|

市場調查報告書

商品編碼

2065584

歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Europe LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

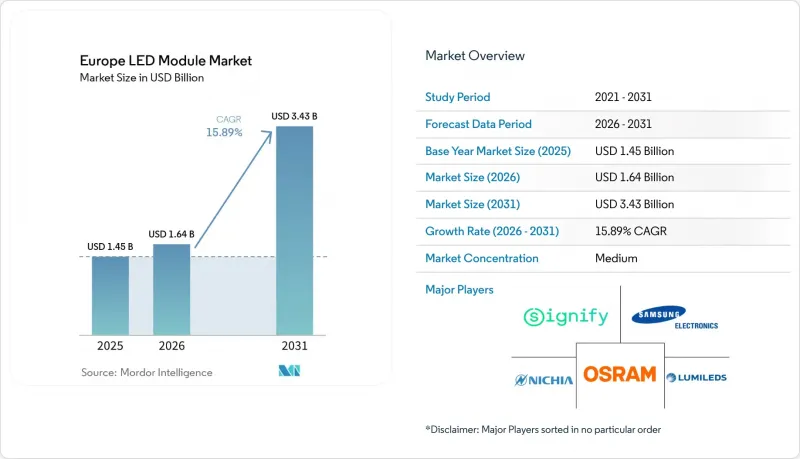

根據 Mordor Intelligence 預測,歐洲 LED 模組市場規模預計在 2025 年達到 14.5 億美元,2026 年達到 16.4 億美元,到 2031 年達到 34.3 億美元,2026 年至 2031 年的複合年成長率為 15.89%。

本報告按模組類型(COB LED模組、SMD LED模組、線性LED模組、LED背光模組及其他模組類型)、應用領域(通用照明、汽車照明、顯示器和背光、指示牌及其他應用)、功率範圍(低、中、高)以及外形規格(剛性LED模組和軟性LED模組)進行細分。市場預測以美元(USD)計價。

歐洲LED模組市場的趨勢與洞察

歐盟迅速淘汰白熾燈泡

根據歐盟2019/2020生態設計法規,白熾燈和鹵素燈的銷售被強制停止,而2024年9月重新啟用能源效率標籤制度進一步強化了這項規定。這些措施使傳統照明產品從零售通路消失,並進一步推動了歐洲LED模組市場向住宅、商業和市政應用領域的LED燈具更換週期轉型。這一轉變使模組化LED產品佔據了有利地位,因為更換模組比運作整個燈具更容易,設施管理人員和電工可以減少停機時間,並簡化已安裝照明系統的備件管理。德國韋德馬克市維修4300盞LED路燈,展示了這項轉型在實踐中的應用。改造後,能耗降低了80%,年耗電量減少了90萬千瓦時,並節省了27萬歐元(約30.5萬美元)的成本。這些模組的額定壽命為12萬小時。這項轉型對SMD和COB供應商尤其有利。這是因為這些規格符合常見的維修要求,例如標準化的插座和溫度控管,適用於各種照明設備。德國聯邦網路局和法國競爭、消費者和通訊監管總局等機構的國內監管執法,透過限制不合規產品的進口和灰色市場產品在歐洲LED模組市場的流通,持續支持合規供應商。

歐洲綠色新政中的能源效率目標

歐洲綠色交易的目標是到2030年將最終能源消耗降低11.7%,這一目標以能源效率指令(EU) 2023/1791為基礎,為歐洲LED模組市場創造了長期需求基礎,因為與白熾燈泡相比,LED模組可節能高達90%。此外,該政策框架將2028年至2030年間的年度能源效率要求提高至1.9%,使得照明昇級成為各成員國公共和商業建築營運商的關鍵採購重點。歐盟委員會估計,到2030年,照明昇級每年將節省41.9太瓦時(TWh)的能源,並為消費者節省520億歐元(586億美元),從而鞏固LED模組作為排放建築和地方政府基礎設施排放最具成本效益手段之一的地位。第8條採購規則優先考慮能源效率等級最高的產品,明確了符合標準的模組供應商參與公開競標的管道,同時將鹵素燈和螢光排除在主要更換週期之外。慕尼黑進行的自適應路燈試點計畫測試了3000K至1700K的可變相關色溫和調光模式,結果表明,在非高峰時段可節能高達93%。這引起了人們對具有控制功能的連網LED系統的關注,其應用遠不止於簡單的燈具更換。

