|

市場調查報告書

商品編碼

2064022

法國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)France Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

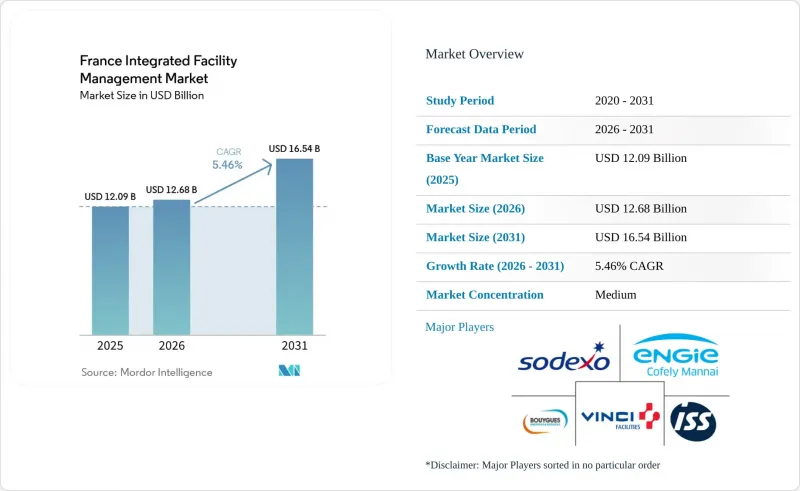

根據 Mordor Intelligence 預測,法國綜合設施管理市場規模將從 2025 年的 120.9 億美元成長到 2026 年的 126.8 億美元,到 2031 年達到 165.4 億美元,2026 年至 2031 年的複合年成長率為 5.46%。

本報告按服務類型(硬性設施管理[資產管理、機電/暖通空調服務等]、軟性設施管理[辦公室支援/安保、清潔服務、餐飲服務等])和最終用戶(商業、飯店、醫療、設施/公共基礎設施等)分類。市場預測以美元計價。

法國綜合設施管理市場的趨勢與洞察

公共基礎設施外包綜合服務需求增加

法國公共部門擁有9000萬平方米的國有房地產,並管理著數千個市政機構和公共設施,這些機構和設施仍然嚴重依賴內部團隊和分散的合約。第三項部長級法令規定,面積超過1000平方公尺的第三產業建築必須在2030年前將能耗降低40%,並在2040年前降低50%,並要求每年提交營運報告(OPERAT),違規者可能面臨最高7,500歐元(約8,475美元)的罰款。如果沒有集中式的監控和報告工具,這些義務難以履行,這促使法國綜合設施管理市場中越來越多的公共採購負責人轉向一站式合約。隨著2030年目標的檢驗日期臨近(2026年12月),監理要求正從長期規劃轉向積極主動的採購活動。此外,由於將不合規建築物列入官方登記冊可能會引起公眾對地方政府領導人的關注,因此,除了營運成本壓力外,政治風險也會影響法國綜合設施管理 (IFM) 市場的外包決策。

加速醫療機構向績效合約轉型

法國醫院正從傳統的P1-P2-P3維護體系轉向「全球績效公共合約」(Marche Public Global de Performance),該合約將技術服務和能源保障相結合。在尼斯大學醫院(CHU de Nice)巴斯德醫院2025年的競標中,一份價值3000萬歐元(3390萬美元)的合約涵蓋了暖通空調、電氣和消防系統,其中能源和環境績效佔中標標準的15%。 2026年1月,馬蒂格綜合醫院授予Equans Services Batiments et Infrastructures公司一份為期108個月、價值746.4341萬歐元(840萬美元)的能源績效合約。綜合設施管理(CPOM)架構持續加強老年照護機構(EHPAD)和其他醫療機構的預算管理,支持法國綜合設施管理(IFM)市場中較長期、更一體化的服務模式。在法國 IFM 市場,能夠提供「盡力而為」的維護服務,並且能夠透過合約保證降低成本的供應商,更有可能獲得更長的合約期限和更高的客戶維繫率。

