|

市場調查報告書

商品編碼

2064378

歐洲機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe Mechanical, Electrical, And Plumbing (MEP) Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

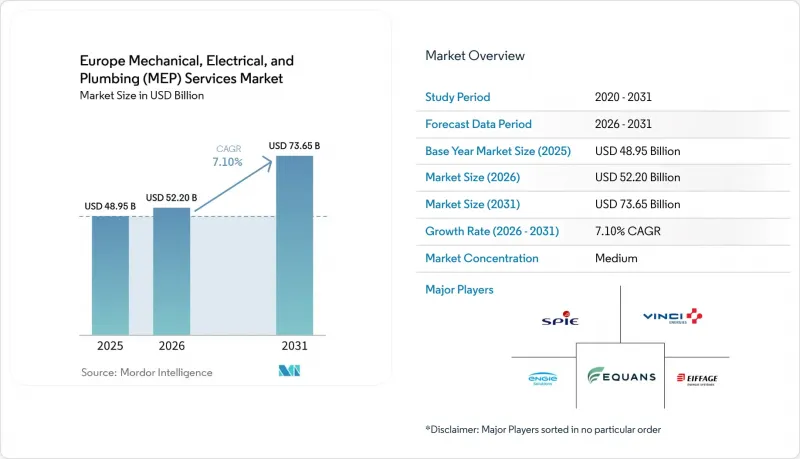

據 Mordor Intelligence 稱,2025 年歐洲機電管道 (MEP) 服務市場價值為 489.5 億美元,預計到 2031 年將達到 736.5 億美元,而 2026 年為 522 億美元,預測期(2026-2031 年)的複合年成長率為 7.10%。

本報告按類型(機械、電氣、給排水、機電一體化)、服務類型(設計與工程、安裝與試運行、維護與維修、管理服務)、最終用戶(住宅、商業、基礎設施)以及地區(德國、英國、法國、西班牙、義大利、荷蘭、瑞典、丹麥、挪威及其他歐洲國家)進行分類。預測以美元計價。

歐洲機電管道(MEP)服務市場趨勢與分析

EPBD修正案和最低能源性能標準

修訂後的《能源性能指令》(EPBD)仍然是當前週期內歐洲機電管道(MEP)服務市場面臨的最大政策障礙。該指令規定,到2030年,能源效率最低的非住宅建築中,16%必須進行維修;到2033年,這一比例需達到26%;而住宅建築的平均初級能源消耗量必須在2030年之前降低16%,到2035年降低20%至22%。成員國須在2025年12月31日前提交「國家建築維修計畫」草案,最終計畫須在2026年12月31日前提交,這將使承包商和工程公司對未來的工作量有更清晰的了解。與以往的政策週期相比,這套規則更具針對性,優先關注各國建築存量中表現最差的部分,導致大量建築需要進行大規模的MEP改造。此外,歐盟能源效率資金在2021年至2027年間大幅成長,撥款總額達1,447億歐元(1,563億美元),其中794億歐元(858億美元)撥給了建築領域的復甦與韌性基金(RRF)。這提高了全部區域項目的資金籌措潛力。因此,歐洲機電管道(MEP)服務市場將減少對短期新建專案的依賴,而更依賴現有資產的維修,以滿足監管要求。

電氣化是替代石化燃料主導維修。

根據修訂後的《能源性能指令》(EPBD)第17(15)條,對獨立式石化燃料鍋爐的財政支持將於2025年1月1日終止,電氣化正在重塑歐洲的機電管道(MEP)服務市場。歐盟熱泵銷售量預計將從2024年的211萬台回升至2025年的234萬台,來自13個歐盟成員國的快報數據顯示,2025年市場成長率將達到11%。這項轉變也改變了維修工程的範圍,因為承包商現在不僅需要簡單的鍋爐更換,還需要電氣系統升級、液壓平衡、控制系統整合和試運行。德國計畫實施的《德國現代化改造法》(GModG)框架透過收緊現代化法規和擴大低排放建築的義務,進一步強化了這一趨勢。即使技術方案不斷發展,這也將使維修活動保持活力。歐盟熱泵加速平台和未來的建築排放交易體系(ETS2)將為此方向提供進一步的政策支援。對於歐洲機電管道 (MEP) 服務市場而言,這意味著需求正在轉向更複雜、更具附加價值的維修方案。

