|

市場調查報告書

商品編碼

2064014

德國綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Germany Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

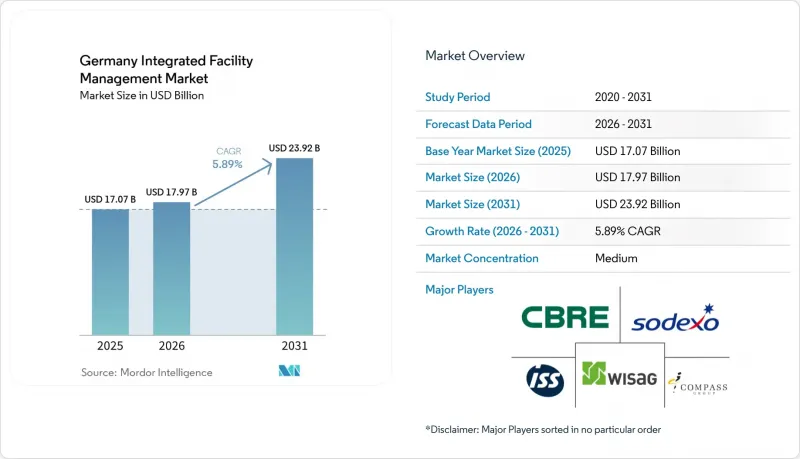

根據 Mordor Intelligence 預測,德國綜合設施管理市場規模預計將從 2025 年的 170.7 億美元成長到 2026 年的 179.7 億美元,到 2031 年達到 239.2 億美元,2026 年至 2031 年的複合年成長率為 5.89%。

本報告按服務類型(硬性設施管理[資產管理、機電和暖通空調服務等]、軟性設施管理[辦公室支援和安保、清潔服務、餐飲服務等])和最終用戶行業(商業、酒店、醫療保健、公共機構和公共基礎設施等)進行細分。市場預測以價值(美元)為單位。

德國綜合設施管理市場的趨勢與洞察

提高能源效率法規和永續性

能源法規是德國綜合設施管理(IFM)市場短期內最顯著的成長要素,因為這些法規正將合規義務從一次性安裝項目轉移到持續的營運任務。德國《通用能源法》(GEG)第71a條規定,所有暖氣、冷氣或通風系統功率超過290千瓦的非住宅建築,必須在2024年12月31日前安裝經認證的建築自動化和控制系統。這擴大了技術設施管理(FM)服務提供者的潛在基本客群,涵蓋了辦公室、工廠、醫院、大學和零售設施等場所。即使這些系統已經安裝完畢,業主仍然需要服務提供者能夠透過開放介面監控系統效能、分析能源資料、維護控制系統並定期建立運作記錄。這使得合約價值超越了基本的維護範疇。這波合規浪潮並非德國獨有,因為2024年頒布的《能源性能指令》(EPBD)及其相關的公共建築能源效率要求,也要求業主遵守更嚴格的建築性能標準和更完善的營運規範。這使得德國綜合設施管理市場對那些能夠將現場工程、基於軟體的監控和能源最佳化整合到一個負責任的服務結構中的公司更具吸引力。

資料中心的成長帶動了對專業硬體維修。

資料中心正在挑戰德國整合設施管理市場的技術極限,因為它們需要運作為核心的服務模式,而這種模式難以在標準商業建築合約中有效複製。預計到2025年,德國裝置容量將達到約3,000兆瓦,並預計在2030年之前進一步成長。這將持續催生對冷卻、配電、消防、維護計劃和全天候事件回應的需求。谷歌正在德國實施55億歐元(約64億美元)的投資計劃,投資年限為2026年至2029年。該計劃表明,大型營運商仍然致力於開設新站點並提高能源效率,從而擴大未來數位基礎設施技術設施管理需求的管道。人工智慧驅動環境下的機架密度已經超過了傳統暖通空調合約能夠有效管理的等級。因此,為了保持競爭力,服務供應商需要具備液冷、資料中心基礎設施管理(DCIM)整合能力以及符合廢熱法規的專業知識。因此,在德國 IFM 市場的這一領域,那些早期投資於專業工程團隊、快速反應和關鍵環境營運深度的公司將具有優勢。

