|

市場調查報告書

商品編碼

2063968

中東和非洲綜合設施管理:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East And Africa Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

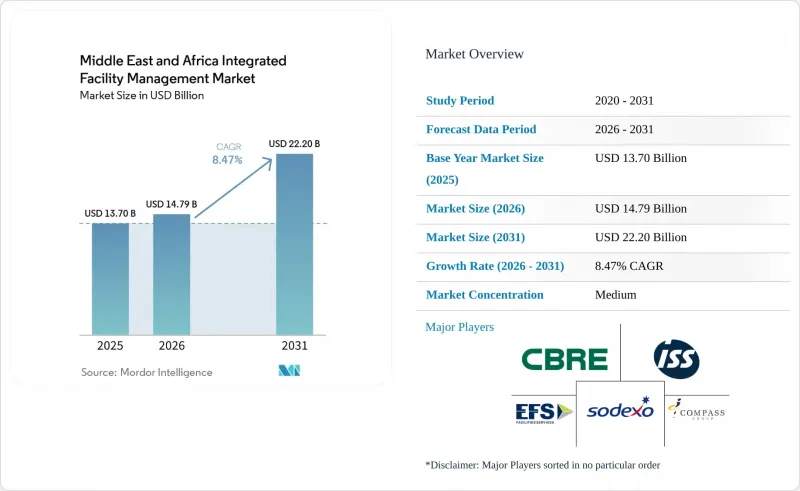

根據 Mordor Intelligence 預測,中東和非洲地區的綜合設施管理市場規模將從 2025 年的 137 億美元和 2026 年的 147.9 億美元成長到 2031 年的 222 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 8.47%。

本報告按服務類型(硬性設施管理[資產管理、機電和暖通空調服務等]、軟性設施管理[辦公室支援和安保、清潔服務、餐飲服務等])、最終用戶(商業、醫療保健等)和地區進行細分。市場預測以價值(美元)表示。

中東和非洲地區整合性機構管理市場的趨勢和見解。

政府願景計畫旨在促進智慧基礎設施建設

沙烏地阿拉伯的「2030願景」和阿拉伯聯合大公國的長期發展框架正在擴大資產基礎,這需要對營運、維護和工作場所服務進行一體化交付。到2025年,沙烏地阿拉伯非石油產業的經濟活動將佔實際GDP的55.6%,這意味著與旅遊、服務、物流和公共基礎設施相關的建築存量正在超越碳氫化合物基礎而擴展。根據同一份年度報告,預計到2025年,遊客數量將達到1.23億人次,旅遊消費將達到810億美元。這將確保酒店、娛樂區、交通設施和公共設施保持全面運作。在中東和非洲綜合設施管理(MEA FM)市場,這種轉變正在推動大規模、更全面的合約的出現,因為新建區域和綜合用途項目需要單一供應商以一體化的方式管理清潔、保全、工程和全生命週期績效。中東和非洲綜合設施管理(MEA FM)市場也正在轉向基於結果的採購模式。這是因為公共部門客戶要求承包商在整個營運週期中保護資產價值、達到服務水準並支援本地化目標。這使得能夠整合技術專長、人員規模和跨多個地點的數位化監控的供應商更具優勢。

商業不動產節能維修增加

隨著業主努力降低能源成本並實現永續發展目標,節能維修正成為中東和非洲綜合設施管理市場的常規服務。國際能源總署 (IEA) 指出,建築能耗佔全球能源消耗的 40%,因此能源效率對業主和公共機構至關重要。 2025 年 10 月發表的一項同行評審研究發現,住宅和商業建築佔阿拉伯聯合大公國國內能源消耗的 39%,顯示維修需求與明確的營運成本密切相關。 2025 年 10 月,Emrill Energy 宣布,其在杜拜和沙迦的工廠實施的人工智慧驅動的冷暖氣空調空調 (HVAC)維修,在 18 個月內實現了 14% 的節能檢驗,所有工廠的平均效率提升了 21%。在中東和非洲的綜合設施管理市場,這些維修計畫不僅能提升設備效能,還能在工程完成後產生長期的監測、維護和檢驗工作。這一趨勢導致合約從一次性工程項目轉向與績效掛鉤的多年營運合約。

