|

市場調查報告書

商品編碼

2064379

中東和北非地區的機電管道(MEP)服務:市場佔有率分析、行業趨勢與統計數據以及成長預測(2026-2031 年)Middle East And North Africa Mechanical, Electrical, And Plumbing (MEP) Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

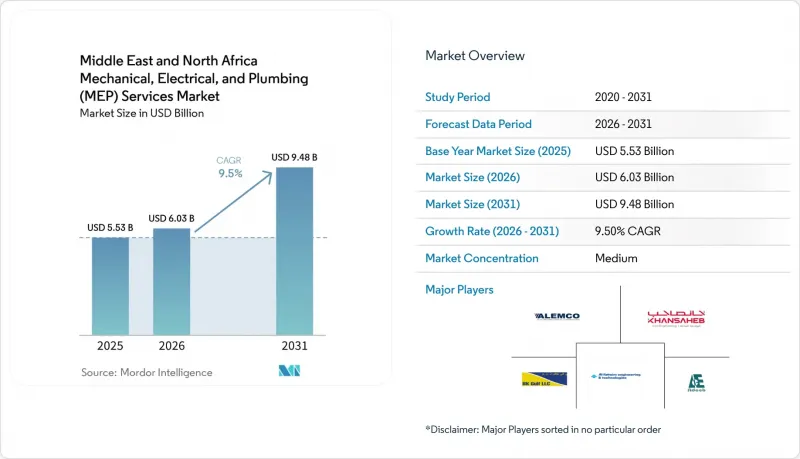

根據 Mordor Intelligence 預測,中東和北非 (MENA) 的機電管道 (MEP) 服務市場規模預計在 2025 年達到 55.3 億美元,在 2026 年達到 60.3 億美元,在 2031 年達到 94.8 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 9.5%。

本報告按類型(機械、電氣、管道、機電一體化服務)、服務類型(設計與工程、安裝、測試與試運行、維護與維修、其他)、最終用戶行業(住宅、商業、基礎設施)以及地區(沙烏地阿拉伯、阿拉伯聯合大公國、埃及、土耳其、摩洛哥及其他中東和北非國家)進行分類。市場預測以美元計價。

中東和北非機械、電氣和管道 (MEP) 服務市場趨勢與分析

沙烏地阿拉伯的超級計畫和阿拉伯聯合大公國的綜合用途開發擴張

儘管沙烏地阿拉伯的大型專案業主在大規模專案中實施了更嚴格的流程控制和可行性檢驗,但其巨型專案活動仍然是中東和北非地區機電工程服務市場最大的需求來源。隨著2030年利雅德世博會和2034年國際足總世界盃的舉辦,短期合約包與明確的交付里程碑掛鉤,使得正在進行的項目更加注重「執行主導」而非「宣傳主導」。在阿拉伯聯合大公國,綜合用途和目的地項目正在將中東和北非地區的機電工程服務市場拓展至商業、休閒、酒店和住宅等多元化領域,從而降低了對單一項目類型的依賴。此外,沙烏地阿拉伯的客戶更積極提出本土價值創造要求,將競爭轉向那些擁有本土製造能力、人才培育能力和專案執行深度的承包商。雖然規模在這一細分市場仍然很重要,但如今人們更加重視執行的可靠性,而非公佈的專案規模。

資料中心、區域冷卻和關鍵任務需求

資料中心、區域冷卻和其他關鍵任務專案正在改變中東和北非地區機電工程服務市場的商業結構,因為它們需要從初始設計階段就開始進行更深入的系統整合。機架密度的增加對電力冗餘、液冷策略和備用系統提出了比傳統商業建築更複雜的要求。這使得價值更多地流向那些能夠及早調整機電工程範圍的工程師和承包商,而不是在採購決策最終確定後才在安裝階段進行修改。區域供冷廠和管網系統也將中東和北非地區的機電工程服務市場與綜合城市發展規劃連結起來,在大規模機械裝置與公共產業和公共基礎設施一同部署。由於這些需求與數位基礎設施、公共產業規劃和城市服務平台相關聯,因此它們受短期房地產市場波動的影響較小。

