|

市場調查報告書

商品編碼

2064002

北美機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)North America Mechanical, Electrical, Plumbing (MEP) Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

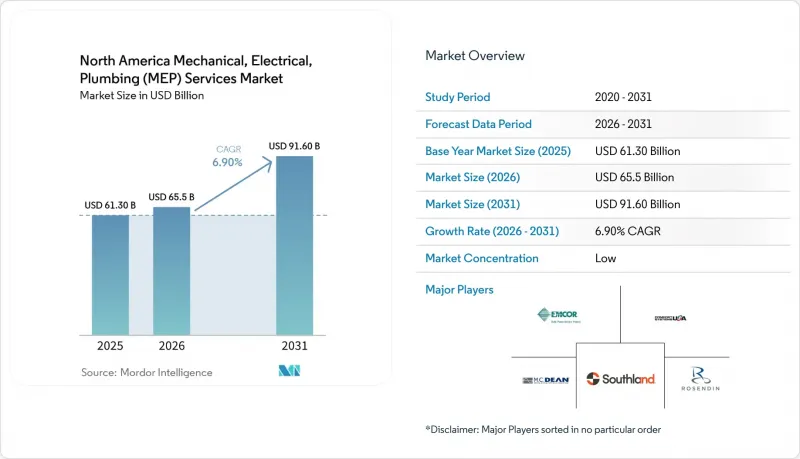

根據 Mordor Intelligence 預測,北美機械、電氣和管道 (MEP) 服務市場將從 2025 年的 613 億美元成長到 2026 年的 655 億美元,到 2031 年達到 916 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 6.90%。

本報告按類型(機械、電氣、管道、一體化機電)、服務類型(設計與工程、安裝、測試與試運行、維護、維修與維修、管理型和績效型)、最終用戶行業(住宅、商業、基礎設施)以及地區(美國、加拿大、墨西哥)進行細分。市場預測以美元計價。

北美機電管道(MEP)服務市場趨勢與洞察

聯邦和州基礎設施資金

聯邦預算撥款支持涉及大規模機電管道工程的項目類別,為北美機電工程服務市場創造了長期成長潛力。 《通貨膨脹控制與投資法案》(IIJA)授權建造主要公路和交通基礎設施,而美國運輸部(DOT)的數據顯示,到2026年4月,所有項目的支出義務將達到4902億美元,其中2186億美元已支出。這證實了支出已從宣布階段進入實際執行階段。對機電工程承包商而言,支出最關鍵的領域是交通基礎設施、雨水排放系統、污水處理廠、抽水站和公共建築。在這些設施中,電力分配、控制、管道、通風和消防系統都已納入核心工作範圍,而不是後期添加。美國環保署(EPA)的撥款模式也支持這一觀點。該機構已支持超過1200個飲用水週轉基金項目,撥款150億美元用於更換鉛水管,這些項目主要集中在管道工程方面。聯邦政府為許多城市計畫提供80%的資金,也減少了地方政府資金籌措的阻力。這縮短了採購週期,使得以機電工程為中心的公共工程專案能夠比以往的基礎設施建設週期更快地推進。這個因素也解釋了北美機電工程服務市場累積訂單的可見性,因為公共工程通常需要經歷設計、採購、安裝和試運行等多個階段,從而將商機分散到多個合約期間。

資料中心和電動車充電基礎設施的開發

北美機電工程服務市場也受到資料中心和電動車充電基礎設施建設浪潮的推動,這些基礎設施的電力消耗量標準商業建築。配電室、中壓配電、變電站、開關設備、直接液冷迴路、備用系統和控制平台如今已成為超大規模專案的關鍵路徑,使得專案價值的更大比例轉移到了機電工程領域。 2025年11月,亞馬遜宣佈在印第安納州北部投資150億美元興建資料中心園區。同樣在2025年7月,CyrusOne與Calpine合作,宣佈在德克薩斯州投資12億美元建設一個超大規模資料中心項目,初始容量為190兆瓦。這兩個項目都清楚地展現了當前電力和冷卻需求的規模。這些專案不僅規模不斷擴大,技術複雜性也在不斷提升,因為要實現高密度機架安裝和可靠的正常運作目標,就需要電氣設計、冷卻、控制和試運行之間更加緊密的協調。此外,電動車充電也帶來了新的挑戰。根據2026年版《美國國家電氣規範》(NEC),商業和公共設施對服務升級、緊急切斷措施以及與建築負載管理策略的協調需求日益成長。因此,北美機電工程服務市場不僅面臨來自安裝商的需求成長,也面臨來自能夠在緊迫的工期內設計、管理和試運行高度整合系統的公司的需求成長。

