|

市場調查報告書

商品編碼

2073598

中國緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Controlled Release Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

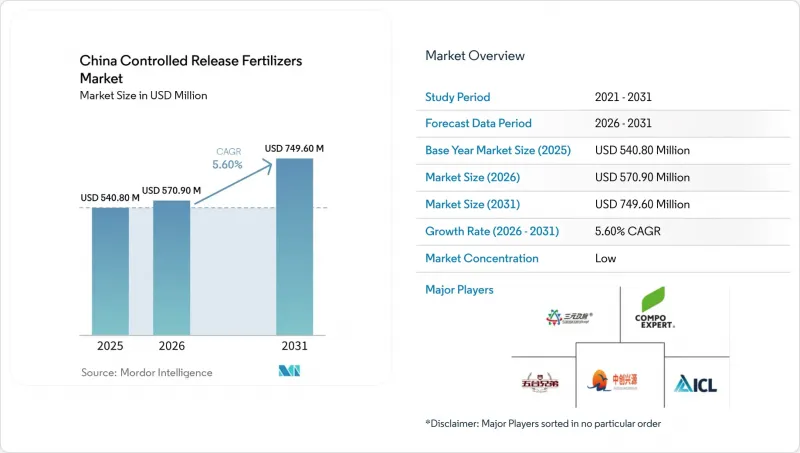

據 Mordor Intelligence 稱,2025 年中國緩釋肥料市場價值為 5.408 億美元,預計在預測期(2026-2031 年)內將以 5.60% 的複合年成長率成長,從 2026 年的 5.709 億美元成長到 2031 年的 7.496 億美元。

本報告按塗料類型(聚合物塗料、聚合物硫塗料及其他)和作物類型(田間作物、園藝作物和草坪/觀賞作物)進行細分。市場預測以價值(美元)和數量(公噸)表示。

中國緩釋肥料市場趨勢與洞察

政府對高效肥料的生態補貼

在農業農村部「2025+」架構下,中央政府的補貼計畫為獲得認證的生態農場提供緩釋肥成本30%的補貼。這為縮小緩釋肥與傳統肥料的價格差距提供了直接的經濟獎勵。這項政策干預措施不僅解決了推廣應用的主要障礙,也有助於推動中國農業永續性目標的實現。該補貼計畫由各省農業廳負責實施,江蘇省於2024年主導實施,涵蓋超過200萬畝稻田。該計劃將於2025年推廣至其他省份,產生綜效。早期採用該計畫的農戶產量提高了5-6%,這鼓勵了鄰近農戶效仿。 「綠色食品」認證體系的合規要求確保了獲得補貼的農民維持養分利用效率標準,從而形成推廣永續農業實踐的良性循環。

人事費用上升正在推動機械化和低勞動強度施肥方法的採用。

在農業大區,由於農業勞動成本超過每天180元人民幣(約25美元),生產者被迫採用機械化、低維護成本的施肥系統。使用緩釋肥可以將傳統的每季3-4次施肥頻率降低到每季1次。勞動成本的降低使得緩釋肥(CRF)的應用極具經濟吸引力,尤其是在水稻和玉米生產系統中,人工施肥佔總生產成本的15-20%。這一趨勢在中國東北地區的大規模農業生產中最為顯著。與傳統的分段施肥相比,採用緩釋肥的機械化插秧系統可降低25%的人事費用。隨著農村人口持續向城市遷移,這一趨勢正在加速發展,農業勞動力數量每年減少3%,而剩餘勞動力的工資卻在不斷上漲。像雷沃(Lovol)和中聯重科(Zoomlion)這樣的智慧施肥設備製造商正在將兼容緩釋肥的系統整合到他們的機器中,從而形成技術鎖定效應,並維持市場需求的成長。

與傳統散裝NPK肥料相比,價格差異顯著。

緩釋肥的價格是傳統散裝複合肥(NPK)的兩到三倍,這給利潤率低於收入10%且缺乏農業貸款購買昂貴農資的小規模農戶造成了購買障礙。在農產品價格下跌、農民優先考慮降低成本而非提高效率的情況下,這種價格差異尤其顯著。中國有2億小規模農戶,平均每戶耕地面積僅0.6公頃,除非能證明產量增加15%以上,否則很難證明緩釋肥(CRF)的高價合理。價格敏感度因地區而異,中國中部和西南地區的價格抵觸情緒最為強烈,這些地區的農作物價值較低,機械化程度也較低。化肥合作社和集中採購計畫雖然能提供部分解決方案,但僅涵蓋了30%的符合條件的農戶,阻礙了價格敏感型農戶的市場滲透。

細分市場分析

聚合物包膜性肥料肥料在中國緩釋肥料市場佔據主導地位,預計2025年將佔約72.4%的市場。此細分市場的主導地位源自於其卓越的養分釋放調控能力,可透過包膜特性、厚度和材料配比等方式,根據不同作物的特定需求進行客製化。其中,聚合物包膜尿素肥料正迅速成為領先產品,尤其因其氮肥利用率高、可減少30%至40%的氮肥用量而備受青睞。

