|

市場調查報告書

商品編碼

2063962

南美洲綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

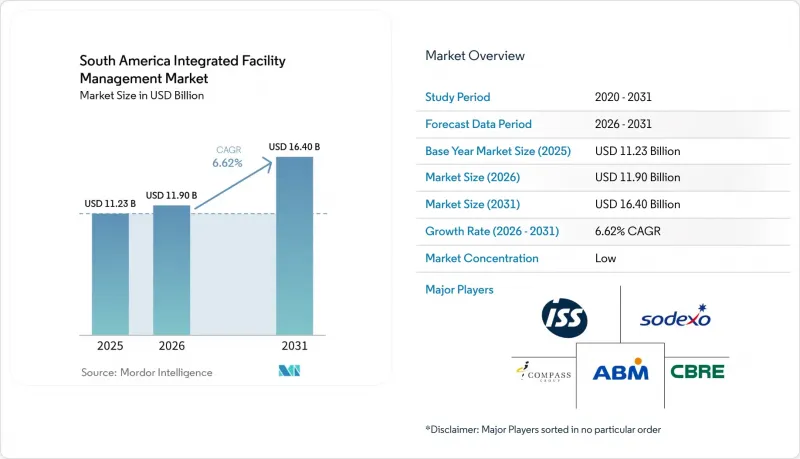

據 Mordor Intelligence 稱,2025 年南美洲綜合設施管理市場價值為 112.3 億美元,預計到 2031 年將達到 164 億美元,而 2026 年為 119 億美元,2026 年至 2031 年預測期內的複合年成長率為 6.62%。

本報告按服務類型(硬性設施管理[資產管理、機電和暖通空調服務等]、軟性設施管理[辦公室支援和安保、清潔服務、餐飲服務等])、最終用戶(商業、醫療保健、工業和流程行業等)以及地區進行細分。市場預測以價值(美元)為單位。

南美洲綜合設施管理市場的趨勢與洞察

擴大智慧建築平台的應用

智慧建築的普及仍然是推動整合式合約短期需求的最大動力。這是因為營運商擴大將入住率、暖通空調、照明和門禁系統與日常服務交付決策聯繫起來,而不是依賴固定的維護計劃。巴西能源績效評估機構(EPE)報告稱,暖通空調和照明在商業和公共建築的電力消耗中佔很大比例,這為業主提供了將建築系統與以性能主導的設施管理(FM)模式整合的明確成本理由。 Aureside 的報告顯示,巴西大量新建商業建築已經採用了一定程度的自動化,這意味著即使不考慮維修需求,平台整合式綜合設施管理(IFM)合約的需求基礎也在不斷成長。更大的機會在於老舊商業地產,在這些地產中,在真正的單一管理層投入實用化之前,需要更換和整合傳統的獨立解決方案。這種積壓需求正在推動南美洲(SA)綜合設施管理市場形成多年合約儲備。此外,巴西的技術標準和能源標籤系統正在促進業主採用更系統化的建築管理方法,從而擴大能夠整合機電系統和數位控制系統的供應商的服務範圍。因此,在南美洲 IFM 市場,已經經營整合儀表板和遠端監控工具的供應商更有優勢將自動化投資轉化為長期、持續的合約。

人們越來越關注節能設施

能源效率不再僅被視為永續發展目標,因為客戶現在已將能耗目標、監控程序和營運處罰直接納入服務合約。國際能源總署 (IEA) 在 2025 年宣布,建築感測器和監控軟體可將商業設施的能耗降低高達 30%。這使得採購團隊能夠利用綜合設施管理 (FM) 合約來證明技術投資的合理性。這項轉變在南美洲意義重大,因為能源績效歷來不在外包設施服務的核心範圍內,尤其是在業主和租戶共同承擔責任的租賃結構中。隨著這些責任轉移到服務合約中,設施管理服務提供者無需擁有資產即可提供可衡量的價值,從而拓展了南美洲綜合設施管理市場的商業案例。 GBC 巴西也指出,ESG 指標和技術標準(例如 ABNT 和 ASHRAE)正逐漸成為日常設施管治的一部分。這推動了對能夠在單一營運架構下管理能源、室內環境和合規性結果的認證供應商的需求。因此,南美洲的綜合設施管理市場正在穩步從以勞動力主導的合約轉向以能源績效為價值提案一部分的合約。