設施管理(FM)人員長期短缺和薪資上漲。

在德國的綜合設施管理市場,人才取得仍然是一項重大的執行風險。這是因為軟性服務和硬性服務的需求成長速度超過了供應商招募、培訓和留住合格員工的速度。德國建築清潔業的報告顯示,45.3%的公司經常因為人手不足而拒絕新訂單,47.4%的公司表示,由於人手不足,其收入損失高達10%。這表明,勞動力短缺不僅推高了成本,而且已經限制了服務的提供。這種壓力不僅限於入門職位。自動化支援、技術設施管理和資料中心營運也需要具備專業技能的員工,而這些員工難以取得且維修成本。 2025年3月,夏里特設施管理公司發生的一起勞資糾紛表明,工資調整可能會大幅增加年度人事費用,並可能迫使公司重新評估合約價格,從而導致其大規模業務組合的利潤率下降。因此,德國綜合設施管理市場的供應商面臨著強勁的客戶需求與可靠服務水準所需的勞動力之間的持續差距。

細分市場分析

至2025年,軟性設施管理業將佔據德國綜合設施管理市場61.64%的佔有率,繼續保持其作為德國商業、工業和公共設施建築基礎設施領域最大服務集團的地位,並遙遙領先。這一規模源於清潔、餐飲、接待、廢棄物管理和場地管理——這些都是日常建築運營必不可少的服務,適用於從豪華住宅到老舊建築等各類物業。該服務基礎設施涵蓋範圍廣、持續且勞動密集,使得大型營運商能夠將日常營運打包成全國性契約,即使在資本投資週期放緩的情況下也能維持穩定的收入來源。然而,德國的綜合設施管理市場正逐步從勞動密集型套裝保險契約轉向將軟性服務與技術監督、報告要求和與永續性相關的績效指標相結合的合約。這項轉變至關重要,因為客戶越來越傾向於尋找能夠持續管理多地點設施標準的單一、負責的營運合作夥伴,而不是由多個分散的供應商分別管理各項服務。

在德國綜合設施管理市場中,硬設施管理是成長最快的服務類別,預計到2031年將以6.59%的複合年成長率成長。其主要推動要素包括強制性建築自動化自動化、節能維修專案、關鍵環境管理,以及維護非住宅物業技術資產的合規性、效率和數位化可視性的廣泛需求。根據GEFMA的報告,到2025年,德國房地產相關設施管理軟體市場將成長12.8%,其中70%的供應商將提供CAFM或IWMS工具。這表明,技術服務的交付比以往任何時候都更加依賴軟體驅動的監控和協調的工作訂單管理。實際上,德國綜合設施管理產業正在從基礎維護轉向以資料品質、運作保證和能源績效為中心的服務模式,尤其是在配備先進控制系統的建築物中。雖然小規模技術專家仍然佔據著有價值的細分市場,但德國綜合設施管理市場越來越重視那些能夠在單一合約結構中整合工程師、數位系統和全天候服務交付的供應商。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 德國公司必須實施與永續發展掛鉤的採購。

- 破舊商業地產亟待維修

- 德國各州加強能源效率法規

- 資料中心的成長正在推動對專業硬體維修) 的需求。

- 全球設施管理服務供應商擴展整合設施管理商品搭售

- 以ESG主導的外包以實現範圍3排放

- 市場限制因素

- 設施管理(FM)人員長期短缺和薪資上漲。

- 能源價格波動給FM合約的利潤率帶來了壓力。

- 聯邦州的監管碎片化

- 德國中型企業的數位化成熟度較低

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 硬設施管理

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全

- 其他硬設施管理服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟性設施管理服務

- 硬設施管理

- 按最終用戶行業分類

- 商業

- 飯店業

- 公共和機構基礎設施

- 衛生保健

- 工業和流程部門

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ISS A/S

- Sodexo SA

- Compass Group PLC

- Dussmann Stiftung & Co. KGaA

- Wisag Facility Service Holding GmbH

- Gegenbauer Holding SE & Co. KG

- SPIE Deutschland & Zentraleuropa GmbH

- Strabag PFS GmbH

- Hectas Facility Services Stiftung & Co. KG

- Apleona GmbH

- CBRE Group Inc.