LED模組製造業初始資本投入高

在歐洲建立一條具競爭力的LED模組生產線,仍需在晶片鍵合設備、回流焊接爐、自動化光學檢測設備和環境測試實驗室等方面投入5000萬至1.5億歐元(約合5600萬至1.69億美元),這限制了新進入者,並導致產能持續集中在現有供應商手中。隨著功率等級、基板和光學架構的需求不斷變化,以及技術進步可能導致設備在3至5年內過時,這種負擔進一步加重。南歐和東歐的中小型組裝資金籌措管道有限,預計到2025年,歐洲投資銀行提供的LED製造貸款總額僅2.5億歐元(約2.82億美元),遠低於支持國內生產進一步擴張所需的水平。歐司朗宣布將在2030年前投資5.88億歐元(約6.63億美元)擴大其在奧地利的業務,這表明資本壁壘正在被克服,尤其對於那些財務基礎雄厚、獲得政府支持或在半導體行業具有戰略意義的公司而言更是如此。在歐洲LED模組市場,軟性及專業化領域受到的衝擊更為顯著,因為這些領域的產量較低,且客製化規格普遍存在,固定成本無法像通用照明產品線那樣有效地分攤。

細分市場分析

2025年,SMD LED模組在歐洲LED模組市場佔33.43%的佔有率。這反映了其在住宅和商業通用照明應用中的成熟應用,並得益於3528、5050和2835等標準化封裝,這些封裝便於自動化組裝,並保證了不同照明燈具品牌之間的兼容性。隨著消費性電子產品製造商轉向對比度更高、局部調光更密集的mini-LED和micro-LED架構,預計2026年至2031年間,背光模組的複合年成長率將達到16.43%。飛利浦於2026年10月推出的MLED981 RGB mini-LED電視凸顯了這一轉變,該電視擁有11,520個局部調光區域,峰值亮度達2,500尼特。由於COB模組在散熱性能和光通量密度方面比SMD產品高出15%至25%,因此它們繼續應用於工業高棚照明和零售聚光燈領域。線性LED模組在建築內凹照明和櫥櫃底部安裝中仍然發揮著重要作用。這是因為它們的連續排列方式適合狹窄的安裝空間,並且能夠輕鬆營造出一條連續光線的視覺效果。

功率超過30瓦的高功率LED模組在垂直農業領域也備受矚目。北歐地區的垂直農業設施利用這些模組實現了全年作物生長週期的控制,其最大光合有效輻射(PAR)效率可達3.5 μmol/J。其他模組形式,例如軟性燈條、迷你LED陣列和客製化組件,則應用於更專業的專案。例如,2026年冬季奧運場館米蘭體育館就採用了54,560條客製化的線性LED燈條,總長度達50公里。這些燈條採用IP67防護等級的RGBW模組,並透過DMX512控制,涵蓋3,785個光路。在這種組合中,溫度控管和色彩品質是關鍵的競爭優勢。雖然COB模組在顯色指數(CRI)要求達到95或更高、R9值要求達到80或更高的應用中仍然佔據優勢,但在CRI達到80即可滿足需求的通用照明應用中,成本更低的SMD產品仍然佔據主導地位。背光模組的設計要求十分特殊,例如高度必須小於1毫米,並且需要與量子點薄膜精確耦合。因此,投資主要集中在覆晶封裝和微透鏡陣列技術上。為了符合有關閃爍限制和最低發光效率的生態設計法規,歐洲LED模組市場中,排名較低的SMD供應商已被淘汰出局,生產集中在擁有卓越驅動和散熱設計能力的頂級製造商手中。

2025年,通用照明將佔歐洲LED模組市場規模的42.72%。這主要歸功於LED模組在住宅、商業和工業領域逐步取代螢光槽、下照燈和高棚燈。預計2026年至2031年,顯示器和背光產業將以16.78%的複合年成長率成長。這是因為螢幕製造商和汽車製造商正致力於在高階電視、儀表叢集和中央資訊顯示器中採用局部調光技術。西歐對高階電視的需求推動了這一趨勢,預計2025年65吋以上螢幕將佔總銷售量的38%,這將持續迫使供應商提供更高密度和更亮的背光系統。

汽車照明仍然是一個戰略性領域。這是因為矩陣式LED頭燈和數位光投射系統需要亞毫秒級的開關速度和車規級認證,這縮小了能夠滿足全球OEM專案需求的供應商範圍。歐司朗(OSRAM)報告稱,其「數位光」平台的設計採用額已超過5億歐元(5.64億美元),這表明在歐洲LED模組市場,特定應用的功能可能比大規模生產的經濟效益更為重要。

