|

市場調查報告書

商品編碼

2065485

亞太地區GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific GPU Cooling Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

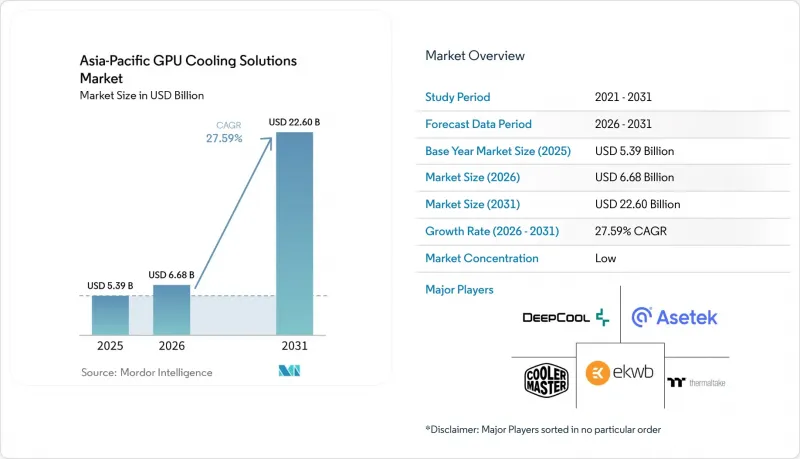

預計亞太地區 GPU 散熱解決方案市場規模將從 2025 年的 53.9 億美元成長到 2026 年的 66.8 億美元,並將在 2026 年至 2031 年期間以 27.59% 的複合年成長率成長,到 2031 年達到 226 億美元。

本報告按冷卻技術(風冷、液冷(晶片級)、浸沒式冷卻、混合冷卻)、冷卻等級(組件級冷卻和伺服器/機架級冷卻)、部署類型(超大規模雲端、企業級、邊緣運算)、GPU 功率密度(300W 以下、300W-700W、700W 及以上)和國家/地區進行細分。市場預測以美元 (USD) 為單位。

亞太地區GPU散熱解決方案市場趨勢及洞察。

亞太各國政府對資料中心能源效率的監管規定

亞太地區的GPU散熱解決方案市場也受惠於一系列政策框架,這些框架正將能源效率從單純的「建議」轉變為「設計要求」。中國根據GB/T 44989-2024制定的綠色資料中心架構及相關能源效率法規,正在收緊對大型資料中心(尤其是支援高密度運算環境的資料中心)的運作要求。日本的2026會計年度零排放資料中心商業化計畫以及對脫碳設施的廣泛補貼,正在縮短先進散熱投資的回報週期。韓國於2026年5月通過的《人工智慧資料中心特別法》表明,國家主導的人工智慧基礎設施建設將由更快的採購速度和對高密度設施更直接的政策支援來推動。從實際角度來看,這些框架將促進散熱系統的發展,使其能夠在GPU密集型機房中實現更低的PUE值,而傳統的風冷設計則無法滿足這些需求。對於亞太地區的GPU散熱解決方案市場而言,這意味著監管合規正在進一步推動GPU功率密度不斷提高所驅動的技術變革。

液冷式高密度邊緣微型資料中心的激增

第二個需求細分市場與超大規模模型截然不同,它源自於靠近終端用戶工作負載的緊湊型人工智慧設施。 Preferred Networks、日本網路計劃組織(Internet Initiative Japan)和日本科學技術大學院大學(JAIST)在日本聯合推出了「AImod」系統,該系統採用直接液冷設計,水冷比為7:3,設計PUE值為1.1,WUE值為0。這為高密度都市區人工智慧基礎設施提供了一個重要的案例研究。這種架構之所以備受關注,是因為許多邊緣和模組化站點缺乏傳統大型冷卻系統所需的面積、水源和機械設備。此外,NHN Cloud在首爾部署的擁有7656個GPU的叢集也證明,與傳統的風冷相比,液冷可以支援高密度部署,同時提高能源效率。隨著推理工作負載向工廠、通訊樞紐、交通樞紐和城市郊區遷移,日本、韓國、新加坡和東南亞部分地區對緊湊型液冷的需求日益凸顯。因此,亞太地區的 GPU 散熱解決方案市場正在從超大規模園區擴展到更廣泛的領域,進一步擴大了機架整合散熱供應商和緊湊型 CDU 供應商的基本客群。

