|

市場調查報告書

商品編碼

2045745

2026 年至 2035 年緩釋肥料市場的商業機會、成長要素、產業趨勢與預測。Controlled Release Fertilizers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

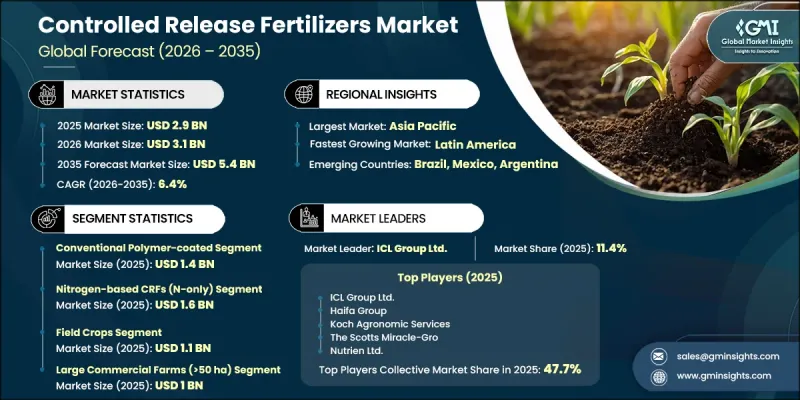

2025年全球緩釋肥料市場價值為29億美元,預計到2035年將以6.4%的複合年成長率成長至54億美元。

緩釋肥(CRF)是一種專門設計的營養劑,旨在長期緩慢地為作物提供必需的營養。與施用後立即釋放營養的傳統肥料不同,緩釋肥的釋放速度受控,並受土壤溫度、水分含量和微生物活性等因素的影響。這種可控制的營養釋放方式提高了作物整個生長週期內營養的利用效率,同時促進作物穩定生長。人們對永續農業、精密農業和高效營養利用的日益關注,進一步推動了市場需求。農民和商業種植者擴大採用緩釋肥,以提高作物產量,同時減少因淋溶、徑流和揮發造成的營養損失。人們對土壤劣化、水資源保護和環境永續性的日益關注,也促使這些產品在全球農業系統中得到更廣泛的應用。緩釋肥廣泛應用於農業、園藝、景觀美化和草坪管理等領域,在這些領域,維持土壤長期肥力和穩定的植物營養至關重要。包膜技術和營養輸送系統的進步進一步提高了肥料效率,使種植者能夠過渡到先進的作物營養解決方案,從而支持更高的產量和改進的土壤管理技術。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 29億美元 |

| 預計金額 | 54億美元 |

| 複合年成長率 | 6.4% |

緩釋肥料採用先進的包膜技術生產,能夠減緩養分的溶解速度,進而為作物提供持續穩定的養分供應。由於緩效肥料能夠在整個生長季節維持養分平衡,有助於改善植物健康狀況並提高整體農業生產力,因此越來越受到生長週期長作物的青睞。農民對高效施肥和永續耕作方式的認知不斷提高,正在加速已開發和新興農業經濟體對這類產品的需求。此外,日益嚴格的養分流失和環境保護監管壓力也推動了能夠提高養分吸收效率並減少對生態系統影響的肥料的應用。對精密農業技術和注重資源最佳化及長期土壤生產力的現代耕作方法的投資增加,也促進了市場的發展。隨著農業管理不斷努力在最大限度提高作物產量的同時最大限度地減少對環境的影響,緩釋肥料預計將繼續成為現代養分管理策略中的關鍵要素。

預計2025年,傳統聚合物包膜肥料市場規模將達14億美元。由於此類產品在廣泛的農業應用中都能提供可預測的養分釋放模式和可靠的作物產量,因此市場對傳統聚合物包膜肥料的需求仍然強勁。它們能夠長期保持養分穩定性,使其成為商業農業和大規模作物生產的理想選擇。同時,硫包膜肥料因其成本效益和雙重養分供應的優勢而日益受到關注。這些產品不僅能夠持續釋放養分,還能提供植物生長和土壤健康所必需的硫元素。預計大規模田間作物種植和商業農業中硫包膜肥料的廣泛應用將進一步推動該市場的成長。

