|

市場調查報告書

商品編碼

2065488

北美GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)North America GPU Cooling Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

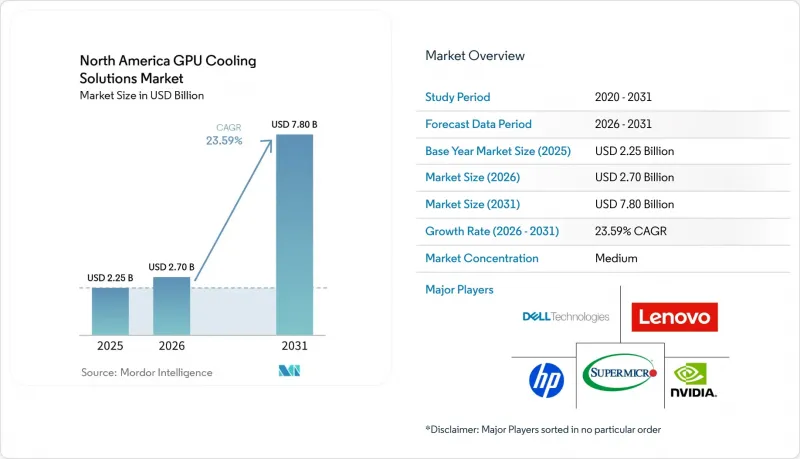

預計北美 GPU 散熱解決方案市場規模將從 2025 年的 22.5 億美元和 2026 年的 27 億美元成長到 2031 年的 78 億美元,2026 年至 2031 年的複合年成長率為 23.59%。

本報告按冷卻技術(風冷、水冷(晶片級)、浸沒式冷卻、混合冷卻)、冷卻等級(組件級冷卻和伺服器/機架級冷卻)、部署類型(超大規模雲端、邊緣運算、其他)、GPU 功率密度(低於 300W、300W-700W、高於 700W)以及國家進行細分。市場預測以美元 (USD) 為單位。

北美GPU散熱解決方案市場趨勢與洞察

用於生成式人工智慧和大規模語言模型的 GPU 工作負載激增

在北美GPU散熱解決方案市場,推動需求成長的最主要因素是傳統雲端工作負載朝向以高密度加速器為中心的AI工廠的轉變。 NVIDIA Blackwell Ultra將每顆GPU的熱設計功耗(TDP)提升至約2000瓦。與上一代A100的約700瓦相比,這是一個顯著的成長,使得許多傳統的風冷散熱方案超出了其實際運行範圍。這種轉變意義重大,因為操作員不再只專注於短時訓練負載的散熱,而是要為長時間高熱負載的持續推理處理做好準備。一項針對H100系統的2025年研究發現,在持續負載下,水冷節點每顆GPU的TFLOPS比同類風冷系統高出約17%。這顯示散熱設計如今與實際計算輸出直接相關。在北美GPU散熱解決方案市場,由於散熱架構現在同時影響吞吐量、可靠性和能源效率,因此散熱決策擴大與GPU採購同步進行。

擴大液冷技術在資料中心的應用,以降低PUE值

液冷技術正從單純的效率提升轉變為支援當今商業規模人工智慧平台的設施的必要設計要求。 NVIDIA 於 2025 年宣布,其 Blackwell 平台在液冷環境下可將水的利用效率提升 300 倍以上,這凸顯了營運商為何將液冷系統視為核心基礎設施規劃中不可或缺的一部分,而不僅僅是可選項。 Vertiv 也報告稱,其 NVIDIA GB300 NVL72 平台的參考架構可實現年度能耗降低 25%,功耗降低 30%,這使得大規模部署的營運優勢對買家而言更加清晰。這些成果正在改變託管的經濟格局,因為在超大規模資料中心和超大規模資料中心業者企業的採購週期中,能夠降低功耗和實現卓越散熱的設施更具優勢。因此,北美 GPU 冷卻解決方案市場正受到多種因素的共同驅動:機架密度不斷提高、能源目標日益嚴格,以及買家對能夠同時提升運作和設施效率的冷卻系統的偏好。

