|

市場調查報告書

商品編碼

2064376

亞太地區機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Asia-Pacific Mechanical, Electrical, And Plumbing (MEP) Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

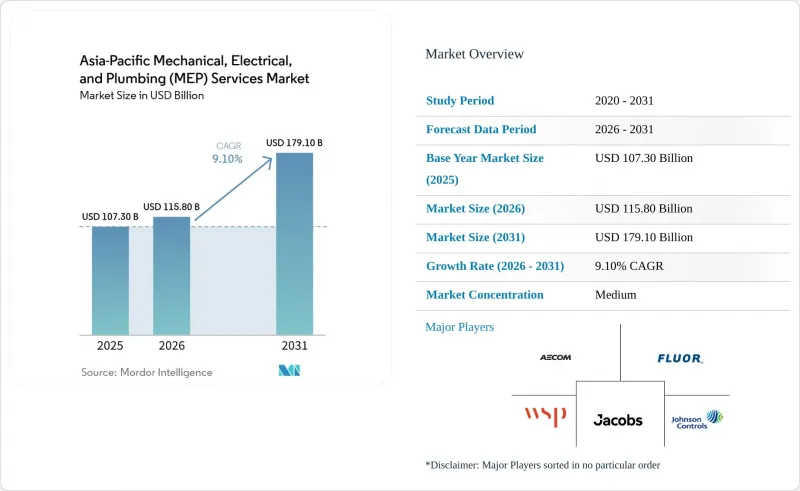

根據 Mordor Intelligence 預測,亞太地區機械、電氣和管道 (MEP) 服務市場規模預計將在 2025 年達到 1,073 億美元,在 2026 年達到 1,158 億美元,在 2031 年達到 1,791 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 9.10%。

本報告按類型(機械、電氣、給排水、機電一體化)、服務類型(設計與工程、安裝、測試與試運行、維護與維修等)、最終用戶行業(住宅、商業、基礎設施)以及地區(中國、印度、日本、韓國、澳大利亞、印尼及其他亞太地區)進行細分。市場預測以美元計價。

亞太地區機械、電氣及管道(MEP)服務市場趨勢及分析

用於交通運輸主導的城市大型企劃的支出

即使私人建設週期放緩,政府基礎建設項目仍持續支撐著亞太地區的機電工程服務市場。越南已批准興建連接老街、河內和海防的標準軌鐵路,計劃於2025年動工。工程包括174座橋樑及55條隧道,施工階段需隧道通風、消防、安全、牽引動力及相關系統。大規模交通基礎設施專案更青睞能夠協調單一範圍內多個系統的承包商,而不是按類型分類工作。這有利於擁有鐵路級認證、具備整條線路系統實施經驗以及試運行記錄的公司,尤其是在東協部分地區,這類人才仍然稀缺。因此,公共交通支出持續為亞太地區(包括澳洲、越南、泰國和印度)的機電工程服務市場創造高價值的商業機會。

資料中心和半導體設施建設的擴建

關鍵任務設施仍然是亞太地區機電工程服務市場成長最顯著的領域之一。與傳統伺服器機房相比,人工智慧賦能的資料中心需要更高密度的電力、冷卻、備份和控制架構,這就要求承包商重新設計整個服務佈局,而不僅僅是簡單地套用標準的辦公室機電工程模板。江森自控承諾在未來五年內投資高達6000萬美元,用於擴建其位於新加坡的創新中心,預計將於2026年完工,重點發展先進的冷卻和溫度控管,以滿足該地區資料中心的需求。半導體專案也在推動需求成長,因為無塵室空調、超純水管道和高可用性電氣系統對性能的要求比普通商業建築更為嚴格。東協投資報告也重點介紹了幾個重要的製造業項目,包括台積電在新加坡投資43億美元的工廠、英飛凌在馬來西亞投資54億美元的碳化矽(SiC)產能擴建項目以及聯華電子在新加坡投資50億美元的工廠。因此,亞太地區的機電服務市場正朝著更專業化的工程、更嚴格的試運行和更強大的整合交付能力的方向發展。

