compo Expert)

- Yara International ASA

- Profile Products LLC

- The Andersons, Inc.

- J.R. Simplot Company

- Pursell Agri-Tech, LLC

- EuroChem Group AG

- New Mountain Capital (Florikan)

- The Scotts Miracle-Gro Company

- Helena Agri-Enterprises, LLC (Marubeni Corporation)

- Timac Agro USA, Inc. (Groupe Roullier)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Key Industry Trends

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.1.3 Turf and Ornamental

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1.3 Turf and Ornamental

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Precision agriculture and fertigation adoption

- 4.5.2 Nutrient-runoff compliance pressure

- 4.5.3 Field-crop nitrogen-use efficiency needs

- 4.5.4 Protected horticulture expansion

- 4.5.5 United States Department of Agriculture backed domestic capacity build

- 4.5.6 Biodegradable coating innovation

- 4.6 Market Restraints

- 4.6.1 Premium price versus conventional fertilizers

- 4.6.2 Dealer and grower application-learning gap

- 4.6.3 Microplastic scrutiny of polymer shells

- 4.6.4 Highly cyclical raw-material prices

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.1.1 Polyurethane and resin-coated

- 5.1.1.2 Biodegradable polymer-coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Sulfur Coated

- 5.1.4 Other Coated Technologies

- 5.1.1 Polymer Coated

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.1.1 Cereals and Grains

- 5.2.1.2 Oilseeds and Pulses

- 5.2.1.3 Cotton and Other Fiber Crops

- 5.2.2 Horticultural Crops

- 5.2.2.1 Fruits

- 5.2.2.2 Vegetables

- 5.2.2.3 Orchard and Vineyard Crops

- 5.2.3 Turf and Ornamental

- 5.2.3.1 Golf and Sports Turf

- 5.2.3.2 Professional Landscaping

- 5.2.3.3 Nursery and Greenhouse Ornamentals

- 5.2.1 Field Crops

- 5.3 Geography

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 Competitive Landscape

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Nutrien Ltd.

- 6.4.2 ICL Group Ltd.

- 6.4.3 Koch Industries Inc.

- 6.4.4 Haifa Group

- 6.4.5 Grupa Azoty S.A. (Compo Expert)

- 6.4.6 Yara International ASA

- 6.4.7 Profile Products LLC

- 6.4.8 The Andersons, Inc.

- 6.4.9 J.R. Simplot Company

- 6.4.10 Pursell Agri-Tech, LLC

- 6.4.11 EuroChem Group AG

- 6.4.12 New Mountain Capital (Florikan)

- 6.4.13 The Scotts Miracle-Gro Company

- 6.4.14 Helena Agri-Enterprises, LLC (Marubeni Corporation)

- 6.4.15 Timac Agro USA, Inc. (Groupe Roullier)

7 Market Opportunities and Future Outlook

2026 年至 2035 年緩釋肥料市場的商業機會、成長要素、產業趨勢與預測。

2026 年至 2035 年緩釋肥料市場的商業機會、成長要素、產業趨勢與預測。 全球種子與肥料處理市場(2025-2032 年)

全球種子與肥料處理市場(2025-2032 年) 控釋肥料(CRF):市佔率分析、產業趨勢與統計、成長預測(2026-2031)

控釋肥料(CRF):市佔率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球緩釋肥料市場報告控釋肥料市場-2026-2031年預測

2026年全球緩釋肥料市場報告控釋肥料市場-2026-2031年預測 非農業用控制釋放肥料顆粒市場(依配方類型、養分機制、成分、應用、最終用戶和通路分類),全球預測(2026-2032年)

非農業用控制釋放肥料顆粒市場(依配方類型、養分機制、成分、應用、最終用戶和通路分類),全球預測(2026-2032年) 緩釋性肥料市場規模、佔有率及成長分析(按類型、應用方法、最終用途及地區分類)-2026-2033年產業預測

緩釋性肥料市場規模、佔有率及成長分析(按類型、應用方法、最終用途及地區分類)-2026-2033年產業預測 控釋肥料市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用途、應用方式、地區和競爭格局分類,2020-2030年預測

控釋肥料市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用途、應用方式、地區和競爭格局分類,2020-2030年預測 全球控釋肥料(CRF)市場按類型、功能、產品等級、應用方法、最終用途和地區分類-預測至2030年包衣肥料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、作物類型、地區和競爭情況分類,2020-2030 年)

全球控釋肥料(CRF)市場按類型、功能、產品等級、應用方法、最終用途和地區分類-預測至2030年包衣肥料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、作物類型、地區和競爭情況分類,2020-2030 年)