冷卻劑供應鏈的波動

第二個主要限制因素是浸沒式冷卻系統專用冷卻劑供應鏈的緊張和不穩定。草案指出,在亞太地區的大部分地區,介電液的採購仍然高度集中且依賴進口。這使得營運商在供應緊張時面臨前置作業時間延長和認證延遲的風險。針對 PFAS 相關化學品的監管壓力以及 3M 公司 Novec 產品線的撤市,進一步加劇了需要在多個地點使用長效冷卻劑的營運商的不確定性。為此,區域內一些公司已開始開發本地替代方案,例如,韓國 S-Oil 公司與 GST 公司於 2026 年 5 月合作,利用韓國本土的冷卻劑和設備能力開發浸沒式冷卻解決方案。儘管這是一個充滿希望的開端,但考慮到人工智慧叢集部署的預期擴張,區域產能仍處於起步階段。在亞太地區的 GPU 冷卻解決方案市場,這種情況使得「直接晶片冷卻」系統仍然具有吸引力。這是因為這種方法避免了對液體的依賴,而對液體的依賴仍然阻礙了浸沒式冷卻技術的廣泛應用。

細分市場分析

2025年,風冷在亞太地區GPU散熱解決方案市場規模中佔比49.15%,持續維持其最大散熱技術細分市場的地位。同時,預計到2031年,浸沒式散熱將以24.12%的複合年成長率成長。這種情況是由於該地區企業、公共部門和消費用戶部署了大量GPU系統,這些系統採用的散熱溫度控管嚴重依賴氣流,尚未達到全面過渡到液冷的閾值。在亞太地區的GPU散熱解決方案市場中,遊戲、工作站和低密度伺服器環境中仍存在相當數量的風冷系統。在預算和設施限制導致大規模升級延遲的領域,這種趨勢尤其明顯。另一方面,隨著最新的AI硬體將熱密度推向傳統風冷設計的允許運行範圍之外,預計到2031年,浸沒式散熱將成為成長最快的技術領域。

直接晶片液冷 (DTC) 正逐漸成為連接現有基礎設施與下一代 GPU 功耗範圍的最實用橋樑。與浸沒式冷卻相比,DTC 通常能夠以更小的干擾整合到現有伺服器設計中,對於需要支援新型加速器而無需重建整個機房的企業、託管和公共部門買家而言,它極具吸引力。混合冷卻在都市區高密度部署中也越來越受到關注,尤其是那些希望對高發熱組件使用液冷,而對系統其餘部分使用餘熱空氣冷卻的運營商。日本 AImod 設施就是一個很好的例子,它證明了水冷-空氣混合模式在緊湊型 AI 部署環境中可以非常有效率。雖然整個亞太地區的 GPU 冷卻解決方案產業正在向液冷設計轉型,但轉型的路徑仍會因設施的建成時間、工作負載強度和可用資金而有所不同。

到2025年,伺服器機架級冷卻將佔亞太地區GPU冷卻解決方案市場61.25%的佔有率,並且在整個預測期內也將是成長最快的冷卻等級。這一趨勢反映了人工智慧資料中心架構的顯著轉變,機架不再只是單一組件的集合,而是被視為一個整合的散熱和供電區域。亞太地區GPU冷卻解決方案市場正朝著這個方向發展,因為整合GPU系統現在被部署為緊密協調的叢集,這些集群共用的冷卻液路徑、通用的監控和協同故障安全控制。因此,在人工智慧工廠和國家級運算中心,機架級冷卻比單一組件級解決方案更有價值。

在消費級遊戲、工作站系統和小規模專業環境中,組件級散熱仍然至關重要,因為這些領域的溫度控管仍然基於顯示卡,且部署規模較小。台灣和中國大陸的製造商繼續受益於其龐大的銷售規模,尤其是在售後市場和專業消費級通路。然而,隨著高密度人工智慧叢集需要對整個系統進行協調的溫度控管,銷售結構正轉向機架級平台。 NHN Cloud 在首爾部署的液冷叢集展示了這種模式的運作效率,其機架層級管理與大規模GPU 環境中的壓力、流量和溫度監控相連。這種轉變賦予了機架級廠商更強的定價權,並使他們能夠將研發重點放在分配單元、歧管系統和協調的機架冷卻控制上。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- AI工作負載中GPU熱設計功耗的增加

