|

市場調查報告書

商品編碼

2065504

亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

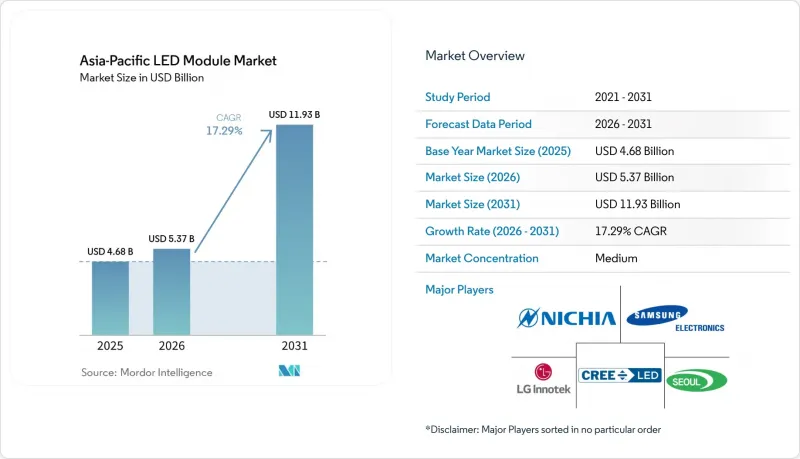

根據 Mordor Intelligence 預測,亞太地區 LED 模組市場預計將從 2025 年的 46.8 億美元成長到 2026 年的 53.7 億美元,到 2031 年達到 119.3 億美元,2026 年至 2031 年的複合年成長率為 17.29%。

本報告按模組類型(COB、SMD、線性、背光、高功率及其他模組類型)、應用領域(通用照明、汽車、顯示器及背光、指示牌及其他應用)、功率範圍(低、中、高)、外形尺寸(剛性、軟性)以及國家(中國、日本、印度及其他亞太地區)進行細分。市場預測以美元(USD)為單位。

亞太地區LED模組市場趨勢及洞察。

高功率LED的每流明成本正在快速下降。

晶圓級良率從25%大幅提升至75%,使得2003年至2020年間每千流明封裝成本降低了95%。近期對板載晶片(COB)產品線的升級,在保持價格不變的情況下,光通量提高了5-8%,進一步降低了每流明成本。這些成本的降低使得一些先前因投資回報瓶頸而難以實現的應用場景得以實現,例如10萬流明體育場泛光燈和3.0µmol J-1園藝照明燈具。到2025年,中國晶片製造企業已實現模組級成本降低近40%,並實現了P1.0以下小間距顯示器99.99%的晶片轉移良率。傳統供應商必須將業務重心轉向自適應光束頭燈和微型LED電影螢幕,才能擺脫價格競爭的困境。

商業建築中智慧照明生態系統的擴展

亞太地區建築自動化投資正以兩位數的速度成長,其中智慧照明是人員佔用偵測和自然光利用策略的核心。有線或無線維修專案已證實可節能40-60%,促使新加坡、上海和孟買的業主採用亞太地區LED模組市場的可控產品。桃園市6000戶的市政試點計畫凸顯了使用DALI-2和藍牙Mesh進行大規模部署的可行性。整合無線功能和感測器的模組供應商在系統層面獲得了溢價,同時與建築管理整合商合作,以確保符合印度監管要求。

主要磷光體材料供應鏈的集中化

中國提煉了全球整體80%以上的鑭、釔、銪和鈰原料,而2025年10月推出的出口許可證制度使前置作業時間延長了45天。 2025年下半年,磷光體價格飆升30%,導致沒有長期合約的買家毛利率下降高達3個百分點。庫存已膨脹至90-120天的用量,佔用了流動資金,並隨著RGB COB堆疊技術的成熟,增加了庫存過時的風險。預計澳洲和越南的礦業開發案要到2028年才能對供應來源多元化做出實質貢獻。