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield plc

- Engie SA

- Cofely Deutschland GmbH

- Gegenbauer Holding SE & Co. KG

- WISAG Sicherheit & Service Holding GmbH & Co. KG

- KOTTER Services

- Sasse Group

- Kluh Service Management GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany integrated facility management market size is expected to increase from USD 17.07 billion in 2025 to USD 17.97 billion in 2026 and reach USD 23.92 billion by 2031, growing at a CAGR of 5.89% over 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Healthcare, Institutional and Public Infrastructure, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Integrated Facility Management Market Trends and Insights

Rising Energy Efficiency Regulations and Sustainability

Energy regulation is the clearest near-term growth force in the Germany IFM market because it turns compliance obligations into recurring operating work rather than one-time installation projects. GEG Section 71a required non-residential buildings with heating, cooling, or ventilation systems above 290 kW to install certified building automation and control systems by December 31, 2024, which widened the addressable base for technical FM providers across offices, factories, hospitals, universities, and retail assets. Once these systems are in place, building owners still need providers that can monitor performance, interpret energy data, maintain controls, and produce regular operating records through open interfaces, which lifts contract value above basic maintenance work. The compliance cycle also extends beyond Germany because the 2024 EPBD and related energy efficiency obligations in public buildings keep pushing owners toward tighter building performance standards and better operating discipline. This makes the Germany integrated facility management market more attractive for firms that can combine field engineering, software-enabled monitoring, and energy optimization within one accountable service structure.

Growth Of Data Centers Fueling Specialized Hard FM Demand

Data centers are pushing the technical edge of the Germany integrated facility management market because they require uptime-focused service models that standard commercial building contracts cannot easily replicate. Germany reached ~3000 MW of installed data center capacity in 2025, and national capacity is expected to expand further by 2030, which creates recurring demand for cooling, power distribution, fire protection, maintenance planning, and 24/7 incident response. Google's EUR 5.5 billion (USD 6.40 billion) investment program in Germany for 2026-2029. The program underlines how large operators are still adding new sites and upgrading energy profiles, which extends the pipeline for future technical FM demand in digital infrastructure. Rack densities in AI-oriented environments are moving beyond levels that conventional HVAC contracts can manage efficiently, so providers need liquid cooling knowledge, DCIM integration capability, and waste heat compliance expertise to stay relevant. This part of the Germany IFM market therefore favors firms that invest early in specialized engineering teams, faster response structures, and operational depth in critical environments.

Persistent FM Talent Shortage and Wage Inflation

Labor availability remains the main execution risk in the Germany integrated facility management market because demand growth is arriving faster than providers can recruit, train, and retain qualified staff across soft and hard services. Germany's building cleaning trade reported that 45.3% of firms regularly turned away new orders because they lacked staff, while 47.4% said the shortage caused revenue losses of up to 10%, which shows how labor scarcity is already limiting service delivery rather than only raising costs. The pressure is not limited to entry-level roles because automation support, technical FM, and data center operations also require workers with specialized skills that are harder to source and more expensive to keep. The Charite Facility Management labor dispute in March 2025 showed how wage alignment can sharply raise annual labor costs and force contract repricing or margin compression across large portfolios. As a result, providers in the Germany integrated facility management market face a persistent gap between strong client demand and the labor base needed to deliver it at reliable service levels.

Other drivers and restraints analyzed in the detailed report include:

- ESG-Driven Outsourcing to Achieve Scope 3 Emission Reductions

- Sustainability and Procurement Initiatives by German Companies

- Volatile Energy Prices Pressuring FM Contract Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft facility management segment held 61.64% of the Germany integrated facility management market share in 2025, which kept it as the largest service group by a clear margin across the country's commercial, industrial, and institutional building base. That scale comes from cleaning, catering, reception, waste handling, and grounds maintenance, all of which remain embedded in day-to-day building operations and are required across both premium assets and older building stock. The service base is broad, recurring, and labor intensive, which gives larger operators room to bundle routine activities across national contracts and maintain steady revenue flows even when capital spending cycles soften. Even so, the Germany integrated facility management market is gradually moving beyond labor-heavy bundles toward contracts that connect soft services with technical oversight, reporting requirements, and sustainability-linked performance measures. That change matters because clients increasingly want one accountable operating partner that can manage site standards consistently across multi-location portfolios rather than several fragmented vendors with separate service controls.