- 亞太各國政府對資料中心能源效率的監管規定

- 液冷式高密度邊緣微型資料中心的激增

- 中國和日本對綠色IT基礎設施的稅收優惠

- 透過超大規模資料中心業者實現晶片級直接冷卻硬體的垂直整合

- 半導體OEM廠商正在發布適用於身臨其境型環境的GPU參考設計。

- 市場限制因素

- 維修浸沒式冷卻需要大量資金投入

- 冷卻劑供應鏈的可變性

- 缺乏熟練工人來進行液體迴路試運行

- 冷卻技術領域整體缺乏通用的開放標準。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按類型分類的冷卻技術

- 空冷式

- 液冷(直接冷卻至噴嘴)

- 浸沒式冷卻

- 混合冷卻

- 冷卻水平

- 組件級冷卻

- 伺服器/機架級冷卻

- 不同的發展

- 超大規模/雲

- 公司

- 政府和研究機構(高效能運算)

- 邊緣

- 按GPU功率密度

- 小於300瓦

- 300W~700W

- 700瓦或以上

- 國家

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cooler Master Technology Inc.

- Deepcool Industries Co., Ltd.

- Asetek A/S

- Noctua GmbH

- EKWB doo

- Alphacool International GmbH

- Thermaltake Technology Co., Ltd.

- Corsair Gaming Inc.

- Gigabyte Technology Co., Ltd.

- Micro-Star International Co., Ltd.

- ASUSTeK Computer Inc.

- ZALMAN Tech Co., Ltd.

- Arctic GmbH

- NZXT, Inc.

- Phanteks BV

- SilverStone Technology Co., Ltd.

- Aquacomputer GmbH and Co. KG

- Bykski Technology Co., Ltd.

- Bitspower International Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific gPU cooling solutions market size is expected to grow from USD 5.39 billion in 2025 to USD 6.68 billion in 2026 and is forecast to reach USD 22.60 billion by 2031 at 27.59% CAGR over 2026-2031.

This report is Segmented by Cooling Technology (Air Cooling, Liquid Cooling (Direct-To-Chip), Immersion Cooling, and Hybrid Cooling), Cooling Level (Component-Level Cooling and Server / Rack-Level Cooling), Deployment (Hyperscale-Cloud, Enterprise, and Edge), GPU Power Density (Below 300W, 300W - 700W, and Above 700W), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific GPU Cooling Solutions Market Trends and Insights

Data-Center Energy Efficiency Mandates By Asia-Pacific Governments

The Asia-Pacific GPU cooling solutions market is also benefiting from policy frameworks that turn energy efficiency from a preference into a design requirement. China's green data center framework under GB/T 44989-2024 and related energy efficiency rules is tightening the operating envelope for large data facilities, especially those that support dense compute deployments. Japan's fiscal 2026 zero-emission data center commercialization program and its broader subsidy support for decarbonized facilities are reducing the payback period for advanced cooling investments. South Korea's AI Data Center Special Act, cleared in May 2026, signaled that sovereign AI infrastructure will move forward with faster procurement and more direct policy support for high-density facilities. In practical terms, these frameworks favor cooling systems that can support lower PUE targets in GPU-heavy halls where legacy air designs struggle. For the Asia-Pacific GPU cooling solutions market, this means regulatory compliance is now reinforcing the same technology shift that GPU power density has already set in motion.

Proliferation Of Liquid-Cooled High-Density Edge Micro-Data Centers

A second layer of demand is coming from compact AI facilities that sit outside the hyperscale model and closer to end-use workloads. Preferred Networks, Internet Initiative Japan, and JAIST brought AImod into operation in Japan with a direct liquid cooling design, a 7:3 water-to-air ratio, a design PUE of 1.1, and a WUE of 0, which makes it an important reference point for dense urban AI infrastructure. That type of architecture is relevant because many edge and modular sites cannot absorb the space, water, or mechanical plant footprint associated with larger conventional cooling systems. NHN Cloud's 7,656-GPU cluster in Seoul also showed that liquid cooling can support dense deployment while improving energy performance compared with conventional air-cooled setups. As inference workloads move closer to factories, telecom sites, transport nodes, and city-edge facilities, the need for compact liquid cooling becomes more visible across Japan, South Korea, Singapore, and selected Southeast Asian markets. The Asia-Pacific GPU cooling solutions market is therefore widening beyond hyperscale campuses, which gives rack-integrated cooling vendors and compact CDU suppliers a broader customer base.

