|

市場調查報告書

商品編碼

2063964

亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

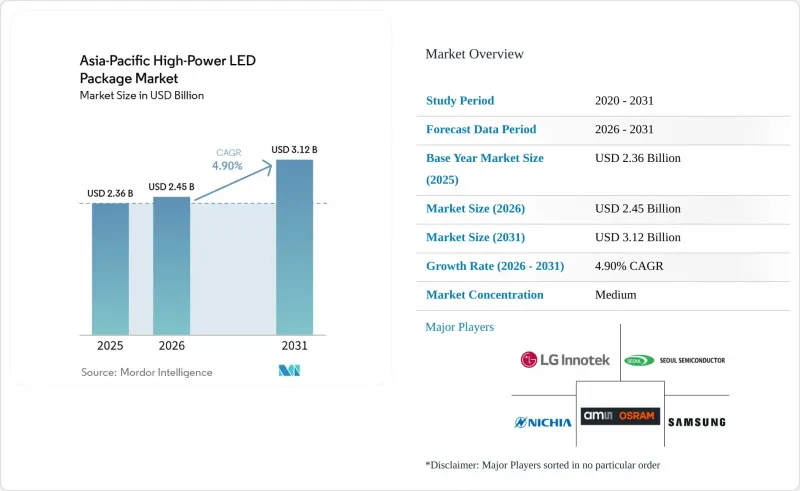

根據 Mordor Intelligence 預測,亞太地區高功率LED構裝市場規模預計到 2031 年將達到 31.2 億美元,從 2025 年的 23.6 億美元成長到 2026 年的 24.5 億美元,2026 年至 2031 年的複合成長率將達到 4.90%。

本報告按功率輸出範圍(1W–3W、3W–10W、10W以上)、架構(單晶片封裝(SMD/分離式封裝)、多晶片封裝(SMD)等)、應用(單晶片照明、汽車照明、顯示和背光、特殊/小眾應用)以及國家/地區(中國、日本、印度通用照明、東南亞及其他亞地區)進行細分。市場預測以美元(USD)為單位。

亞太地區高功率LED構裝市場趨勢與洞察。

高階消費性電子產品中採用Mini-LED背光技術的趨勢正在快速成長。

高階電視和平板電腦正從側入式背光轉向mini-LED直下式背光,以提高對比度和局部調光精度,這直接推動了對能夠承受高電流密度而不發生色偏的高功率封裝的需求。三星2026年的Neo QLED產品線和聯發科的micro-LED顯示引擎演示都支持了這項技術變革,其應用範圍已超越消費級螢幕。 TrendForce預測,從2024年到2029年,mini-LED背光出貨量將以每年17%的速度成長,到2027年,平板電腦的滲透率將達到15%。 3W至10W範圍內的封裝將受益最大,因為它們兼具高發光效率和可控的散熱面積。能夠將波長容差控制在5nm以內的供應商(目前仍集中在日本和韓國)正在獲得更高的利潤率,因為OEM廠商正在收緊分級標準。

東亞地區智慧工廠的LED維修正在加速進行中。

為了符合節能法規並提高機器視覺的精確度,中國和日本的製造工廠正在用高功率LED陣列取代傳統的放電燈泡。大谷化學的2025年計畫包括將智慧照明控制與其ERP系統整合,以最佳化照明水平,並在兩年內實現投資回報。功率超過5瓦的LED燈具可以減少照明設備的數量,從而縮短安裝時間和維護週期,並延長其10年的使用壽命。 2024年,中國工業和資訊化部發布指南,將LED維修認定為合格的碳減排措施。此外,市場對可調色溫、可調光的頻譜產品的需求也在不斷成長,以改善夜班的工作環境。

預計從2025年起藍寶石基板供應將出現短缺

由於半導體晶圓廠將外延生產線轉向生產用於5G基礎設施的高頻濾波器,藍寶石晶圓供應趨緊,導致現貨價格較上一季上漲20%。沒有長期採購協議的中國大陸和台灣封裝製造商被迫在波動劇烈的現貨市場競標,這給它們的毛利率帶來了壓力。像三安光電這樣運作自有藍寶石生長爐的垂直整合型企業,透過保持成本穩定並以低於競爭對手的價格供應,正在整合整個產業。雖然預計隨著馬來西亞和越南的新產能從2027年開始投入運作,這種情況將有所緩解,但供應緊張的局面預計在短期內仍將持續,這可能會阻礙中小企業與汽車行業簽訂多年期合約。