在指示牌和廣告領域,採用防護等級為IP65或IP67、亮度超過10,000尼特的戶外模組對於確保日間可見性仍然至關重要,性能和成本在該領域都佔據著舉足輕重的地位。其他應用包括建築立面照明、針對450奈米和660奈米峰值波長最佳化的園藝模組、工作波長為265-280奈米的UV-C紫外線殺菌模組,以及色溫(CCT)可在3,000K至6,500K範圍內調節的手術照明。目前的應用格局呈現出明顯的兩極化:通用照明專案與汽車、園藝和顯示器背光等專業細分市場。在後者中,更高的利潤率得益於更嚴格的公差、更長的認證週期和更先進的光學要求。雖然通用照明仍然是銷售量的基礎,但由於需要進行難以快速複製的認證測試、頻譜調諧和系統整合,專業應用在技術價值方面仍然佔據更大的佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟迅速淘汰白熾燈泡

- 歐洲綠色交易中的能源效率目標

- LED每流明成本更低

- 歐盟委員會正加緊為智慧城市維修提供資金。

- 辦公空間對人性化、可調光的白色模組的需求日益成長。

- 北歐垂直農業設施的需求激增

- 市場限制因素

- LED模組製造業初始資本投入高

- 半導體晶片供應鏈中斷

- 嚴格的生態設計法規限制有害物質的使用

- 歐盟《基本原料法》實施後稀土元素磷光體價格波動

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按模組類型

- COB(板載晶片)LED模組

- SMD LED模組

- 線性LED模組

- LED背光模組

- 高功率LED模組

- 其他模組類型(靈活型、迷你型、客製化組裝型)

- 透過使用

- 一般照明

- 住宅

- 商業

- 產業

- 汽車照明

- 顯示器和背光

- 招牌和廣告

- 其他用途(建築、園藝、紫外線、特殊照明)

- 一般照明

- 輸出範圍

- 低功率(5瓦或以下)

- 中功率(5瓦以上至30瓦以下)

- 高功率(超過 30 瓦)

- 按外形規格

- 剛性LED模組

- 軟性LED模組

- 國家

- 英國

- 德國

- 法國

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Signify NV

- Osram Opto Semiconductors GmbH

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- Lumileds Holding BV

- Seoul Semiconductor Co., Ltd.

- Cree LED

- Tridonic GmbH and Co KG

- Bridgelux, Inc.

- Citizen Electronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- Lextar Electronics Corporation

- LG Innotek Co., Ltd.

- Edison Opto Corporation

- Fagerhult Group

- Zumtobel Group AG

- Hella GmbH and Co. KGaA

- Stanley Electric Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe lED module market size is projected to be USD 1.45 billion in 2025, USD 1.64 billion in 2026, and reach USD 3.43 billion by 2031, growing at a CAGR of 15.89% from 2026 to 2031.

This report is Segmented by Module Type (COB LED Modules, SMD LED Modules, Linear LED Modules, LED Backlight Modules, and Other Module Types), Application (General Lighting, Automotive, Display and Backlighting, Signage, and Other Applications), Power Range (Low, Mid, and High), and Form Factor (Rigid LED Modules and Flexible LED Modules). The Market Forecasts are Provided in Terms of Value (USD).

Europe LED Module Market Trends and Insights

Rapid Phasing Out Of Incandescent Lighting Across EU

The mandatory withdrawal of incandescent and halogen lamps under Ecodesign Regulation (EU) 2019/2020, reinforced by energy-label rescaling in September 2024, removed legacy options from retail channels and pushed the Europe LED Module Market further toward LED-based replacement cycles in residential, commercial, and municipal uses. This change has favored modular LED products because facility managers and electrical contractors can replace modules more easily than complete luminaires, which lowers downtime and reduces spare-part complexity across installed fleets.Wedemark municipality in Germany showed how this shift works in practice when it retrofitted 4,300 LED lanterns, cut energy use by 80%, reduced annual consumption by 900,000 kWh, and avoided EUR 270,000 (USD 305,000) in costs, with module life rated at 120,000 hours. The transition has been especially favorable for SMD and COB suppliers because these formats fit common retrofit requirements for standardized sockets and thermal management across a wide set of luminaires. National enforcement by authorities such as Germany's Bundesnetzagentur and France's DGCCRF continues to support compliant suppliers by limiting the room for non-compliant imports and gray-market products in the Europe LED Module Market.

