|

市場調查報告書

商品編碼

2064349

印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)India High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

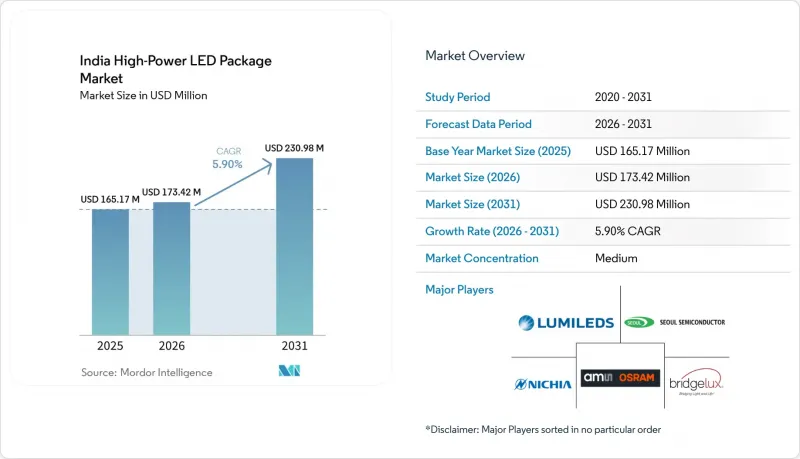

根據 Mordor Intelligence 預測,印度高功率LED構裝市場規模將從 2025 年的 1.6517 億美元成長到 2026 年的 1.7342 億美元,到 2031 年將達到 2.3098 億美元,2026 年至 2031 年的複合年成長率為 5.9%。

本報告依輸出功率範圍(1W–3W、3W–10W、10W以上)、封裝架構(單晶片封裝(SMD/分離式封裝)、多晶片封裝(SMD)、COB(板載晶片)等)及應用領域(通用照明、汽車照明、顯示器與背光、特殊/小眾應用)進行分類。市場預測以美元(USD)計價。

印度高功率LED構裝市場趨勢與洞察

政府透過UJALA和SLNP計畫進行推廣

透過「全民可負擔LED照明計畫 (UJALA)」和「國家路燈計畫 (SLNP)」的大量採購,全國已部署了3.687億個LED燈泡和1340萬盞路燈,為高功率LED替換產品創造了可預測的售後市場。 UJALA啟動後的前16個月內,單價下降了75%,LED確立了其作為標準光源的地位,並擴大了國內組裝商的潛在基本客群。隨著EESL將新的競標重點轉向智慧可調光照明燈具,封裝供應商需要整合驅動器和物聯網控制功能才能保持其資格。採用SLNP照明燈具的市政當局預計更換週期為7至10年,這確保了對15W-50W、高光通量維持率的封裝產品的穩定需求。這一趨勢有利於那些既能滿足政府的價格上限,又能滿足印度標準局 (BIS) 發光測量和安全測試要求的垂直整合型企業。

城市基礎設施和智慧城市計畫的快速擴張

智慧城市計畫的預算撥款正用於資助100個城市的LED照明維修。艾哈默德巴德投資50億盧比(約5,670萬美元)升級21萬盞路燈,而科欽則斥資3億盧比(約340萬美元)購置4萬套連網照明設備。這些大規模合約規定了超過5萬小時的光通量維持率和80以上的顯色指數,這為低成本進口產品設置了很高的進入門檻。古瓦哈提的2025專案透過降低60%的能耗並將維護週期延長至5萬小時,證明了高階方案在降低總擁有成本(TCO)方面的有效性。各邦的競標有利於能夠根據區域氣候客製化散熱設計的本地分銷商。隨著城市合約中對整合感測器的需求日益成長,擁有自主研發的驅動器和射頻技術的供應商正在獲得競爭優勢。