技術純熟勞工及工程人員短缺

中東和北非地區機電工程服務市場仍面臨技術純熟勞工及工程人才短缺的結構性限制因素。這是因為能夠管理和安裝複雜系統的訓練有素人員的供應速度跟不上專案數量的成長。該地區急需主管、專案經理、試運行專家和認證安裝人員,但培訓這些人員需要時間,而且在專案工期緊張時,人員難以替代。如果機電工程分包商未能按計劃將人員部署到現場,主要承包商將被迫承擔工期延誤,從而增加整個專案鏈的索賠風險。在某些市場,暖通空調及相關產業安裝人員缺乏完全標準化的資質要求,也導致技能水準參差不齊,進而影響品質。雖然投資建造內部培訓中心和製定現場標準化流程的公司可以降低風險,但中東和北非地區整體機電工程服務市場仍然嚴重缺乏人員。

細分市場分析

2025年,機械設備服務在中東和北非地區機電工程服務市佔率中佔比高達48.3%,成為最大的細分市場,遙遙領先。該地區對製冷的持續需求使得暖通空調(HVAC)相關工作在商業建築、住宅小區、酒店、交通基礎設施和公共設施中至關重要,從而支撐了新建和維修項目中對大規模機械設備包的需求。電氣服務仍然是第二大細分市場,這主要得益於資料中心、智慧建築系統、緊急電源系統和低壓網路等因素導致新計畫整體系統日益複雜。管道服務呈現穩定成長,這得益於海水淡化相關網路的需求、節水義務以及現有資產中處理後水的日益增加。

預計2026年至2031年間,整合式機電工程(MEP)服務將以12.1%的複合年成長率成長,成為中東和北非地區(MENA)MEP服務產業中成長最快的細分市場。在綜合用途設施、酒店設施、基礎設施和大型項目中,總開發人員越來越傾向於簽訂涵蓋機械、電氣和管道領域的單一契約,以確保責任明確。這是因為一個系統出現偏差可能會導致其他多個系統在交付時出現延遲。擁有關鍵任務系統、智慧低壓裝置和能夠快速交貨的專家團隊的供應商將能夠很好地受益於這一轉變,尤其是在專案業主要求減少介面和更嚴格的進度管理的情況下。整合式交付也符合日益嚴格的能源效能要求,因為在單一總承包商的管理下,跨系統的建模、測試和試運行更容易完成。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 沙烏地阿拉伯的大型專案和阿拉伯聯合大公國混合用途開發專案的擴張

- 資料中心、區域冷卻和關鍵任務需求

- 高冷卻負荷建築的節能維修

- BIM主導的設計協調和模組化機電系統的推廣

- 北非的機場、旅遊業和新城市發展

- 需要將水資源再利用,與海水淡化相結合,並採用高效管道。

- 市場限制因素

- 技術純熟勞工和工程師短缺

- 材料前置作業時間和激烈的價格競爭

- 付款授權延遲和索賠管理風險

- 特定市場的地緣政治與安全變化

- 價值鍊和供應鏈分析

- 監理情勢

- 技術展望

- 市場吸引力:波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 成本結構分析

第5章:預測市場規模與成長率

- 按類型

- 機械服務

- 電力服務

- 管道服務

- 綜合機電服務

- 按服務類型

- 設計與工程

- 安裝、測試和試運行

- 維護/修理

- 其他服務

- 按最終用戶行業分類

- 住宅

- 商業

- 基礎設施

- 按地區

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 埃及

- 土耳其

- 摩洛哥

- 其他中東和北非(MENA)地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BK Gulf

- ALEMCO

- Al-Futtaim Engineering & Technologies

- Khansaheb MEP

- Adeeb Group

- AG Engineering

- Al Shafar United

- Menasco Mechanical Contracting

- Voltas Limited

- Orascom Construction

- International Electromechanical Services

- Drake & Scull Engineering

- ETA Engineering

- KEO International Consultants

- Dar Al-Handasah

- Jacobs

- AECOM

- WSP Global

- AtkinsRealis

- Cundall

- Buro Happold

- Khatib & Alami

- Johnson Controls Arabia

- JLW Middle East

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east and north africa mechanical, electrical, and plumbing services market size is projected to be USD 5.53 billion in 2025, USD 6.03 billion in 2026, and reach USD 9.48 billion by 2031, growing at a CAGR of 9.5% from 2026 to 2031.