預計到2031年,聚合物包衣硫磺產品將成為成長最快的包衣類型,年複合成長率(CAGR)將達到6.2%。這一成長主要得益於包覆成本低廉,以及其能夠為大面積農田種植的作物提供持續的養分釋放。此外,由於園藝和觀賞作物對養分釋放的精準要求和環境因素的考量日益嚴格,聚合物包膜性肥料也保持著強勁的市場地位。包衣技術和材料的進步使生產商能夠在兼顧環境永續性的同時最佳化產量,市場也因此持續擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 主要農作物種植面積

- 大田作物

- 園藝作物

- 平均施肥量

- 主要營養素

- 田間作物

- 園藝作物

- 主要營養素

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 政府對高效肥料的生態補貼

- 人事費用上升推動了機械化和低接觸式營養管理的發展。

- 加強營養物徑流監管後

- 對能夠確保養分穩定釋放的智慧施肥系統的需求日益成長。

- 評估氮利用效率的排碳權試點項目

- 電子商務平台擴大農村產品取得管道

- 市場限制因素

- 與傳統散裝NPK肥料相比,價格差異顯著。

- 缺乏針對特種塗料的公共研發資金

- 正在考慮的有關微塑膠塗層的法律法規

- 聚合物原料價格波動

第5章 市場規模與成長預測

- 塗層類型

- 聚合物塗層

- 聚合物硫塗層

- 其他

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介。

- Hebei Woze Wufeng Biological Technology Co., Ltd

- Grupa Azoty SA(Compo Expert)

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- Zhongchuang xingyuan chemical technology co.ltd

- Kingenta Ecological Engineering Group Co., Ltd.

- Sinochem Holdings Corporation Ltd.

- Xinyangfeng Agricultural Technology Co., Ltd.

- Stanley Agriculture Group Co., Ltd.

- Haifa Group

- Luxi Chemical Group Co., Ltd.

- Shikefeng Chemical Industry Co., Ltd.

- ICL Group Ltd.

- Zhongchuang Xingyuan Chemical Technology Co., Ltd.

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the china controlled release fertilizers market size was valued at USD 540.80 million in 2025 and is estimated to grow from USD 570.90 million in 2026 to USD 749.60 million by 2031, at a CAGR of 5.60% during the forecast period (2026-2031).

This report is Segmented by Coating Type (Polymer Coated, Polymer-Sulfur Coated, and Others) and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons)

China Controlled Release Fertilizers Market Trends and Insights

Government Eco-Subsidies for Efficiency Fertilizers

Central government subsidies under the Ministry of Agriculture and Rural Affairs' 2025+ framework reimburse 30% of controlled-release fertilizer costs for certified eco-farms, creating a direct economic incentive that narrows the price gap with conventional fertilizers. This policy intervention addresses the primary adoption barrier while advancing China's agricultural sustainability objectives. The subsidy mechanism operates through provincial agricultural bureaus, with Jiangsu Province leading implementation by covering over 2 million mu of rice paddies in 2024. The program's expansion to additional provinces in 2025 creates a multiplier effect where early adopters demonstrate yield improvements of 5-6%, encouraging neighboring farms to transition. Compliance requirements under the Green Food certification system ensure that subsidized farms maintain nutrient use efficiency standards, creating a self-reinforcing cycle of sustainable practices adoption.

Rising Labor Costs Driving Mechanized, Low-Touch Nutrition

Agricultural labor costs exceeding CNY 180 per day (USD 25) in major farming regions force growers to adopt mechanized, low-maintenance fertilization regimes where controlled-release products reduce application frequency from 3-4 times to once per season. This labor arbitrage creates compelling economics for CRF adoption, particularly in rice and corn production systems where manual broadcasting represents 15-20% of total production costs. Northeast China's large-scale farming operations demonstrate the clearest adoption patterns, with mechanized transplanting systems incorporating slow-release fertilizers achieving 25% labor cost reductions compared to conventional split applications. The trend accelerates as rural-urban migration continues, with agricultural employment declining 3% annually while remaining workers command premium wages. Smart application equipment manufacturers like Lovol and Zoomlion integrate CRF-compatible systems into their machinery offerings, creating technology lock-in effects that sustain demand growth.

Premium Price Gap Versus Conventional Bulk NPK

Controlled-release fertilizers command 2-3 times the price of conventional bulk NPK, creating affordability barriers for smallholder farmers who operate on margins below 10% of revenue and lack access to agricultural credit for premium inputs. This price differential becomes particularly constraining during commodity price downturns when farmers prioritize cost reduction over efficiency gains. China's 200 million smallholder farming households, averaging 0.6 hectares per operation, struggle to justify CRF premiums without demonstrated yield improvements exceeding 15% . Regional price sensitivity varies significantly, with Central and Southwest China showing the highest resistance due to lower crop values and limited mechanization. Fertilizer cooperatives and bulk purchasing programs provide partial solutions, but coverage remains limited to 30% of eligible farms, constraining market penetration in price-sensitive segments.

