|

市場調查報告書

商品編碼

2063982

北美高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)North America High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

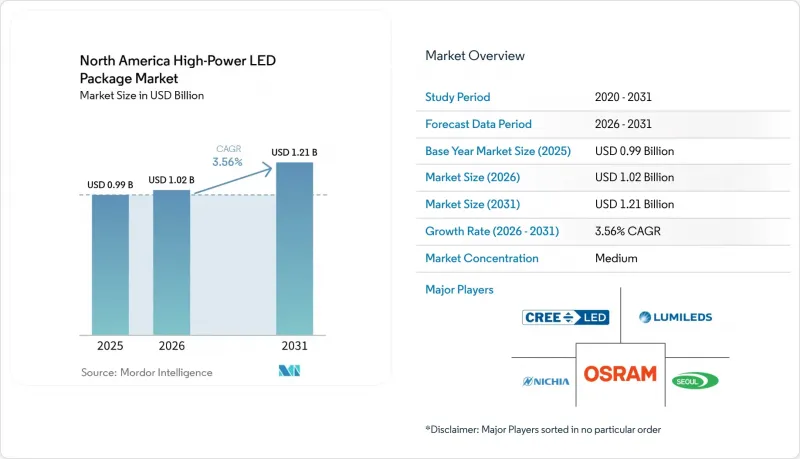

根據 Mordor Intelligence 預測,北美高功率LED構裝市場規模將從 2025 年的 9.9 億美元和 2026 年的 10.2 億美元成長到 2031 年的 12.1 億美元,2026 年至 2031 年的複合年成長率為 3.56%。

本報告按輸出功率範圍(1W–3W、3W–10W、10W以上)、封裝架構(單晶片封裝、多晶片封裝、COB封裝及其他)、應用領域(通用照明、汽車照明、顯示器與背光、特殊應用)以及地區(美國、加拿大、墨西哥)進行細分。市場預測以美元(USD)為單位。

北美高功率LED構裝市場趨勢與洞察

政府正逐步淘汰低效燈具。

聯邦和州政府的法規正迫使白熾燈和螢光產品迅速退出市場,推動了對高功率燈具的需求激增,這些燈具能夠在現有燈具外殼內實現每瓦120流明的光通量。這項轉變的驅動力來自美國能源局將於2028年7月生效的法規,以及2024年至2027年間六個州頒布的禁令,這些法規使得3至10瓦的發光元件成為改裝下照燈和卡車燈的標準選擇。經銷商正在趕在淘汰期限前清理舊庫存,而燈具製造商則在快速開發符合發光效率、流明密度和色彩品質目標的板載晶片(COB)和多晶片模組。由於合規性審核會使性能不佳的產品面臨召回風險,因此擁有磷光體和熱設計方面內部專業知識的供應商將從中受益。這為結構性成長創造了有利條件,並將持續到預測期中期。

LED在汽車前燈的快速普及

自我調整遠光燈的核准正在重新定義頭燈的組件配置。隨著LED在乘用車中的滲透率已超過70%,以及新的頭燈眩光法規的實施,像素級照明系統正從豪華車型走向大眾市場。矩陣陣列將數十個可獨立控制的晶片排列在緊湊的基板上,是實現高功率、低熱阻和精確分級的理想選擇。 LG Innotek的超薄像素模組在2026年國際消費電子展(CES)上榮獲大獎,它展示了小型化以及V2X(車聯網)外形規格的發展前景如何將照明轉變為安全和通訊工具。佔據汽車市場69.2%佔有率的一級供應商正利用專利聯盟和交叉許可來確保設計方案的採用,從而保證在2027款車型上市前實現多年的產能擴張。

驅動電流超過 1A 時,溫度控管和可靠性面臨挑戰。

當驅動電流超過 1 安培時,封裝的結溫會升至 150 度C以上,且每升高 10 度C,壽命就會減半。設計人員必須採用陶瓷基板、均熱板或主動冷卻,但這會導致成本和重量增加。由於熱降,發光效率會從 350 毫安培的 150 流明/瓦下降到 1.5 安培時的近 120 流明/瓦,抵消了減少發光元件數量的優勢。由於循環電流會導致介面材料劣化和焊點疲勞,從而增加保固風險,許多照明燈具會將額定電流降低至額定電流的 70%。在基板和磷光體材料的技術進步能夠降低光源產生的熱量之前,高電流運行仍將是注重成本的通用照明產業面臨的成本限制。

