|

市場調查報告書

商品編碼

2065502

LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

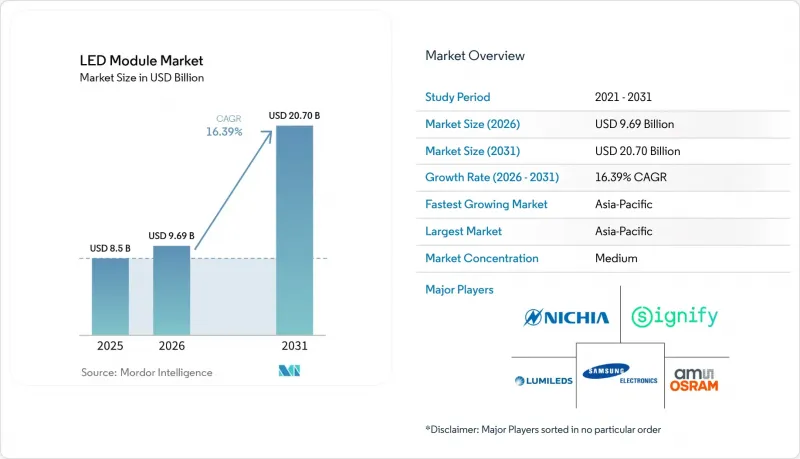

LED 模組市場預計在 2025 年達到 85 億美元,在 2026 年達到 96.9 億美元,從 2026 年到 2031 年的複合年成長率為 16.39%,到 2031 年將達到 207 億美元。

本報告按模組類型(COB、SMD、線性、背光、高功率及其他模組類型)、應用領域(通用照明、汽車、顯示器及背光、指示牌及其他應用)、功率範圍(低、中、高)、外形規格(剛性和軟性)以及地區(北美、歐洲及其他地區)進行細分。市場預測以美元(USD)為單位。

全球LED模組市場趨勢與洞察

將智慧照明與支援物聯網的建築系統整合

在商業建築中,連網照明正日益普及,每個LED模組都被視為一個智慧邊緣設備,用於收集有關人員佔用情況、自然光照和健康狀況的遙測數據。預計到2025年,北美和歐洲新建占地面積的60%將投資超過55萬美元用於無線閘道器、感測器陣列和雲端服務。經證實,該系統可降低30-40%的電力和維護成本,且投資回收期不到三年,符合財務長可接受的投資報酬率。全新的Matter協定整合了Zigbee、Thread和專有網狀網路,顯著縮短了試運行時間和支援電話。預測分析功能可在故障發生前安排更換計劃,從而提高租戶滿意度和物業所有者的資產價值。

政府正逐步淘汰低效照明設備。

三大洲的立法機構正在縮短合規期限,並將以往可選項的能源效率升級轉變為法律強制要求。歐盟於2021年禁止大多數鹵素照明產品使用庫存單位(SKU),並將於2024年加強海關執法,以防止不合規商品在港口進口。加州2025年修訂的第24號法規要求,新商業建築中90%的照明電力必須由配備人體感應器和自然光利用功能的LED光源提供。中國2024年藍圖要求,到2026年,公共基礎設施照明燈具的光通量效率必須提高到每瓦130流明或更高。這些同步推出的法規將確保對模組化LED維修套件和整合式天花板面板的持續需求。

高功率模組的溫度控管挑戰

在功率超過 30 瓦的高功率模組中,密集排列的發光元件產生的熱量難以散發,如果結溫超過 125 度C,光輸出會在數千小時內減半。為了滿足新的 IEC 62031:2026 熱阻報告規則,供應商被迫投資紅外線成像、有限元素模擬,甚至使用昂貴的金屬芯和陶瓷基板。被動式散熱器會增加重量和體積,而主動式風扇則會引發噪音和可靠性方面的擔憂。由於環境溫度本身就較高,園藝和工業照明燈具首當其衝受到影響,導致保固索賠增加,並阻礙了買家採取主動的過載運作策略。

細分市場分析

從2026年到2031年,LED背光模組的複合年成長率將達到16.81%,顯著高於整體LED模組市場的成長率,這主要得益於Mini-LED技術在高階電視和顯示器中的廣泛應用。 SMD模組在2025年仍將佔據LED模組市場33.61%的佔有率,這主要得益於其在住宅和商業照明設備中卓越的成本績效。在背光設計中,數千顆Mini-LED被用於實現超過1000個局部調光區域,推動了對超薄、高效散熱基板的需求。同時,板載晶片(COB)架構在汽車頭燈領域也越來越受歡迎,其緊湊的尺寸使其能夠在不增大反射器外殼的情況下實現10000流明的亮度。線性模組在辦公室燈具照明維修中仍然佔據主導地位,因為它們無需重新佈線即可替換螢光管,從而有助於控制專案進度。