外延和封裝設備高度依賴進口

印度製造商仍然嚴重依賴海外供應商,例如 Aixtron、Veeco 和 ASM Pacific,為其提供大部分 MOCVD 反應器、光刻生產線和引線鍵合機,這限制了上游工程的價值創造。單一反應器的成本在 300 萬至 500 萬美元之間,而整個晶圓廠的建設成本超過 1 億美元,這樣的投資對於中型照明製造商來說是難以承受的。儘管 Halonix 透過組裝流程的在地化,已將其進口依賴度從 2021 會計年度的 60% 降低到 2025 會計年度的 24%,但其外延晶圓和晶片仍依賴從台灣和韓國採購。生產關聯獎勵(PLI) 計畫的目標是到 2029 年實現 75-80% 的國內增加價值比率,但要實現這一目標,需要供應商之間共用製造中心和成立合資企業。如果沒有這些發展,外匯波動和地緣政治風險將繼續對高功率封裝的獲利能力和供應穩定性構成壓力。

細分市場分析

2025年,1W-3W功率等級的LED燈具在印度高功率LED構裝市場佔據主導地位,市佔率高達47.84%。同時,預計到2031年,10W以上功率等級的LED燈具將以6.47%的複合年成長率成長。目前,10W以上功率等級的LED燈具主要供應給高桿路燈、工業廠房和運動設施,使用者願意承擔更高的採購成本以獲得更低的整體擁有成本(TCO)。印度體育場館維修計畫對節能20-30%和更窄光束角的需求,推動了此頻寬高功率LED構裝市場的發展。 50W以上的LED燈具通常採用陶瓷基板和精密光學元件,促進了二極體和燈具製造商之間的合作。對於安裝商而言,更長的維護週期至關重要,因為塔上維護成本仍然很高。另一方面,曾經由UJALA燈泡主導的傳統1W-3W功率等級的LED燈具,在都市區住宅正逐步被淘汰,限制了其成長潛力。

市場參與企業目前正在設計模組化引擎,將6至8個15W LED陣列整合到單一基板上,從而簡化高桿照明燈具的組裝流程。這種系統整合趨勢使供應商更具優勢,他們不僅可以共同設計二極體,還可以共同設計驅動器、光學元件和散熱路徑。在農村電氣化計畫中,高功率太陽能路燈套件開始採用20W至30W的LED陣列和鋰離子電池組合,而功率超過10W的組件也擴大應用於離網系統。因此,透過生產連結獎勵計畫(PLI)擴大產能的契約製造製造商正將投資重點放在能夠處理高達200W組件的自動化組裝線上。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府透過UJALA和SLNP計畫進行推廣

- 城市基礎設施和智慧城市計畫的快速擴張

- 降低高功率LED構裝的每流明成本

- 汽車產業向LED頭燈過渡

- 受控環境農業中園藝LED農場的興起

- 即將到來的賽事對更換高桿體育照明設備的需求激增。

- 市場限制因素

- 外延和封裝設備高度依賴進口

- 熱帶氣候下溫度控管的挑戰

- 高功率LED可靠性測試標準存在差異

- SiC基板供應鏈的波動性

- 監理情勢

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 1W~3W

- 3W~10W

- 10瓦或以上

- 以建築學為例

- 單晶片封裝(SMD/分離式)

- 多晶片封裝(SMD)

- COB(板載晶片)

- 其他架構(CSP、覆晶、混合模組)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 特殊/小眾

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corp.

- Everlight Electronics Co., Ltd.

- Osram Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding BV

- Cree LED(Wolfspeed, Inc.)

- Samsung Electronics Co., Ltd.(LED Business)

- MLS Co., Ltd.

- Bridgelux, Inc.

- Citizen Electronics Co., Ltd.

- Edison Opto Corp.

- Dominant Opto Technologies Sdn. Bhd.

- LG Innotek Co., Ltd.

- Surya Roshni Ltd.

- Havells India Ltd.

- Bajaj Electricals Ltd.

- Wipro Lighting(Wipro Enterprises Pvt. Ltd.)