細分市場分析

在北美高功率LED構裝市場,10瓦及以上功率段的LED產品正以4.11%的複合年成長率快速成長。這主要是因為體育場館、倉庫和道路營運商更傾向於選擇單封裝亮度超過10,000流明的產品。板載晶片(COB)技術正逐漸佔據主導地位。這是因為將裸晶直接安裝在金屬基板上,可以將熱阻控制在2 K/W以下,因此可以使用更小的散熱器。到2025年,1-3瓦功率段的LED產品將保持47.88%的市場佔有率,主要用於改裝現有下照燈,因為在這些應用中,與現有燈具外殼和安裝空間的兼容性至關重要。

隨著美國能源局(DOE) 的光通量效率法規和 8K 廣播合約的實施,設計人員正將光通量集中到更少的光學點上,從而減少組裝工作量和反射器數量,成長勢頭正在轉變。為了抓住這一趨勢,Lumileds 等供應商於 2026 年 3 月推出了 LUXEON CS 系列產品,提供 6.3 毫米至 22 毫米的 LES 直徑以及 90 和 95 的顯色指數 (CRI) 選擇。 3 瓦至 10 瓦功率範圍仍然是高棚照明燈具的一個過渡領域,但與其他極端功率頻寬相比,它缺乏明顯的經濟優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府正逐步淘汰低效照明設備。

- LED在汽車前燈的快速普及

- 穩定高功率LED構裝的平均售價

- 8K 體育和廣播照明標準將提高流明需求。

- 暗夜天空法規推廣低藍光夜景套餐

- 在PoE智慧照明設計中,高壓CSP LED是首選。

- 市場限制因素

- 1. 超過 1A 電流的驅動器面臨的溫度控管和可靠性挑戰

- 高初始成本和中功率LED的比較

- 氦氣短缺正在擾亂氮化鎵晶圓的製造過程。

- 稀土元素紅色磷光體供應面臨的地緣政治風險

- 科技趨勢

- 監理情勢

- 宏觀經濟因素的影響

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 1 W~3 W

- 3 W~10 W

- 超過10瓦

- 以建築學為例

- 單晶片封裝(SMD/分離式)

- 多晶片封裝(SMD)

- COB(板載晶片)

- 其他

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 特殊/小眾

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- ams OSRAM International GmbH

- Lumileds Holding BV

- Cree LED Inc.

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Citizen Electronics Co., Ltd.

- Bridgelux Inc.

- Luminus Devices Inc.

- Epistar Corporation

- Toyoda Gosei Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Signify NV

- LITE-ON Technology Corporation

- Broadcom Inc.

- Foshan Refond Optoelectronics Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america high-power LED package market size is projected to expand from USD 0.99 billion in 2025 and USD 1.02 billion in 2026 to USD 1.21 billion by 2031, registering a CAGR of 3.56% between 2026 to 2031.

This report is Segmented by Power Range (1 W To 3 W, 3 W To 10 W, and Above 10 W), Architecture (Single-Die Packages, Multi-Die Packages, COB, and Others), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America High-Power LED Package Market Trends and Insights

Government-Mandated Phase-Out of Inefficient Lamps

Federal and state rules are forcing incandescent and fluorescent products off shelves on a compressed timeline, triggering a sharp pull in demand for high-power packages that can clear 120 lumens per watt within existing fixture envelopes. The U.S. Department of Energy rule, effective July 2028, and six state bans enacted between 2024 and 2027 anchor this shift, making 3-watt to 10-watt emitters the default choice for retrofit downlights and track heads. Distributors are liquidating legacy inventory ahead of cut-off dates, while luminaire brands are fast-tracking chip-on-board and multi-die modules that meet efficacy, lumen density, and color-quality targets. Vendors with in-house phosphor and thermal expertise benefit because compliance audits expose under-performing products to recall risk. The result is a structural growth tailwind that will persist through the middle of the forecast window.

Rapid LED Penetration in Automotive Headlamps

Adaptive driving beam approval is reshaping the front-lighting bill of materials. Passenger-car LED penetration already exceeds 70%, and pixel-level systems are moving from luxury to mass-market models under new regulatory headlamp glare rules. Matrix arrays place dozens of individually addressable dice onto compact substrates, favoring high-power packages with low thermal resistance and precise binning. LG Innotek's ultra-thin pixel module, which won a CES 2026 award, illustrates how shrinking form factors and vehicle-to-everything projections are turning lighting into a safety and communications asset. Tier-one suppliers holding 69.2% automotive share are leveraging patent pools and cross-licenses to secure design wins, locking in multi-year volume ramps as 2027 model launches approach.