LED模組市場也受惠於新興細分領域。軟性燈條可用於曲面標誌照明,UV-C模組正在醫療領域嶄露頭角。 COB單晶片透過降低熱阻並將顯色指數提升至90以上,滿足了博物館和零售商的需求。科銳LED的L2 PCBA平台將這些優勢與整合式驅動器結合,從而縮短了OEM廠商的照明燈具設計週期。隨著自動化降低Mini-LED的成本,背光模組將在高亮度顯示領域逐步取代SMD,進而強化供應商的多元化產品組合策略。

預計到2025年,通用照明LED模組市場將佔42.59%,但其成長動能正逐漸被顯示器和背光領域超越,預計到2031年將以16.98%的複合年成長率成長。直下式電視和遊戲顯示器的更換推動了替換需求,而HDR面板的普及則促進了局部調光技術的應用,從而提高了單一螢幕模組的使用量。商業照明仍然是模組消費的最大佔有率,這主要得益於辦公室、零售和酒店業的維修,但由於能源法規的限制,其成長速度低於螢幕相關領域。

汽車外飾照明,尤其是自我調整頭燈,由於需要進行嚴格的光度測試,價格居高不下。指示牌和戶外廣告則採用亮度超過5000尼特且防護等級達到IP65的LED模組,主要得益於智慧城市專案的持續需求。園藝和紫外線殺菌是高利潤領域,透過光譜調諧和殺菌波長,彌補了出貨量較低的不足。即使燈泡市場日趨成熟,這些細分市場仍在不斷擴大LED模組的潛在市場規模。

區域分析

預計到2025年,亞太地區將佔全球LED模組市場銷售額的67.73%,並將在2031年之前維持17.05%的複合年成長率。中國擁有全球70%以上的晶片產能,仍在持續擴張。京東方華燦在江蘇建設的價值20億元人民幣(約2.8億美元)的晶圓廠將新增50萬片的月產能,主要面向汽車和Mini-LED背光市場(BOE.COM)。印度正崛起為第二個LED中心,公共部門路燈競標規模已達數千萬套。日本憑藉日亞化學工業株式會社的磷光體專利,在紫外線LED和微型LED等細分領域保持主導,並獲得價格溢價。

北美是全球第二大銷售市場,這主要得益於相關法規禁止使用螢光安定器以及自我調整LED頭燈的快速普及。在加拿大,不斷上漲的碳價促使建築業主將40%的維修預算用於照明昇級。同時,墨西哥靠近美國邊境的各州計劃在2025年將其模組組裝產能提高25%,以滿足近岸OEM製造商的需求。

在歐洲,嚴格的生態設計標準使維修步伐保持穩定,其中德國和英國在辦公大樓和公共建築維修處於領先地位。中東和非洲市場主要集中在阿拉伯聯合大公國和沙烏地阿拉伯的知名智慧城市區域,而南美洲和非洲的需求則零星出現,主要與離網太陽能和LED計畫有關。在所有地區,政策壓力和本地製造業激勵措施共同推動了LED模組市場的高速成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 住宅和商業建築維修中LED的快速普及

- 將智慧照明與支援物聯網的建築系統整合

- 政府正逐步淘汰低效照明設備。

- 汽車製造商向LED頭燈和內裝模組的過渡

- 小型、靈活的模組,可實現新的外形尺寸

- 透過使用板載驅動IC,降低了系統物料清單成本。

- 市場限制因素

- 產能過剩導致價格下跌和利潤率承壓

- 高功率模組的溫度控管挑戰

- 主要外延晶圓半導體供應鏈的波動

- 模組層面缺乏通用安全標準

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 模組類型

- COB(板載晶片)LED模組

- SMD LED模組

- 線性LED模組

- LED背光模組

- 高功率LED模組

- 其他模組類型(靈活型、迷你型、客製化組裝型)

- 透過使用

- 一般照明

- 住宅

- 商業

- 產業

- 汽車照明

- 顯示器和背光

- 招牌和廣告

- 其他用途(建築、園藝、紫外線防護、特殊應用)

- 輸出範圍

- 低功率(5瓦或以下)

- 中功率(5瓦以上至30瓦以下)

- 高功率(超過 30 瓦)

- 按外形規格

- 剛性LED模組

- 軟性LED模組

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太國家

- 南美洲

- 中東

- 非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Signify NV

- ams-OSRAM AG

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- Lumileds Holding BV

- Cree LED, Inc.

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Acuity Brands, Inc.

- Eaton Corporation plc

- General Electric Company

- Toyoda Gosei Co., Ltd.

- Bridgelux, Inc.

- Citizen Electronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- Epistar Corporation

- Opple Lighting Co., Ltd.

- Hubbell Incorporated

- Dialight plc

- Zhejiang Yankon Group Co., Ltd.