合格維修技師短缺

在歐洲機電管道(MEP)服務市場,勞動力短缺仍然是最明顯的供應限制因素。歐盟委員會估計,至少需要新增75萬名熱泵安裝人員,並且至少50%的現有安裝人員需要接受熱泵安裝的再訓練。政策架構也承認技能障礙和缺乏一站式服務體係是維修工程實施的重大障礙,這表明該限制因素既存在於體制層面,也存在於營運層面。隨著維修工程的範圍越來越傾向於將電氣、機械、管道、自動化和控制工作整合到一個專案中,熟練工人的短缺問題如今更加嚴峻。此外,資質認證系統縮小了合格承包商的範圍,雖然提高了技術質量,但也減少了能夠競標複雜、合規性主導的專案的公司數量。儘管這維持了市場需求,但政策驅動的需求轉化為整個歐洲機電管道(MEP)服務市場訂單收入的速度正在放緩。

細分市場分析

到2025年,機械設備服務將佔歐洲機電管道(MEP)服務市場佔有率的37%,成為該地區最大的細分市場。這一主導地位反映了在當前政策組合下,暖通空調升級改造、熱泵安裝和區域供熱維修專案日益成長的趨勢。電氣和管道服務仍然是重要的相關領域,因為大多數節能維修現在都包含電力設備升級、控制線路、水力平衡調整以及供水和排水工程等內容。管道服務也受益於熱泵和低溫系統的重新設計,其中水側最佳化是工程範圍的核心部分。因此,歐洲機電管道(MEP)服務市場仍與整體系統維修緊密相關,而非單一設備的更換。

預計到2031年,整合式機電管道(MEP)服務將以9.09%的複合年成長率成長。隨著買家越來越傾向於由單一責任方負責設計、安裝、自動化和試運行,歐洲機電管道(MEP)服務市場在該領域的規模正在加速擴張。在歐洲機電管道(MEP)服務業,這種轉變在資料中心、生命科學和技術複雜的公共專案中最為明顯,因為這些專案中的介面風險會導致更高的成本。此外,德國的現代化框架正在推動對綜合服務範圍的需求,這些服務將自動化、平衡和性能標準合規性整合到一份合約中。 VINCI Energies在2025年收購德國Zimmer & Halbig和R+S的案例表明,主要企業正在建立更深入、更全面的交付能力,而不是依賴單一領域的擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- EPBD修正案和最低能源性能標準

- 電氣化是替代石化燃料主導維修。

- 建築自動化和數位化EPC的引入

- 區域和一站式服務中心維修計劃

- 大型服務業建築的智慧維修

- 重新設計以碳排放彙報為驅動的全生命週期系統

- 市場限制因素

- 合格維修技師短缺

- 對分散的現有建築存量進行大量資本投資。

- 房東與房客之間的獎勵衝突

- BACS中的資料和互通性合規負擔

- 價值鍊和供應鏈分析

- 監理情勢

- 技術展望

- 產業吸引力:五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 成本結構分析

第5章:預測市場規模與成長率

- 按類型

- 機械服務

- 電力服務

- 管道服務

- 綜合機電服務

- 按服務類型

- 設計與工程

- 安裝、測試和試運行

- 維護、修理和維修

- 託管/績效服務

- 按最終用戶行業分類

- 住宅

- 商業

- 基礎設施

- 按地區

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 瑞典

- 丹麥

- 挪威

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SPIE

- VINCI Energies

- Equans

- ENGIE Solutions

- Eiffage Energie Systemes

- Bilfinger

- Exyte

- Ramboll

- Cundall

- Arup

- WSP

- AtkinsRealis

- AECOM

- Jacobs

- Mott MacDonald

- Stantec

- Mercury Engineering

- Dornan

- Bouygues Energies & Services

- Hochtief Engineering

- Arcadis

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe mechanical, electrical, and plumbing services market size was valued at USD 48.95 billion in 2025 and is estimated to grow from USD 52.20 billion in 2026 to reach USD 73.65 billion by 2031, at a CAGR of 7.10% during the forecast period (2026-2031).

This report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation & Commissioning, Maintenance & Retrofit, Managed Services), End-User (Residential, Commercial, Infrastructure), and Geography (Germany, UK, France, Spain, Italy, Netherlands, Sweden, Denmark, Norway, Rest of Europe). Forecasts are Provided in Terms of Value (USD).