細分市場分析

2025年,1W-3W功率範圍的LED封裝產品佔據了高功率LED構裝市場45.51%的佔有率,這主要得益於對成本高度敏感的通用照明領域。預計到2031年,10W以上功率範圍的LED封裝產品將以5.39%的年均成長率成長。這一成長將主要由汽車前照燈、工業高棚燈和體育場館泛光燈等應用領域推動,這些領域更傾向於採用以高亮度模組而非少數模組為中心的照明燈具。這種結構性轉變得益於鑽石基板和低於0.5KΩ/W的結殼電阻,使得封裝產品能夠突破傳統的散熱極限。汽車OEM廠商正在優先考慮更精確的光束控制和更簡化的驅動器,這與10W以上功率產品的普及趨勢相符,也符合中國GB 4599-2024標準和印度AIS-199草案的要求。缺乏先進材料科學和技術的供應商可能會將這個高利潤市場拱手讓給垂直整合的中國和日本競爭對手。

3W至10W中階的燈泡能夠有效平衡流明輸出和資本投資預算限制,尤其適用於公共路燈和花園燈等應用。這些應用領域仍然依賴該功率範圍的燈泡,因為它們具有成本效益,並且能夠滿足特定需求。然而,高功率燈泡每流明成本的下降可能會對該功率範圍燈泡的長期市場競爭力構成潛在挑戰。隨著智慧工廠維修和mini-LED背光技術的不斷進步,這一趨勢可能會更加明顯。這些技術越來越注重更高的發光效率和更嚴格的功率分級標準,這可能會促使市場偏好轉向性能更高的產品。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高階消費性電子產品中採用Mini-LED背光技術的趨勢正在快速成長。

- 加速東亞智慧廠採用LED照明

- 中國和印度政府主導強制汽車採用LED燈。

- 溫度控管技術的突破使得單一封裝的輸出功率超過 5 瓦。

- 中國包裝製造商垂直整合模式的興起

- 由於先進駕駛輔助系統(ADAS)的普及,對高亮度頭燈的需求增加。

- 市場限制因素

- 預計從2025年起藍寶石基板供應將出現短缺

- 覆晶封裝設計中的智慧財產權訴訟風險

- 在一般照明領域,中功率替代方案與現有方案之間存在持續的成本差距。

- 對公共照明中藍光危害的監管

- 產業價值鏈分析

- 技術分析

- 監理情勢

- 宏觀經濟因素的影響

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 1 W~3 W

- 3 W~10 W

- 10瓦或以上

- 以建築學為例

- 單晶片封裝(SMD/分離式)

- 多晶片封裝(SMD)

- COB(板載晶片)

- 其他架構(CSP、覆晶、混合模組)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 特殊/小眾

- 國家

- 中國

- 日本

- 印度

- 東南亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Cree LED, a SMART Global Holdings Inc. company

- OSRAM Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding BV

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Epistar Corporation

- Toyoda Gosei Co., Ltd.

- Seoul Viosys Co., Ltd.

- Lite-On Technology Corporation

- Honglitronic Co., Ltd.

- Lextar Electronics Corporation

- Foshan NationStar Optoelectronics Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Genesis Photonics Inc.

- Edison Opto Corporation

- Dominant Opto Technologies Sdn. Bhd.

- ProLight Opto Technology Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific high-Power lED package market size was valued at USD 2.45 billion in 2026 and is projected to expand from USD 2.36 billion in 2025 to reach USD 3.12 billion by 2031, registering a 4.90% CAGR over 2026-2031.

This report is Segmented by Power Range (1W-3W, 3W-10W, Above 10W), Architecture (Single-Die Packages (SMD / Discrete), Multi-Die Packages (SMD), and More), Application (General Lighting, Automotive Lighting, Display and Backlighting, Specialty / Niche), and Country (China, Japan, India, Southeast Asia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific High-Power LED Package Market Trends and Insights

Surge in Mini-LED Backlight Adoption in Premium Consumer Devices

Premium televisions and tablets are shifting from edge-lit designs to mini-LED direct backlighting to raise contrast ratios and local dimming precision, a move that directly lifts demand for high-power packages capable of handling elevated current densities without color-shift drift. Samsung's 2026 Neo QLED lineup and MediaTek's showcase of micro-LED display engines confirm technology migration beyond consumer screens. TrendForce estimates show that mini-LED backlight unit shipments will grow 17% annually from 2024 through 2029, with tablet penetration reaching 15% by 2027. Packages in the 3 W-10 W bracket benefit most because they combine high luminous efficacy with manageable thermal footprints. Suppliers able to maintain sub-5 nm wavelength tolerance, still concentrated in Japan and South Korea, secure margin expansion as OEMs tighten binning specifications.

Accelerated Smart-Factory LED Retrofits Across East Asia

Manufacturing plants in China and Japan are swapping legacy discharge lamps for high-power LED arrays to meet energy-efficiency mandates and improve machine-vision accuracy. Dagu Chemical's 2025 program integrated smart lighting controls with enterprise resource planning systems to optimize lux levels, achieving operational payback within 2 years. Packages above 5 W reduce luminaire counts, thereby cutting installation labor and maintenance cycles over a 10-year life. In 2024, China's Ministry of Industry and Information Technology issued guidance classifying LED retrofits as a qualified carbon-reduction measure. Demand is also rising for tunable white-spectrum products that shift color temperature for night-shift ergonomics.

