|

市場調查報告書

商品編碼

2063961

高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

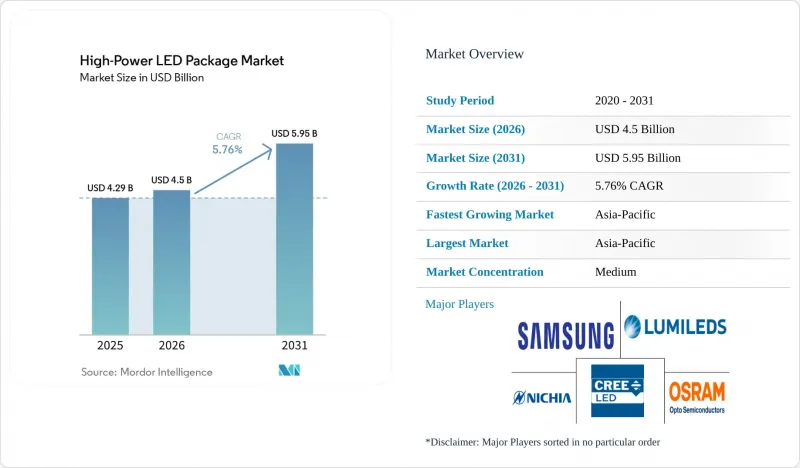

Mordor Intelligenceによると、高功率LED構裝の市場規模は、2025年の42億9,000万米ドルから2026年には45億米ドルに拡大し、2031年までに59億5,000万米ドルに達すると予測されており、2026年から2031年にかけてCAGR5.76%で成長すると見込まれています。

本報告按輸出功率範圍(1W–3W、3W–10W、其他)、封裝架構(單晶片封裝、多晶片封裝、COB、其他)、應用領域(通用照明、汽車照明、顯示和背光、其他)以及地區(北美、歐洲、亞太、南美、其他)進行細分。市場預測以美元(USD)為單位。

全球高功率LED構裝市場趨勢及洞察

高功率燈泡每流明美元價格大幅下降。

憑藉規模化生產、95%的晶圓良率和製程自動化,3W封裝LED的市場價格已跌至每批0.5美元以下。即使在嚴格的投資回收規則下,市政競標也傾向於選擇LED。實驗室原型產品的光效已超過200 lm/W,商用模組在結溫低於85 度C的情況下,光效穩定在140-160 lm/W,從而減少了散熱器品質並簡化了燈具設計。中國氮化鎵晶片的月產量已達1748萬片,給全球價格帶來了下行壓力。但金光光電在2026年1月漲價,顯示利潤率可能已觸底,未來的成本降低將取決於新型基板和磷光體化學成分。每流明成本的下降正在將目標市場從路燈擴展到體育場館和港口照明,加速了高強度氣體放電燈(HID)的早期淘汰,並推動了強制性的能源效率提升。

政府正逐步淘汰高強度氣體放電燈(HID路燈)。

美國《明亮照明法案》(BRIGHT Act)和2024年4月能源部的相關規定要求,到2028年7月,通用照明燈具的發光效率必須達到120 lm/W。華盛頓州已於2026年起禁止使用不符合該標準的金屬鹵化物照明燈具。加州的市政當局正利用電力公司的補貼計劃,在聯邦規定的最後期限前加快轉型。歐洲也採取了類似的措施,將非定向光源的發光效率標準設定為160 lm/W。這些政策規定了50,000小時的L70壽命和IP66防塵防水等級,從而推動了多表面黏著技術和板載晶片(COB)封裝的採購,這些封裝能夠分散熱負荷並承受戶外環境。印度的生產連結獎勵計畫計畫(總額達62.38億印度盧比,約7.5億美元)進一步支持了國內封裝產業,並促進了對東南亞和中東的出口。

結功率為 10 W 或更高時,溫度控管的複雜性。

10 W以上で動作するパッケージは、多くの場合10 mm×10 mm未満のフットプリント内で3~5 Wの熱を放散し、接合部温度を125 度C近くまで上昇させます。この温度では、ルーメンの低下が加速し、色度もドリフトします。周囲温度が40 度Cを超える地域では、園芸用照明器具やUV-Cモジュールにおいて、熱伝導率2 W m-1K以上の絶縁金属基板、マイクロチャネル液体プレート、または熱電冷却器を使用する必要があります。これらはいずれも、1ユニットあたり5~10米ドルのコスト増となります。Bridgelux社や同業他社は、複数のダイをセラミックキャリア上に配置することでホットスポットを低減しており、これによりピーク接合部温度を15~20 度C低下させていますが、材料費と組裝の複雑さは増しています。改裝用ハウジングでは、従来のフォームファクタでは必ずしも大型のヒートシンクを収容できないため、さらなる制約が生じ、熱暴走が発生した場合のリコールや責任リスクが高まります。

