|

市場調查報告書

商品編碼

2064004

南美洲機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)South America Mechanical, Electrical, And Plumbing (MEP) Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

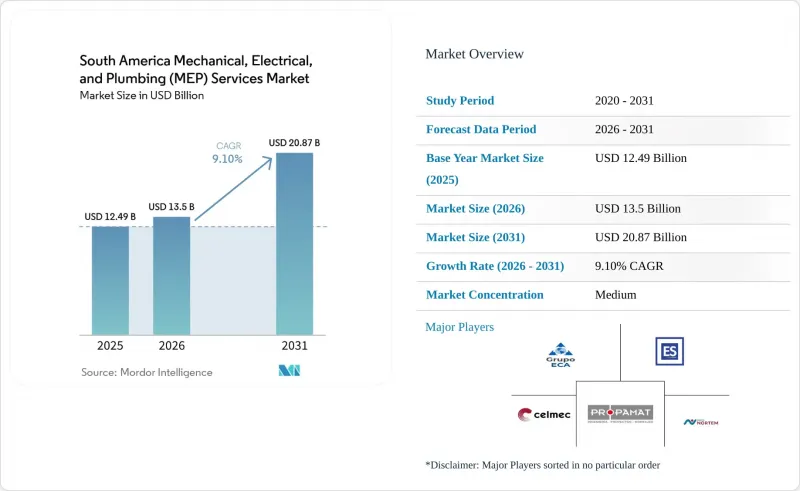

根據 Mordor Intelligence 預測,南美洲機械、電氣和管道 (MEP) 服務市場規模預計將從 2025 年的 124.9 億美元成長到 2026 年的 135 億美元,到 2031 年將達到 208.7 億美元,2026 年至 2031 年的複合年成長率為 20319.0%。

本報告按類型(機械、電氣、管道、一體化機電)、服務類型(設計與工程、安裝、測試與試運行、維護、維修與維修、管理型和績效型)、最終用戶行業(住宅、商業、基礎設施)以及地區(巴西、阿根廷、智利、哥倫比亞、秘魯及其他南美國家)進行細分。市場預測以美元計價。

南美機械、電氣和管道 (MEP) 服務市場的趨勢和洞察

商業設施和基礎設施的現代化

南美洲的機電管道(MEP)服務市場正受益於該地區在交通、醫療、水務和城市資產等領域的大規模現代化改造。巴西的建築業佔其GDP的近6%,而PAC-3已承諾在交通、能源、水務和城市交通領域投資3330億美元,這為醫院、機場、地鐵系統和衛生設施等項目帶來了多年期的MEP分包機會。類似的趨勢也出現在巴西以外的地區。 AECOM的合資企業被秘魯衛生署選中,將於2024年負責管理皮烏拉和特魯希略的兩家大型區域醫院。該公司將根據BIM主導的模式,承擔整個MEP生命週期的責任。此外,巴西在全球LEED認證建築數量排名中位列前五,這進一步凸顯了可審計的MEP性能的重要性,因為認證現在不僅取決於設備安裝的完成情況,還取決於系統的整體運行結果。這延長了南美機電管道(MEP)服務市場的合約期限,提高了那些在專案移交後繼續參與監測、試運行和能源最佳化等工作的公司的價值。這也意味著南美MEP服務市場不再那麼依賴一次性的施工週期,而是與持續的建築性能義務更加緊密地聯繫在一起。

資料中心和物流設施的擴建

南美洲的機電管線(MEP)服務市場正受惠於巴西和智利資料中心園區和現代化物流設施的擴張。智利2024-2030年國家資料中心計畫旨在將該產業的規模擴大三倍,預計從2025年起,超大規模資料中心業者中心的投資將超過80億美元。這將持續創造對冷卻、電力品質、緊急電源和消防系統等配套設備的需求。以人工智慧為中心的機房正從傳統的每機架10千瓦的設計要求轉向每機架100千瓦的密度,這需要液冷迴路、高壓母線槽和N+1冗餘冷卻器。這種轉變導致能夠提供高密度機電配套設備並順利完成試運行的承包商數量減少。因此,在南美洲機電管道(MEP)服務市場中,普通供應商和能夠處理高密度數位園區的專業承包商之間的差距正在擴大。類似的變化正在蔓延到鄰近的物流設施,營運商在試運行中越來越要求容錯電力系統、先進的通風系統和自動化服務框架。