預計2025年,氮基緩釋肥料市場規模將達16億美元。由於氮在促進植物生長、提高葉綠素產量和支持作物整體發育方面發揮著至關重要的作用,因此對這類肥料的需求仍然強勁。農民越來越傾向於使用氮基緩釋產品,因為它們能夠提高氮肥利用率,同時最大限度地減少養分浪費。此外,均衡營養配方,例如NPK緩釋肥料,在各種種植系統和土壤條件下也越來越受到關注。這些配方提供更全面的養分,有助於改善作物生長和長期土壤肥力管理。預計在預測期內,對能夠支持精密農業和永續作物生產實踐的高效肥料的需求不斷成長,將進一步推動氮基和多營養素緩釋肥料產品的普及應用。

預計北美緩釋肥市場規模將從2025年的5.683億美元成長到2035年的10億美元。該地區的需求成長主要得益於大規模商業農業的快速發展以及對先進養分管理策略日益成長的關注。北美農民優先選擇能夠提高養分利用效率並同時符合徑流預防和土壤保護等環境法規的肥料技術。在美國,精密農業技術的日益普及和對現代農業材料的投資增加正在加速市場成長。由於緩釋肥能夠穩定作物養分供應並提高營運效率,因此在特種作物、草坪管理、景觀美化和溫室種植等領域的應用也日益廣泛。人們對永續農業實踐的日益重視以及確保土壤長期生產力的需求預計將在整個預測期內持續推動區域市場擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章:行業洞察

- 工業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 人們對高效率利用養分的農業越來越感興趣。

- 擴大精密農業的全球實踐

- 較長的種植週期需要持續的養分供應。

- 產業潛在風險與挑戰

- 與傳統肥料相比,其初始成本較高。

- 發展中農業地區農業工人的意識程度較低

- 市場機遇

- 對永續土壤養分管理的需求日益成長

- 全球園藝和草坪用途的擴展

- 生物分解塗層材料技術的進步

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 技術與創新展望

- 最新科技趨勢

- 新技術

- 價格趨勢

- 按地區

- 按營養成分

- 未來市場趨勢

- 專利趨勢

- 貿易統計

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續發展計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依塗層技術分類,2022-2035年

- 硫基塗料

- 傳統聚合物塗層

- 可生物分解聚合物塗層

- 其他包膜和封裝肥料

第6章 市場估計與預測:依營養成分分類,2022-2035年

- 氮基緩釋肥(僅含氮)

- 磷基 CRF(僅含磷)

- 鉀基CRF(僅含鉀)

- NPK 混合物(多營養素 CRF)

- 特殊微量營養素 CRF

第7章 市場估計與預測:依作物類型分類,2022-2035年

- 田間作物

- 特色作物和種植作物

- 柑橘類水果和亞熱帶水果

- 園藝-蔬菜和溫帶水果

- 園藝-幼苗和花卉栽培

- 草坪和景觀美化

- 其他

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 大型商業農場(超過50公頃)

- 專業人士/組織

- 中型商業農場(10-50公頃)

- 小規模農戶和合作社(10公頃或以下)

- 其他

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷(從製造商到最終用戶)

- 銷售代理和化工公司

- 特種化學品供應商

- 線上平台

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲國家

第11章:公司簡介

- ICL Group Ltd.

- Haifa Group

- Koch Agronomic Services

- The Scotts Miracle-Gro

- Nutrien Ltd.

- Yara International ASA

- The Mosaic Company

- Kingenta Ecological Engineering

- COMPO EXPERT GmbH

- SQM

The Global Controlled Release Fertilizers Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 5.4 billion by 2035.

Controlled release fertilizers are specialized nutrient formulations designed to supply crops with essential nutrients gradually over an extended period. Unlike conventional fertilizers that release nutrients immediately after application, these products deliver nutrients at a controlled pace influenced by factors such as temperature, moisture levels, and microbial activity in the soil. This regulated nutrient distribution supports consistent crop development while improving nutrient availability throughout the plant growth cycle. The increasing emphasis on sustainable agriculture, precision farming, and efficient nutrient utilization continues to strengthen market demand. Farmers and commercial growers are increasingly adopting these fertilizers to reduce nutrient losses caused by leaching, runoff, and volatilization while enhancing crop productivity. Rising concerns regarding soil degradation, water conservation, and environmental sustainability are also contributing to broader product adoption across global agricultural systems. Controlled release fertilizers are widely utilized in agriculture, horticulture, landscaping, and turf management where maintaining long-term soil fertility and stable plant nutrition remains essential. Advancements in coating technologies and nutrient delivery systems are further improving fertilizer efficiency, encouraging growers to transition toward advanced crop nutrition solutions that support higher yields and improved soil management practices.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 6.4% |