Other drivers and restraints analyzed in the detailed report include:

- Tighter Nutrient-Runoff Regulations

- Smart-Fertigation Demand for Steady Nutrient Release

- Polymer-Feedstock Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The polymer-coated fertilizer segment dominates the Chinese controlled-release fertilizer market, commanding about 72.4% market share in 2025. This segment's prominence stems from its superior ability to regulate nutrient release through tailored coating characteristics, thickness, and material ratios aligned with specific crop needs. Within this category, polymer-coated urea fertilizer has emerged as the leading variant, particularly valued for its nitrogen efficiency and potential to reduce nitrogen fertilizer use by 30% to 40%.

Polymer sulfur-coated products are projected to be the fastest-growing coating type, with a projected CAGR of 6.2% through 2031. This growth is driven by lower coating costs and the ability to provide extended nutrient release for broad-acre crops. Additionally, polymer-coated fertilizers maintain a strong market position due to increasing adoption in horticultural and ornamental crops, where precise nutrient-release requirements and environmental considerations are essential. Advancements in coating technologies and materials continue to enhance the market by enabling manufacturers to optimize yields while addressing environmental sustainability.

Complete Report Scope:

- Coating Type

- Polymer Coated

- Polymer-Sulfur Coated

- Others

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

List of Companies Covered in this Report:

- Hebei Woze Wufeng Biological Technology Co., Ltd

- Grupa Azoty S.A. (Compo Expert)

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- Zhongchuang xingyuan chemical technology co.ltd

- Kingenta Ecological Engineering Group Co., Ltd.

- Sinochem Holdings Corporation Ltd.

- Xinyangfeng Agricultural Technology Co., Ltd.

- Stanley Agriculture Group Co., Ltd.

- Haifa Group

- Luxi Chemical Group Co., Ltd.

- Shikefeng Chemical Industry Co., Ltd.

- ICL Group Ltd.

- Zhongchuang Xingyuan Chemical Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Government eco-subsidies for efficiency fertilizers

- 4.5.2 Rising labor costs driving mechanized, low-touch nutrition

- 4.5.3 Tighter nutrient-runoff regulations post

- 4.5.4 Smart-fertigation demand for steady nutrient release

- 4.5.5 Carbon-credit pilots rewarding nitrogen-use efficiency

- 4.5.6 E-commerce platforms expanding rural product access

- 4.6 Market Restraints

- 4.6.1 Premium price gap versus conventional bulk NPK

- 4.6.2 Limited public R&D funding for specialty coatings

- 4.6.3 Pending micro-plastic coating legislation

- 4.6.4 Polymer-feedstock price volatility

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Hebei Woze Wufeng Biological Technology Co., Ltd

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.4 Zhongchuang xingyuan chemical technology co.ltd

- 6.4.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.6 Sinochem Holdings Corporation Ltd.

- 6.4.7 Xinyangfeng Agricultural Technology Co., Ltd.

- 6.4.8 Stanley Agriculture Group Co., Ltd.

- 6.4.9 Haifa Group

- 6.4.10 Luxi Chemical Group Co., Ltd.

- 6.4.11 Shikefeng Chemical Industry Co., Ltd.

- 6.4.12 ICL Group Ltd.

- 6.4.13 Zhongchuang Xingyuan Chemical Technology Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

北美緩釋肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美緩釋肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 2026 年至 2035 年緩釋肥料市場的商業機會、成長要素、產業趨勢與預測。

2026 年至 2035 年緩釋肥料市場的商業機會、成長要素、產業趨勢與預測。 全球種子與肥料處理市場(2025-2032 年)控釋肥料(CRF):市佔率分析、產業趨勢與統計、成長預測(2026-2031)

全球種子與肥料處理市場(2025-2032 年)控釋肥料(CRF):市佔率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球緩釋肥料市場報告控釋肥料市場-2026-2031年預測

2026年全球緩釋肥料市場報告控釋肥料市場-2026-2031年預測 非農業用控制釋放肥料顆粒市場(依配方類型、養分機制、成分、應用、最終用戶和通路分類),全球預測(2026-2032年)

非農業用控制釋放肥料顆粒市場(依配方類型、養分機制、成分、應用、最終用戶和通路分類),全球預測(2026-2032年) 緩釋性肥料市場規模、佔有率及成長分析(按類型、應用方法、最終用途及地區分類)-2026-2033年產業預測

緩釋性肥料市場規模、佔有率及成長分析(按類型、應用方法、最終用途及地區分類)-2026-2033年產業預測 控釋肥料市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用途、應用方式、地區和競爭格局分類,2020-2030年預測

控釋肥料市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用途、應用方式、地區和競爭格局分類,2020-2030年預測 全球控釋肥料(CRF)市場按類型、功能、產品等級、應用方法、最終用途和地區分類-預測至2030年

全球控釋肥料(CRF)市場按類型、功能、產品等級、應用方法、最終用途和地區分類-預測至2030年