外匯波動與通膨壓力

外匯波動和資金籌措成本仍然是南美機電管道(MEP)服務市場業務運作面臨的重大障礙。巴西的法定利率預計將在2025年5月達到14.8%,而經合組織僅預測溫和寬鬆,導致客戶的借貸成本居高不下,給依賴進口設備的固定價格項目的承包商利潤率帶來壓力。截至2026年2月的12個月內,PVC管道價格已上漲16.3%,建築成本通膨可能將INCC(建築成本指數)在2026年推高至9.7%。這將進一步加劇在這些材料價格上漲之前簽訂的合約的壓力。這種影響在可再生能源、數位基礎設施和其他依賴美元計價組件和對沖成本的MEP密集型項目中尤為顯著。在南美洲的機電管線(MEP)服務市場,採購團隊無法快速將成本波動轉嫁給客戶,可能導致專案延期、範圍縮小或競標條件更加嚴苛。在阿根廷,疲軟的貨幣進一步加劇了這種壓力,導致當地MEP系統的成本急劇上升,而與傳統解決方案相比,這些系統需要更高的資本支出(CAPEX)。這可能導致買家擴大選擇推遲部署,而不是進行升級。

細分市場分析

到2025年,機械服務將佔南美機電管道(MEP)服務市場37%的佔有率,成為最大的服務細分市場。這一地位反映了暖通空調、冷凍和工業製程冷卻設備在商業建築、醫療設施和數位基礎設施等領域的廣泛應用。南美機電管道(MEP)服務市場將繼續聚焦機械領域,因為巴西的熱帶氣候條件以及高可用性設施的冷卻需求,使得溫度控管成為專案設計和維護的核心。管道服務也持續佔據重要地位,因為巴西的衛生設施差距依然巨大,47%的人口尚未連接污水管網,這持續推動與水和污水相關的維修和管網建設需求。綜合機電服務是成長最快的行業,預計到 2031 年將以 11.7% 的複合年成長率成長,因為客戶降低了單獨協調機械、電氣和管道承包商的成本和風險。

在南美洲的機電管道 (MEP) 服務業,整合合約的興起使那些能夠調動多學科現場團隊並在單一合約範圍內持續管理設計、安裝、測試和試運行的公司受益匪淺。這種轉變在資料中心領域尤其顯著,因為高密度機房需要同時重新設計冷卻迴路、配電和水資源管理系統,而不是單獨交付各個組件。業主也利用整合合約來減少介面糾紛、縮短交接週期,並確保由一家供應商而非三家供應商提供性能保證。這正在擴大南美洲 MEP 服務市場中具備全生命週期能力的公司與僅提供獨立安裝套件的公司之間的差距。因此,能夠將機械專業知識、電氣可靠性、管道整合和正式試運行能力整合到單一、可管理的提案中的承包商,將擁有更有利的成長前景。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 商業設施和基礎設施的現代化

- 資料中心和物流設施的擴建

- 硬體服務和生命週期維護的外包

- 在智利和巴西開發電力整合園區

- ESG主導的能源和冷媒審計範圍

- 水資源韌性及閉式循環冷卻系統的維修

- 市場限制因素

- 外匯波動與通膨壓力

- 非正式就業和工作表現品質的波動

- 建築和消防安全法規執行分散

- 數位產業叢集周邊電網連接出現延遲

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 產業吸引力—五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 成本結構分析

第5章 市場規模與成長預測

- 按類型

- 機械服務

- 電力服務

- 管道服務

- 綜合機電服務

- 按服務類型

- 設計與工程

- 安裝、測試和試運行。

- 維護、修理和維修

- 託管/績效服務

- 按最終用戶行業分類

- 住宅

- 商業

- 基礎設施

- 按地區

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Grupo ECA

- ES4Q

- Propamat

- CELMEC

- Grupo Nortem

- MEPSIS

- JIC Ingenieria

- Semaica

- AECOM

- WSP

- Jacobs

- Arup

- Stantec

- Mott MacDonald

- Hatch

- Techint Engineering & Construction

- ACCIONA

- Equans Brasil

- ENGIE Solutions Brasil

- VINCI Energies Brasil

- Fluor

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america mechanical, electrical, and plumbing services market size is expected to grow from USD 12.49 billion in 2025 to USD 13.5 billion in 2026 and is forecast to reach USD 20.87 billion by 2031 at 9.10% CAGR over 2026-2031.