- Crompton Greaves Consumer Electricals Ltd.

- Halonix Technologies Pvt. Ltd.

- Syska LED Lights Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the india high-Power lED package market size is expected to increase from USD 165.17 million in 2025 to USD 173.42 million in 2026 and reach USD 230.98 million by 2031, growing at a CAGR of 5.9% over 2026-2031.

This report is Segmented by Power Range (1W-3W, 3W-10W, Above 10W), Architecture (Single-Die Packages (SMD / Discrete), Multi-Die Packages (SMD), COB (Chip-On-Board), and More), Application (General Lighting, Automotive Lighting, Display and Backlighting, Specialty/Niche). The Market Forecasts are Provided in Terms of Value (USD).

India High-Power LED Package Market Trends and Insights

Government Push Through UJALA and SLNP Programs

Bulk procurement under the Unnat Jyoti by Affordable LEDs for All and Street Lighting National Program has seeded a nationwide installed base of 36.87 crore LED bulbs and 1.34 crore streetlights, creating a predictable aftermarket for high-power replacements. Unit prices fell by 75% within the first 16 months of UJALA, normalizing LEDs as the default light source and widening the addressable base for domestic assemblers. As EESL pivots new tenders toward smart, dimmable luminaires, package suppliers must now integrate drivers and IoT controls to stay qualified. Municipalities that adopted SLNP fixtures face seven-to-ten-year replacement cycles, ensuring steady demand for 15 W-50 W packages with higher lumen maintenance. This dynamic favors vertically integrated firms that can meet Bureau of Indian Standards photometric and safety tests while keeping costs aligned with government price ceilings.

Rapid Urban Infrastructure Expansion and Smart City Projects

Smart Cities Mission allocations have financed LED retrofits across 100 cities, with Ahmedabad investing INR 5 billion (USD 56.7 million) to upgrade 210 000 poles and Kochi spending INR 300 million (USD 3.4 million) on 40 000 networked luminaires. These large contracts specify lumen maintenance above 50 000 hours and a color rendering index above 80, raising entry barriers for low-cost imports. Guwahati's 2025 project cut energy use by 60% while stretching maintenance intervals to 50 000 hours, validating the total-cost-of-ownership case for premium packages. Decentralized tendering across states rewards regional distributors that can customize thermal designs for local climate zones. As city contracts increasingly require integrated sensors, suppliers with in-house driver and RF capabilities gain a competitive edge.

High Import Dependence for Epitaxy and Packaging Equipment

Indian manufacturers still source most MOCVD reactors, lithography lines, and wire-bonders from overseas suppliers such as Aixtron, Veeco, and ASM Pacific, constraining upstream value addition. A single reactor costs USD 3-5 million, while a full fab can exceed USD 100 million, placing such investments beyond the reach of mid-sized lighting firms. Halonix reduced reliance on imports from 60% in FY2021 to 24% in FY2025 by localizing assembly, yet epitaxial wafers and chips still arrive from Taiwan and South Korea. The PLI scheme targets 75-80% domestic value addition by 2029, but achieving this goal will require shared fabrication hubs or joint ventures between equipment vendors. Without such moves, currency volatility and geopolitical risks will continue to pressure margins and supply assurance for high-power packages.

Other drivers and restraints analyzed in the detailed report include:

- Declining Cost-Per-Lumen of High-Power LED Packages

- Automotive Industry Shift to LED Headlamps

- Thermal Management Challenges in Tropical Climate

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the 1 W-3 W class dominated the India High-Power LED package market, capturing 47.84% share. Meanwhile, the Above 10 W segment is set to grow at a 6.47% CAGR, continuing through 2031. Above 10 W packages now supply high-mast streetlights, industrial bays, and sports venues, where users accept higher purchase costs in exchange for better total cost of ownership. The India High-Power LED package market in this band is benefiting from stadium retrofits that demand 20-30% energy savings and tighter beam angles. Packages exceeding 50 W typically employ ceramic substrates and precision optics, driving collaboration between diode makers and luminaire houses. Installers view longer service intervals as critical because tower-top maintenance remains cost-intensive. Meanwhile, the legacy 1 W-3 W class, once propelled by UJALA bulbs, is entering a slow-replacement phase in urban homes, limiting its growth potential.