缺乏技術嫻熟的多學科工程師

該地區的勞動力短缺並非僅僅是維修工人的匱乏。真正的短缺在於能夠統籌處理機電系統、數位控制、監控工具以及合規性要求的技術人員。 2026年2月,GBC巴西指出,設施管理人員的角色已從被動營運轉向數據主導的策略管治,並將這一轉變與日常營運中ABNT、ASHRAE和CRI-204標準的日益普及聯繫起來。這種轉變加重了服務提供者的培訓負擔,因為客戶現在期望技術人員不僅能夠進行實體維護,還必須解讀建築資料、協助審計並管理性能系統。在大都會圈區以外的地區,這個問題更為嚴重,因為這些地區的勞動力稀缺,而且多站點合約的招募也需要時間。這減緩了整合模式在次市場的部署,並增加了複雜專案的推出成本,即使市場有需求也是如此。實際上,這種人才短缺為那些能夠將集中式專業知識、遠端支援和現場執行整合到單一交付模式中的供應商帶來了結構性優勢。

細分市場分析

至2025年,軟性設施管理服務(IFM)將佔據南美綜合設施管理市場64.21%的佔有率。這證實了清潔、餐飲、辦公室支援和保全仍然是大多數客戶機構外包的主要切入點。清潔服務比高技術性任務更容易外包,因此仍然是應用最廣泛的服務,尤其受到那些剛開始擺脫內部營運的中小型企業的青睞。因此,軟性設施管理服務在工業園區、商業建築、醫院和教育機構等領域擁有大規模的應用群體,尤其是在外包市場比鄰國更成熟的巴西。該類別的優勢還在於它與設施的日常使用、員工體驗和設施印象直接相關,即使在預算緊張的情況下,合約續約率也保持相對穩定。因此,即使客戶在服務設計方面變得更加挑剔,軟性設施管理服務仍然是支撐南美洲綜合設施管理(IFM)市場規模的基石。

此外,在南美洲的綜合設施管理(IFM)產業中,軟性設施管理(Soft FM)的結構正在發生顯著變化。客戶不僅越來越期望固定的流程,還希望獲得靈活的人員配備、基於使用量的排班以及透過數位化技術實現的服務視覺性。在辦公大樓和綜合用途設施中,由於運轉率每日和區域波動較大,因此按需清潔和與入住率相關的工作場所支援變得越來越重要。餐飲服務也正在經歷類似的變革,索迪斯巴西計畫在2025年將自主微型市場部署範圍擴大到企業、醫院、學校和工廠等場所。這表明,食品相關服務正在轉向更適合混合辦公和長輪班工作的便利模式。保安和辦公室支援也在經歷類似的轉變,客戶尋求在多個地點實現更有效率的管理、報告和適應性。這意味著軟性設施管理很可能仍將是南美洲綜合設施管理市場中最大的服務層級。然而,其成長將擴大受到技術和合約設計的影響,而不僅僅是員工規模。

預計到2031年,硬設施管理將以7.43%的複合年成長率成長,並有望成為南美綜合設施管理市場中成長最快的細分領域,因為客戶正在加大對資產運作、合規性和技術可靠性的投資。醫療機構、資料中心、工業設施和礦業資產的停機時間會對營運和安全造成直接影響,因此,機電(MEP)和冷暖氣空調(HVAC)服務成為市場需求的核心。消防系統和安全合規性在採購中也變得越來越重要,更新後的2025版NFPA 72標準被工程師和尋求跨區域通用標準的跨國租戶視為性能基準。這在南美洲尤其重要,因為許多國際租戶要求當地服務供應商提供與北美和歐洲同等水準的維護服務。因此,結合先進工程技術、合規能力和監控工具的硬體維修提案在競爭性競標中變得越來越重要。