暖通空調和機電工程師的結構性短缺限制了硬體維修。

法國綜合設施管理市場面臨技術人才結構性錯配的問題。每年需要新增15,000名暖通空調(中央通風、暖氣和供水)技術人員,但培訓計畫畢業的只有8,000人。這導致每年技術人員缺口達7,000人,且未考慮退休因素。此外,約30%的在職暖通空調技術人員年齡已超過55歲。有關建築自動化控制系統(BACS)合規性和低全球暖化潛值(GWP)冷媒的法規加劇了這一問題,這些法規要求技術人員掌握數位控制知識、熟練相關協議並持有最新的F-Gaz認證。因此,在法國綜合設施管理(IFM)市場,硬體維修)服務提供者需要在確保能源效率和運轉率的同時,應對不斷上漲的招募成本和人才獲取困難。儘早投資遠端診斷和人工智慧監控正成為一種切實可行的解決方案,因為它可以減少每個站點所需的技術人員數量,並幫助服務提供者維持履行合約的能力。

細分市場分析

至2025年,軟性設施管理(soft FM)將佔據法國綜合設施管理(IFM)市場64.61%的佔有率。這反映了公共機構、醫療機構和企業設施對清潔、餐飲、保全、接待和辦公室支援等服務的巨大需求。由於後疫情時代的衛生規範已深深融入眾多客戶類別的服務規範中,軟性設施管理在法國綜合設施管理市場持續受到青睞。彈性辦公空間的擴展也拓展了捆綁式軟性服務的範圍。到2026年,法國的彈性辦公空間將超過140萬平方公尺,其中85萬平方公尺位於法國法蘭西島大區。此外,營運辦公室模式的服務內容也在發生變化,單一供應商現在可以提供包括接待、清潔、餐飲和工作場所協調在內的全方位服務。保安和害蟲防治在軟性設施管理領域仍屬於小規模業務板塊,但隨著營業時間更長的客戶要求持續監控和更高的服務連續性,其業務範圍正在擴大。

預計到2031年,硬體設施管理將以6.22%的複合年成長率成長,成為法國綜合設施管理(IFM)服務細分市場中成長最快的領域。法國綜合設施管理產業的加速發展主要得益於BACS法規、第三產業法規以及2026年實施的RE2020擴展措施,這些措施都要求企業具備更先進的技術能力,而僅靠軟體模式無法滿足這些需求。根據2024年OPERAT評估報告,許多受監管企業仍未能按計劃實現其2030年目標,這加劇了維修的緊迫性,並縮短了向多技術合約過渡的進程。隨著客戶越來越傾向於從單一供應商獲得安裝、維護、測量和報告服務,擁有內部機電工程、感測器部署能力和報告能力的供應商在訂單這些合約方面更具優勢。因此,複雜性驅動的需求正在迅速超過數量主導的需求,這正在逐步改變法國IFM市場的整體服務組成。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 公共基礎設施領域對綜合外包服務的需求日益成長

- 加速醫療機構向績效合約轉型

- 利用物聯網感測器實現預測性設施管理的智慧建築正在發展。

- 對能源效率目標的監管壓力加大

- 資料中心的快速擴張正在推動對專業設施管理 (FM) 的需求。

- 辦公空間「飯店化」的新趨勢正在推動軟性設施管理商品搭售。

- 市場限制因素

- 熟練的暖通空調和機電技術人員短缺

- 從2025年起,退休金改革將導致人事費用上升,利潤率將受到擠壓。

- 互聯建築管理系統中的網路安全風險

- 地方政府分散採購慣例

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章:預測市場規模與成長率

- 按服務類型

- 硬體設施管理

- 資產管理

- 機電/暖通空調服務

- 消防系統和安全

- 其他硬體設施管理服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟性設施管理服務

- 硬體設施管理

- 按最終用戶行業分類

- 商業

- 飯店業

- 設施和公共基礎設施

- 醫療保健

- 工業和流程部門

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- VINCI Facilities

- ENGIE Cofely

- Sodexo SA

- ISS A/S

- Bouygues Energies & Services

- Atalian Global Services

- Derichebourg Multiservices

- Elior Group

- Samsic Facility

- Apleona GmbH

- Dalkia Groupe EDF

- CBRE Group Inc.