細分市場分析

到2025年,1-3W頻寬的銷售量佔比將達到47.80%。這主要得益於通用改造項目、商用下照燈以及適合現有驅動裝置和光學元件的住宅照明燈具。同時,3-10W功率段則滿足了工業高棚燈和都市區路燈的需求,這些應用需要高流明密度和優異的散熱性能。 10W以上的功率段目前仍屬於小眾市場,但預計到2031年將以每年7.11%的速度成長,因為垂直農業對光合有效輻射(光合有效輻射)的要求超過1500µmol m⁻² s⁻¹,醫療保健機構也開始採用265-280nm的UV-C光源進行消毒。這些高電流模組必須在環境溫度通常超過35 度C的封閉空間內,達到50,000小時的L70壽命等級。 As a result, vendors are focusing on ceramic 基板, copper cores, and in-package 熱敏電阻器 to regulate current and prevent thermal runaway.

溫度控管是決定該領域技術極限的關鍵因素,因為在高溫環境下,僅靠被動散熱器無法始終將結溫維持在 100 度C以下。供應商除了提供可將晶片分佈在更大表面積上的板載晶片封裝 (COB) 佈局外,還提供適用於嚴苛環境的可選液態微通道和相變基板。在通用照明領域,1-3W 級高功率LED構裝的市場規模受益於商品化,但隨著零售價格跌破每片 0.50 美元,維持利潤率變得越來越困難。另一方面,10W 及以上級別的 LED 由於具有針對特定應用的波長和壽命保證,因此能夠保持高價,即使銷量不高,供應商也能確保盈利。

區域分析

アジア太平洋地域は2025年に世界売上高の68.60%を占め、インフラ整備、国内景気獎勵策略、およびエピタキシャルウエハーから磷光體に至る広範な製造基盤を背景に、2031年まで年率7.20%で成長すると予測されています。中国はガリウム精製能力の98%、ユーロピウム加工の85%を支配しており、この集中化により、世界のサプライチェーンは急な政策転換や工場の操業停止の影響を受けやすくなっています。インドの生產連結獎勵計畫(623.8億ルピー、7億5,000万米ドル相当)は、国内の街路灯のLED化および南アジアや中東への輸出を目的とした新しいパッケージングラインの推出を支援しています。日本は、日亜化学工業やシチズンなどのベンダーのおかげで、覆晶の知的財産においてリーダーシップを維持し、自動車OEM供給においてプレミアム価格を確立しています。

北美和歐洲合計約佔總需求的四分之一,這一趨勢與監管壓力和智慧建築投資密切相關。美國計畫到2028年7月強制規定通用照明燈具的光通量效率達到120 lm/W,而加州將於2026年1月生效的第24號法規包含一項遙測要求,建議採用內建感測器和藍牙低功耗(BLE)無線功能的燈具。歐洲提案的第四階段生態設計目標是非定向燈具達到160 lm/W,要求對散熱基板和高頻驅動器進行聯合設計,以在不影響L70壽命的情況下維持電流脈衝。

儘管南美洲、中東和非洲的LED燈具數量絕對值落後於其他地區,但隨著當地政府負責人利用多邊銀行的優惠貸款推動LED轉型,這些地區正經歷爆炸性成長。離網太陽能燈和混合路燈需要700-1000mA的驅動電流以及IP66或更高的防塵防水等級,以應對多塵和炎熱的氣候,這就對具有可靠焊點的高功率封裝提出了更高的要求。地域多角化戰略正在加速推進。來自台灣和韓國的供應商正在泰國和越南投資建造組裝線,以降低對單一國家依賴的風險。同時,美國和歐盟分別撥款32億美元和28億歐元(約31.6億美元)用於國內鎵和稀土元素加工廠建設,目標是在五年內打破中國在該領域的近乎壟斷地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高功率封裝產品每流明單價大幅下降。

- 政府正逐步淘汰高強度氣體放電燈(HID路燈)。

- 汽車產業向固態頭燈和自動遠光燈的過渡

- 需要大電流LED的智慧照明控制設備的普及。

- 室內垂直農業設施需求激增

- UV-C高功率LED 在消毒領域的應用日益廣泛。

- 市場限制因素

- 結功率為 10 W 或更高時,溫度控管的複雜性。

- 中國產能過剩導致的價格壓力

- 覆晶和CSP製程的IP壁壘

- 高純度鎵和稀土元素磷光體的供應風險

- 產業供應鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 1W~3W

- 3W~10W

- 10瓦或以上

- 以建築學為例

- 單晶片封裝(SMD/分離式)

- 多晶片封裝(SMD)

- COB(板載晶片)

- 其他架構(CSP、覆晶、混合模組)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 特殊/小眾

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 東南亞

- 其他亞太國家

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corp.