Europe Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

EPBD Recast and Minimum Energy Performance Standards

The recast EPBD remains the strongest policy driver for the Europe Mechanical, Electrical, and Plumbing (MEP) Services market in the current cycle. It requires renovating the worst-performing 16% of non-residential buildings by 2030 and 26% by 2033, while residential buildings must reduce average primary energy use by 16% by 2030 and by 20% to 22% by 2035. Member states were required to submit draft National Building Renovation Plans by December 31, 2025, and final plans are due by December 31, 2026, providing contractors and engineering firms with clearer visibility into future workloads. The rule set is more targeted than earlier policy cycles because it directs countries toward the worst-performing part of the stock first, creating a concentrated pool of buildings requiring deep MEP intervention. EU energy efficiency funding also expanded sharply for 2021 to 2027, with EUR 144.7 billion (USD 156.3 billion) allocated and EUR 79.4 billion (USD 85.8 billion) of Recovery and Resilience Facility funding directed to buildings, which improves project bankability across the region. This makes the Europe Mechanical, Electrical, and Plumbing (MEP) Services market less dependent on short new-build cycles and more dependent on compliance-led upgrades across existing assets.

Electrification Replacing Fossil Boiler-Led Retrofits

Electrification is reshaping the Europe Mechanical, Electrical, and Plumbing (MEP) Services market because financial support for stand-alone fossil fuel boilers ended from January 1, 2025 under Article 17(15) of the recast EPBD. Heat pump sales in the EU recovered to 2.34 million units in 2025 from 2.11 million units in 2024, and preliminary data from 13 EU member states pointed to 11% market growth in 2025. This shift changes the nature of retrofit scopes because contractors now need electrical upgrades, hydraulic balancing, controls integration, and commissioning rather than simple boiler replacements. Germany's planned GModG framework adds another layer by tightening modernization rules and expanding obligations for low-emission buildings, which keeps retrofit activity active even as technology choices evolve. The EU Heat Pump Accelerator Platform and the future ETS2 regime for buildings add further policy support to this direction of travel. For the Europe Mechanical, Electrical, and Plumbing (MEP) Services market, this means demand is shifting toward more complex, higher-value retrofit packages.

Shortage of Certified Retrofit Technicians

Labor availability remains the clearest delivery constraint for the Europe Mechanical, Electrical, and Plumbing (MEP) Services market. The European Commission estimates that at least 750,000 additional heat pump installers are needed, and at least 50% of current installers will need reskilling for heat pump work. The same policy framework also recognizes skills barriers and one-stop-shop gaps as material obstacles to renovation delivery, indicating that the constraint is both institutional and operational. Shortages matter more now because retrofit scopes increasingly combine electrical, mechanical, wet-services, automation, and controls work in a single project. Qualification schemes also narrow the eligible contractor base, thereby improving technical quality but reducing the number of firms that can bid for complex compliance-led projects. This keeps demand intact but slows conversion of policy demand into booked revenue across the Europe Mechanical, Electrical, and Plumbing (MEP) Services market.

Other drivers and restraints analyzed in the detailed report include:

- Building Automation and Digital EPC Rollout

- District and One-Stop-Shop Renovation Programs

- High Capex Across Fragmented Legacy Building Stock

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mechanical Services held 37% of the Europe Mechanical, Electrical, and Plumbing (MEP) Services market share in 2025, which made it the largest type segment in the region. This lead reflects HVAC replacement cycles, heat pump adoption, and district heating retrofit work that are all moving higher under the current policy mix. Electrical Services and Plumbing Services remain important adjacent volumes because most energy upgrades now involve power upgrades, controls wiring, hydraulic balancing, and wet-services work in the same package. Plumbing Services also benefits from the move toward heat pump and low-temperature system redesign, where water-side optimization becomes part of the core engineering scope. This keeps the Europe Mechanical, Electrical, and Plumbing (MEP) Services market firmly tied to whole-system retrofits rather than isolated equipment replacements.