Energy Efficiency Targets Under European Green Deal

The European Green Deal target to reduce final energy consumption by 11.7% by 2030, backed by the Energy Efficiency Directive (EU) 2023/1791, creates a long-duration demand base for the Europe LED Module Market because LED modules can deliver up to 90% energy savings against incandescent alternatives. The policy framework also raises annual savings obligations to 1.9% during 2028-2030, which keeps lighting upgrades on procurement agendas for public bodies and commercial building operators across member states. European Commission assessments linked lighting upgrades to 41.9 TWh of annual electricity savings by 2030 and EUR 52 billion (USD 58.6 billion) in consumer savings, which keeps LED modules positioned as one of the lowest-cost pathways for abatement in buildings and municipal infrastructure. Article 8 procurement rules favor top energy-performance classes, which gives compliant module suppliers a clearer path into public tenders while keeping halogen and fluorescent options out of the main replacement cycle. Munich's adaptive street-lighting pilot, which tested tunable correlated color temperature from 3,000K to 1,700K and dimming profiles, showed energy reductions of up to 93% during low-traffic periods and pushed attention beyond simple lamp replacement toward networked LED systems with controls.

High Initial Capital Expenditure For LED Module Manufacturing

Building a competitive LED module line in Europe still requires EUR 50 million to EUR 150 million (USD 56 million to USD 169 million) in upfront spending on die-bonding tools, reflow ovens, automated optical inspection, and environmental chambers, which limits new entry and keeps capacity concentrated among established suppliers. This burden is heavier because technology shifts can strand equipment within 3-5 years as demand moves across power classes, substrates, and optical architectures. Smaller assemblers in Southern and Eastern Europe face a narrower financing window, and European Investment Bank lending for LED manufacturing totaled only EUR 250 million (USD 282 million) in 2025, which remains below what would be needed to support stronger domestic scaling. ams OSRAM's commitment of EUR 588 million (USD 663 million) through 2030 for its Austria expansion shows that the capital barrier is manageable mainly for companies with balance-sheet strength, policy support, or strategic semiconductor relevance The burden is felt more sharply in flexible and specialty segments because lower volumes and custom formats do not spread fixed costs as efficiently as general-lighting lines do in the Europe LED Module Market.

Other drivers and restraints analyzed in the detailed report include:

- Declining LED Cost Per Lumen

- Surge In European Commission Funding For Smart City Retrofits

- Supply Chain Disruptions For Semiconductor Chips

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SMD LED Modules held 33.43% of Europe LED Module Market share in 2025, which reflected their entrenched use in residential and commercial general lighting where standardized footprints such as 3528, 5050, and 2835 packages support automated assembly and interchangeability across luminaire brands. Backlight Modules are projected to grow at a 16.43% CAGR through 2026-2031 as consumer-electronics manufacturers shift toward mini-LED and micro-LED architectures that support higher contrast and denser local dimming. Philips underlined this shift with the October 2026 launch of the MLED981 RGB Mini-LED TV, which featured 11,520 local dimming zones and 2,500-nit peak brightness. COB modules continue to serve industrial high-bay and retail spotlight applications where thermal performance and lumen density support a 15% to 25% premium over SMD alternatives. Linear LED modules remain important in architectural cove lighting and under-cabinet installations because continuous-run formats fit narrow installation spaces and simplify the visual effect of uninterrupted light lines.

High-power LED modules above 30 W are also gaining traction in vertical farming, where photosynthetically active radiation efficacies of up to 3.5 μmol/J help Nordic facilities run controlled crop cycles across the year. Other module formats, including flexible strips, mini-LED arrays, and custom assemblies, are serving more specialized projects such as Arena Milano, where 54,560 bespoke linear LED bars spanning 50 km were specified for the 2026 Winter Olympics venue with IP67-rated RGBW modules and DMX512 control across 3,785 universes. Thermal management and color quality are shaping competitive positions inside this mix, because COB modules remain strong in applications that need CRI of 95 or more and R9 values above 80, while lower-cost SMD products continue to dominate utility lighting where CRI 80 is sufficient. Backlight modules face separate design demands such as sub-1 mm height limits and precise coupling with quantum-dot films, which keeps investments focused on flip-chip attachment and micro-lens arrays. Ecodesign compliance around flicker limits and minimum efficacy has pushed lower-tier SMD suppliers out of higher-quality categories and concentrated volume around Tier-1 manufacturers with stronger driver and thermal design capabilities in the Europe LED Module Market.