Supply Tightness of Sapphire Substrates Post-2025

As semiconductor fabs reallocated epitaxy lines toward radio-frequency filters for 5G infrastructure, sapphire wafer supply tightened, and spot prices rose by 20% quarter over quarter. Chinese and Taiwanese packagers without long-term offtake contracts must bid in volatile spot markets, eroding gross margins. Vertically integrated players such as Sanan Optoelectronics, which runs captive sapphire-growth furnaces, maintain cost stability and underprice rivals, driving consolidation. Relief is likely after 2027 when new Malaysian and Vietnamese capacity becomes operational, yet near-term tightness is expected to restrict smaller firms from committing to multi-year automotive contracts.

Other drivers and restraints analyzed in the detailed report include:

- Government-Backed Automotive LED Mandates in China and India

- Thermal-Management Breakthroughs Enabling Above 5 W Single-Package Output

- IP Litigation Risks in Flip-Chip Package Designs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the 1 W-3 W bracket captured 45.51% of the High-Power LED Package market, a position rooted in cost-sensitive general lighting. The Above 10 W group is forecast to grow 5.39% annually through 2031, propelled by automotive headlamps, industrial high bays, and stadium floodlights that benefit from luminaires built around fewer yet brighter modules. This structural pivot is possible because diamond substrates and sub-0.5 K W-1 junction-to-case resistance allow packages to exceed earlier thermal ceilings. Automotive original equipment manufacturers value tighter beam control and reduced driver complexity, aligning with Above 10 W adoption with China's GB 4599-2024 and India's Draft AIS-199 standards. Suppliers lacking advanced material science risk ceding this high-margin turf to vertically integrated Chinese and Japanese rivals.

The prospects for the 3 W-10 W middle tier remain favorable, driven by its ability to effectively balance lumen output with capital budget constraints, particularly in applications such as municipal street lighting and horticulture lamps. These segments continue to rely on this power range due to its cost-effectiveness and suitability for their specific requirements. However, the declining cost per lumen at higher power ratings poses a potential challenge to the long-term relevance of this tier. This trend could become more pronounced if advancements in smart-factory retrofits and mini-LED backlights persist, as these technologies increasingly emphasize premium efficacy and tighter binning standards, which may shift market preferences toward higher-performing alternatives.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Cree LED, a SMART Global Holdings Inc. company

- OSRAM Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Epistar Corporation

- Toyoda Gosei Co., Ltd.

- Seoul Viosys Co., Ltd.

- Lite-On Technology Corporation

- Honglitronic Co., Ltd.

- Lextar Electronics Corporation

- Foshan NationStar Optoelectronics Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Genesis Photonics Inc.

- Edison Opto Corporation

- Dominant Opto Technologies Sdn. Bhd.

- ProLight Opto Technology Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Mini-LED Backlight Adoption in Premium Consumer Devices

- 4.2.2 Accelerated Smart-Factory LED Retrofits Across East Asia

- 4.2.3 Government-Backed Automotive LED Mandates in China and India

- 4.2.4 Thermal-Management Breakthroughs Enabling Above 5 W Single-Package Output

- 4.2.5 Rise of Vertical-Integration Models Among Chinese Packaging Houses

- 4.2.6 Advanced Driver-Assistance Systems Demanding High-Intensity Headlamps

- 4.3 Market Restraints

- 4.3.1 Supply Tightness of Sapphire Substrates Post-2025

- 4.3.2 IP Litigation Risks in Flip-Chip Package Designs

- 4.3.3 Persistent Cost Gap Versus Mid-Power Alternatives in General Lighting

- 4.3.4 Regulatory Scrutiny on Blue-Light Hazard in Public Illumination

- 4.4 Industry Value Chain Analysis

- 4.5 Technology Analysis

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 1 W - 3 W

- 5.1.2 3 W - 10 W

- 5.1.3 Above 10 W

- 5.2 By Architecture

- 5.2.1 Single-Die Packages (SMD / Discrete)

- 5.2.2 Multi-Die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Other Architectures (CSP, Flip-Chip, Hybrid Modules)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Country

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 Southeast Asia

- 5.4.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Cree LED, a SMART Global Holdings Inc. company

- 6.4.4 OSRAM Opto Semiconductors GmbH

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Epistar Corporation

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 Seoul Viosys Co., Ltd.

- 6.4.12 Lite-On Technology Corporation

- 6.4.13 Honglitronic Co., Ltd.

- 6.4.14 Lextar Electronics Corporation

- 6.4.15 Foshan NationStar Optoelectronics Co., Ltd.

- 6.4.16 Sanan Optoelectronics Co., Ltd.

- 6.4.17 Genesis Photonics Inc.

- 6.4.18 Edison Opto Corporation

- 6.4.19 Dominant Opto Technologies Sdn. Bhd.

- 6.4.20 ProLight Opto Technology Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年)

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年) 歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測

二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測 氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測

氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測