- Edison Opto Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the lED module market size was USD 8.50 billion in 2025 and USD 9.69 billion in 2026, and is expected to reach USD 20.70 billion by 2031, growing at a CAGR of 16.39% over 2026-2031.

This report is Segmented by Module Type (COB, SMD, Linear, Backlight, High-Power, and Other Module Types), Application (General Lighting, Automotive, Display and Backlighting, Signage, and Other Applications), Power Range (Low, Mid, and High), Form Factor (Rigid, and Flexible), and Geography (North America, Europe, and Other Geographies). The Market Forecasts are Provided in Terms of Value (USD).

Global LED Module Market Trends and Insights

Smart-Lighting Integration With IoT-Enabled Building Systems

Commercial construction increasingly embeds networked lighting that treats every LED module as an intelligent edge device collecting occupancy, daylight, and health telemetry. In 2025, sixty percent of new floor space commissioned in North America and Europe funded wireless gateways, sensor arrays, and cloud subscriptions worth more than USD 550 000 per site. Measured savings of 30 to 40 percent on electricity and maintenance deliver sub-three-year paybacks, satisfying CFO hurdle rates. The new Matter protocol unifies Zigbee, Thread, and proprietary meshes, slashing commissioning time and calls. Predictive analytics schedule replacements before outages, lifting tenant satisfaction and landlord valuation premiums.

Government-Mandated Phase-Out of Inefficient Light Sources

Legislators on three continents are compressing compliance timelines, converting what was a voluntary efficiency upgrade into a statutory requirement. The European Union banned most halogen stock-keeping units in 2021 and heightened customs enforcement in 2024, blocking non-compliant imports at ports. California's 2025 Title 24 revision stipulates that 90 percent of installed lighting power in new commercial buildings must originate from LED sources equipped with occupancy sensors and daylight harvesting. China's 2024 roadmap demands public infrastructure luminaires exceeding 130 lumens per watt by 2026. These synchronized decrees guarantee sustained demand for modular LED retrofit kits and integrated ceiling panels.

Thermal Management Challenges in High-Power Modules

High-power modules operating above 30 watts struggle to shed the heat generated by tightly packed emitters, and junction temperatures that drift beyond 125 °C can cut luminous output in half within a few thousand hours. Meeting new IEC 62031:2026 thermal resistance reporting rules forces suppliers to invest in infrared imaging, finite element simulation, and more expensive metal core or ceramic substrates. Passive heat sinks add weight and volume, while active fans raise noise and reliability worries. Horticulture and industrial luminaires feel the impact first because ambient temperatures already sit high, amplifying warranty claims and deterring aggressive overdrive strategies among buyers.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Shift to LED Headlamps and Interior Modules

- Rapid LED Penetration in Residential and Commercial Retrofits

- Price-Erosion and Margin Pressure Owing to Excess Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

LED backlight modules are advancing at a 16.81% CAGR from 2026-2031, significantly outpacing overall LED module market growth as Mini-LED technology scales into premium televisions and monitors. SMD modules retained 33.61% of the LED module market share in 2025, buoyed by strong cost-performance in residential and commercial luminaires. Backlight designs tap thousands of Mini-LEDs to achieve greater-than 1,000 local-dimming zones, pushing demand for thin, thermally efficient boards. Meanwhile, chip-on-board (COB) architectures win in automotive headlamps where compact footprints meet 10,000-lumen targets without enlarging reflector housings. Linear modules continue to dominate office troffer retrofits because contractors can replace fluorescent lamps without rewiring, preserving tight project timelines.

The LED module market benefits from new specialty niches: flexible strips illuminate curved signage, and UV-C modules expand into healthcare. COB's monolithic die reduces thermal resistance and elevates color rendering above 90, fitting museum and retail needs. Cree LED's L2 PCBA platform packages this benefit with integrated drivers, thereby trimming luminaire OEM design cycles. As automation lowers Mini-LED cost, backlight modules will progressively steal share from SMD in high-brightness displays, reinforcing a mixed portfolio strategy for suppliers.

General lighting represented 42.59% of the LED module market size in 2025, yet is ceding relative momentum to display and backlighting, forecast to climb at a 16.98% CAGR through 2031. Direct-lit TV and gaming-monitor refresh cycles fuel replacement demand, while HDR-ready panels push local-dimming counts upward, inflating module content per screen. Commercial lighting still absorbs the largest module volume via office, retail, and hospitality retrofits, but energy regulations are flattening growth relative to screen-based segments.

Automotive exterior lighting, especially adaptive headlamps, commands premium pricing due to rigorous photometric testing. Signage and outdoor advertising install high-brightness modules rated above 5,000 nits and protected to IP65, sustaining demand from smart-city projects. Horticulture and UV-C disinfection form high-margin verticals where spectral tuning or germicidal wavelengths offset lower shipment volumes. Each niche enlarges the addressable LED module market even as the bulb segment matures.