Thermal Management and Reliability Challenges Above 1 A Drive

Driving packages at currents above 1 ampere elevates junction temperatures beyond 150 °C, cutting lifetime in half for every 10 °C rise. Designers must adopt ceramic boards, vapor chambers, or active cooling, which adds cost and weight. Thermal droop reduces efficacy from 150 lumens per watt at 350 mA to near 120 lumens per watt at 1.5 A, negating emitter-count savings. Interface material degradation and solder fatigue under cycling raise warranty exposure, so many luminaires derate to 70% of nameplate current. Until breakthroughs in substrate or phosphor materials lower heat at the source, high-current operation will remain cost-capped in cost-sensitive general lighting.

Other drivers and restraints analyzed in the detailed report include:

- 8K Sports-Broadcast Lighting Standards Lifting Lumen Demand

- Dark-Sky Regulations Driving Low-Blue NightScape Packages

- Helium Shortage Disrupting GaN Wafer Processing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The above 10 watt tier of the North America high-power LED package market size is on a 4.11% CAGR path as sports venues, warehouses, and roadway operators favor single-package outputs above 10,000 lumens. Chip-on-board formats dominate because they mount bare dice directly onto metal-core boards, delivering thermal resistance under 2 K/W and supporting smaller heatsinks. In 2025 the 1 watt-3 watt tier retained 47.88% share, serving retrofit downlights that prize footprint compatibility with legacy housings.

Growth momentum is shifting as the DOE efficacy rule and 8K broadcast contracts encourage designers to consolidate flux into fewer optical points, cutting assembly labor and reflector count. Vendors such as Lumileds introduced LUXEON CS in March 2026 to exploit this trend, offering LES diameters from 6.3 mm to 22 mm and CRI options of 90 and 95. The 3 watt-10 watt range remains a transitional bracket for high-bay fixtures but lacks the clear economic edge enjoyed by either extreme.

List of Companies Covered in this Report:

- Nichia Corporation

- ams OSRAM International GmbH

- Lumileds Holding B.V.

- Cree LED Inc.

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Citizen Electronics Co., Ltd.

- Bridgelux Inc.

- Luminus Devices Inc.

- Epistar Corporation

- Toyoda Gosei Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Signify N.V.

- LITE-ON Technology Corporation

- Broadcom Inc.

- Foshan Refond Optoelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-Mandated Phase-Out of Inefficient Lamps

- 4.2.2 Rapid LED Penetration in Automotive Headlamps

- 4.2.3 Stabilization of High-Power LED Package ASPs

- 4.2.4 8K Sports-Broadcast Lighting Standards Lifting Lumen Demand

- 4.2.5 Dark-Sky Regulations Driving Low-Blue Nightscape Packages

- 4.2.6 PoE Smart-Lighting Designs Favoring High-Voltage CSP LEDs

- 4.3 Market Restraints

- 4.3.1 Thermal Management and Reliability Challenges Above 1 A Drive

- 4.3.2 Up-Front Cost Premium Versus Mid-Power LEDs

- 4.3.3 Helium Shortage Disrupting GaN Wafer Processing

- 4.3.4 Geopolitical Risk to Rare-Earth Red Phosphors Supply

- 4.4 Technology Outlook

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 1 W - 3 W

- 5.1.2 3 W - 10 W

- 5.1.3 Above 10 W

- 5.2 By Architecture

- 5.2.1 Single-die Packages (SMD / Discrete)

- 5.2.2 Multi-die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 ams OSRAM International GmbH

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Cree LED Inc.

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Citizen Electronics Co., Ltd.

- 6.4.10 Bridgelux Inc.

- 6.4.11 Luminus Devices Inc.

- 6.4.12 Epistar Corporation

- 6.4.13 Toyoda Gosei Co., Ltd.

- 6.4.14 NationStar Optoelectronics Co., Ltd.

- 6.4.15 Hongli Zhihui Group Co., Ltd.

- 6.4.16 Sanan Optoelectronics Co., Ltd.

- 6.4.17 Signify N.V.

- 6.4.18 LITE-ON Technology Corporation

- 6.4.19 Broadcom Inc.

- 6.4.20 Foshan Refond Optoelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年)

全球LED背光市場規模、市佔率、趨勢及成長分析報告(2026-2034年) 歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

歐洲LED模組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)LED模組:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED模組:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)高功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測

二極體市場規模、佔有率和成長分析:按類型、材料、應用、最終用途和地區分類-2026-2033年產業預測 氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測

氮化鎵LED晶片市場機會、成長要素、產業趨勢分析及2026-2035年預測