浸沒式冷卻系統維修需要較高的初始資本投入。

浸沒式冷卻技術在現有設施中的應用仍面臨許多挑戰。這是因為老舊的資料中心在設計之初並未考慮該系統所需的樓層荷載、管線佈局和服務模式。在企業級和託管資料中心,這項挑戰尤其突出,因為這些場所需要在不關閉整個設施的情況下提升人工智慧容量。此外,高負載的液冷配置可能需要結構加固,因此維修方案更像是大規模建設項目,而不僅僅是更換設備。正因如此,在北美GPU冷卻解決方案市場,液冷技術在新建設的超大規模資料中心的應用速度遠超現有企業級環境。直接晶片冷卻(DTC)系統通常優先考慮作為第一步,因為它們能夠在保持高GPU密度的同時,最大限度地減少對現有運作的干擾,從而實現液冷部署。

細分市場分析

2025年,風冷在北美GPU散熱解決方案市場仍佔47.90%的佔有率。這主要得益於企業和託管機房中大量部署的GPU,而這些機房最初的設計並未考慮液冷基礎設施。這種情況反映的是現有設施的容量限制,而非新的設計偏好。如今,北美GPU散熱解決方案市場圍繞著密度遠超過傳統機房承載能力的GPU叢集而建構。隨著機架向當今高密度AI配置演進,如何在不大幅犧牲功率和空間的情況下克服風冷的物理限制變得越來越困難。因此,大多數新的超大規模AI部署專案一開始就啟用液冷或採用完整的液冷方案,而不是將液冷系統作為後期升級。

由於其在散熱性能和易於改造的設施方面的出色平衡,直接晶片級(DTC)液冷已成為當今高密度GPU系統的主要部署方式。各廠商的產品公告表明,北美GPU散熱解決方案市場的供應端準備工作已遠遠超越了試點階段。 Vertiv發布了針對NVIDIA GB300 NVL72平台的2025年檢驗參考架構,而Supermicro也擴展了以NVIDIA Blackwell系統為核心的液冷產品組合。這兩家公司都清楚地表明,商業性環境正在向優先考慮液冷的基礎設施轉型。浸沒式冷卻仍是成長最快的技術類別,成長率高達24.12%,因為最先進的AI叢集每個機架的功率超過100千瓦,需要更有效率的散熱策略。混合設計在北美GPU散熱解決方案產業仍然至關重要,因為許多業者需要在同一機房內容納不同世代的GPU和不同的散熱需求。

到2025年,伺服器和機架級冷卻將佔北美GPU冷卻解決方案市場佔有率的59.35%,並且到2031年仍將是成長最快的冷卻等級。這種雙重地位表明,買家現在將機架(而非單一組件)視為AI基礎設施的主要溫度控管和採購單元。隨著GPU封裝、記憶體和互連擴大被設計成一個緊密整合的單一散熱區域,北美GPU冷卻解決方案市場的這種轉變更加顯著。 DCX在2026年1月發布了一款8兆瓦的設施分配單元(FDU),用於下一代NVIDIA部署的熱水冷卻,以集中式設計取代多個小型傳統CDU,從而反映了這一趨勢。

由於在標準面積下功率密度不斷提高,每個伺服器節點都需要更精確的溫度控制,因此組件級散熱仍然至關重要。 2026年3月,ZutaCore宣布其OmniTherm冷板為NVIDIA RTX PRO 6000 Blackwell伺服器版GPU提供無水雙相散熱,該GPU採用單槽PCIe封裝,這顯示精準散熱仍是商業性差異化的關鍵因素。 2026年5月,Accelsius推出的NeuCool IR150進一步加速了這個趨勢。 NeuCool IR150是一款機架級解決方案,將雙相CDU、42U機架空間和整合式歧管整合於單一機殼內,支援高達150kW的功率。因此,隨著供應商擴大將這兩種功能整合到單一可部署系統中,組件級散熱和機架級散熱之間的界限變得越來越模糊。這清楚地徵兆,北美GPU散熱解決方案產業正在從獨立的散熱組件轉向整合式溫度控管平台。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 用於生成式人工智慧和大規模語言模型的 GPU 工作負載激增

