|

市場調查報告書

商品編碼

2065490

歐洲GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Europe GPU Cooling Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

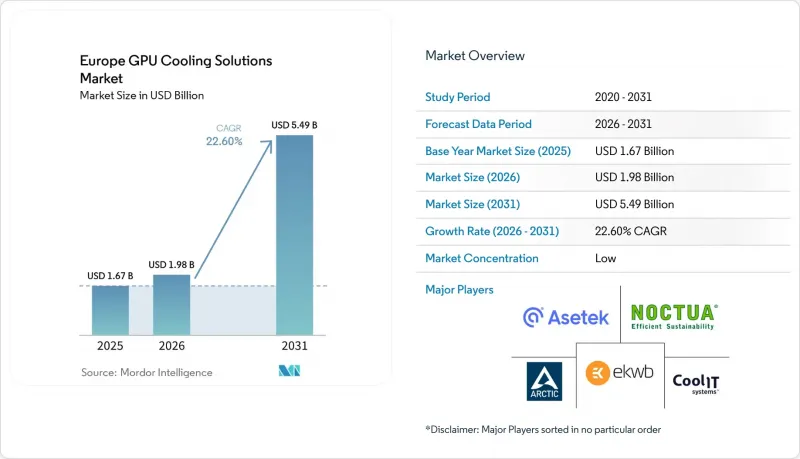

歐洲GPU散熱解決方案市場規模預計將在2025年達到16.7億美元,2026年達到19.8億美元,到2031年達到54.9億美元,2026年至2031年的複合年成長率為22.6%。

本報告按冷卻技術(風冷、液冷(晶片級)、浸沒式冷卻、混合冷卻)、冷卻等級(組件級冷卻和伺服器/機架級冷卻)、部署類型(超大規模雲端、企業級、邊緣運算)、GPU 功率密度(300W 以下、300W-700W、700W 及以上)和國家/地區進行細分。市場預測以美元 (USD) 為單位。

歐洲GPU散熱解決方案市場趨勢與洞察

人工智慧技術的加速應用正在推動GPU出貨量的成長。

歐洲GPU散熱解決方案市場正從單一GPU購買轉向機架級AI系統,這項轉變使得散熱不再只是輔助功能,而是成為核心設計選擇。 HPE與NVIDIA合作推出的下一代AI工廠產品組合,包含專為超大規模模型打造的水冷機架級系統,顯示先進的GPU部署從一開始就依賴整合式散熱設計架構。德國電信位於慕尼黑的「工業AI雲」以約1萬塊Blackwell GPU為核心,顯示歐洲自主開發的AI項目已與對高密度散熱基礎設施的即時需求緊密相連。隨著這些系統規模的擴大,OEM認證的冷板、歧管和冷卻液供應單元正成為歐洲GPU散熱解決方案市場硬體堆疊的標準組件。隨著超大規模部署的擴展,組件認證、維護和系統熟悉度將得到提升,這種標準化有望降低未來企業買家採用這些解決方案的門檻。

歐盟關於資料中心效率的指令更為嚴格。

歐洲GPU散熱解決方案市場也受到資料中心能源效率揭露法規日益嚴格的影響。能源效率指令強制要求IT設備額定功率超過500千瓦的資料中心揭露能源效率數據,而授權條例(EU) 2024/1364則制定了PUE、用水效率和熱能再利用等指標的報告架構。由於營運商需要每年報告這些指標,低效率的散熱方案將更容易被監管機構、客戶和投資者所關注。這進一步增強了採用液冷系統和混合系統的商業性合理性,尤其是在能夠將高等級廢熱貨幣化的設施中。從實際角度來看,歐洲GPU散熱解決方案市場正從中受益,因為散熱系統升級現在可以在同一投資週期內同時滿足運作性能和合規性要求。

設施維修相關的高額初始資本支出(CAPEX)。

在歐洲GPU散熱解決方案市場,營運商在嘗試將舊的風冷機房改造為液冷機房時,仍面臨巨大的成本障礙。現有設施的升級通常需要結構加固、鋪設新的管道、重新設計消防系統以及改造通道,這使得改造過程比簡單地更換設備要複雜得多。對於那些沒有大規模內部熱工程團隊或資金核准週期較長的公司而言,這種成本結構尤其具有挑戰性。因此,許多業者選擇採用後門式熱交換器或混合配置作為過渡方案,然後再逐步過渡到完整的液冷系統。儘管液冷的長期營運經濟效益更佳,但這仍減緩了歐洲GPU散熱解決方案市場的改造步伐。