供應商生態系統分散阻礙了標準化。

在中東和非洲的綜合設施管理 (CAFM) 市場,許多二線城市仍沿用多層分包結構。這種結構導致跨多個地點的合約在服務品質、人員配備標準和報告方面存在不一致。奈及利亞的商業區和內羅畢不斷擴建的辦公大樓持續湧入大量小規模企業,加劇了價格競爭,使得符合 ISO 標準的供應商難以提供標準化服務。當供應商必須同時應對不同的建築規範、安全法規和認證流程時,跨境營運的複雜性進一步增加。雖然實施 CAFM 系統並應用更嚴格的供應商資格標準的公司可以提高中東和非洲綜合設施管理市場的一致性,但系統整合和員工培訓的成本正在影響其初期盈利能力。因此,試圖在多個非洲市場建立統一服務模式的區域平台的擴張速度正在放緩。

細分市場分析

在中東和非洲的綜合設施管理市場中,硬設施管理(Hard FM)是成長最快的服務領域,預計2026年至2031年的複合年成長率(CAGR)將達到8.53%。這一成長反映了資料中心園區、醫療機構、工業園區以及需要對機電(MEP)、暖通空調(HVAC)和消防系統進行專業管理的大型商業建築的需求不斷成長。 2025年推出的新安全和施工合規要求擴大了主要城市資產(尤其是受技術法規約束的建築物)的預防性維護和檢查活動範圍。資產管理、機電和暖通空調服務仍然是硬體維修服務的最大支柱,因為大型專案的營運模式依賴於長期的預防性維護,而不是被動的故障回應。在中東和非洲的綜合設施管理市場中,資料中心目前在硬體維修需求方面佔據主導地位。這是因為與傳統商業設施相比,資料中心需要更多專業人員、持續監控和更嚴格的環境控制。

2025年,軟性設施管理(Soft FM)在中東和非洲的綜合設施管理市場規模中佔比高達62.33%。這主要得益於飯店、醫療保健和政府機構中清潔、餐飲、辦公室支援和保全等服務的勞力密集特性。對於許多區域性項目而言,這一優勢仍然至關重要,因為大規模公共設施、綜合用途社區和公共建築仍然需要大規模的服務交付。 2025年9月,Farnek在阿拉伯聯合大公國推廣了其混合清潔模式。該公司已部署了30多台機器人清潔設備,並訂購了另外60台,目標是在2026年中期之前達到100多台。這表明,軟性服務在實現自動化的同時,並未犧牲規模。沙烏地阿拉伯的旅遊業也持續推動著度假村、娛樂場所和飯店綜合體對餐飲和支援服務的需求。預計到2025年,沙烏地阿拉伯將接待1.23億遊客,創造810億美元的消費。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 商業不動產節能維修增加

- 加強對遵守建築安全標準的監管要求

- 資料中心的擴張需要專業的設施管理服務。

- 擴大物聯網在預測性維護的應用

- 政府旨在促進智慧基礎設施建設的願景計畫(例如,沙烏地阿拉伯2030願景、阿拉伯聯合大公國2031願景)

- 社會基礎設施維護和管理中公私合營模式的快速成長

- 市場限制因素

- 供應商生態系統分散阻礙了標準化進程。

- 暖通空調和機電工程行業技術純熟勞工短缺

- 原油價格波動導致預算不穩定,給政府設施的營運成本帶來了壓力。

- 互聯建築系統相關的網路安全問題

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 硬設施管理

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全

- 其他硬設施管理服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟性設施管理服務

- 硬設施管理

- 最終用戶

- 商業

- 飯店業

- 公共和機構基礎設施

- 衛生保健

- 工業和流程部門

- 其他終端用戶產業

- 按地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 埃及

- 其他非洲國家

- 中東

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CBRE Group Inc.