Supply-Chain Volatility For Coolant Fluids

The second major restraint is the tight and changing supply chain for specialty cooling fluids used in immersion deployments. The draft highlighted that dielectric fluid sourcing remains concentrated and import-dependent across much of the Asia-Pacific, which exposes operators to lead-time risk and qualification delays when supply conditions tighten. Regulatory pressure on PFAS-linked chemistries and the exit of 3M's Novec line have added another layer of uncertainty for operators that need long-life fluid choices across multiple sites. In response, regional players have started to build local alternatives, including the May 2026 partnership between S-Oil and GST in South Korea to develop an immersion cooling solution around domestically linked fluid and equipment capabilities. That is a useful first step, but regional capacity is still early relative to the expected rise in AI cluster deployment. In the Asia-Pacific GPU cooling solutions market, this keeps direct-to-chip systems attractive because they avoid part of the fluid dependency that still slows broader immersion adoption.

Other drivers and restraints analyzed in the detailed report include:

- Tax Incentives For Green IT Infrastructure In China And Japan

- Rising GPU Thermal Design Power In AI Workloads

- High Capital Expenditure Of Immersion Cooling Retrofits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air cooling held 49.15% of the Asia-Pacific GPU cooling solutions market size in 2025, which kept it as the largest cooling technology segment, while immersion cooling is projected to expand at a 24.12% CAGR through 2031. That position came from the region's large installed base of enterprise, public sector, and consumer GPU systems that were built around airflow-heavy thermal management and have not yet crossed the threshold for full liquid adoption. The Asia-Pacific GPU cooling solutions market still has meaningful air-cooled volume in gaming, workstation, and lower-density server environments, particularly where budgets or facility limitations delay major upgrades. At the same time, immersion cooling is the fastest-growing technology segment through 2031 because the newest AI hardware is pushing heat density beyond the comfortable operating range of traditional air designs.

Direct-to-chip liquid cooling is gaining ground as the most practical bridge between installed infrastructure and next-generation GPU power envelopes. It can often be introduced into existing server designs with less disruption than immersion, which makes it attractive for enterprise, colocation, and public sector buyers that need to support newer accelerators without rebuilding entire halls. Hybrid cooling is also gaining traction in dense urban deployments, especially where operators want liquid cooling for high-heat components and residual air support for the rest of the system. Japan's AImod facility is a useful signal because it showed how a water-air hybrid model can achieve strong efficiency results in a compact AI deployment. Across the Asia-Pacific GPU cooling solutions industry, the technology mix is shifting toward liquid-based designs, but the transition path still differs by facility age, workload intensity, and available capital.

Server-rack-level cooling accounted for 61.25% share of the Asia-Pacific GPU cooling solutions market size in 2025, and it is also the fastest-growing cooling level over the forecast period. That combination reflects a clear architectural change in AI data centers, where the rack is now treated as a unified thermal and power domain rather than a collection of separate components. The Asia-Pacific GPU cooling solutions market is moving in this direction because integrated GPU systems are now deployed in tightly linked clusters with shared coolant routing, common monitoring, and coordinated fail-safe controls. Rack-level cooling, therefore, carries more value in AI factories and sovereign compute sites than isolated component-level solutions.

Component-level cooling still matters in consumer gaming, workstation systems, and lower-scale professional environments where thermal management remains card-specific, and the deployment unit is much smaller. Vendors based in Taiwan and China continue to benefit from that volume base, especially in aftermarket and prosumer channels. Even so, the revenue mix is migrating upward toward rack-scale platforms because dense AI clusters now require thermal management that is coordinated across the whole system. NHN Cloud's liquid-cooled cluster in Seoul illustrated the operational case for this model, with rack-level management tied to pressure, flow, and temperature monitoring across a very large GPU environment. That shift gives rack-level vendors stronger pricing power and keeps R&D focused on distribution units, manifold systems, and coordinated rack cooling controls.