- Cree LED Inc.

- OSRAM Opto Semiconductors GmbH

- Samsung Electronics Co., Ltd.

- Lumileds Holding BV

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Citizen Electronics Co., Ltd.

- Bridgelux Inc.

- MLS Co., Ltd.

- LITE-ON Technology Corp.

- NationStar Optoelectronics Co., Ltd.

- Luminus Devices Inc.

- Foshan Nationstar Optoelectronics Co., Ltd.

- Epistar Corp.

第7章 市場機會與未來展望

According to Mordor Intelligence, the high-Power lED package market size is expected to increase from USD 4.29 billion in 2025 to USD 4.50 billion in 2026 and reach USD 5.95 billion by 2031, growing at a CAGR of 5.76% over 2026-2031.

This report is Segmented by Power Range (1W-3W, 3W-10W, and More), Architecture (Single-Die Packages, Multi-Die Packages, COB, and More), Application (General Lighting, Automotive Lighting, Display and Backlighting, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global High-Power LED Package Market Trends and Insights

Rapid Decline in USD per Lumen for High-Power Packages

Manufacturing scale, 95% wafer yields, and process automation have pushed street prices for 3 W packages below USD 0.50 in bulk lots, tipping municipal tenders in favor of LEDs even under strict payback rules. Laboratory prototypes already exceed 200 lm/W and commercial modules routinely deliver 140-160 lm/W at junction temperatures under 85 °C, trimming heatsink mass and simplifying fixture design. China's monthly output of 17.48 million gallium-nitride chips exerts downward price pressure worldwide, yet Kinglight Optoelectronics' January 2026 price increase signals that margins may have reached a structural floor where future cost cuts hinge on new substrates or phosphor chemistry. The sliding cost per lumen broadens the addressable market from street lighting to sports arenas and seaport illumination, fast-tracking the retirement of high-intensity discharge incumbents and reinforcing efficiency mandates.

Government-Mandated Phase-Out of HID Streetlights

The United States BRIGHT Act and the April 2024 Department of Energy rules require 120 lm/W efficacy for general service lamps by July 2028, while Washington State bans non-compliant metal-halide fixtures from 2026. California municipalities, armed with utility rebates, are front-loading conversions ahead of the federal deadline, and parallel measures in Europe raise the bar to 160 lm/W for non-directional sources. These policies specify 50,000-hour L70 ratings plus IP66 ingress protection, conditions that steer procurement toward multi-die surface-mount and chip-on-board packages capable of spreading thermal load and surviving outdoor environments. India's Production Linked Incentive scheme, worth INR 6,238 crore (USD 750 million), further supports domestic packaging and export supply into Southeast Asia and the Middle East.

Thermal Management Complexity at ≥10 W Junction Power

Packages operating above 10 W dissipate 3-5 W of heat inside footprints often under 10 mm X 10 mm, pushing junction temperatures toward 125 °C, where lumen depreciation accelerates, and chromaticity drifts. In regions where ambient temperatures exceed 40 °C, horticultural fixtures and UV-C modules must use insulated metal substrates with a thermal conductivity of 2 W m-1 K or higher, micro-channel liquid plates, or thermoelectric coolers, each adding USD 5-10 per unit. Bridgelux and peers mitigate hot spots by spreading multiple dies across ceramic carriers, lowering peak junction temperatures by 15-20 °C but raising material costs and assembly complexity. Retrofit housings introduce additional constraints because legacy form factors cannot always accommodate larger heatsinks, elevating recall and liability risk if thermal runaway occurs.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Shift to Solid-State Headlamps and ADB

- Proliferation of Smart Lighting Controls Requiring High-Current LEDs

- Price Compression from China-Based Overcapacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 1-3 W bracket accounted for 47.80% of revenue in 2025, underpinned by general-purpose retrofits, commercial downlights, and residential fixtures that align with established drivers and optics. Meanwhile, the 3-10 W segment supports industrial high-bay luminaires and urban streetlights that require elevated lumen density and robust thermal performance. Above-10 W packages, though niche in volume, are forecast to advance at 7.11% through 2031 as vertical farms specify photosynthetic photon flux densities above 1,500 µmol m-2 s-1 and healthcare operators adopt 265-280 nm UV-C sources for germicidal duty cycles. These high-current modules must survive 50,000-hour L70 ratings inside enclosures where ambient temperatures often exceed 35 °C. Consequently, vendors emphasize ceramic substrates, copper cores, and in-package thermistors that modulate current to prevent thermal runaway.