This report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP Services), Service Type (Design & Engineering, Installation Testing & Commissioning, Maintenance & Repair, Other), End-User Industry (Residential, Commercial, Infrastructure), and Geography (Saudi Arabia, UAE, Egypt, Turkey, Morocco, Rest of MENA). The Market Forecasts are Provided in Terms of Value (USD).

Middle East And North Africa Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Saudi Giga-Projects and UAE Mixed-Use Expansion

Saudi giga-project activity remains the largest demand engine in the MENA MEP services market, even as project owners apply tighter sequencing and feasibility checks across very large programs. Expo 2030 Riyadh and the 2034 FIFA World Cup keep near-term packages tied to visible delivery milestones, which makes the active pipeline more execution-led than headline-led. In the UAE, mixed-use and destination projects keep the MENA MEP services market broad across commercial, leisure, hospitality, and residential formats, which reduces dependence on a single project class. Saudi clients are also applying in-country value requirements more actively, and that is shifting competition toward contractors with local manufacturing, training capacity, and delivery depth inside the Kingdom. Scale still matters in this part of the market, but execution credibility now matters more than announced project value.

Data-Center, District-Cooling, and Mission-Critical Demand

Data-center, district-cooling, and other mission-critical projects are changing the mix of work in the MENA MEP services market because they require deeper system integration from the first design stage. Higher rack densities are pushing designers toward more complex power redundancy, liquid-cooling strategies, and backup systems than conventional commercial buildings usually require. This shifts value toward engineers and contractors that can coordinate mechanical and electrical scopes early, rather than rely on late installation fixes after procurement decisions are already locked in. District-cooling plants and network pipework also keep the MENA MEP services market tied to master-planned urban developments where large mechanical packages move in parallel with utilities and public infrastructure. These demand streams are less exposed to short-term real estate sentiment because they are linked to digital infrastructure, utility planning, and urban service platforms.

Skilled-Labor and Engineering Talent Shortages

Skilled labor and engineering shortages remain a structural limit on the MENA MEP services market because project volume is rising faster than the supply of trained people who can manage and install complex systems. The regional pipeline needs more supervisors, project managers, commissioning specialists, and certified installers, but that workforce takes time to build and is not easily replaced once project schedules compress. When MEP subcontractors cannot staff work fronts on time, main contractors absorb schedule slippage and wider claims exposure across the full project chain. Skill inconsistency is also a quality issue because some markets still lack fully standardized installer qualification requirements across HVAC and related trades. Companies that invest in internal training centers and repeatable site processes are better protected, but the workforce gap remains material across the MENA MEP services market.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Retrofits in Cooling-Intensive Buildings

- BIM-Led Design Coordination and Modular MEP Uptake

- Material Lead Times and Aggressive Price Competition

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mechanical Services held 48.3% of the MENA MEP services market share in 2025, which made it the largest type segment by a wide margin. The region's sustained cooling load keeps HVAC-related work essential across commercial buildings, residential compounds, hotels, transport assets, and public facilities, which supports large mechanical packages through both new build and retrofit cycles. Electrical Services remained the second-largest segment because data centers, smart-building systems, backup power architecture, and low-voltage networks are expanding overall system complexity in new projects. Plumbing Services stayed steady, with demand supported by desalination-linked networks, water-efficiency mandates, and wider adoption of treated-water reuse in built assets.

Integrated MEP Services is projected to grow at a 12.1% CAGR from 2026 to 2031, the fastest pace among type segments in the MENA MEP services industry. Master developers increasingly prefer single-contract accountability across mechanical, electrical, and plumbing scopes on mixed-use, hospitality, infrastructure, and giga-project programs, because coordination failures on one system can delay several others at handover. Providers with specialist teams across mission-critical systems, intelligent low-voltage work, and fast-track delivery are well positioned to benefit from this shift, particularly where project owners want fewer interfaces and tighter schedule control. Integrated delivery also aligns with stricter energy-performance expectations because cross-system modeling, testing, and commissioning are easier to manage under one lead contractor.