Hard facility management is the fastest-growing service category in the Germany integrated facility management market, and its Germany integrated facility management market size is projected to expand at a 6.59% CAGR through 2031. The strongest pull comes from building automation mandates, energy retrofit programs, critical environment management, and the broader need to keep technical assets compliant, efficient, and digitally visible across non-residential properties. GEFMA reported that Germany's real estate-related FM software market grew 12.8% in 2025, while 70% of providers offered CAFM or IWMS tools, which shows how technical service delivery now depends far more on software-enabled monitoring and coordinated work-order management than in the past. In practical terms, the Germany integrated facility management industry is moving from basic maintenance toward service models built around data quality, uptime assurance, and energy performance, especially in buildings with more advanced controls. Smaller technical specialists still hold useful niches, but the Germany integrated facility management market increasingly rewards providers that can combine engineers, digital systems, and round-the-clock service coverage within one contract structure.

List of Companies Covered in this Report:

- ISS A/S

- Sodexo SA

- Compass Group PLC

- Dussmann Stiftung & Co. KGaA

- Wisag Facility Service Holding GmbH

- Gegenbauer Holding SE & Co. KG

- SPIE Deutschland & Zentraleuropa GmbH

- Strabag PFS GmbH

- Hectas Facility Services Stiftung & Co. KG

- Apleona GmbH

- CBRE Group Inc.

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield plc

- Engie SA

- Cofely Deutschland GmbH

- Gegenbauer Holding SE & Co. KG

- WISAG Sicherheit & Service Holding GmbH & Co. KG

- KOTTER Services

- Sasse Group

- Kluh Service Management GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainability-Linked Procurement Mandates by German Corporates

- 4.2.2 Aging Commercial Real Estate Stock Requiring Retrofit FM Solutions

- 4.2.3 Rising Energy-Efficiency Regulations in Bundeslander

- 4.2.4 Growth of Data Centers Fueling Specialized Hard FM Demand

- 4.2.5 Expansion of Integrated FM Bundling by Global FM Providers

- 4.2.6 ESG-Driven Outsourcing to Achieve Scope 3 Emission Reductions

- 4.3 Market Restraints

- 4.3.1 Persistent FM Talent Shortage and Wage Inflation

- 4.3.2 Volatile Energy Prices Pressuring FM Contract Margins

- 4.3.3 Fragmented Regulatory Codes Across Federal States

- 4.3.4 Limited Digital Maturity in Mid-Sized German Enterprises

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industries

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ISS A/S

- 6.4.2 Sodexo SA

- 6.4.3 Compass Group PLC

- 6.4.4 Dussmann Stiftung & Co. KGaA

- 6.4.5 Wisag Facility Service Holding GmbH

- 6.4.6 Gegenbauer Holding SE & Co. KG

- 6.4.7 SPIE Deutschland & Zentraleuropa GmbH

- 6.4.8 Strabag PFS GmbH

- 6.4.9 Hectas Facility Services Stiftung & Co. KG

- 6.4.10 Apleona GmbH

- 6.4.11 CBRE Group Inc.

- 6.4.12 Jones Lang LaSalle Incorporated

- 6.4.13 Cushman & Wakefield plc

- 6.4.14 Engie SA

- 6.4.15 Cofely Deutschland GmbH

- 6.4.16 Gegenbauer Holding SE & Co. KG

- 6.4.17 WISAG Sicherheit & Service Holding GmbH & Co. KG

- 6.4.18 KOTTER Services

- 6.4.19 Sasse Group

- 6.4.20 Kluh Service Management GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)