|

市場調查報告書

商品編碼

2064013

英國綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)United Kingdom Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

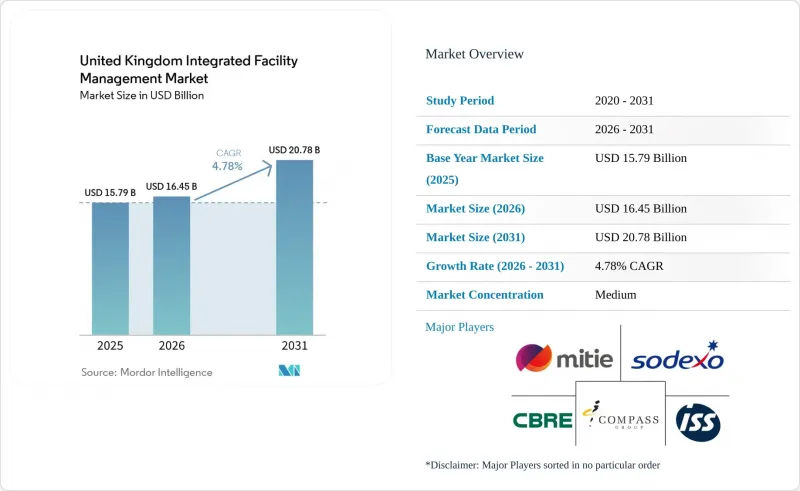

據 Mordor Intelligence 稱,英國綜合設施管理市場在 2025 年的價值為 157.9 億美元,預計到 2031 年將達到 207.8 億美元,而 2026 年為 164.5 億美元,2026 年至 2031 年預測成長率為 4.78%。

本報告按服務類型(硬性設施管理[資產管理、機電和暖通空調服務等]、軟性設施管理[辦公室支援和保全、清潔服務、餐飲服務等])和最終用戶(商業、旅館、公共機構和公共基礎設施等)進行細分。市場預測以美元計價。

英國綜合設施管理市場的趨勢與洞察

資料中心擴建催生了新的設施管理需求類別。

2024年英國資料中心被重新歸類為關鍵國家基礎設施,改變了人們對運作、容錯能力和實體安全相關服務的預期。 2025年1月發布的《人工智慧機會行動計畫》進一步強化了這一方向,將數位容量的擴展與新技術設施和配套基礎設施連結起來。對於英國綜合設施管理市場而言,這意味著對全天候機電維護、冷卻監控、高壓電氣管理、消防控制以及敏感環境專業清潔的需求發生了轉變。 AECOM在2026年2月的評估報告中警告稱,倫敦對專業機械、電氣和公共衛生分包商的需求已經超過供應,這表明關鍵環境的需求正以驚人的速度加劇勞動力供應緊張。 CBRE在2024年12月訂單了Kao Data在英國的全部資產組合的收購,這表明租戶越來越傾向於尋求能夠管理這些場所所有硬性服務和軟性服務的單一供應商。這導致英國綜合設施管理市場出現明顯的兩極化,一方是已經具備關鍵環境能力的大型供應商,另一方是仍需建立這些能力的普通供應商。

物聯網和電腦輔助設施管理(CAFM)平台正在提高智慧建築的生產力標準。

隨著物聯網感測器、建築管理系統 (BMS) 平台和電腦輔助設施管理 (CAFM) 系統在運作中物業中日益緊密地整合,英國綜合設施管理 (IFM) 市場正逐漸擺脫被動的工作訂單模式。能源安全營運標準 (ESOS) 和永續能源合規與合規 (SECR) 持續推動著這一轉變,因為對定期能源監測、文件記錄和資產級可視性的需求不斷成長。愛丁堡瑪格麗特女王大學於 2025 年 8 月啟動的 IES數位雙胞胎孿生項目,透過低成本的調度和控制變更,實現了每年 64,000 英鎊(81,280 美元)的節能效益,相當於該建築能源支出的 11%。客戶也擴大將能源和碳排放相關的關鍵績效指標 (KPI) 納入服務契約,使永續發展報告從獨立的 ESG 目標轉變為合約績效挑戰。 2025 年下半年的調查結果表明,許多設施管理負責人仍然無法追蹤或自動化大部分合規工作,這增加了報告缺陷、漏報和合約續約談判不充分的風險。在英國綜合設施管理 (IFM) 市場,能夠利用即時數據證明資產績效的供應商在競標和合約續約中獲得了更明顯的優勢。