細分市場分析

2025年,SMD基板在亞太地區LED模組市佔率中佔31.29%,主要得益於量產獎盃燈、下照燈和條形燈的廣泛應用。出貨量趨勢也證實,亞太地區LED模組市場仍以SMD架構為主,預計2025年SMD模組將佔該地區總銷售量的三分之一。 SMD陣列透過多個結點散熱,實現了每小時超過5萬個元件的自動化高速貼裝,無需主動散熱即可達到高達181 lm W⁻¹的能源效率。在亞太地區LED模組市場中,背光模組的成長速度最快,這主要得益於mini-LED電視的訂單以及汽車駕駛座領域兩位數的成長。板載晶片(COB)產品雖然目前仍佔少數,但單一發送器的光通量密度可高達8000流明,使其成為博物館聚光燈、自我調整頭燈和影院投影的理想選擇。

競爭對手之間的市場定位呈現兩極化。 SMD供應商面臨來自中國新晉參與企業的商品化壓力,這些企業以更低的成本提供性能相當的產品;而COB專家則憑藉其獨特的陶瓷基板和反射塗層維持著利潤率。線性替換基板在商業維修市場需求強勁,而軟性條帶則正轉向間接照明和曲面標牌應用。投資於無線互連技術和高導熱複合材料的供應商正被應用於下一代汽車陣列設計。

到2025年,通用照明將佔住宅、商業和工業設施總需求的44.68%,但隨著一線城市家庭照明普及率超過60%,其成長速度正在放緩。在亞太地區的LED模組市場,顯示背光燈的佔有率正以17.58%的複合年成長率成長,這反映了高階電視的普及和電動汽車儀錶板的升級。工業用戶正在尋求發光效率超過140流明/瓦、壽命達10萬小時的高棚燈模組,以降低10公尺高環境的維護負擔。由於像素化頭燈和需要毫秒響應時間的動畫顯示器外部訊號,汽車照明市場正在快速擴張。

智慧型商用照明燈具整合了藍牙Mesh和Zigbee無線功能,這使得在驅動和感測技術方面擁有專業知識的供應商更具優勢。小間距數位電子看板現已低於1.0毫米,使戶外廣告看板和店內自助服務終端能夠達到與液晶電視牆相媲美的解析度。隨著零售商對產品照明高顯色性的需求日益成長,採用光學薄膜和頻譜調節演算法進行差異化生產的模組製造商能夠確保穩定的收入。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速逐步取消對使用螢光的禁令

- 高功率LED的每流明成本正在快速下降。

- 商業建築中智慧照明生態系統的擴展

- 高階顯示器中Mini-LED背光燈的激增

- 根據中國五年計劃,在地化享有優惠待遇

- 擴大專門用於園藝的LED模組的創業投資(VC)資金籌措。

- 市場限制因素

- 高功率模組持續的溫度控管挑戰

- 主要磷光體材料供應鏈的集中度

- 更嚴格的汽車電磁相容性法規所帶來的成本

- 一線城市的房屋維修需求已趨於穩定。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按模組類型

- COB(板載晶片)LED模組

- SMD LED模組

- 線性LED模組

- LED背光模組

- 高功率LED模組

- 其他模組化類型

- 透過使用

- 一般照明

- 住宅

- 商業

- 產業

- 汽車照明

- 顯示器和背光

- 招牌和廣告

- 其他用途

- 一般照明

- 輸出範圍

- 低功率(5瓦或以下)

- 中功率(5瓦以上至30瓦以下)

- 高功率(超過 30 瓦)

- 按外形規格

- 剛性LED模組

- 軟性LED模組

- 按地區

- 中國

- 日本

- 印度

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Cree LED, a Smart Global Holdings Company

- Lumileds Holding BV

- Osram GmbH

- Bridgelux, Inc.

- Everlight Electronics Co., Ltd.

- Lite-On Technology Corporation

- Stanley Electric Co., Ltd.

- Sharp Corporation

- Citizen Electronics Co., Ltd.

- Lextar Electronics Corporation

- Toyoda Gosei Co., Ltd.

- Nationstar Optoelectronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- MLS Co., Ltd.