技術工人短缺和工資上漲

勞動力短缺仍然是亞太地區機電工程服務市場面臨的最嚴峻的交付限制因素之一。在亞太地區最繁忙的地區,尤其是在交通、能源、工業和建築項目同時進行的情況下,電工、暖通空調技師、水管工和消防安全專家等人員尤其難以招募。勞動力短缺導致人事費用和加班費增加,承包商不得不更加依賴外籍勞工和專業分包團隊。更大的問題在於合約簽訂時間,因為許多項目的價格早在現場施工開始之前就已經確定。這種不匹配會導致固定價格項目的利潤率降低,並減緩亞太地區機電工程服務市場產能的擴張,即使市場需求強勁也是如此。

細分市場分析

到2025年,機械安裝服務將佔亞太地區機電工程服務市場佔有率的41%,其中冷凍和通風工程仍將是該地區專案支出的核心。人口密集的城市市場需求最為強勁,在這些市場中,暖通空調、冷凍水循環系統和區域供冷系統在建築安裝價值中佔據相當大的比例。此外,機械安裝的範圍在合規性方面仍然至關重要,因為節能維修通常從冷卻器、水泵、空氣側系統和控制系統入手,而不是僅僅進行表面維修。電氣安裝服務和給排水服務是接下來的主要類別,資料中心、工業設施和高層建築專案都需要可靠的電力和供水系統,因此對這兩類服務的需求特別旺盛。

隨著開發商轉向複雜設施的總價合約模式,預計到2031年,亞太地區機電工程服務市場規模結構中,整合機電工程服務將以11.65%的複合年成長率成長。這反映了人們對協調風險、返工和專案延誤的擔憂,這些風險和延誤通常是由於多個專家在不同的專業領域工作造成的。在亞太地區的機電工程服務業,具備BIM就緒能力、干擾檢測能力和端到端執行能力的公司比僅提供單一專業的公司更具優勢。這種優勢在交通運輸系統、資料中心和半導體設施等領域尤其顯著,因為這些領域的服務密度高,後期變更成本高。因此,儘管機械、電氣和管道方面的專業知識在最終方案中仍然至關重要,但亞太地區的機電工程服務市場正在朝著減少介面和大規模整合專案的方向發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 用於交通運輸主導的城市大型企劃的支出

- 資料中心和半導體設施建設的擴建

- 綠建築計劃和更嚴格的冷媒法規

- 向東協和印度轉移產業

- 公共工程強制實施BIM及引進預製機電系統

- 加快區域冷卻和熱泵系統的維修。

- 市場限制因素

- 技術工人短缺和工資上漲

- 銅、開關設備和暖通空調組件的價格波動

- 跨境代碼片段化與本地內容監管

- 關鍵任務項目中公用設施連接方面的瓶頸

- 價值鍊和供應鏈分析

- 監理情勢

- 技術展望

- 產業吸引力:波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 成本結構分析

第5章:預測市場規模與成長率

- 按類型

- 機械服務

- 電力服務

- 管道服務

- 綜合機電服務

- 按服務類型

- 設計與工程

- 安裝、測試和試運行

- 維護/修理

- 託管/績效服務

- 按最終用戶行業分類

- 住宅

- 商業

- 基礎設施

- 按地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AECOM

- WSP Global

- Jacobs

- Fluor Corporation

- Johnson Controls

- Honeywell Building Solutions

- Siemens Smart Infrastructure

- Larsen & Toubro Construction

- Voltas Limited

- Sterling and Wilson

- Shinryo Corporation

- Meinhardt Group

- Surbana Jurong

- Arup

- Aurecon

- Mott MacDonald

- Tata Projects

- Beca Group

- Nippon Koei

- Obayashi Corporation

- Gammon Construction

- Kinden Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific mechanical, electrical, and plumbing services market size is projected to be USD 107.30 billion in 2025, USD 115.80 billion in 2026, and reach USD 179.10 billion by 2031, growing at a CAGR of 9.10% from 2026 to 2031.