- ISS A/S

- Compass Group plc

- Sodexo SA

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield plc

- G4S plc

- Serco Group plc

- EFS Facilities Services Group

- Emrill Services LLC

- Farnek Services LLC

- Imdaad LLC

- Khidmah LLC

- Transguard Group LLC

- Atalian Servest Group Ltd

- Veolia Environnement SA

- Bouygues Energies & Services

- ENGIE Solutions

- Aden Group

- Al Shirawi Facilities Management LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east and Africa integrated facility management market size is projected to expand from USD 13.70 billion in 2025 and USD 14.79 billion in 2026 to USD 22.20 billion by 2031, registering a CAGR of 8.47% between 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), End User (Commercial, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Middle East And Africa Integrated Facility Management Market Trends and Insights

Government Vision Programs Driving Smart Infrastructure

Saudi Arabia's Vision 2030 and the UAE's long-range development frameworks are expanding the asset base that needs bundled operations, maintenance, and workplace services. In 2025, Saudi Arabia's non-oil activities made up 55.6% of real GDP, which shows how the building stock tied to tourism, services, logistics, and public infrastructure is widening beyond the hydrocarbon base.The same annual report stated that tourism reached 123 million arrivals and USD 81 billion in spending in 2025, which keeps hotels, entertainment districts, transport assets, and public venues in continuous operating mode. In the Middle East and Africa integrated facility management market (MEA IFM), that shift supports larger bundled contracts because new districts and mixed-use projects need one provider to manage cleaning, security, engineering, and lifecycle performance together. The Middle East and Africa integrated facility management (MEA FM) market is also moving closer to outcome-based procurement because public clients want contractors to protect asset value, meet service levels, and support localization goals through the full operating cycle. This raises the advantage of providers that can combine technical depth, workforce scale, and digital oversight across multiple sites.

Rise in Energy-Efficiency Retrofits Across Commercial Real Estate

Energy-efficiency retrofits are turning into a recurring service line for the Middle East and Africa integrated facility management market as owners try to cut utility spend and meet sustainability targets. The IEA stated that buildings account for 40% of global energy consumption, which keeps energy performance high on the agenda for property owners and public authorities. A peer-reviewed study published in October 2025 found that residential and commercial buildings represented 39% of the UAE's national energy use, which keeps retrofit demand tied to a clear operating cost base. Emrill Energy stated in October 2025 that AI-driven HVAC retrofits across sites in Dubai and Sharjah delivered 14% verified electricity savings over 18 months, with average site efficiency gains of 21%. In the Middle East and Africa integrated facility management market, these retrofit programs do more than improve equipment, because they create longer monitoring, maintenance, and verification work after the first project is complete. That pattern is moving more contracts away from one-time engineering jobs and toward multi-year operating agreements tied to performance.

Fragmented Vendor Ecosystem Limiting Standardization

The Middle East and Africa integrated facility management market still works through dense subcontractor layers in many African and tier-2 Middle Eastern locations. This structure creates variation in service quality, staffing standards, and reporting discipline across multi-site contracts. Nigeria's commercial corridors and Nairobi's expanding office stock still attract many small operators that compete strongly on price, which makes standardized delivery harder for ISO-aligned providers. Cross-border work becomes more complex when providers must manage different building codes, safety rules, and certification practices at the same time. In the Middle East and Africa integrated facility management market, firms that deploy CAFM systems and stricter vendor qualification rules can improve consistency, but the cost of systems integration and workforce training weighs on early returns. The result is a slower scaling path for regional platforms that want to build uniform service models across several African markets.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Data Centers Demanding Specialized FM Services

- Increasing Adoption Of IoT-Enabled Predictive Maintenance

- Skilled-Labor Shortages in HVAC And MEP Trades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard Facility Management (Hard FM) is the fastest-growing service type in the Middle East and Africa integrated facility management market, with a forecast CAGR of 8.53% from 2026 to 2031. The expansion reflects rising demand from data center campuses, healthcare facilities, industrial sites, and large commercial buildings that need specialist management of MEP, HVAC, and fire systems. New safety and construction compliance requirements in 2025 widened the scope of preventive maintenance and inspection activity across major urban assets, especially in technically regulated buildings. Asset management, MEP, and HVAC services remain the largest hard service anchors because giga-project operating models depend on long-duration preventive work rather than break-fix activity. In the Middle East and Africa integrated facility management market, data centers now sit at the top end of hard FM demand because they require specialist staffing, continuous oversight, and tighter environmental control than conventional commercial properties.