專業技術純熟勞工短缺

由於熟練勞動力需求持續超過供應,人力資源保障仍是北美機電工程服務市場最明顯的短期限制。根據美國總承包商協會 (AGC) 和美國國家建築工程與工程研究中心 (NCCER) 2025 年的勞動力調查,92% 的企業將面臨招聘小時工的困難,其中超過 75% 的企業表示,電工、水管工和水務工人尤其難以招聘。美國承包商學院 (ABC) 指出,到 2026 年,建設產業需要淨增加 34.9 萬名新員工,這意味著目前的招募速度不足以滿足專案需求。資料中心建設加劇了這種勞動力緊張局面,吸引了經驗最豐富的電工、試運行專家和控制人員湧向高薪項目,導致傳統商業和公共工程領域嚴重的勞動力短缺。這種供需失衡推高了競標溢價,延長了專案工期,並促使客戶傾向於選擇擁有預製和培訓系統的大型建築商。此外,北美機電工程服務市場在整合交付方面仍有發展空間。這是因為客戶越來越傾向於選擇能夠自行解決員工調整問題的公司,而不是依賴將各個專業工種移交給外部機構。

細分市場分析

到2025年,電氣服務將佔北美機電工程(MEP)服務市場規模的35%,成為收入最高的細分市場。這一主導地位反映出,資料中心、商業設施維修和電氣化專案都將配電、控制、保護系統和設備升級置於專案預算的核心位置。 EMCOR美國電氣工程部門2026年第一季營收累計8.456億美元,年增12.8%。經營團隊將這一業績歸功於高科技製造業和資料中心活動支撐了該部門的短期需求。 2026年版《美國國家電氣規範》(NEC)也推動了該細分市場的發展。新的中壓法規、擴展的標籤要求以及電力控制系統認證將增加商業和公共設施項目的設計和現場合規工作,從而轉化為收入。此外,隨著現有建築物向熱泵、充電器、儲能系統和更先進的數位控制系統過渡,電氣服務部門將佔據顯著的價值佔有率。這是因為所有這些變更都會影響服務規模和配電架構。在北美機電工程服務市場,這將推動電氣工程在「數量」和「複雜性」方面的成長,使其比僅依賴更換需求更具優勢。

機械和工業設備服務仍然佔據第二大市場。這是因為暖通空調、消防、製程管道和關鍵任務冷卻系統是醫院、先進製造工廠和資料中心的核心。隨著機架密度增加,業主從標準風冷系統轉向液冷或液性冷卻策略,冷卻設計變得越來越複雜,需要管道、控制、電力和試運行之間更緊密的協調。雖然管道服務的收入佔有率較小,但它受益於與水基礎設施建設和鉛水管更換計劃相關的清晰更新周期,並且與許多其他非必需的建築領域相比,其來自市政當局的需求基礎更為穩定。預計到2031年,整合式機電服務將以8.86%的複合年成長率成長,是北美機電服務市場所有細分領域中成長最快的。業主更傾向於這種模式,因為單一承包商擁有明確的責任分類,可以減少協調方面的不足,縮短試運行週期,並降低複雜設施的索賠風險。這一趨勢表明,在北美機電服務業,兼具深厚技術專長和專案管理能力的公司比只提供單一服務包的公司更有價值。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 聯邦和州基礎設施資金

- 資料中心和電動車充電基礎設施的開發

- 加強對建築性能和能源的監管

- NEC和電力公司主導的電氣設備升級

- 重新設計關鍵任務冷卻系統的複雜性

- 區域城市對併網維修的需求

- 市場限制因素

- 專業技術純熟勞工短缺

- 開關設備、變壓器和銅價波動

- 高電氣化率工程中與電力公司接取的延誤

- 互聯建築系統網路安全合規的負擔

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 產業吸引力—五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 成本結構分析

第5章 市場規模與成長預測

- 按類型

- 機械服務

- 電力服務

- 管道服務

- 綜合機電服務

- 按服務類型

- 設計與工程

- 安裝、測試和試運行。

- 維護、修理和維修

- 託管/績效服務

- 按最終用戶行業分類

- 住宅

- 商業

- 基礎設施

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- EMCOR Group

- Comfort Systems USA

- Southland Industries

- MC Dean

- Rosendin Electric

- ArchKey Solutions

- TDIndustries

- Brandt

- McKinstry

- ACCO Engineered Systems

- Power Design

- Limbach Holdings

- AECOM

- WSP

- Jacobs

- Stantec

- Bowman Consulting Group

- Kimley-Horn

- Galloway & Company

- McGill Associates

- Prime Electric

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america mechanical, electrical, plumbing services market size is expected to increase from USD 61.30 billion in 2025 to USD 65.5 billion in 2026 and reach USD 91.60 billion by 2031, growing at a CAGR of 6.90% over 2026-2031.