隨著資產管理從預防性維護轉向由軟體和遠端資料支援的長期規劃,硬體維修)的機會正在進一步擴大。西班牙電信(Telefónica)在其聖保羅資料中心部署了人工智慧驅動的數位雙胞胎,以最佳化冷卻系統,預計可降低15-20%的能耗。這體現了技術設施管理正從被動維修轉向持續最佳化。 Leadec也發布了其在美洲地區2025年的強勁業績報告,重點指出其「綠色工廠解決方案」業務(包括能源管理、電池儲能、太陽能和智慧工廠維護等與硬體維修管理需求密切相關的活動)的收入已達到1.4億歐元(1.58億美元)。這些案例表明,南美洲的綜合設施管理產業越來越重視能夠提高可靠性、能源利用率和生命週期效益的技術服務。因此,在南美洲綜合設施管理市場,儘管軟性設施管理(Soft FM)的營收仍佔比較大,但硬體維修管理正展現出最強勁的成長動能。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧建築平台的廣泛應用

- 人們越來越關注節能設施。

- 後疫情時代的混合工作模式需要靈活的整合功能管理 (IFM)。

- 增加私募股權對設施管理服務供應商的投資

- 加速採用數位雙胞胎進行資產最佳化

- 政府主導的基礎設施現代化計劃

- 市場限制因素

- 缺乏技術嫻熟的多學科工程師

- 本地供應商分散的現狀阻礙了標準化。

- 外匯波動推高了服務合約成本。

- 大城市以外地區的終端用戶認知度較低。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 硬設施管理

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全

- 其他硬設施管理服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟性設施管理服務

- 硬設施管理

- 最終用戶

- 商業(銀行、金融服務與保險、IT與通訊、零售與倉儲)

- 餐飲服務業(餐廳、餐廳、大型飯店)

- 公共機構和公共基礎設施(政府、教育、機場、鐵路)

- 醫療保健(公立和私立機構)

- 工業和流程部門(製造業、能源、採礦業)

- 其他終端用戶產業(住宅、娛樂、運動和休閒)

- 按地區

- 巴西

- 阿根廷

- 智利

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Leadec Brasil

- ISS A/S

- Sodexo SA

- Compass Group PLC

- Grupo Eulen SA

- GDI Integrated Facility Services Inc.

- CBRE Group Inc.

- Jones Lang LaSalle Incorporated(JLL)

- Cushman & Wakefield PLC

- Aramark Corporation

- Apleona GmbH

- OCS Group Ltd.

- Mitie Group PLC

- Manserv Facilities

- Grupo Verzani & Sandrini S/A

- Brasanitas Servicos Integrados

- Allonda Ambiental SA

- Grupo GPS Participacoes e Empreendimentos SA

- Quifel Holdings SA(Ecotrade)

- Engie SA(IFM Division)

- Veolia Environnement SA(FM Division)

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america integrated facility management market size was valued at USD 11.23 billion in 2025 and estimated to grow from USD 11.90 billion in 2026 to reach USD 16.40 billion by 2031, at a CAGR of 6.62% during the forecast period 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), End User (Commercial, Healthcare, Industrial and Process Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America Integrated Facility Management Market Trends and Insights

Increasing Adoption Of Smart-Building Platforms

Smart-building adoption remains the strongest near-term demand trigger for integrated contracts because operators are increasingly connecting occupancy, HVAC, lighting, and access systems to daily service delivery decisions rather than relying on fixed maintenance calendars. Brazil's EPE reported that HVAC and lighting represented a significant portion of electricity consumption in commercial and public buildings, which gives owners a clear cost reason to connect building systems with performance-led FM models. Aureside also reported that a substantial number of new commercial constructions in Brazil already include some level of automation, which means the installed base available for platform-linked IFM contracts is expanding even before retrofit demand is considered. The larger opportunity still sits in older commercial stock, where legacy point solutions need replacement or integration before a true single management layer becomes practical, and that backlog supports a multi-year contract pipeline for the SA integrated facility management market. Technical standards and energy-labeling programs in Brazil are also pushing owners toward more structured building management approaches, which broadens the service scope for providers that can manage MEP systems and digital controls together. Providers that already operate with integrated dashboards and remote visibility tools are therefore in a better position to convert automation spending into long-term recurring contracts across the South America IFM market.