Market participants now design modular engines that group six to eight 15 W LED arrays on a single plate, cutting assembly steps for high-mast luminaires. This system-integration trend rewards suppliers that co-design drivers, optics, and thermal paths, not merely diodes. In rural electrification schemes, higher-wattage solar-streetlight kits have begun to specify 20-W to 30-W arrays paired with Li-ion batteries, pushing above 10 W packages further into off-grid applications. Consequently, contract manufacturers expanding PLI-backed capacity are focusing CAPEX on automated assembly lines rated up to 200 W modules.

List of Companies Covered in this Report:

- Nichia Corp.

- Everlight Electronics Co., Ltd.

- Osram Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Cree LED (Wolfspeed, Inc.)

- Samsung Electronics Co., Ltd. (LED Business)

- MLS Co., Ltd.

- Bridgelux, Inc.

- Citizen Electronics Co., Ltd.

- Edison Opto Corp.

- Dominant Opto Technologies Sdn. Bhd.

- LG Innotek Co., Ltd.

- Surya Roshni Ltd.

- Havells India Ltd.

- Bajaj Electricals Ltd.

- Wipro Lighting (Wipro Enterprises Pvt. Ltd.)

- Crompton Greaves Consumer Electricals Ltd.

- Halonix Technologies Pvt. Ltd.

- Syska LED Lights Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Push Through UJALA and SLNP Programs

- 4.2.2 Rapid Urban Infrastructure Expansion and Smart City Projects

- 4.2.3 Declining Cost-per-Lumen of High-Power LED Packages

- 4.2.4 Automotive Industry Shift to LED Headlamps

- 4.2.5 Rise of Horticulture LED Farms in Controlled-Environment Agriculture

- 4.2.6 Surge in High-Mast Sports Lighting Upgrades for Upcoming Events

- 4.3 Market Restraints

- 4.3.1 High Import Dependence for Epitaxy and Packaging Equipment

- 4.3.2 Thermal Management Challenges in Tropical Climate

- 4.3.3 Fragmented Standards for High-Power LED Reliability Testing

- 4.3.4 Supply-Chain Volatility for SiC Substrates

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 1W-3W

- 5.1.2 3W-10W

- 5.1.3 Above 10W

- 5.2 By Architecture

- 5.2.1 Single-die Packages (SMD / Discrete)

- 5.2.2 Multi-die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Other Architectures (CSP, Flip-chip, Hybrid Modules)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corp.

- 6.4.2 Everlight Electronics Co., Ltd.

- 6.4.3 Osram Opto Semiconductors GmbH

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Cree LED (Wolfspeed, Inc.)

- 6.4.7 Samsung Electronics Co., Ltd. (LED Business)

- 6.4.8 MLS Co., Ltd.

- 6.4.9 Bridgelux, Inc.

- 6.4.10 Citizen Electronics Co., Ltd.

- 6.4.11 Edison Opto Corp.

- 6.4.12 Dominant Opto Technologies Sdn. Bhd.

- 6.4.13 LG Innotek Co., Ltd.

- 6.4.14 Surya Roshni Ltd.

- 6.4.15 Havells India Ltd.

- 6.4.16 Bajaj Electricals Ltd.

- 6.4.17 Wipro Lighting (Wipro Enterprises Pvt. Ltd.)

- 6.4.18 Crompton Greaves Consumer Electricals Ltd.

- 6.4.19 Halonix Technologies Pvt. Ltd.

- 6.4.20 Syska LED Lights Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space And Unmet-Need Assessment

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年)

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年) 歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測

二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測 氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測

氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測