Integrated MEP Services is projected to grow at a 9.09% CAGR through 2031, and the Europe Mechanical, Electrical, and Plumbing (MEP) Services market size for this segment is expanding faster because buyers want single-point responsibility for design, installation, automation, and commissioning. Within the Europe Mechanical, Electrical, and Plumbing (MEP) Services industry, this shift is most visible in data centers, life sciences, and technically demanding public projects where interface risk is costly. Germany's modernization framework is also increasing the need for bundled scopes that combine automation, balancing, and performance compliance in the same contract. VINCI Energies' 2025 acquisitions of Zimmer & Halbig and R+S in Germany show how major players are building deeper integrated delivery capacity rather than relying on single-trade expansion.

List of Companies Covered in this Report:

- SPIE

- VINCI Energies

- Equans

- ENGIE Solutions

- Eiffage Energie Systemes

- Bilfinger

- Exyte

- Ramboll

- Cundall

- Arup

- WSP

- AtkinsRealis

- AECOM

- Jacobs

- Mott MacDonald

- Stantec

- Mercury Engineering

- Dornan

- Bouygues Energies & Services

- Hochtief Engineering

- Arcadis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EPBD Recast and Minimum Energy Performance Standards

- 4.2.2 Electrification Replacing Fossil Boiler-Led Retrofits

- 4.2.3 Building Automation and Digital EPC Rollout

- 4.2.4 District And One-Stop-Shop Renovation Programs

- 4.2.5 Smart Readiness Upgrades in Large Tertiary Buildings

- 4.2.6 Whole-Life Carbon Reporting Driving System Redesign

- 4.3 Market Restraints

- 4.3.1 Shortage of Certified Retrofit Technicians

- 4.3.2 High Capex Across Fragmented Legacy Building Stock

- 4.3.3 Split Incentives Between Landlords and Tenants

- 4.3.4 Data and Interoperability Compliance Burden for BACS

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Cost Structure Analysis

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Type

- 5.1.1 Mechanical Services

- 5.1.2 Electrical Services

- 5.1.3 Plumbing Services

- 5.1.4 Integrated MEP Services

- 5.2 By Service Type

- 5.2.1 Design & Engineering

- 5.2.2 Installation, Testing, and Commissioning

- 5.2.3 Maintenance, Repair, and Retrofit

- 5.2.4 Managed / Performance-based Services

- 5.3 By End-User Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Spain

- 5.4.5 Italy

- 5.4.6 Netherlands

- 5.4.7 Sweden

- 5.4.8 Denmark

- 5.4.9 Norway

- 5.4.10 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 SPIE

- 6.4.2 VINCI Energies

- 6.4.3 Equans

- 6.4.4 ENGIE Solutions

- 6.4.5 Eiffage Energie Systemes

- 6.4.6 Bilfinger

- 6.4.7 Exyte

- 6.4.8 Ramboll

- 6.4.9 Cundall

- 6.4.10 Arup

- 6.4.11 WSP

- 6.4.12 AtkinsRealis

- 6.4.13 AECOM

- 6.4.14 Jacobs

- 6.4.15 Mott MacDonald

- 6.4.16 Stantec

- 6.4.17 Mercury Engineering

- 6.4.18 Dornan

- 6.4.19 Bouygues Energies & Services

- 6.4.20 Hochtief Engineering

- 6.4.21 Arcadis

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

中東歐機械、電氣和管道 (MEP) 服務:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)東協機械、電氣和管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和北非地區的機電管道(MEP)服務:市場佔有率分析、行業趨勢與統計數據以及成長預測(2026-2031 年)亞太地區機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)北美機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)南美洲機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中東歐機械、電氣和管道 (MEP) 服務:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)東協機械、電氣和管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和北非地區的機電管道(MEP)服務:市場佔有率分析、行業趨勢與統計數據以及成長預測(2026-2031 年)亞太地區機電管道(MEP)服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)北美機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)南美洲機電管道(MEP)服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 機械、電氣和管道服務市場:按服務類型、最終用戶和地區分類

機械、電氣和管道服務市場:按服務類型、最終用戶和地區分類 機械、電氣和管道服務市場:按服務類型、服務形式、計劃規模、技術和建築類型分類-2026-2032年全球市場預測

機械、電氣和管道服務市場:按服務類型、服務形式、計劃規模、技術和建築類型分類-2026-2032年全球市場預測 2026年全球機械、電氣和管道(MEP)服務市場報告2026年全球管道服務軟體市場報告

2026年全球機械、電氣和管道(MEP)服務市場報告2026年全球管道服務軟體市場報告