This report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design and Engineering, Installation, Testing and Commissioning, Maintenance, Repair and Retrofit, Managed and Performance-Based), End-User Industry (Residential, Commercial, Infrastructure), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Mechanical, Electrical, Plumbing (MEP) Services Market Trends and Insights

Federal and State Infrastructure Funding

Federal appropriations are giving the North America MEP services market a long runway because they support project categories that carry large mechanical, electrical, and plumbing packages. The IIJA includes major highway and transportation authorization, and DOT data showed USD 490.2 billion obligated and USD 218.6 billion outlaid across programs by April 2026, which confirms that spending has moved beyond announcement into active execution. For MEP contractors, spending matters most in transit facilities, stormwater systems, treatment plants, pump stations, and public buildings, where electrical distribution, controls, piping, ventilation, and fire protection are built into the core scope rather than added later. The EPA's funding pattern reinforces that view because it had already supported more than 1,200 drinking water revolving fund projects and designated USD 15 billion for lead service line replacement, which is overwhelmingly plumbing-intensive work. The 80% federal cost share on many urban projects also reduces local funding friction, which shortens procurement cycles and moves MEP-heavy public jobs forward faster than in prior infrastructure cycles. This driver supports backlog visibility in the North America MEP services market because public projects usually extend across multi-year design, procurement, installation, and commissioning phases, which spreads revenue opportunities across more than one contracting season.

Data Center and EV Charging Build-out

The North America MEP services market is also being lifted by a data center and EV charging wave that is far more power-intensive than standard commercial construction. Electrical rooms, medium-voltage distribution, substations, switchgear, direct liquid cooling loops, backup systems, and control platforms now define the critical path on hyperscale projects, which shifts a larger share of project value into MEP scope. Amazon announced a USD 15 billion investment in Northern Indiana data center campuses in November 2025, and CyrusOne, with Calpine, announced a USD 1.2 billion hyperscale data center project in Texas with 190 MW of initial capacity in July 2025, both of which illustrate the scale of current power and cooling requirements. These projects not only increase volume, but they also raise technical complexity because dense racks and resilient uptime targets demand closer integration between electrical design, cooling, controls, and commissioning. EV charging adds another layer because commercial and institutional sites increasingly need service upgrades, emergency disconnect arrangements, and coordination with building load management strategies under the 2026 NEC. The result is that the North America MEP services market is seeing stronger demand not just for installers, but also for firms that can engineer, sequence, and commission tightly integrated systems on compressed schedules.

Skilled Labor Shortages in Specialty Trades

Labor availability remains the clearest short-term constraint on the North America MEP services market because demand is rising faster than the skilled workforce pipeline. The 2025 AGC and NCCER workforce survey found that 92% of firms had difficulty filling hourly craft positions, and more than 75% specifically cited electricians, pipefitters, and plumbers as hard to recruit. Associated Builders and Contractors said the construction industry must attract 349,000 net new workers in 2026, which shows that current hiring flows are not enough to meet project demand. Data center construction worsens the strain because it pulls the most experienced electricians, commissioning specialists, and controls staff toward high-pay projects, leaving conventional commercial and institutional work with tighter labor pools. That imbalance raises bid premiums, extends schedules, and pushes owners toward larger contractors with prefabrication and workforce training systems. It also creates room for integrated delivery in the North America MEP services market because owners increasingly value firms that can solve labor coordination internally rather than depend on separate trade handoffs.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Building Performance and Energy Codes

- NEC and Utility-Driven Electrical Service Upgrades

- Switchgear, Transformer, and Copper Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrical Services held 35% of the North America MEP services market size in 2025, which made it the largest type segment by revenue. That leadership reflects the fact that data centers, commercial retrofits, and electrification programs all place power distribution, controls, protection systems, and service upgrades near the center of project budgets. EMCOR's U.S. Electrical Construction segment generated USD 845.6 million in Q1 2026 revenue, up 12.8% year on year, and management linked that performance to high-tech manufacturing and data center activity, which supports the segment's near-term demand base. The 2026 NEC further supports the segment because new medium-voltage provisions, expanded labeling requirements, and power control system recognition raise billable design and field compliance work on commercial and institutional projects. Electrical Services also captures a large share of value when existing buildings shift toward heat pumps, chargers, storage, and more digital controls, since all of those changes affect service sizing and distribution architecture. In the North America MEP services market, that makes electrical scope both volume-led and complexity-led, which is a stronger position than relying on replacement demand alone.