細分市場分析

截至2025年,風冷佔歐洲GPU散熱解決方案市場46.8%的佔有率。這主要得益於在GPU功率密度大幅提升之前,企業和託管機房中大量風冷設備的安裝。同時,預計到2031年,浸沒式冷卻將以每年24.12%的速度成長。現有設施在歐洲GPU散熱解決方案市場仍扮演重要角色。這是因為它們維持了對風冷系統的短期需求,同時也為液冷和混合冷卻供應商創造了可預測的維修專案。然而,新的AI部署正朝著不同的方向發展。機架級GPU系統從設計初就考慮到了液冷。混合配置正成為連接這兩種現實的有效橋樑,因為它允許營運商在維護現有機房的同時,準備能夠處理更高熱負荷的新型GPU機房。

在歐洲GPU散熱解決方案市場,浸沒式冷卻技術是成長最快的技術,因為它能夠應對遠超標準風冷佈局舒適運作範圍的機架密度。這項轉變主要得益於產品層面的創新,例如Alphacool專為高密度機架環境設計的「2026 ES RTX 6000 Pro」伺服器版GPU散熱器。此外,在2026年OCP EMEA大會上,Submer與2CRSi和Eneos合作,發布了一款採用浸沒式冷卻技術的AI推理參考設計,這表明商業生態系統正進一步向浸沒式冷卻技術擴展。儘管PFAS相關冷卻劑的不確定性仍導致兩相系統採購時存在謹慎態度,但目前來看,這更有可能鞏固單相解決方案的地位,而不是阻礙歐洲GPU散熱解決方案市場向液冷技術的轉型。

2025 年歐洲 GPU 散熱解決方案市場中,伺服器和機架級散熱仍將佔據 59% 的市場佔有率,繼續成為新興 AI 基礎設施的主要採購單位。這種在歐洲 GPU 散熱解決方案市場的主導地位反映了一種「機架優先」的設計模式,即伺服器、歧管和冷卻液分配單元作為一個單一的運行包進行認證。 HPE 的液冷 NVL72 平台表明,溫度控管現在已整合到機架級採購中,而不是像過去那樣作為附加組件添加到設施中。即使底層組件來自多個供應商,這種模式也能將支出集中在機架層級。

在歐洲GPU散熱解決方案產業,組件級散熱仍然至關重要,尤其是在工作站、部門級高效能運算叢集和客製化GPU配置領域。 Alphacool於2025年推出了適用於NVIDIA RTX 5090和5080顯示卡的全新Core系列GPU液冷散熱器,進一步拓展了該產品線,也反映了市場對專用組件的持續強勁需求。展望未來,組件級散熱的需求可能會朝向低功耗和專用環境集中,而伺服器和機架級系統仍將在歐洲GPU散熱解決方案市場佔據大規模佔有率。因此,該細分市場將形成一個獨特的機架級高階產品線和一個更專業的組件級產品線。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人工智慧的加速普及正在推動GPU出貨量的成長。

- 歐盟關於資料中心效率的指令變得更加嚴格。

- 超大規模設施中液冷技術的廣泛應用

- 擴大邊緣人工智慧在 5G 微型資料中心的應用

- 創業投資對浸沒式冷卻新創企業的投入激增。

- 與區域供熱網簽訂餘熱再利用合約

- 市場限制因素

- 與設施維修相關的高額初始資本支出(CAPEX)。

- 無氟冷卻劑的供應鏈風險

- 冷凍系統維護的技術純熟勞工短缺。

- 直通式歧管標準缺乏明確性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按類型分類的冷卻技術

- 風冷,風冷

- 液冷(直接冷卻至噴嘴)

- 浸沒式冷卻

- 混合冷卻

- 冷卻程度

- 組件級冷卻

- 伺服器/機架級冷卻

- 不同的發展

- 超大規模/雲

- 公司

- 政府和研究機構(高效能運算)

- 邊緣

- 按GPU功率密度

- 小於300瓦

- 300W~700W

- 700瓦或以上

- 國家

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Asetek A/S

- CoolIT Systems Inc.

- Noctua GmbH

- EKWB doo

- Arctic GmbH

- be quiet!(Listan GmbH)

- Alphacool International GmbH

- Schneider Electric SE

- Vertiv Group Corp.

- Nvidia Corporation

- Dell Technologies Inc.

- ASUS Tek Computer Inc.

- Giga-byte Technology Co. Ltd.

- Lenovo Group Ltd.

- Hewlett Packard Enterprise Co.

- Midas Immersion Cooling SL

- Submer Technologies SL

- Asperitas BV

- Rittal GmbH and Co. KG

- LiquidStack Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe gPU cooling solutions market size is projected to be USD 1.67 billion in 2025, USD 1.98 billion in 2026, and reach USD 5.49 billion by 2031, growing at a CAGR of 22.6% from 2026 to 2031.