技能不足不僅僅是招募問題。

英國綜合設施管理市場面臨的並非只是招募週期短,而是結構性勞動力短缺。這源自於多種因素的綜合作用:新冠疫情後的員工流動率上升、勞動力老化、新入行者的減少。到2025年,超過三分之二的設施管理領導者將表示招募和留住員工面臨困難,這將直接導致服務標準下降和日常合約管理能力減弱。此問題的技術層面更為嚴峻,因為暖通空調、機電和消防系統的操作需要專業訓練和多年的資格認證流程,員工才能獨立操作。商業性影響也十分巨大,因為客戶在評估合約時,如今更關注實際服務質量,而不僅僅是承包商是否展現出努力和誠意。因此,即使供應商仍在履行大部分合約義務,服務申訴和合約不續約的風險也在不斷增加。在英國設施管理市場,擁有完善的培訓項目、學徒制和卓越排班系統的公司正在拉大與那些仍然依賴有限外部勞動力的公司之間的差距。

細分市場分析

在英國綜合設施管理市場中,硬設施管理(硬體維修)是成長最快的服務領域,預計2026年至2031年將以5.38%的複合年成長率成長。這一成長與資料中心、生命科學設施、英國國家醫療服務體系(NHS)設施以及老舊建築日益成長的技術需求密切相關,這些設施面臨著更嚴格的安全和合規要求。建築結構工程、暖通空調維護、高壓電氣管理和消防安全合規性都對技能和文件提出了更高的要求,這不僅增加了服務的複雜性,也提升了認證團隊的價值。併購趨勢也呈現類似的趨勢,2021年至2024年間,英國設施管理(FM)產業中與能源服務相關的交易成長了67%,而消防系統和電梯服務在2025年約佔設施管理交易的三分之一。管道和硬體服務承包商的基數仍然龐大,相關市場規模預計將在2024年超過270億英鎊(343億美元),並在2029年達到325億英鎊(413億美元)。

到2025年,軟性設施管理(Soft FM)將佔英國綜合設施管理(IFM)市場規模的55.41%,這表明持續的現場服務仍然是英國IFM市場的主要基礎。混合型工作模式改變了這些服務的形式,而非降低了其需求。清潔服務現在按入住率計費,安保服務擴大與CCTV監控和門禁系統相結合,餐飲服務也在重新設計,以適應中心輻射式辦公模式。 2024年11月,英國國家醫療服務體系(NHS)共享業務服務推出了包括布草洗滌、場地管理和保全在內的服務,總價值達3.75億英鎊(4.763億美元)。這凸顯了公共部門需求的強勁和規模之大。公共部門的採購方也在提高准入門檻,透過審計、健康與安全以及感染控制方面的要求,使擁有成熟管理體系和公共部門良好業績記錄的供應商更具優勢。在綜合設施管理產業,這意味著軟性設施管理將成為規模化的基礎,而硬體維修將成為技術成長的引擎,而非替代品。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 英國公司將非核心業務職能外包

- 符合英國淨零排放指令下的能源效率要求

- 資料中心的發展正在推動對專業設施管理的需求。

- 公共部門基於績效的綜合設施管理合約的興起

- 引入用於預測性設施管理的智慧建築物聯網平台

- 中型設施管理公司私募股權併購活動增加

- 市場限制因素

- 機電工程服務領域熟練技術人員短缺

- 通貨膨脹導致成本上升,給家庭設施管理 (FM) 企業的利潤率帶來了壓力。

- 互聯建築系統中的網路安全風險

- 英國脫歐後勞動力流動受限

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 硬設施管理

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全

- 其他硬設施管理服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟性設施管理服務

- 硬設施管理

- 最終用戶

- 商業

- 飯店業

- 機構和公共基礎設施

- 衛生保健

- 工業和流程部門

- 其他最終用戶

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mitie Group plc

- ISS Facility Services Ltd.