This report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation/Testing/Commissioning, Maintenance/Repair/Retrofit, Managed/Performance-based), End-User Industry (Residential, Commercial, Infrastructure), and Geography (Brazil, Argentina, Chile, Colombia, Peru, Rest of South America). The Market Forecasts are in Terms of Value (USD).

South America Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Commercial and Infrastructure Modernization

The South America mechanical, electrical, and plumbing (MEP) services market is drawing steady support from the region's wider modernization cycle in transport, health, water, and urban assets. Brazil's construction sector contributes close to 6% of GDP, and PAC-3 has committed USD 333 billion across transport, energy, water, and urban mobility, which is converting into multi-year MEP subcontract opportunities in hospitals, airports, metro systems, and sanitation plants. The same pattern is visible outside Brazil, where AECOM's joint venture was selected by Peru's Ministry of Health in 2024 to manage two major regional hospitals in Piura and Trujillo with responsibility across the MEP lifecycle under a BIM-led model. Brazil's position among the top five countries globally for LEED-certified buildings is also deepening the role of auditable MEP performance, because certification now depends on system outcomes rather than simple installation completion. This is extending the life of contracts in the South America mechanical, electrical, and plumbing (MEP) services market and raising the value of firms that can stay involved after handover through monitoring, recommissioning, and energy optimization. It also means that the South America mechanical, electrical, and plumbing (MEP) services market is becoming less tied to one-time construction cycles and more linked to ongoing building performance obligations.

Data Center and Logistics Facility Expansion

The South America mechanical, electrical, and plumbing (MEP) services market is gaining from the expansion of data center campuses and modern logistics facilities in Brazil and Chile. Chile's National Data Center Plan for 2024 to 2030 aims to triple the size of the sector, and projected hyperscaler investment from 2025 onward exceeds USD 8 billion, creating a sustained pipeline for cooling, power quality, backup generation, and fire suppression packages. These facilities are no longer being designed around traditional 10 kW per rack conditions, as AI-oriented halls are moving toward 100 kW per rack densities that require liquid-cooling loops, higher-voltage busways, and N+1 redundant chillers. That change is narrowing the pool of contractors capable of delivering dense mechanical and electrical packages and completing commissioning without performance failures. The South America mechanical, electrical, and plumbing (MEP) services market is therefore seeing a wider gap between standard installation vendors and specialized contractors that can work on high-density digital campuses. The same shift is spilling into adjacent logistics facilities, where operators increasingly want resilient power systems, advanced ventilation, and automation-ready service frameworks at commissioning.

FX Volatility and Inflation Pressure

FX volatility and financing costs remain a major operational brake on the South America mechanical, electrical, and plumbing (MEP) services market. Brazil's Selic rate reached 14.8% in May 2025 and the OECD expects only gradual easing, which keeps borrowing costs high for clients and compresses contractor returns on fixed-price projects that rely on imported equipment. PVC pipe prices were already up 16.3% in the 12 months to February 2026, and construction cost inflation could push the INCC to 9.7% in 2026, which puts further pressure on contracts signed before those inputs moved higher. The effect is especially visible in renewables, digital infrastructure, and other MEP-heavy projects that depend on dollar-linked components and hedging costs. In the South America mechanical, electrical, and plumbing (MEP) services market, this can lead to delayed starts, smaller scopes, or tighter bid discipline when procurement teams cannot pass cost changes through quickly. Argentina intensifies the pressure because depreciation sharply increases the local cost of high-CAPEX MEP systems relative to legacy solutions, which can shift buyers toward deferral rather than upgrade.

Other drivers and restraints analyzed in the detailed report include:

- Outsourcing of Hard Services and Lifecycle Maintenance

- Chile and Brazil Power-Linked Campus Development

- Labor Informality and Uneven Execution Quality

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mechanical Services held 37% of the South America mechanical, electrical, and plumbing (MEP) services market share in 2025, which made it the largest service cluster by type. That position reflects the large installed base of HVAC, refrigeration, and industrial process cooling equipment across commercial buildings, healthcare facilities, and digital infrastructure. The South America mechanical, electrical, and plumbing (MEP) services market continues to lean toward mechanical scopes because tropical operating conditions in Brazil and the cooling demands of high-availability facilities keep thermal management at the center of project design and maintenance. Plumbing services also retain solid relevance because Brazil still faces a major sanitation gap, with 47% of the population not connected to the sewage system, which sustains demand for water and wastewater-related retrofits and network work. Integrated MEP Services is the fastest-growing type and is projected to expand at 11.7% CAGR through 2031 as clients reduce the cost and risk of coordinating separate mechanical, electrical, and plumbing contractors.