- 擴大液冷技術在資料中心的應用,以降低PUE值

- 對模組化和擴充性冷卻架構的需求日益成長

- 熱管和均熱板技術的進步

- 資料中心永續性的法規和碳中和目標

- 政府為農村地區邊緣資料中心提供激勵措施

- 市場限制因素

- 維修浸沒式冷卻需要較高的初始資本投入

- 冷卻液和幫浦組件供應鏈的波動性

- 液冷機架設計與維護的技能差距

- 絕緣油污染引發的可靠性問題

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型分類的冷卻技術

- 空冷式

- 液冷(直接冷卻至噴嘴)

- 浸沒式冷卻

- 混合冷卻

- 冷卻程度

- 組件級冷卻

- 伺服器/機架級冷卻

- 不同的發展

- 超大規模/雲

- 公司

- 政府和研究機構(高效能運算)

- 邊緣

- 按GPU功率密度

- 小於300瓦

- 300W~700W

- 700瓦或以上

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Super Micro Computer, Inc.

- Cisco Systems, Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- ASUSTeK Computer Inc.

- Giga-Byte Technology Co., Ltd.

- Cooler Master Technology Inc.

- EKWB doo

- Noctua GmbH

- Arctic GmbH

- Asetek A/S

- Fujitsu Limited

- ZutaCore, Inc.

- Vertiv Holdings Co.

- Rittal GmbH and Co. KG

- Schneider Electric SE

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america gPU cooling solutions market size is projected to expand from USD 2.25 billion in 2025 and USD 2.70 billion in 2026 to USD 7.80 billion by 2031, registering a CAGR of 23.59% between 2026 to 2031.

This report is Segmented by Cooling Technology (Air Cooling, Liquid Cooling (Direct-To-Chip), Immersion Cooling, and Hybrid Cooling), Cooling Level (Component-Level Cooling and Server / Rack-Level Cooling), Deployment (Hyperscale-Cloud, Edge, and More), GPU Power Density (Below 300W, 300W - 700W, and Above 700W), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America GPU Cooling Solutions Market Trends and Insights

Surge In GPU Workloads For Generative AI And Large Language Models

The strongest demand trigger in the North America GPU cooling solutions market is the move from traditional cloud workloads to AI factory deployments built around high-density accelerators. NVIDIA Blackwell Ultra raises thermal design power to around 2,000 W per GPU, compared with around 700 W for the earlier A100 generation, which pushes many legacy air-cooled layouts beyond their practical operating range. That shift matters because operators are no longer cooling short training bursts alone; they are preparing for sustained inference activity that keeps thermal stress high for far longer periods. A 2025 study on H100 systems found that liquid-cooled nodes delivered around 17% higher TFLOPS per GPU under sustained load than comparable air-cooled systems, which shows that thermal design is now tied directly to usable compute output. In the North America GPU cooling solutions market, cooling decisions are increasingly being made alongside GPU procurement because thermal architecture now affects throughput, reliability, and power efficiency at the same time.