- Refond Optoelectronics Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific lED module market size is expected to increase from USD 4.68 billion in 2025 to USD 5.37 billion in 2026 and reach USD 11.93 billion by 2031, growing at a CAGR of 17.29% over 2026-2031.

This report is Segmented by Module Type (COB, SMD, Linear, Backlight, High-Power, and Other Module Types), Application (General Lighting, Automotive, Display and Backlighting, Signage, and Other Applications), Power Range (Low, Mid, and High), and Form Factor (Rigid, and Flexible), and Country (China, Japan, India and Rest of Asia- Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific LED Module Market Trends and Insights

Rapid Decline in High-Power LED Cost per Lumen

Wafer-scale yields jumping from 25% to 75% pushed package cost per kilolumen down by 95% between 2003 and 2020. Recent chip-on-board (COB) portfolio upgrades lifted luminous flux 5-8% at unchanged prices, further shrinking dollar per lumen metrics. These savings unlock use cases once blocked by payback hurdles, such as 100,000-lumen stadium floods and 3.0 µmol J-1 horticulture fixtures. Chinese chip fabs drove module-level cost drops near 40% in 2025 on sub-P1.0 fine-pitch displays, hitting 99.99% die-transfer yields. Legacy suppliers must now pivot toward adaptive driving beam headlamps or micro-LED cinema screens to escape price wars.

Expansion of Smart Lighting Ecosystems in Commercial Buildings

Asia-Pacific building-automation investments are expanding at double-digit rates, and smart lighting sits at the heart of occupancy sensing and daylight harvesting strategies. Demonstrated energy savings of 40-60% in wired or wireless retrofits have convinced property owners in Singapore, Shanghai, and Mumbai to specify controllable Asia-Pacific LED module market SKUs. Municipal pilots like Taoyuan's 6,000-pole project validate large-scale deployments using DALI-2 and Bluetooth mesh. Module vendors embedding radios and sensors enjoy a systems-level premium while partnering with building-management integrators to guarantee compliance with India's code requirements.

Supply-Chain Concentration of Key Phosphor Materials

China refines more than 80% of global lanthanum, yttrium, europium, and cerium feedstock, and its October 2025 export license mechanism extends lead times by 45 days. Phosphor powders jumped 30% in late 2025, trimming gross margin by up to three points for buyers lacking long contracts. Inventories have ballooned to 90-120 days, locking working capital and heightening obsolescence risk if RGB COB stacks mature. Mining projects in Australia and Vietnam will not materially diversify supply before 2028.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Mini-LED Backlighting for High-End Displays

- Accelerating Phase-Out of Fluorescent Lighting Mandates

- Persistent Thermal Management Challenges in High-Power Modules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SMD boards captured 31.29% of the Asia-Pacific LED module market share in 2025, supported by mass-manufactured troffers, downlights, and strip fixtures. Shipment trends confirm that the Asia-Pacific LED module market remains anchored in SMD architectures, which accounted for one-third of 2025 regional revenue. SMD arrays dissipate heat across multiple junctions, tolerate automated high-speed placement exceeding 50,000 components per hour, and meet efficacy targets up to 181 lm W-1 without active cooling. The Asia-Pacific LED module market size, attributed to backlight modules, is expanding fastest, propelled by mini-LED television orders and double-digit growth in automotive cockpits. Chip-on-board entries, although still a minority, offer flux densities up to 8,000 lumens from a single emitter, ideal for museum spots, adaptive headlamps, and cinema projection.

Competitive positioning is diverging. SMD providers face commodity erosion as new Chinese entrants match performance at lower costs, whereas COB specialists shield margins through proprietary ceramic substrates and reflective coatings. Linear replacement boards remain resilient in commercial retrofits, while flexible strips migrate toward ambient lighting and curved signage duties. Suppliers that invest in no-wire interconnects and high-thermal conductivity composites are winning design-ins for next-generation automotive arrays.