- Compass Group plc

- Serco Group plc

- JLL Integrated Facilities Management

- Cushman & Wakefield plc

- BNP Paribas Real Estate Property Management

- GSF Groupe

- Groupe Penelope

- SPIE Facilities

第7章 市場機會與未來展望

According to Mordor Intelligence, the france integrated facility management market size is expected to increase from USD 12.09 billion in 2025 to USD 12.68 billion in 2026 and reach USD 16.54 billion by 2031, growing at a CAGR of 5.46% over 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Healthcare, Institutional and Public Infrastructure, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Integrated Facility Management Market Trends and Insights

Rising Demand for Outsourced Integrated Services in Public Infrastructure

France's public sector owns 90 million m2 of government real estate and manages thousands of municipal and institutional sites that still depend heavily on in-house teams or fragmented contracts. The Tertiary Decree requires 40% energy consumption cuts by 2030 and 50% by 2040 for tertiary buildings above 1,000 m2, with annual OPERAT reporting and penalties that can reach EUR 7,500 (USD 8,475), per legal entity for non-compliance. Those obligations are difficult to manage without centralized monitoring and reporting tools, which is pushing more public buyers toward bundled contracts in the France integrated facility management market. The December 2026 verification milestone against 2030 targets is turning a regulatory requirement into active procurement rather than a long-range planning exercise. Municipal leaders also face public visibility risk when non-compliant buildings appear on official registers, so outsourcing decisions are being shaped by political exposure as well as operating cost pressure in the France integrated facility management (IFM) market.

Accelerating Shift to Performance-Based Contracts in Healthcare Facilities

French hospitals are moving away from legacy P1-P2-P3 maintenance structures and toward Marche Public Global de Performance contracts that combine technical services with energy guarantees. A 2025 tender at CHU de Nice, Hopital Pasteur covered HVAC, electrical, and fire systems under a EUR 30 million contract (USD 33.9 million), with energy and environmental performance carrying 15% of award criteria. In January 2026, Centre Hospitalier de Martigues awarded a 108-month energy performance contract worth EUR 7,464,341 (USD 8.4 million), to Equans Services Batiments and Infrastructures. The CPOM framework continues to reinforce budget discipline across EHPADs and other healthcare settings, which supports longer and more integrated service models in the France integrated facility management market. Providers that can contractually guarantee savings instead of offering only best-effort maintenance are likely to secure longer tenures and better retention in the France IFM market.

Structural HVAC And MEP Skills Shortage Constraining Hard FM Delivery

The France integrated facility management market faces a structural mismatch in technical labor because the sector needs 15,000 new CVC technicians each year while training programs produce only 8,000 graduates. That leaves a yearly deficit of 7,000 profiles before accounting for retirements, and nearly 30% of active CVC technicians are already older than 55 years. The problem is becoming more acute because BACS compliance and low-GWP refrigerant rules now require digital controls knowledge, protocol familiarity, and updated F-Gaz certification. Hard FM providers are therefore being asked to guarantee energy and uptime outcomes while facing higher hiring costs and tighter staffing availability in the France IFM market. Early investment in remote diagnostics and AI-assisted monitoring is becoming a practical response because it reduces technician intensity per site and helps providers protect contract delivery capacity.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Smart Buildings Enabling Predictive FM Via IoT Sensors