Geography Analysis

Asia-Pacific accounted for 67.73% of the LED module market revenue in 2025 and is projected to post a 17.05% CAGR through 2031. China controls more than 70% of global chip capacity and continues to expand; BOE Huacan's RMB 2 billion (USD 280 million) wafer plant in Jiangsu will add 500,000 pieces per month, aimed at automotive and Mini-LED backlights BOE.COM. India is emerging as a secondary hub as public-sector street-light tenders scale into the tens of millions of units. Japan retains leadership in UV and micro-LED specialties, leveraging Nichia's phosphor patents to command price premiums.

North America ranks second by revenue, sustained by regulatory bans on fluorescent ballasts and the accelerating adoption of adaptive LED headlamps. Canada's rising carbon price moved building owners to allocate 40% of retrofit budgets to lighting upgrades, while Mexican states near the U.S. border expanded module-assembly capacity by 25% during 2025 to serve nearshoring OEMs.

Europe's strict Ecodesign thresholds guarantee a steady retrofit cadence, with Germany and the United Kingdom spearheading office and municipal conversions. Middle East and Africa markets concentrate on prestige smart-city districts in the United Arab Emirates and Saudi Arabia, whereas South America and Africa see sporadic demand tied to off-grid solar-LED programs. Across all regions, policy pressure and local manufacturing incentives intersect to keep the LED module market on a high-growth trajectory.

- Signify N.V.

- ams-OSRAM AG

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- Lumileds Holding B.V.

- Cree LED, Inc.

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Acuity Brands, Inc.

- Eaton Corporation plc

- General Electric Company

- Toyoda Gosei Co., Ltd.

- Bridgelux, Inc.

- Citizen Electronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- Epistar Corporation

- Opple Lighting Co., Ltd.

- Hubbell Incorporated

- Dialight plc

- Zhejiang Yankon Group Co., Ltd.

- Edison Opto Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid LED Penetration in Residential and Commercial Retrofits

- 4.2.2 Smart-Lighting Integration with IoT-Enabled Building Systems

- 4.2.3 Government-Mandated Phase-Out of Inefficient Light Sources

- 4.2.4 Automotive OEM Shift to LED Headlamps and Interior Modules

- 4.2.5 Miniaturised & Flexible Modules Enabling New Form-Factors

- 4.2.6 On-Board Driver IC Adoption Reducing System BOM Cost

- 4.3 Market Restraints

- 4.3.1 Price-Erosion and Margin Pressure Owing to Excess Capacity

- 4.3.2 Thermal Management Challenges in High-Power Modules

- 4.3.3 Semiconductor Supply-Chain Volatility for Key Epitaxy Wafers

- 4.3.4 Absence of Universal Module-Level Safety Standards

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Module Type

- 5.1.1 COB (Chip-on-Board) LED Modules

- 5.1.2 SMD LED Modules

- 5.1.3 Linear LED Modules

- 5.1.4 LED Backlight Modules

- 5.1.5 High-Power LED Modules

- 5.1.6 Others, Module Type (Flexible, Mini, Custom Assemblies)

- 5.2 By Application

- 5.2.1 General Lighting

- 5.2.2 Residential

- 5.2.3 Commercial

- 5.2.4 Industrial

- 5.2.5 Automotive Lighting

- 5.2.6 Display and Backlighting

- 5.2.7 Signage and Advertising

- 5.2.8 Others, Application (Architectural, Horticulture, UV, Specialty)

- 5.3 By Power Range

- 5.3.1 Low Power (less than or equal to 5 W)

- 5.3.2 Mid Power (greater than 5 W to less than or equal to 30 W)

- 5.3.3 High Power (greater than 30 W)

- 5.4 By Form Factor

- 5.4.1 Rigid LED Modules

- 5.4.2 Flexible LED Modules

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East

- 5.5.6 Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 ams-OSRAM AG

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 Nichia Corporation

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Cree LED, Inc.

- 6.4.7 Seoul Semiconductor Co., Ltd.

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 Acuity Brands, Inc.

- 6.4.10 Eaton Corporation plc

- 6.4.11 General Electric Company

- 6.4.12 Toyoda Gosei Co., Ltd.

- 6.4.13 Bridgelux, Inc.

- 6.4.14 Citizen Electronics Co., Ltd.

- 6.4.15 Everlight Electronics Co., Ltd.

- 6.4.16 Epistar Corporation

- 6.4.17 Opple Lighting Co., Ltd.

- 6.4.18 Hubbell Incorporated

- 6.4.19 Dialight plc

- 6.4.20 Zhejiang Yankon Group Co., Ltd.

- 6.4.21 Edison Opto Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年)

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年) 歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測

二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測 氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測

氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測