This report is Segmented by Cooling Technology (Air Cooling, Liquid Cooling (Direct-To-Chip), Immersion Cooling, and Hybrid Cooling), Cooling Level (Component-Level Cooling and Server / Rack-Level Cooling), Deployment (Hyperscale-Cloud, Enterprise, and Edge), GPU Power Density (Below 300W, 300W - 700W, and Above 700W), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe GPU Cooling Solutions Market Trends and Insights

Accelerated AI Adoption Driving GPU Shipments

The Europe GPU Cooling Solutions market is moving from single-GPU procurement toward rack-scale AI systems, and that shift is changing cooling from a support feature into a core design choice. HPE's next-generation AI factory portfolio with NVIDIA includes liquid-cooled rack-scale systems built for very large models, which shows how advanced GPU deployments now depend on integrated thermal architecture from launch. Deutsche Telekom's Industrial AI Cloud in Munich, built around 10,000 Blackwell GPUs, shows how sovereign AI programs in Europe are already translating into immediate demand for high-density cooling infrastructure. As these systems scale, OEM-qualified cold plates, manifolds, and coolant delivery units become standard parts of the hardware stack in the Europe GPU Cooling Solutions market. That standardization should lower adoption friction for enterprise buyers over time because component qualification, servicing, and system familiarity improve as hyperscale deployments expand.

Stricter European Union Data-Center Efficiency Directives

The Europe GPU Cooling Solutions market is also being shaped by stricter disclosure rules around data center energy performance. The Energy Efficiency Directive requires data centers above 500 kW installed IT power to make energy performance data publicly available, and Delegated Regulation (EU) 2024/1364 sets the reporting framework for indicators such as PUE, water usage effectiveness, and heat reuse. Once operators must report these metrics every year, inefficient cooling choices become more visible to regulators, customers, and investors. That creates a stronger commercial case for liquid and hybrid systems, especially in facilities that can also monetize higher-grade waste heat. In practical terms, the Europe GPU Cooling Solutions market benefits because cooling upgrades now support both operational performance and compliance needs within the same investment cycle.

High Up-Front CAPEX for Facility Retrofits

The Europe GPU Cooling Solutions market still faces a clear cost barrier when operators try to convert older air-cooled halls into liquid-ready facilities. Brownfield upgrades often require structural reinforcement, new piping routes, revised fire suppression integration, and changes to aisle design, which makes the transition more complex than a simple equipment swap. That cost profile is especially difficult for enterprise buyers that do not have large internal thermal engineering teams or long capital approval windows. As a result, many operators are using rear-door heat exchangers and hybrid configurations as intermediate steps before moving to full liquid systems. This slows the pace of conversion in the Europe GPU Cooling Solutions market, even when the long-term operating economics of liquid cooling are more favorable.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Liquid Cooling Adoption in Hyperscale Facilities

- Rising Edge-AI Deployments in 5G Micro-Data Centers

- Supply-Chain Risk for Fluorocarbon-Free Coolants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air cooling held 46.8% of the European GPU Cooling Solutions market share in 2025, supported by the large installed base of enterprise and colocation facilities built before GPU power density moved materially higher, while immersion cooling is projected to expand at the 24.12% pace through 2031. In the European GPU Cooling Solutions market, the installed base still matters because it preserves near-term demand for air systems while creating a predictable retrofit pipeline for liquid and hybrid suppliers. New greenfield AI deployments are moving in a different direction, with rack-scale GPU systems now being designed around liquid cooling from launch. Hybrid layouts are becoming the practical bridge between those two realities because they let operators protect older halls while preparing new GPU pods for higher thermal loads.

Immersion cooling is the fastest-growing technology segment in the Europe GPU Cooling Solutions market because it can manage rack densities that stretch beyond the comfortable operating range of standard air layouts. That shift is being supported by product-level innovation such as Alphacool's 2026 ES RTX 6000 Pro server-edition GPU cooler, which was engineered for dense rack environments. Submer also introduced an immersion-cooled AI inference reference design with 2CRSi and Eneos at OCP EMEA 2026, which points to a broader commercial ecosystem for immersion-based deployments. PFAS-related fluid uncertainty is still creating procurement caution for two-phase systems, but for now it is strengthening the position of single-phase solutions rather than stopping the Europe GPU Cooling Solutions market from moving toward liquid methods.

Server and rack-level cooling accounted for 59% share of the Europe GPU Cooling Solutions market size in 2025 and remained the main buying unit for new AI infrastructure. In the Europe GPU Cooling Solutions market, that dominance reflects a rack-first design model in which servers, manifolds, and coolant distribution units are qualified as one operating package. HPE's liquid-cooled NVL72 platforms show how thermal management is now embedded inside rack-scale procurement rather than added later as a facility accessory H. This keeps spending concentrated at the rack level even when the underlying parts are supplied by multiple vendors.