Growing Adoption Of Liquid Cooling To Reduce Data Center PUE

Liquid cooling has moved from an efficiency upgrade to a design requirement for facilities that intend to support current AI platforms at commercial scale. NVIDIA stated in 2025 that its Blackwell platform can improve water efficiency by more than 300x in liquid-cooled deployments, which reinforces why operators are treating liquid systems as part of core infrastructure planning rather than optional optimization. Vertiv also reported that its reference architecture for the NVIDIA GB300 NVL72 platform reduced annual energy consumption by 25% and lowered the power footprint by 30%, which gives buyers a clearer operating case for large-scale deployment. These gains are changing colocation economics because facilities that can prove lower power overhead and better thermal control are better positioned in hyperscaler and enterprise procurement cycles. The North America GPU cooling solutions market is therefore being pulled forward by the combined effect of denser racks, tighter energy targets, and buyer preference for cooling systems that improve both uptime and facility efficiency.

High Upfront Capex For Immersion Cooling Retrofits

Immersion cooling still faces a clear adoption barrier in retrofit settings because older halls were not built for the floor loading, piping layout, and service model these systems demand. That challenge is most visible in enterprise and colocation sites where operators need to add AI capacity without shutting down the broader facility. A loaded immersion configuration can also require structural reinforcement, which pushes the retrofit decision closer to a major building project rather than a simple equipment swap. This is why the North America GPU cooling solutions market shows faster immersion uptake in greenfield hyperscale builds than in legacy enterprise environments. Direct-to-chip systems often become the preferred first step because they offer a lower-disruption path into liquid cooling while still supporting higher GPU density.

Other drivers and restraints analyzed in the detailed report include:

- Increased Preference For Modular, Scalable Cooling Architectures

- Advances In Heat Pipe And Vapor Chamber Technologies

- Supply Chain Volatility In Coolant Fluids And Pump Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air cooling retained a 47.90% share of the North America GPU cooling solutions market size in 2025, supported by the large installed base of enterprise and colocation facilities that were not originally designed for liquid infrastructure. That position reflects existing capacity more than new design preference, because the North America GPU cooling solutions market is now being built around far denser GPU clusters than earlier halls could support. Once racks move into current high-density AI configurations, the physical limit of air cooling becomes much harder to manage without large power and space penalties. This is why most new hyperscale AI deployments now start with liquid-ready or fully liquid-cooled plans instead of treating liquid systems as a later upgrade.

Direct-to-chip liquid cooling has consolidated its position as the main deployment path for current high-density GPU systems because it balances thermal performance with manageable facility change. Product launches across the vendor base show that supply-side readiness has moved well beyond pilot status in the North America GPU cooling solutions market. Vertiv published a validated reference architecture for the NVIDIA GB300 NVL72 platform in 2025, and Supermicro expanded its liquid-cooled portfolio around NVIDIA Blackwell systems, which together point to a clear commercial shift toward liquid-first infrastructure. Immersion cooling is still the fastest-growing at 24.12% technology category because frontier AI clusters are moving beyond 100 kW per rack and need more aggressive heat removal strategies. Hybrid designs also remain relevant in the North America GPU cooling solutions industry because many operators must support mixed GPU generations and varied thermal profiles within the same hall.

Server and rack-level cooling held 59.35% of the North America GPU cooling solutions market share in 2025 and is also the fastest-growing cooling level through 2031. That dual position shows how buyers now treat the rack, rather than the individual component, as the main thermal and procurement unit for AI infrastructure. The North America GPU cooling solutions market is reinforcing this shift because GPU packages, memory, and interconnects are being designed as one tightly linked thermal zone. DCX reflected that direction in January 2026 when it introduced its 8 MW Facility Distribution Unit for warm-water cooling in next-generation NVIDIA deployments, replacing multiple smaller legacy CDUs with a centralized design.

Component-level cooling still matters because each server node needs tighter thermal control as power density rises inside standard footprints. In March 2026, ZutaCore said its OmniTherm cold plate enabled waterless two-phase cooling for NVIDIA RTX PRO 6000 Blackwell Server Edition GPUs in a single-slot PCIe form factor, which shows that precision cooling remains a commercial differentiator. Accelsius added to that trend in May 2026 with the NeuCool IR150, a rack-level solution that combines a two-phase CDU, 42U of rack space, and integrated manifolds in a single enclosure supporting up to 150 kW. The boundary between component and rack-level cooling is therefore becoming less rigid because suppliers increasingly package both functions into one deployable system. This is one of the clearer signs that the North America GPU cooling solutions industry is moving toward integrated thermal platforms rather than isolated cooling parts.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Super Micro Computer, Inc.