General lighting still supplied 44.68% of 2025 demand across residential, commercial, and industrial premises, but its growth decelerates as household penetration in tier-1 cities surpasses 60%. The Asia-Pacific LED module market share weighted to display backlighting is climbing at a 17.58% CAGR, reflecting premium television diffusion and instrument-cluster upgrades in electric vehicles. Industrial buyers pursue high-bay modules with >140 lm W-1 efficacy and 100,000-hour lifetimes to curb maintenance at 10-m ceiling heights. Automotive lighting expands briskly thanks to pixelated headlamps and animated exterior signals that require millisecond response times.

Smart-ready commercial luminaires bundle Bluetooth mesh or Zigbee radios, tilting the specification in favor of vendors with embedded driver and sensing know-how. Fine-pitch digital signage drops below P1.0 mm, allowing outdoor billboards and in-store kiosks to rival LCD video walls in perceived resolution. Module makers differentiating through optical films and spectrum-tuning algorithms can lock in sticky revenues as retailers demand high color rendering for merchandise illumination.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Cree LED, a Smart Global Holdings Company

- Lumileds Holding B.V.

- Osram GmbH

- Bridgelux, Inc.

- Everlight Electronics Co., Ltd.

- Lite-On Technology Corporation

- Stanley Electric Co., Ltd.

- Sharp Corporation

- Citizen Electronics Co., Ltd.

- Lextar Electronics Corporation

- Toyoda Gosei Co., Ltd.

- Nationstar Optoelectronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- MLS Co., Ltd.

- Refond Optoelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Phase-Out of Fluorescent Lighting Mandates

- 4.2.2 Rapid Decline in High-Power LED Cost per Lumen

- 4.2.3 Expansion of Smart Lighting Ecosystems in Commercial Buildings

- 4.2.4 Surge in Mini-LED Backlighting for High-End Displays

- 4.2.5 Localization Incentives Under China's Five-Year Plan

- 4.2.6 Growing VC Funding for Horticulture-Specific LED Modules

- 4.3 Market Restraints

- 4.3.1 Persistent Thermal Management Challenges in High-Power Modules

- 4.3.2 Supply-Chain Concentration of Key Phosphor Materials

- 4.3.3 Stringent Automotive EMC Compliance Costs

- 4.3.4 Plateauing Retrofit Demand in Tier-1 Cities

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Module Type

- 5.1.1 COB (Chip-on-Board) LED Modules

- 5.1.2 SMD LED Modules

- 5.1.3 Linear LED Modules

- 5.1.4 LED Backlight Modules

- 5.1.5 High-Power LED Modules

- 5.1.6 Others, Module Type

- 5.2 By Application

- 5.2.1 General Lighting

- 5.2.1.1 Residential

- 5.2.1.2 Commercial

- 5.2.1.3 Industrial

- 5.2.2 Automotive Lighting

- 5.2.3 Display and Backlighting

- 5.2.4 Signage and Advertising

- 5.2.5 Others, Application

- 5.2.1 General Lighting

- 5.3 By Power Range

- 5.3.1 Low Power (less than or equal to 5 W)

- 5.3.2 Mid Power (greater than 5 W to less than or equal to 30 W)

- 5.3.3 High Power (greater than 30 W)

- 5.4 By Form Factor

- 5.4.1 Rigid LED Modules

- 5.4.2 Flexible LED Modules

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 LG Innotek Co., Ltd.

- 6.4.5 Cree LED, a Smart Global Holdings Company

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 Osram GmbH

- 6.4.8 Bridgelux, Inc.

- 6.4.9 Everlight Electronics Co., Ltd.

- 6.4.10 Lite-On Technology Corporation

- 6.4.11 Stanley Electric Co., Ltd.

- 6.4.12 Sharp Corporation

- 6.4.13 Citizen Electronics Co., Ltd.

- 6.4.14 Lextar Electronics Corporation

- 6.4.15 Toyoda Gosei Co., Ltd.

- 6.4.16 Nationstar Optoelectronics Co., Ltd.

- 6.4.17 Hongli Zhihui Group Co., Ltd.

- 6.4.18 Dominant Opto Technologies Sdn. Bhd.

- 6.4.19 MLS Co., Ltd.

- 6.4.20 Refond Optoelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年)

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年) 歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測

二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測 氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測

氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測