Component-level cooling still plays a meaningful role in the Europe GPU Cooling Solutions industry, especially in workstations, departmental HPC clusters, and custom GPU builds. Alphacool expanded that product space with new Core series GPU water coolers for NVIDIA RTX 5090 and 5080 cards in 2025, which shows that specialized component demand remains active. Over time, component-level demand is likely to narrow toward lower-power and specialized environments, while server and rack-level systems keep capturing the larger contracts in the Europe GPU Cooling Solutions market. That leaves the segment with a clear premium tier at rack scale and a more specialized tier at the component level.

List of Companies Covered in this Report:

- Asetek A/S

- CoolIT Systems Inc.

- Noctua GmbH

- EKWB d.o.o

- Arctic GmbH

- be quiet! (Listan GmbH)

- Alphacool International GmbH

- Schneider Electric SE

- Vertiv Group Corp.

- Nvidia Corporation

- Dell Technologies Inc.

- ASUS Tek Computer Inc.

- Giga-byte Technology Co. Ltd.

- Lenovo Group Ltd.

- Hewlett Packard Enterprise Co.

- Midas Immersion Cooling S.L.

- Submer Technologies S.L.

- Asperitas B.V.

- Rittal GmbH and Co. KG

- LiquidStack Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated AI Adoption Driving GPU Shipments

- 4.2.2 Stricter European Union Data-Center Efficiency Directives

- 4.2.3 Mainstream Liquid Cooling Adoption in Hyperscale Facilities

- 4.2.4 Rising Edge-AI Deployments in 5G Micro-Data Centers

- 4.2.5 Surging Venture Capital Into Immersion-Cooling Start-ups

- 4.2.6 Heat-Reuse Contracts With District Heating Networks

- 4.3 Market Restraints

- 4.3.1 High Up-Front CAPEX for Facility Retrofits

- 4.3.2 Supply-Chain Risk for Fluorocarbon-Free Coolants

- 4.3.3 Limited Skilled Labor for Coolant-System Maintenance

- 4.3.4 Uncertain Standards for Direct-to-Chip Manifolds

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cooling Technology

- 5.1.1 Air Cooling

- 5.1.2 Liquid Cooling (Direct-to-Chip)

- 5.1.3 Immersion Cooling

- 5.1.4 Hybrid Cooling

- 5.2 By Cooling Level

- 5.2.1 Component-Level Cooling

- 5.2.2 Server / Rack-Level Cooling

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.3.4 Edge

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Asetek A/S

- 6.4.2 CoolIT Systems Inc.

- 6.4.3 Noctua GmbH

- 6.4.4 EKWB d.o.o

- 6.4.5 Arctic GmbH

- 6.4.6 be quiet! (Listan GmbH)

- 6.4.7 Alphacool International GmbH

- 6.4.8 Schneider Electric SE

- 6.4.9 Vertiv Group Corp.

- 6.4.10 Nvidia Corporation

- 6.4.11 Dell Technologies Inc.

- 6.4.12 ASUS Tek Computer Inc.

- 6.4.13 Giga-byte Technology Co. Ltd.

- 6.4.14 Lenovo Group Ltd.

- 6.4.15 Hewlett Packard Enterprise Co.

- 6.4.16 Midas Immersion Cooling S.L.

- 6.4.17 Submer Technologies S.L.

- 6.4.18 Asperitas B.V.

- 6.4.19 Rittal GmbH and Co. KG

- 6.4.20 LiquidStack Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

GPU散熱解決方案:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)GPU液冷:市佔率分析、產業趨勢與統計、成長預測(2026-2031)歐洲GPU液冷:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

GPU散熱解決方案:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)GPU液冷:市佔率分析、產業趨勢與統計、成長預測(2026-2031)歐洲GPU液冷:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業及資料中心規模分類-2026-2032年全球市場預測

資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業及資料中心規模分類-2026-2032年全球市場預測 全球資料中心液冷歧管市場:按歧管類型、冷卻類型、材料類型、設計類型、資料中心類型、安裝類型和地區分類-預測至2033年

全球資料中心液冷歧管市場:按歧管類型、冷卻類型、材料類型、設計類型、資料中心類型、安裝類型和地區分類-預測至2033年 資料中心液冷市場:按組件、冷卻類型、資料中心類型、企業規模和最終用戶產業分類-市場規模、產業動態、機會分析和預測(2026-2035 年)亞太地區GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

資料中心液冷市場:按組件、冷卻類型、資料中心類型、企業規模和最終用戶產業分類-市場規模、產業動態、機會分析和預測(2026-2035 年)亞太地區GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)