Soft Facility Management (Soft FM) held 62.33% of the Middle East and Africa integrated facility management market size in 2025, supported by the labor intensity of cleaning, catering, office support, and security across hospitality, healthcare, and government assets. That lead remains important because many regional portfolios still need high-headcount service delivery across large public venues, mixed-use communities, and institutional facilities. Farnek expanded its hybrid cleaning model across the UAE in September 2025, with more than 30 robotic cleaners deployed, 60 more on order, and a target of over 100 units by mid-2026, which shows how soft services are being automated without losing scale. Saudi Arabia's tourism activity also keeps catering and support services active across resorts, entertainment assets, and hospitality complexes, with the kingdom reporting 123 million tourist arrivals and USD 81 billion in spending in 2025.

List of Companies Covered in this Report:

- CBRE Group Inc.

- ISS A/S

- Compass Group plc

- Sodexo SA

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield plc

- G4S plc

- Serco Group plc

- EFS Facilities Services Group

- Emrill Services LLC

- Farnek Services LLC

- Imdaad LLC

- Khidmah LLC

- Transguard Group LLC

- Atalian Servest Group Ltd

- Veolia Environnement SA

- Bouygues Energies & Services

- ENGIE Solutions

- Aden Group

- Al Shirawi Facilities Management LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Energy-Efficiency Retrofits Across Commercial Real Estate

- 4.2.2 Growing Regulatory Mandates for Building Safety Compliance

- 4.2.3 Expansion of Data Centers Demanding Specialized FM Services

- 4.2.4 Increasing Adoption of IoT-Enabled Predictive Maintenance

- 4.2.5 Government Vision Programs Driving Smart Infrastructure (e.g., Saudi Vision 2030, UAE Vision 2031)

- 4.2.6 Upsurge in Public-Private Partnership Models for Social Infrastructure Upkeep

- 4.3 Market Restraints

- 4.3.1 Fragmented Vendor Ecosystem Limiting Standardization

- 4.3.2 Skilled-Labor Shortages in HVAC and MEP Trades

- 4.3.3 Volatile Oil-Linked Budgets Curtailing OPEX in Government Facilities

- 4.3.4 Cyber-Security Concerns Around Connected Building Systems

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

- 5.3 By Geography

- 5.3.1 Middle East

- 5.3.1.1 Saudi Arabia

- 5.3.1.2 United Arab Emirates

- 5.3.1.3 Qatar

- 5.3.1.4 Kuwait

- 5.3.1.5 Rest of Middle East

- 5.3.2 Africa

- 5.3.2.1 South Africa

- 5.3.2.2 Nigeria

- 5.3.2.3 Kenya

- 5.3.2.4 Egypt

- 5.3.2.5 Rest of Africa

- 5.3.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group Inc.

- 6.4.2 ISS A/S

- 6.4.3 Compass Group plc

- 6.4.4 Sodexo SA

- 6.4.5 Jones Lang LaSalle Incorporated

- 6.4.6 Cushman & Wakefield plc

- 6.4.7 G4S plc

- 6.4.8 Serco Group plc

- 6.4.9 EFS Facilities Services Group

- 6.4.10 Emrill Services LLC

- 6.4.11 Farnek Services LLC

- 6.4.12 Imdaad LLC

- 6.4.13 Khidmah LLC

- 6.4.14 Transguard Group LLC

- 6.4.15 Atalian Servest Group Ltd

- 6.4.16 Veolia Environnement SA

- 6.4.17 Bouygues Energies & Services

- 6.4.18 ENGIE Solutions

- 6.4.19 Aden Group

- 6.4.20 Al Shirawi Facilities Management LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)