- Heightened Regulatory Pressure on Energy Efficiency Targets

- Escalating Public Sector Payroll Costs From CNRACL Employer Contribution Increases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft facility management held 64.61% of the France integrated facility management market share in 2025, which reflects the scale of cleaning, catering, security, reception, and office support demand across institutional, healthcare, and corporate sites. The France IFM market has continued to favor Soft FM because post-pandemic hygiene protocols remain embedded in-service specifications across many client categories. Flexible workspace expansion also widened the addressable base for bundled soft services, with more than 1.4 million m2 of flex office space in France in 2026 and 850,000 m2 located in Ile-de-France. Operated office models are also changing service content because a single provider may now deliver reception, cleaning, catering, and workplace coordination under an all-inclusive operating model. Security and pest control remain smaller lines within Soft FM, but they are gaining scope as clients with longer operating hours ask for constant monitoring and higher service continuity.

Hard facility management is projected to expand at 6.22% CAGR, representing the fastest France integrated facility management (IFM) market size growth by service type through 2031. The France integrated facility management industry is seeing this acceleration because the BACS Decree, the Tertiary Decree, and the 2026 RE2020 expansion all require deeper technical delivery than a soft-only model can provide. The 2024 OPERAT assessment showed that many obligated companies were still behind the path needed for the 2030 target, which keeps retrofit urgency high and shortens conversion timelines for multi-technical contracts. Providers with in-house MEP engineering, sensor deployment capability, and reporting competence are better placed to win this work because clients increasingly want one provider to install, maintain, measure, and report. The result is that complexity-weighted demand is rising faster than volume-led demand, which is gradually changing service mix across the France IFM market.

List of Companies Covered in this Report:

- VINCI Facilities

- ENGIE Cofely

- Sodexo S.A.

- ISS A/S

- Bouygues Energies & Services

- Atalian Global Services

- Derichebourg Multiservices

- Elior Group

- Samsic Facility

- Apleona GmbH

- Dalkia Groupe EDF

- CBRE Group Inc.

- Compass Group plc

- Serco Group plc

- JLL Integrated Facilities Management

- Cushman & Wakefield plc

- BNP Paribas Real Estate Property Management

- GSF Groupe

- Groupe Penelope

- SPIE Facilities

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Outsourced Integrated Services in Public Infrastructure

- 4.2.2 Accelerating Shift to Performance-Based Contracts in Healthcare Facilities

- 4.2.3 Growth of Smart Buildings Enabling Predictive FM via IoT Sensors

- 4.2.4 Heightened Regulatory Pressure on Energy Efficiency Targets

- 4.2.5 Rapid Expansion of Data Centers Requiring Specialized FM

- 4.2.6 Emerging "Hotelization" Trend in Office Spaces Driving Soft FM Bundling

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled HVAC and MEP Technicians

- 4.3.2 Margin Squeeze from Rising Labor Costs Post 2025 Pension Reforms

- 4.3.3 Cybersecurity Risks in Connected Building Management Systems

- 4.3.4 Fragmented Procurement Practices in Municipal Bodies

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 VINCI Facilities

- 6.4.2 ENGIE Cofely

- 6.4.3 Sodexo S.A.

- 6.4.4 ISS A/S

- 6.4.5 Bouygues Energies & Services

- 6.4.6 Atalian Global Services

- 6.4.7 Derichebourg Multiservices

- 6.4.8 Elior Group

- 6.4.9 Samsic Facility

- 6.4.10 Apleona GmbH

- 6.4.11 Dalkia Groupe EDF

- 6.4.12 CBRE Group Inc.

- 6.4.13 Compass Group plc

- 6.4.14 Serco Group plc

- 6.4.15 JLL Integrated Facilities Management

- 6.4.16 Cushman & Wakefield plc

- 6.4.17 BNP Paribas Real Estate Property Management

- 6.4.18 GSF Groupe

- 6.4.19 Groupe Penelope

- 6.4.20 SPIE Facilities

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)