- Cisco Systems, Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- ASUSTeK Computer Inc.

- Giga-Byte Technology Co., Ltd.

- Cooler Master Technology Inc.

- EKWB d.o.o.

- Noctua GmbH

- Arctic GmbH

- Asetek A/S

- Fujitsu Limited

- ZutaCore, Inc.

- Vertiv Holdings Co.

- Rittal GmbH and Co. KG

- Schneider Electric SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in GPU Workloads for Generative AI and Large Language Models

- 4.2.2 Growing Adoption of Liquid Cooling to Reduce Data Center PUE

- 4.2.3 Increased Preference for Modular, Scalable Cooling Architectures

- 4.2.4 Advances in Heat Pipe and Vapor Chamber Technologies

- 4.2.5 Data Center Sustainability Mandates and Carbon-Neutral Targets

- 4.2.6 Government Incentives for Edge Data Centers in Rural Areas

- 4.3 Market Restraints

- 4.3.1 High Upfront Capex for Immersion Cooling Retrofits

- 4.3.2 Supply Chain Volatility in Coolant Fluids and Pump Components

- 4.3.3 Skill Gap in Designing and Maintaining Liquid-Cooled Racks

- 4.3.4 Reliability Concerns Around Dielectric Fluid Contamination

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cooling Technology

- 5.1.1 Air Cooling

- 5.1.2 Liquid Cooling (Direct-to-Chip)

- 5.1.3 Immersion Cooling

- 5.1.4 Hybrid Cooling

- 5.2 By Cooling Level

- 5.2.1 Component-Level Cooling

- 5.2.2 Server / Rack-Level Cooling

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.3.4 Edge

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Super Micro Computer, Inc.

- 6.4.5 Cisco Systems, Inc.

- 6.4.6 Dell Technologies Inc.

- 6.4.7 Hewlett Packard Enterprise Company

- 6.4.8 Lenovo Group Limited

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Giga-Byte Technology Co., Ltd.

- 6.4.11 Cooler Master Technology Inc.

- 6.4.12 EKWB d.o.o.

- 6.4.13 Noctua GmbH

- 6.4.14 Arctic GmbH

- 6.4.15 Asetek A/S

- 6.4.16 Fujitsu Limited

- 6.4.17 ZutaCore, Inc.

- 6.4.18 Vertiv Holdings Co.

- 6.4.19 Rittal GmbH and Co. KG

- 6.4.20 Schneider Electric SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

GPU散熱解決方案:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)GPU液冷:市佔率分析、產業趨勢與統計、成長預測(2026-2031)歐洲GPU液冷:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

GPU散熱解決方案:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)GPU液冷:市佔率分析、產業趨勢與統計、成長預測(2026-2031)歐洲GPU液冷:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業及資料中心規模分類-2026-2032年全球市場預測

資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業及資料中心規模分類-2026-2032年全球市場預測 全球資料中心液冷歧管市場:按歧管類型、冷卻類型、材料類型、設計類型、資料中心類型、安裝類型和地區分類-預測至2033年

全球資料中心液冷歧管市場:按歧管類型、冷卻類型、材料類型、設計類型、資料中心類型、安裝類型和地區分類-預測至2033年 資料中心液冷市場:按組件、冷卻類型、資料中心類型、企業規模和最終用戶產業分類-市場規模、產業動態、機會分析和預測(2026-2035 年)亞太地區GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

資料中心液冷市場:按組件、冷卻類型、資料中心類型、企業規模和最終用戶產業分類-市場規模、產業動態、機會分析和預測(2026-2035 年)亞太地區GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)