Mechanical Services remains the second-largest type because HVAC, fire protection, process piping, and mission-critical cooling sit at the center of hospitals, advanced manufacturing plants, and data centers. Cooling design is becoming more complex as rack densities rise and owners move from standard air systems toward liquid-assisted or liquid-based cooling strategies, which raises the need for tighter coordination between piping, controls, power, and commissioning. Plumbing Services is smaller by revenue share, but it benefits from clear replacement cycles tied to water infrastructure work and lead service line programs, which gives it a steadier municipal demand base than many discretionary building categories. Integrated MEP Services is projected to grow at an 8.86% CAGR through 2031, the fastest pace among type segments in the North America MEP services market. Owners are leaning toward this model because one accountable delivery party reduces coordination gaps, shortens commissioning time, and lowers claims risk on complex facilities. That shift suggests the North America MEP services industry is rewarding firms that can combine trade depth with program management rather than firms that only provide isolated packages.

List of Companies Covered in this Report:

- EMCOR Group

- Comfort Systems USA

- Southland Industries

- M.C. Dean

- Rosendin Electric

- ArchKey Solutions

- TDIndustries

- Brandt

- McKinstry

- ACCO Engineered Systems

- Power Design

- Limbach Holdings

- AECOM

- WSP

- Jacobs

- Stantec

- Bowman Consulting Group

- Kimley-Horn

- Galloway & Company

- McGill Associates

- Prime Electric

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal and State Infrastructure Funding

- 4.2.2 Data Center and EV Charging Build-Out

- 4.2.3 Stricter Building Performance and Energy Codes

- 4.2.4 NEC and Utility-Driven Electrical Service Upgrades

- 4.2.5 Mission-Critical Cooling Redesign Complexity

- 4.2.6 Grid-Interactive Retrofit Demand in Secondary Cities

- 4.3 Market Restraints

- 4.3.1 Skilled Labor Shortages in Specialty Trades

- 4.3.2 Switchgear, Transformer, and Copper Price Volatility

- 4.3.3 Utility Interconnection Delays for Electrification-Heavy Projects

- 4.3.4 Cybersecurity Compliance Burden for Connected Building Systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Cost Structure Analysis

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Type

- 5.1.1 Mechanical Services

- 5.1.2 Electrical Services

- 5.1.3 Plumbing Services

- 5.1.4 Integrated MEP Services

- 5.2 By Service Type

- 5.2.1 Design & Engineering

- 5.2.2 Installation, Testing, and Commissioning

- 5.2.3 Maintenance, Repair, and Retrofit

- 5.2.4 Managed / Performance-based Services

- 5.3 By End-User Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 EMCOR Group

- 6.4.2 Comfort Systems USA

- 6.4.3 Southland Industries

- 6.4.4 M.C. Dean

- 6.4.5 Rosendin Electric

- 6.4.6 ArchKey Solutions

- 6.4.7 TDIndustries

- 6.4.8 Brandt

- 6.4.9 McKinstry

- 6.4.10 ACCO Engineered Systems

- 6.4.11 Power Design

- 6.4.12 Limbach Holdings

- 6.4.13 AECOM

- 6.4.14 WSP

- 6.4.15 Jacobs

- 6.4.16 Stantec

- 6.4.17 Bowman Consulting Group

- 6.4.18 Kimley-Horn

- 6.4.19 Galloway & Company

- 6.4.20 McGill Associates

- 6.4.21 Prime Electric

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

中東歐機械、電氣和管道 (MEP) 服務:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)東協機械、電氣和管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和北非地區的機電管道(MEP)服務:市場佔有率分析、行業趨勢與統計數據以及成長預測(2026-2031 年)亞太地區機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中東歐機械、電氣和管道 (MEP) 服務:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)東協機械、電氣和管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和北非地區的機電管道(MEP)服務:市場佔有率分析、行業趨勢與統計數據以及成長預測(2026-2031 年)亞太地區機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 機械、電氣和管道服務市場:按服務類型、最終用戶和地區分類

機械、電氣和管道服務市場:按服務類型、最終用戶和地區分類 機械、電氣和管道服務市場:按服務類型、服務形式、計劃規模、技術和建築類型分類-2026-2032年全球市場預測

機械、電氣和管道服務市場:按服務類型、服務形式、計劃規模、技術和建築類型分類-2026-2032年全球市場預測 2026年全球機械、電氣和管道(MEP)服務市場報告2026年全球管道服務軟體市場報告

2026年全球機械、電氣和管道(MEP)服務市場報告2026年全球管道服務軟體市場報告