Controlled release fertilizers are manufactured using advanced coating technologies that slow nutrient dissolution and provide crops with a steady nutrient supply over time. These fertilizers are increasingly preferred in crops with longer growth cycles because they maintain balanced nutrient levels throughout the cultivation period, helping improve plant health and overall agricultural productivity. Growing awareness among farmers regarding efficient fertilizer application and sustainable farming methods is accelerating product demand across both developed and emerging agricultural economies. In addition, increasing regulatory pressure associated with nutrient runoff and environmental protection is encouraging the adoption of fertilizers that improve nutrient absorption efficiency while reducing ecological impact. The market is also benefiting from rising investments in precision agriculture technologies and modern farming techniques that prioritize resource optimization and long-term soil productivity. As agricultural operations continue to focus on maximizing crop output while minimizing environmental impact, controlled release fertilizers are expected to remain a critical component of modern nutrient management strategies.

The conventional polymer-coated segment accounted for USD 1.4 billion in 2025. Demand for traditional polymer-coated fertilizers continues to remain strong because these products provide predictable nutrient release patterns and reliable crop performance across a wide range of agricultural applications. Their ability to maintain nutrient consistency over extended periods makes them highly suitable for commercial farming operations and large-scale crop production. At the same time, sulfur-coated fertilizers are attracting growing attention due to their cost efficiency and dual nutrient delivery benefits. These products not only provide controlled nutrient release but also supply sulfur, which is essential for plant growth and soil health. Increasing adoption across large-scale field crop cultivation and commercial agriculture is expected to further support segment growth.

The nitrogen-based controlled release fertilizers segment captured USD 1.6 billion in 2025. These fertilizers continue to witness strong demand because nitrogen plays a critical role in promoting vegetative growth, improving chlorophyll production, and supporting overall crop development. Farmers increasingly prefer nitrogen-based controlled release products due to their ability to enhance nitrogen use efficiency while minimizing nutrient wastage. Additionally, balanced nutrient formulations such as NPK controlled release fertilizers are gaining greater traction across diverse cropping systems and varying soil conditions. These formulations help deliver a more comprehensive nutrient profile, enabling improved crop performance and long-term soil fertility management. Growing demand for high-efficiency fertilizers capable of supporting precision agriculture and sustainable crop production practices is expected to further drive adoption of nitrogen-based and multi-nutrient controlled release fertilizer products during the forecast period.

North America Controlled Release Fertilizers Market is projected to grow from USD 568.3 million in 2025 to USD 1 billion by 2035. Regional demand is fueled by the rapid expansion of large-scale commercial agriculture and increasing focus on advanced nutrient management strategies. Farmers across North America are prioritizing fertilizer technologies that improve nutrient efficiency while helping meet environmental regulations related to runoff control and soil conservation. In the United States, growing adoption of precision farming technologies and rising investments in modern agricultural inputs are accelerating market growth. Controlled release fertilizers are also witnessing higher utilization across specialty crops, turf care, landscaping, and greenhouse cultivation due to their ability to deliver consistent crop nutrition and improve operational efficiency. Increasing awareness regarding sustainable agricultural practices and the need for long-term soil productivity are expected to continue supporting regional market expansion throughout the forecast period.

Major companies operating in the Global Controlled Release Fertilizers Market include Nutrien Ltd., ICL Group Ltd., Koch Agronomic Services, Yara International ASA, The Mosaic Company, Haifa Group, The Scotts Miracle-Gro Company, Kingenta Ecological Engineering, COMPO EXPERT GmbH, and SQM. These industry participants are actively focusing on product innovation, expansion of production capabilities, and advanced nutrient technologies to strengthen their competitive position and expand their presence across global agricultural markets. Companies operating in the controlled release fertilizers market are increasingly adopting strategic initiatives focused on innovation, sustainability, and geographic expansion to strengthen their market position. Major manufacturers are investing heavily in research and development to introduce advanced coating technologies that improve nutrient release efficiency and reduce environmental impact. Businesses are also expanding partnerships with agricultural distributors, precision farming companies, and commercial growers to improve product accessibility and strengthen customer relationships. In addition, companies are increasing investments in sustainable fertilizer solutions that align with environmental regulations and modern farming requirements. Expanding production facilities in high-growth agricultural regions and introducing customized nutrient formulations for specific crop applications are further supporting market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Coating Technology