This report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation Testing & Commissioning, Maintenance & Repair Among Others), End-User Industry (Residential, Commercial, Infrastructure), and Geography (China, India, Japan, South Korea, Australia, Indonesia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Transit-Led Urban Megaproject Spending

Government infrastructure pipelines continue to support the Asia-Pacific MEP services market, even as private construction cycles lose momentum. Vietnam approved the Lao Cai to Hanoi to Hai Phong standard-gauge railway in 2025, and the project includes 174 bridges and 55 tunnels that will require tunnel ventilation, fire-life-safety, traction power, and related systems during delivery. Large transit packages also favor contractors that can coordinate multiple systems within one scope instead of splitting the work trade by trade. That supports firms with railway-grade certifications, linewide systems experience, and proven commissioning depth, especially in parts of ASEAN where that talent pool remains limited. The result is that public transport spending continues to create high-value opportunities in the Asia-Pacific MEP services market across Australia, Vietnam, Thailand, and India.

Data-Center and Semiconductor Facility Build-Out

Mission-critical facilities remain one of the clearest growth pockets in the Asia-Pacific MEP services market. AI-ready data centers require denser power, cooling, backup, and control architectures than legacy server rooms, so contractors must redesign entire service layouts rather than repeating standard office MEP templates. Johnson Controls committed up to USD 60 million over 5 years in 2026 to expand its Singapore Innovation Center, with the site focused on advanced cooling and thermal management to meet regional data center demand. Semiconductor projects add a parallel stream because cleanroom HVAC, ultra-pure water plumbing, and high-availability electrical systems require tighter performance standards than ordinary commercial buildings. ASEAN investment reporting also highlighted major manufacturing projects, including TSMC's USD 4.3 billion Singapore fab, Infineon's USD 5.4 billion Malaysian silicon carbide expansion, and United Microelectronics' USD 5 billion Singapore facility. This is pushing the Asia-Pacific MEP services market toward more specialized engineering, tighter commissioning, and stronger integrated delivery capability.

Skilled-Trade Shortages and Wage Inflation

Labor availability remains one of the clearest delivery limits in the Asia-Pacific MEP services market. Electrical installers, HVAC technicians, plumbing crews, and fire-protection specialists are difficult to secure in the region's busiest hubs, especially when transport, energy, industrial, and building programs move forward at the same time. Tight labor conditions raise wage bills, increase overtime exposure, and push contractors to rely more heavily on imported labor or specialist subcontract crews. The larger problem is contract timing because many jobs are priced well before site execution begins. That mismatch can turn fixed-price work into margin loss and it slows capacity expansion across the Asia-Pacific MEP services market even when demand conditions are strong.

Other drivers and restraints analyzed in the detailed report include:

- Green-Building and Refrigerant Compliance Tightening

- Industrial Relocation into ASEAN and India

- Copper, Switchgear, and HVAC Component Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mechanical Services held 41% of Asia-Pacific MEP services market share in 2025, which kept cooling and ventilation work at the center of regional project spend. Demand remains strongest in dense urban markets where HVAC, chilled-water loops, and district cooling systems account for a large share of installed building value. Mechanical scope also stays central to compliance because energy retrofits usually begin with chillers, pumps, air-side systems, and controls rather than with cosmetic upgrades. Electrical Services and Plumbing Services followed as the next-largest categories, both supported by data centers, industrial facilities, and high-rise projects that require reliable power and water systems.

Integrated MEP Services is projected to grow at 11.65% CAGR within the Asia-Pacific MEP services market size mix through 2031 as developers shift toward single-package awards on complex facilities. This reflects concern over coordination risk, rework, and schedule slippage when multiple trade contractors operate under separate scopes. In the Asia-Pacific MEP services industry, firms with BIM capability, clash detection, and full-cycle execution are gaining ground on companies that supply only one trade. That advantage is strongest on transit systems, data centers, and semiconductor facilities, where service density is great and late-stage changes are expensive. The Asia-Pacific MEP services market is therefore moving toward fewer interfaces and larger integrated mandates, even though mechanical, electrical, and plumbing specialization still matter within the final package.