- Sodexo Limited

- CBRE Group, Inc.

- Compass Group PLC

- Equans UK and Ireland

- Integral UK Ltd.

- Atalian Servest Group Ltd.

- VINCI Facilities

- Kier Group plc

- G4S Limited

- OCS Group Limited

- Bouygues Energies and Services UK

- Serco Group plc

- EMCOR UK

- Bellrock Property and Facilities Management Ltd.

- Skanska UK Plc

- Aramark UK Ltd.

- JLL Integrated Facilities Management UK

- Sodexo Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom integrated facility management market size was valued at USD 15.79 billion in 2025 and is estimated to grow from USD 16.45 billion in 2026 to reach USD 20.78 billion by 2031, at a CAGR of 4.78% during the forecast period 2026-203.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, and More). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Integrated Facility Management Market Trends and Insights

Data Centre Expansion is Creating a New FM Demand Category

The 2024 reclassification of UK data centers as critical national infrastructure changed the service expectations around uptime, resilience, and physical security. January 2025 AI Opportunities Action Plan reinforced that direction by linking digital capacity expansion to new technical facilities and supporting infrastructure. For the United Kingdom integrated facility management market, this means demand is shifting toward round-the-clock M&E maintenance, cooling oversight, high-voltage electrical management, fire suppression controls, and specialist cleaning for sensitive environments. A February 2026 AECOM assessment warned that specialist mechanical, electrical, and public health subcontractor demand was already outstripping supply in London, which shows how quickly critical-environment demand is tightening labor capacity. CBRE's December 2024 appointment across Kao Data's UK portfolio showed that occupiers increasingly want one provider that can manage both hard and soft services across these sites. This leaves the UK integrated facility management market with a clear divide between scaled providers that already have critical-environment capability and generalists that still need to build it.

Smart Building IoT and CAFM Platforms are Raising the Productivity Baseline

The United Kingdom integrated facility management (IFM) market is moving away from a reactive work-order model as IoT sensors, BMS platforms, and CAFM systems become more closely connected across occupied estates. ESOS and SECR continue to support that shift because both frameworks increase the need for regular energy monitoring, documentation, and asset-level visibility. An IES digital twin deployment at Queen Margaret University in Edinburgh, which began in August 2025, identified annual energy savings of GBP 64,000 (USD 81,280), or 11% of the building's energy spend through low-capital scheduling and control changes. Clients are also writing energy and carbon KPIs into service agreements more often, which turns sustainability reporting into a contract performance issue rather than a separate ESG ambition. Late 2025 survey evidence showed that many FM leaders still had a large share of compliance tasks untracked or unautomated, which raises the risk of poor reporting, missed actions, and weak renewal discussions. In the United Kingdom IFM market, providers that can prove asset performance with live data are gaining a clearer edge in tenders and renewals.

Skills Shortage is More Than a Recruitment Problem

The United Kingdom integrated facility management market faces a structural labor gap rather than a short hiring cycle, because the issue now combines post-COVID attrition, an ageing workforce, and weak new entrant volumes. More than two-thirds of FM leaders said in 2025 that recruiting and retaining staff was difficult, and this fed directly into missed service levels and weaker day-to-day contract control. The technical side of the problem is even sharper, because HVAC, M&E, and fire systems roles need specialist training and multi-year qualification paths before staff can work independently. The commercial effect is severe because clients judge contracts on live service quality, not only on whether the contractor can point to effort or intent. That is why service complaints and non-renewal risk are rising even where providers are still delivering most contracted tasks. In the United Kingdom IFM market, the firms with stronger training pipelines, apprenticeship capacity, and better scheduling systems are pulling away from those that still rely on a thin external labor pool.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Procurement Consolidation is Compressing the Supplier Base