- 2.2.2 Nutrient Composition

- 2.2.3 Crop Type

- 2.2.4 End User

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising focus on efficient nutrient use agriculture

- 3.2.1.2 Increasing adoption of precision farming practices globally

- 3.2.1.3 Longer crop cycles requiring sustained nutrient supply

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher initial costs compared with conventional fertilizers

- 3.2.2.2 Limited farmer awareness in developing agricultural regions

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for sustainable soil nutrient management

- 3.2.3.2 Expansion of horticulture and turfgrass applications worldwide

- 3.2.3.3 Advancements in biodegradable coating material technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By nutrient composition

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Coating Technology, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Sulfur-based coatings

- 5.3 Conventional polymer-coated

- 5.4 Biodegradable polymer-coated

- 5.5 Other coated & encapsulated fertilizers

Chapter 6 Market Estimates and Forecast, By Nutrient Composition, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Nitrogen-based CRFs (N-only)

- 6.3 Phosphorus-based CRFs (P-only)

- 6.4 Potassium-based CRFs (K-only)

- 6.5 NPK blends (multi-nutrient CRFs)

- 6.6 Specialty micronutrient CRFs

Chapter 7 Market Estimates and Forecast, By Crop Type, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Field crops

- 7.3 Specialty & plantation crops

- 7.4 Citrus & subtropical fruits

- 7.5 Horticulture - vegetables & temperate fruits

- 7.6 Horticulture - nursery & floriculture

- 7.7 Turf & landscape

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End User, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Large commercial farms (>50 ha)

- 8.3 Professional/institutional

- 8.4 Mid-size commercial farms (10-50 ha)

- 8.5 Smallholder farms & cooperatives (<10 ha)

- 8.6 Other

Chapter 9 Market Estimates and Forecast, By Distribution channel, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Direct sales (manufacturer to end user)

- 9.3 Distributors & chemical traders

- 9.4 Specialty chemical suppliers

- 9.5 Online platforms

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 ICL Group Ltd.

- 11.2 Haifa Group

- 11.3 Koch Agronomic Services

- 11.4 The Scotts Miracle-Gro

- 11.5 Nutrien Ltd.

- 11.6 Yara International ASA

- 11.7 The Mosaic Company

- 11.8 Kingenta Ecological Engineering

- 11.9 COMPO EXPERT GmbH

- 11.10 SQM

北美緩釋肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美緩釋肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 全球種子與肥料處理市場(2025-2032 年)控釋肥料(CRF):市佔率分析、產業趨勢與統計、成長預測(2026-2031)

全球種子與肥料處理市場(2025-2032 年)控釋肥料(CRF):市佔率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球緩釋肥料市場報告控釋肥料市場-2026-2031年預測

2026年全球緩釋肥料市場報告控釋肥料市場-2026-2031年預測 非農業用控制釋放肥料顆粒市場(依配方類型、養分機制、成分、應用、最終用戶和通路分類),全球預測(2026-2032年)

非農業用控制釋放肥料顆粒市場(依配方類型、養分機制、成分、應用、最終用戶和通路分類),全球預測(2026-2032年) 緩釋性肥料市場規模、佔有率及成長分析(按類型、應用方法、最終用途及地區分類)-2026-2033年產業預測

緩釋性肥料市場規模、佔有率及成長分析(按類型、應用方法、最終用途及地區分類)-2026-2033年產業預測 控釋肥料市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用途、應用方式、地區和競爭格局分類,2020-2030年預測

控釋肥料市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用途、應用方式、地區和競爭格局分類,2020-2030年預測 全球控釋肥料(CRF)市場按類型、功能、產品等級、應用方法、最終用途和地區分類-預測至2030年包衣肥料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、作物類型、地區和競爭情況分類,2020-2030 年)

全球控釋肥料(CRF)市場按類型、功能、產品等級、應用方法、最終用途和地區分類-預測至2030年包衣肥料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、作物類型、地區和競爭情況分類,2020-2030 年)