List of Companies Covered in this Report:

- BK Gulf

- ALEMCO

- Al-Futtaim Engineering & Technologies

- Khansaheb MEP

- Adeeb Group

- AG Engineering

- Al Shafar United

- Menasco Mechanical Contracting

- Voltas Limited

- Orascom Construction

- International Electromechanical Services

- Drake & Scull Engineering

- ETA Engineering

- KEO International Consultants

- Dar Al-Handasah

- Jacobs

- AECOM

- WSP Global

- AtkinsRealis

- Cundall

- Buro Happold

- Khatib & Alami

- Johnson Controls Arabia

- JLW Middle East

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Saudi Giga-Projects and UAE Mixed-Use Expansion

- 4.2.2 Data-Center, District-Cooling, and Mission-Critical Demand

- 4.2.3 Energy-Efficiency Retrofits in Cooling-Intensive Buildings

- 4.2.4 BIM-Led Design Coordination and Modular MEP Uptake

- 4.2.5 Airport, Tourism, and New-City Build-Outs in North Africa

- 4.2.6 Water Reuse, Desalination Linkage, and High-Efficiency Plumbing Needs

- 4.3 Market Restraints

- 4.3.1 Skilled-Labor and Engineering Talent Shortages

- 4.3.2 Material Lead Times and Aggressive Price Competition

- 4.3.3 Payment-Certification Delays and Claims-Management Risk

- 4.3.4 Geopolitical and Security Volatility in Select Markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Cost Structure Analysis

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Type

- 5.1.1 Mechanical Services

- 5.1.2 Electrical Services

- 5.1.3 Plumbing Services

- 5.1.4 Integrated MEP Services

- 5.2 By Service Type

- 5.2.1 Design & Engineering

- 5.2.2 Installation, Testing, and Commissioning

- 5.2.3 Maintenance & Repair

- 5.2.4 Other Services

- 5.3 By End-User Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Egypt

- 5.4.4 Turkey

- 5.4.5 Morocco

- 5.4.6 Rest of Middle East and North Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 BK Gulf

- 6.4.2 ALEMCO

- 6.4.3 Al-Futtaim Engineering & Technologies

- 6.4.4 Khansaheb MEP

- 6.4.5 Adeeb Group

- 6.4.6 AG Engineering

- 6.4.7 Al Shafar United

- 6.4.8 Menasco Mechanical Contracting

- 6.4.9 Voltas Limited

- 6.4.10 Orascom Construction

- 6.4.11 International Electromechanical Services

- 6.4.12 Drake & Scull Engineering

- 6.4.13 ETA Engineering

- 6.4.14 KEO International Consultants

- 6.4.15 Dar Al-Handasah

- 6.4.16 Jacobs

- 6.4.17 AECOM

- 6.4.18 WSP Global

- 6.4.19 AtkinsRealis

- 6.4.20 Cundall

- 6.4.21 Buro Happold

- 6.4.22 Khatib & Alami

- 6.4.23 Johnson Controls Arabia

- 6.4.24 JLW Middle East

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

中東歐機械、電氣和管道 (MEP) 服務:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)東協機械、電氣和管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)南美洲機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中東歐機械、電氣和管道 (MEP) 服務:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)東協機械、電氣和管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)南美洲機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 機械、電氣和管道服務市場:按服務類型、最終用戶和地區分類

機械、電氣和管道服務市場:按服務類型、最終用戶和地區分類 機械、電氣和管道服務市場:按服務類型、服務形式、計劃規模、技術和建築類型分類-2026-2032年全球市場預測

機械、電氣和管道服務市場:按服務類型、服務形式、計劃規模、技術和建築類型分類-2026-2032年全球市場預測 2026年全球機械、電氣和管道(MEP)服務市場報告2026年全球管道服務軟體市場報告

2026年全球機械、電氣和管道(MEP)服務市場報告2026年全球管道服務軟體市場報告