General Lighting accounted for 42.72% of the Europe LED Module Market size in 2025, as LED modules replaced fluorescent troffers, downlights, and high-bay fixtures across residential, commercial, and industrial settings. Display and Backlighting is expected to advance at a 16.78% CAGR through 2026-2031 as screen makers and vehicle manufacturers move toward local-dimming architectures in premium televisions, instrument clusters, and center-information displays. Premium TV demand in Western Europe supported this trend, with 65-inch and larger screens accounting for 38% of unit sales in 2025, which kept pressure on suppliers to deliver denser and brighter backlight systems.

Automotive Lighting remains a strategic segment because matrix LED headlamps and digital-light projection systems require sub-millisecond switching and automotive-grade qualification, which narrows the field of suppliers that can serve global OEM programs. ams OSRAM reported more than EUR 500 million (USD 564 million) in design wins for its Digital Light platform, showing how application-specific capability can outweigh volume economics in the Europe LED Module Market.

Signage and Advertising continue to depend on outdoor-rated modules with IP65 or IP67 protection and brightness levels above 10,000 nits for daylight readability, which keeps this segment tied to performance rather than only cost. Other applications span architectural facade lighting, horticulture modules optimized for 450 nm and 660 nm peaks, UV-C disinfection modules operating at 265-280 nm, and surgical lighting with adjustable CCT from 3,000K to 6,500K. The application mix now shows a clear split between commodity general-lighting programs and specialty niches such as automotive, horticulture, and display backlighting, where margins are supported by tighter tolerances, longer qualification periods, and stronger optical requirements. General lighting remains the volume base, but specialty applications keep a larger share of technical value because they demand qualification testing, spectral tuning, and system integration that are harder to replicate quickly.

List of Companies Covered in this Report:

- Signify N.V.

- Osram Opto Semiconductors GmbH

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- Cree LED

- Tridonic GmbH and Co KG

- Bridgelux, Inc.

- Citizen Electronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- Lextar Electronics Corporation

- LG Innotek Co., Ltd.

- Edison Opto Corporation

- Fagerhult Group

- Zumtobel Group AG

- Hella GmbH and Co. KGaA

- Stanley Electric Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Phasing-Out of Incandescent Lighting Across the EU

- 4.2.2 Energy-Efficiency Targets Under the European Green Deal

- 4.2.3 Declining LED Cost Per Lumen

- 4.2.4 Surge in European Commission Funding for Smart-City Retrofits

- 4.2.5 Growing Preference for Human-Centric Tunable-White Modules in Office Spaces

- 4.2.6 Demand Spike From Vertical-Farming Facilities in Nordics

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Expenditure for LED-Module Manufacturing

- 4.3.2 Supply-Chain Disruptions for Semiconductor Chips

- 4.3.3 Stringent Ecodesign Regulations Limiting Hazardous-Substance Use

- 4.3.4 Volatile Rare-Earth-Phosphor Prices Post-EU Critical Raw Materials Act

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Module Type

- 5.1.1 COB (chip-on-board) LED modules

- 5.1.2 SMD LED modules

- 5.1.3 Linear LED modules

- 5.1.4 LED backlight modules

- 5.1.5 High-power LED modules

- 5.1.6 Other module types (flexible, mini, custom assemblies)

- 5.2 By Application

- 5.2.1 General lighting

- 5.2.1.1 Residential

- 5.2.1.2 Commercial

- 5.2.1.3 Industrial

- 5.2.2 Automotive lighting

- 5.2.3 Display and backlighting

- 5.2.4 Signage and advertising

- 5.2.5 Other applications (architectural, horticulture, UV, specialty lighting)

- 5.2.1 General lighting

- 5.3 By Power Range

- 5.3.1 Low Power (less than or equal to 5 W)

- 5.3.2 Mid Power (greater than 5 W to less than or equal to 30 W)

- 5.3.3 High Power (greater than 30 W)

- 5.4 By Form Factor

- 5.4.1 Rigid LED modules

- 5.4.2 Flexible LED modules

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Osram Opto Semiconductors GmbH

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 Nichia Corporation

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Seoul Semiconductor Co., Ltd.

- 6.4.7 Cree LED

- 6.4.8 Tridonic GmbH and Co KG

- 6.4.9 Bridgelux, Inc.

- 6.4.10 Citizen Electronics Co., Ltd.

- 6.4.11 Everlight Electronics Co., Ltd.

- 6.4.12 Lextar Electronics Corporation

- 6.4.13 LG Innotek Co., Ltd.

- 6.4.14 Edison Opto Corporation

- 6.4.15 Fagerhult Group

- 6.4.16 Zumtobel Group AG

- 6.4.17 Hella GmbH and Co. KGaA

- 6.4.18 Stanley Electric Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年)

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年) LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測

二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測 氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測

氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測