Thermal management defines the engineering ceiling in this tier because passive heatsinks cannot always maintain sub-100 °C junction temperatures in hot climates. Suppliers offer chip-on-board layouts that distribute dies across broader surfaces, plus optional liquid microchannels or phase-change substrates for extreme environments. Across general lighting, the High-Power LED Package market size in the 1-3 W range benefits from commoditization, yet margin protection becomes increasingly elusive as street prices dip below USD 0.50 per device. Conversely, the above-10 W class commands premium pricing thanks to application-specific wavelengths and lifetime guarantees, enabling vendors to preserve profitability even when unit sales stay modest.

Geography Analysis

Asia-Pacific accounted for 68.60% of global revenue in 2025 and is projected to grow at 7.20% through 2031 on the back of infrastructure buildouts, domestic stimulus, and an outsized manufacturing base spanning epitaxial wafers to phosphors. China controls 98% of gallium refining capacity and 85% of europium processing, a concentration that exposes the global supply chain to sudden policy shifts or plant outages. India's Production Linked Incentive worth INR 6,238 crore (USD 750 million) underwrites new packaging lines intended for local street-lighting conversions and exports across South Asia and the Middle East. Japan maintains leadership in flip-chip intellectual property and commands premium pricing in automotive OEM supply, thanks to vendors like Nichia and Citizen.

North America and Europe together account for roughly one-quarter of total demand, with their trajectories tightly linked to regulatory pressure and smart-building investments. The United States will enforce 120 lm/W efficacy in general service lamps by July 2028, and California's January 2026 Title 24 code embeds telemetry obligations that favor packages with integrated sensors and BLE radios. Europe's proposed Stage 4 Ecodesign targets 160 lm/W for non-directional lamps, a benchmark that compels co-design of thermal substrates and high-frequency drivers capable of sustaining current pulses without undermining L70 lifetime.

South America, the Middle East, and Africa trail in absolute numbers yet record step-change growth as municipal planners embrace LED conversions powered by concessional finance from multilateral banks. Off-grid solar lanterns and hybrid streetlights require 700-1,000 mA drive currents and IP66 or higher ingress protection to survive dust-laden, high-temperature climates, channeling demand toward high-power packages with robust solder-joint reliability. Regional diversification strategies are accelerating: Taiwanese and South Korean vendors are investing in Thailand and Vietnam assembly lines to sidestep single-country risk, while the United States and European Union have earmarked USD 3.2 billion and EUR 2.8 billion (USD 3.16 billion) respectively for domestic gallium and rare-earth processing plants that aim to dent China's near-monopoly within five years.

- Nichia Corp.

- Cree LED Inc.

- OSRAM Opto Semiconductors GmbH

- Samsung Electronics Co., Ltd.

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Citizen Electronics Co., Ltd.

- Bridgelux Inc.

- MLS Co., Ltd.

- LITE-ON Technology Corp.

- NationStar Optoelectronics Co., Ltd.

- Luminus Devices Inc.

- Foshan Nationstar Optoelectronics Co., Ltd.

- Epistar Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Decline in USD/Lumen for High-Power Packages

- 4.2.2 Government-Mandated Phase-Out of HID Streetlights

- 4.2.3 Automotive Shift to Solid-State Headlamps and ADB

- 4.2.4 Proliferation of Smart Lighting Controls Requiring High-Current LEDs

- 4.2.5 Demand Spike from Indoor Vertical Farming Fixtures

- 4.2.6 Expansion of UV-C High-Power LED Adoption in Disinfection

- 4.3 Market Restraints

- 4.3.1 Thermal Management Complexity at >=10 W Junction Power

- 4.3.2 Price Compression From China-Based Overcapacity

- 4.3.3 IP Barriers on Flip-Chip and CSP Processes

- 4.3.4 Supply Risk of High-Purity Gallium and Rare Earth Phosphors

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 1W - 3W

- 5.1.2 3W - 10W

- 5.1.3 Above 10W

- 5.2 By Architecture

- 5.2.1 Single-die Packages (SMD / Discrete)

- 5.2.2 Multi-die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Other Architecture (CSP, Flip-chip, Hybrid modules)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Southeast Asia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corp.

- 6.4.2 Cree LED Inc.

- 6.4.3 OSRAM Opto Semiconductors GmbH

- 6.4.4 Samsung Electronics Co., Ltd.

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Seoul Semiconductor Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Toyoda Gosei Co., Ltd.

- 6.4.10 Citizen Electronics Co., Ltd.

- 6.4.11 Bridgelux Inc.

- 6.4.12 MLS Co., Ltd.

- 6.4.13 LITE-ON Technology Corp.

- 6.4.14 NationStar Optoelectronics Co., Ltd.

- 6.4.15 Luminus Devices Inc.

- 6.4.16 Foshan Nationstar Optoelectronics Co., Ltd.

- 6.4.17 Epistar Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年)

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年) 歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測

二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測 氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測

氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測