List of Companies Covered in this Report:

- AECOM

- WSP Global

- Jacobs

- Fluor Corporation

- Johnson Controls

- Honeywell Building Solutions

- Siemens Smart Infrastructure

- Larsen & Toubro Construction

- Voltas Limited

- Sterling and Wilson

- Shinryo Corporation

- Meinhardt Group

- Surbana Jurong

- Arup

- Aurecon

- Mott MacDonald

- Tata Projects

- Beca Group

- Nippon Koei

- Obayashi Corporation

- Gammon Construction

- Kinden Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Transit-Led Urban Megaproject Spending

- 4.2.2 Data-Center and Semiconductor Facility Build-Out

- 4.2.3 Green-Building and Refrigerant Compliance Tightening

- 4.2.4 Industrial Relocation into ASEAN and India

- 4.2.5 Public-Project BIM Mandates and Prefab MEP Adoption

- 4.2.6 District Cooling and Heat-Pump Retrofit Acceleration

- 4.3 Market Restraints

- 4.3.1 Skilled-Trade Shortages and Wage Inflation

- 4.3.2 Copper, Switchgear, and HVAC Component Volatility

- 4.3.3 Cross-Border Code Fragmentation and Local-Content Rules

- 4.3.4 Utility-Connection Bottlenecks for Mission-Critical Projects

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Cost Structure Analysis

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Type

- 5.1.1 Mechanical Services

- 5.1.2 Electrical Services

- 5.1.3 Plumbing Services

- 5.1.4 Integrated MEP Services

- 5.2 By Service Type

- 5.2.1 Design & Engineering

- 5.2.2 Installation, Testing, and Commissioning

- 5.2.3 Maintenance & Repair

- 5.2.4 Managed / Performance-based Services

- 5.3 By End-User Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Indonesia

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 AECOM

- 6.4.2 WSP Global

- 6.4.3 Jacobs

- 6.4.4 Fluor Corporation

- 6.4.5 Johnson Controls

- 6.4.6 Honeywell Building Solutions

- 6.4.7 Siemens Smart Infrastructure

- 6.4.8 Larsen & Toubro Construction

- 6.4.9 Voltas Limited

- 6.4.10 Sterling and Wilson

- 6.4.11 Shinryo Corporation

- 6.4.12 Meinhardt Group

- 6.4.13 Surbana Jurong

- 6.4.14 Arup

- 6.4.15 Aurecon

- 6.4.16 Mott MacDonald

- 6.4.17 Tata Projects

- 6.4.18 Beca Group

- 6.4.19 Nippon Koei

- 6.4.20 Obayashi Corporation

- 6.4.21 Gammon Construction

- 6.4.22 Kinden Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

中東歐機械、電氣和管道 (MEP) 服務:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)東協機械、電氣和管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和北非地區的機電管道(MEP)服務:市場佔有率分析、行業趨勢與統計數據以及成長預測(2026-2031 年)歐洲機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)南美洲機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中東歐機械、電氣和管道 (MEP) 服務:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)東協機械、電氣和管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和北非地區的機電管道(MEP)服務:市場佔有率分析、行業趨勢與統計數據以及成長預測(2026-2031 年)歐洲機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)南美洲機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 機械、電氣和管道服務市場:按服務類型、最終用戶和地區分類

機械、電氣和管道服務市場:按服務類型、最終用戶和地區分類 機械、電氣和管道服務市場:按服務類型、服務形式、計劃規模、技術和建築類型分類-2026-2032年全球市場預測

機械、電氣和管道服務市場:按服務類型、服務形式、計劃規模、技術和建築類型分類-2026-2032年全球市場預測 2026年全球機械、電氣和管道(MEP)服務市場報告2026年全球管道服務軟體市場報告

2026年全球機械、電氣和管道(MEP)服務市場報告2026年全球管道服務軟體市場報告