- Public Sector Estate Backlog is Driving Non-Discretionary FM Demand

- Cost Escalation in Hard FM Is Eroding Contract Profitability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard FM is the fastest-growing service type in the United Kingdom integrated facility management market, with a projected 5.38% CAGR over 2026-2031. That growth is tied to higher technical intensity across data centers, life sciences sites, NHS estates, and older buildings that now face firmer safety and compliance requirements. Building fabric work, HVAC servicing, high-voltage electrical management, and fire safety compliance are all becoming more demanding in skill and documentation, which lifts both service complexity and the value of accredited teams. Deal activity points in the same direction, because energy services transactions in UK FM M&A rose by 67% between 2021 and 2024, while fire systems and lift services made up nearly one-third of 2025 FM deals. The plumbing and hard services contractor base also remains large, with an adjacent market valued at more than GBP 27 billion (USD 34.3 billion), in 2024 and projected to reach GBP 32.5 billion (USD 41.3 billion) by 2029.

Soft FM held 55.41% of the United Kingdom integrated facility management market size in 2025, which shows that recurring frontline services still form the volume base of the United Kingdom IFM market. Hybrid working has changed the pattern of those services rather than reduced their needs, because cleaning is now more occupancy-led, security is increasingly layered with CCTV and access control, and catering is being redesigned around hub-and-spoke office use. November 2024 NHS Shared Business Services launch covered linen and laundry, grounds maintenance, and security with a combined value of GBP 375 million (USD 476.3 million), underlining how institutional demand remains steady and large. Public-sector buyers are also raising entry thresholds through audit, health and safety, and infection-control requirements, which gives an advantage to providers with mature management systems and repeat public-sector experience. Within the integrated facility management industry, this leaves Soft FM as the scale anchor and Hard FM as the technical growth engine rather than a substitute.

List of Companies Covered in this Report:

- Mitie Group plc

- ISS Facility Services Ltd.

- Sodexo Limited

- CBRE Group, Inc.

- Compass Group PLC

- Equans UK and Ireland

- Integral UK Ltd.

- Atalian Servest Group Ltd.

- VINCI Facilities

- Kier Group plc

- G4S Limited

- OCS Group Limited

- Bouygues Energies and Services UK

- Serco Group plc

- EMCOR UK

- Bellrock Property and Facilities Management Ltd.

- Skanska UK Plc

- Aramark UK Ltd.

- JLL Integrated Facilities Management UK

- Sodexo Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Outsourcing of Non-Core Activities Among U.K. Corporates

- 4.2.2 Energy-Efficiency Compliance Under U.K. Net-Zero Mandate

- 4.2.3 Growth of Data Centers Driving Specialized FM Demand

- 4.2.4 Rise of Performance-Based IFM Contracts in Public Sector

- 4.2.5 Adoption of Smart Building IoT Platforms for Predictive FM

- 4.2.6 Increased Private Equity Consolidation in Mid-Tier FM Firms

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Tradespeople for MEP Services

- 4.3.2 Inflation-Linked Cost Pressures on Soft FM Margins

- 4.3.3 Cyber-Security Risks in Connected Building Systems

- 4.3.4 Post-Brexit Labor Mobility Constraints

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Segmentation by Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 Segmentation by End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mitie Group plc

- 6.4.2 ISS Facility Services Ltd.

- 6.4.3 Sodexo Limited

- 6.4.4 CBRE Group, Inc.

- 6.4.5 Compass Group PLC

- 6.4.6 Equans UK and Ireland

- 6.4.7 Integral UK Ltd.

- 6.4.8 Atalian Servest Group Ltd.

- 6.4.9 VINCI Facilities

- 6.4.10 Kier Group plc

- 6.4.11 G4S Limited

- 6.4.12 OCS Group Limited

- 6.4.13 Bouygues Energies and Services UK

- 6.4.14 Serco Group plc

- 6.4.15 EMCOR UK

- 6.4.16 Bellrock Property and Facilities Management Ltd.

- 6.4.17 Skanska UK Plc

- 6.4.18 Aramark UK Ltd.

- 6.4.19 JLL Integrated Facilities Management UK

- 6.4.20 Sodexo Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)