List of Companies Covered in this Report:

- Cooler Master Technology Inc.

- Deepcool Industries Co., Ltd.

- Asetek A/S

- Noctua GmbH

- EKWB d.o.o.

- Alphacool International GmbH

- Thermaltake Technology Co., Ltd.

- Corsair Gaming Inc.

- Gigabyte Technology Co., Ltd.

- Micro-Star International Co., Ltd.

- ASUSTeK Computer Inc.

- ZALMAN Tech Co., Ltd.

- Arctic GmbH

- NZXT, Inc.

- Phanteks B.V.

- SilverStone Technology Co., Ltd.

- Aquacomputer GmbH and Co. KG

- Bykski Technology Co., Ltd.

- Bitspower International Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising GPU Thermal Design Power in AI Workloads

- 4.2.2 Data-Center Energy Efficiency Mandates by Asia-Pacific Governments

- 4.2.3 Proliferation of Liquid-Cooled High-Density Edge Micro-Data Centers

- 4.2.4 Tax Incentives for Green IT Infrastructure in China and Japan

- 4.2.5 Vertical Integration of Hyperscalers into Direct-to-Chip Cooling Hardware

- 4.2.6 Emergence of Immersion-Ready GPU Reference Designs from Semiconductor OEMs

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure of Immersion Cooling Retrofits

- 4.3.2 Supply-Chain Volatility for Coolant Fluids

- 4.3.3 Limited Skilled Workforce for Liquid Loop Commissioning

- 4.3.4 Lack of Common Open Standards Across Cooling Technologies

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cooling Technology

- 5.1.1 Air Cooling

- 5.1.2 Liquid Cooling (Direct-to-Chip)

- 5.1.3 Immersion Cooling

- 5.1.4 Hybrid Cooling

- 5.2 By Cooling Level

- 5.2.1 Component-Level Cooling

- 5.2.2 Server / Rack-Level Cooling

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.3.4 Edge

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 South Korea

- 5.5.4 India

- 5.5.5 Southeast Asia

- 5.5.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cooler Master Technology Inc.

- 6.4.2 Deepcool Industries Co., Ltd.

- 6.4.3 Asetek A/S

- 6.4.4 Noctua GmbH

- 6.4.5 EKWB d.o.o.

- 6.4.6 Alphacool International GmbH

- 6.4.7 Thermaltake Technology Co., Ltd.

- 6.4.8 Corsair Gaming Inc.

- 6.4.9 Gigabyte Technology Co., Ltd.

- 6.4.10 Micro-Star International Co., Ltd.

- 6.4.11 ASUSTeK Computer Inc.

- 6.4.12 ZALMAN Tech Co., Ltd.

- 6.4.13 Arctic GmbH

- 6.4.14 NZXT, Inc.

- 6.4.15 Phanteks B.V.

- 6.4.16 SilverStone Technology Co., Ltd.

- 6.4.17 Aquacomputer GmbH and Co. KG

- 6.4.18 Bykski Technology Co., Ltd.

- 6.4.19 Bitspower International Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

GPU散熱解決方案:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)GPU液冷:市佔率分析、產業趨勢與統計、成長預測(2026-2031)歐洲GPU液冷:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

GPU散熱解決方案:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)GPU液冷:市佔率分析、產業趨勢與統計、成長預測(2026-2031)歐洲GPU液冷:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業及資料中心規模分類-2026-2032年全球市場預測

資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業及資料中心規模分類-2026-2032年全球市場預測 全球資料中心液冷歧管市場:按歧管類型、冷卻類型、材料類型、設計類型、資料中心類型、安裝類型和地區分類-預測至2033年

全球資料中心液冷歧管市場:按歧管類型、冷卻類型、材料類型、設計類型、資料中心類型、安裝類型和地區分類-預測至2033年 資料中心液冷市場:按組件、冷卻類型、資料中心類型、企業規模和最終用戶產業分類-市場規模、產業動態、機會分析和預測(2026-2035 年)北美GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

資料中心液冷市場:按組件、冷卻類型、資料中心類型、企業規模和最終用戶產業分類-市場規模、產業動態、機會分析和預測(2026-2035 年)北美GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)