Within the South America mechanical, electrical, and plumbing (MEP) services industry, the rise of integrated contracts is rewarding firms that can mobilize multi-discipline site teams and keep design, installation, testing, and commissioning aligned under one scope. The shift is becoming more visible in data center work, where high-density halls require simultaneous redesign of cooling loops, electrical distribution, and water management systems rather than isolated package delivery. Building owners are also using integrated contracts to reduce interface disputes, shorten handover cycles, and secure performance guarantees from one provider instead of three. That is widening the gap between firms with lifecycle capability and those that only compete on discrete installation packages in the South America mechanical, electrical, and plumbing (MEP) services market. The result is a more favorable growth path for contractors that can combine mechanical depth, electrical reliability, plumbing integration, and formal commissioning discipline in one managed offer.

List of Companies Covered in this Report:

- Grupo ECA

- ES4Q

- Propamat

- CELMEC

- Grupo Nortem

- MEPSIS

- JIC Ingenieria

- Semaica

- AECOM

- WSP

- Jacobs

- Arup

- Stantec

- Mott MacDonald

- Hatch

- Techint Engineering & Construction

- ACCIONA

- Equans Brasil

- ENGIE Solutions Brasil

- VINCI Energies Brasil

- Fluor

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Commercial and Infrastructure Modernization

- 4.2.2 Data Center and Logistics Facility Expansion

- 4.2.3 Outsourcing of Hard Services and Lifecycle Maintenance

- 4.2.4 Chile and Brazil Power-Linked Campus Development

- 4.2.5 ESG-Driven Energy and Refrigerant Audit Scopes

- 4.2.6 Water Resilience and Closed-Loop Cooling Retrofits

- 4.3 Market Restraints

- 4.3.1 FX Volatility and Inflation Pressure

- 4.3.2 Labor Informality and Uneven Execution Quality

- 4.3.3 Fragmented Building and Fire-Code Enforcement

- 4.3.4 Grid Interconnection Delays Near Digital Clusters

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Cost Structure Analysis

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Type

- 5.1.1 Mechanical Services

- 5.1.2 Electrical Services

- 5.1.3 Plumbing Services

- 5.1.4 Integrated MEP Services

- 5.2 By Service Type

- 5.2.1 Design & Engineering

- 5.2.2 Installation, Testing, and Commissioning

- 5.2.3 Maintenance, Repair, and Retrofit

- 5.2.4 Managed / Performance-based Services

- 5.3 By End-User Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Grupo ECA

- 6.4.2 ES4Q

- 6.4.3 Propamat

- 6.4.4 CELMEC

- 6.4.5 Grupo Nortem

- 6.4.6 MEPSIS

- 6.4.7 JIC Ingenieria

- 6.4.8 Semaica

- 6.4.9 AECOM

- 6.4.10 WSP

- 6.4.11 Jacobs

- 6.4.12 Arup

- 6.4.13 Stantec

- 6.4.14 Mott MacDonald

- 6.4.15 Hatch

- 6.4.16 Techint Engineering & Construction

- 6.4.17 ACCIONA

- 6.4.18 Equans Brasil

- 6.4.19 ENGIE Solutions Brasil

- 6.4.20 VINCI Energies Brasil

- 6.4.21 Fluor

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

中東歐機械、電氣和管道 (MEP) 服務:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)東協機械、電氣和管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和北非地區的機電管道(MEP)服務:市場佔有率分析、行業趨勢與統計數據以及成長預測(2026-2031 年)亞太地區機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中東歐機械、電氣和管道 (MEP) 服務:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)東協機械、電氣和管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和北非地區的機電管道(MEP)服務:市場佔有率分析、行業趨勢與統計數據以及成長預測(2026-2031 年)亞太地區機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 機械、電氣和管道服務市場:按服務類型、最終用戶和地區分類

機械、電氣和管道服務市場:按服務類型、最終用戶和地區分類 機械、電氣和管道服務市場:按服務類型、服務形式、計劃規模、技術和建築類型分類-2026-2032年全球市場預測

機械、電氣和管道服務市場:按服務類型、服務形式、計劃規模、技術和建築類型分類-2026-2032年全球市場預測 2026年全球機械、電氣和管道(MEP)服務市場報告2026年全球管道服務軟體市場報告

2026年全球機械、電氣和管道(MEP)服務市場報告2026年全球管道服務軟體市場報告