Growing Emphasis On Energy-Efficient Facilities

Energy efficiency is no longer being treated only as a sustainability objective, because clients are now placing consumption targets, monitoring routines, and operating penalties directly into service agreements. The IEA stated in 2025 that building sensors and monitoring software can reduce commercial energy consumption by up to 30%, which gives procurement teams a concrete basis for using integrated FM contracts to justify technology spending. That change matters in South America because energy performance had often remained outside the core scope of outsourced facility services, especially in lease structures where owners and occupiers split responsibility. As those responsibilities move into the service contract, FM providers can add measurable value without owning the asset itself, and that is expanding the commercial case for the South America integrated facility management market. GBC Brasil also noted that ESG metrics and technical standards such as ABNT and ASHRAE are becoming part of day-to-day facilities governance, which raises the need for credentialed vendors that can manage energy, indoor environment, and compliance outcomes in one operating structure. The result is a steadier shift from labor-led contracts toward contracts where energy performance becomes part of the value proposition in the South America integrated facility management market.

Shortage Of Skilled Multidisciplinary Technicians

The regional labor constraint is not simply a shortage of maintenance workers, because the real gap lies in technicians who can handle MEP systems, digital controls, monitoring tools, and compliance requirements in the same role. GBC Brasil stated in February 2026 that the facility manager role had shifted from reactive operations toward data-led strategic governance, and it linked that change to rising use of ABNT, ASHRAE, and CRI-204 standards in daily practice. That shift increases the training burden for providers because clients now expect technical staff to interpret building data, support audits, and manage performance systems rather than only execute physical maintenance tasks. The problem is more acute outside the largest urban centers, where the available labor pool is smaller and recruitment for multi-site contracts takes longer. This slows the rollout of integrated models in secondary markets and raises the cost of ramping complex accounts even when demand is present. In practice, the talent gap gives a structural advantage to vendors that can combine centralized expertise, remote support, and field execution in one delivery model.

Other drivers and restraints analyzed in the detailed report include:

- Post-Pandemic Hybrid Work Models Demanding Flexible IFM

- Rising Private-Equity Investments in FM Service Vendors

- Fragmented Local Vendor Landscape Limiting Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft Facility Management services held 64.21% of the South America integrated facility management market share in 2025, which confirms that cleaning, catering, office support, and security remained the main outsourcing entry points for most client organizations. Cleaning services continue to form the broadest adoption base because they are easier to contract out than highly technical functions, especially for small and medium-sized firms taking their first step away from in-house operations. That gives soft FM a large installed base across industrial parks, commercial buildings, hospitals, and education sites, particularly in Brazil where outsourcing has matured further than in many neighboring countries. The category also benefits from its direct link to day-to-day occupancy, employee experience, and site presentation, which keeps renewal rates relatively resilient even when budgets tighten. For that reason, soft FM still anchors the operating scale of the South America integrated facility management market even as clients become more selective about service design.

The soft facility management mix is also changing in ways that matter for the South America IFM industry, because clients increasingly expect flexible staffing, usage-based scheduling, and digitally supported service visibility rather than fixed routines alone. Demand-led cleaning and attendance-linked workplace support are becoming more relevant in offices and mixed-use sites where occupancy changes materially by day and by zone. Catering is evolving as well, with Sodexo Brazil expanding autonomous micromarket formats across corporate, hospital, school, and factory environments in 2025, which shows how food-related services are moving toward convenience-led models that fit hybrid work and extended shift operations. Security and office support are following a similar path, where clients want better control, reporting, and adaptability across multiple locations. This means soft FM is likely to remain the largest service layer in the South America integrated facility management market, even though its growth profile is increasingly shaped by technology and contract design rather than labor scale alone.

Hard Facility Management is projected to expand at a CAGR of 7.43% through 2031, making it the fastest-growing part of the SA integrated facility management market size as clients spend more on asset uptime, compliance, and technical reliability. MEP and HVAC services sit at the center of that demand because downtime in healthcare facilities, data centers, industrial sites, and mining assets carries direct operating and safety consequences. Fire systems and safety compliance are also becoming more visible in procurement, and the 2025 edition updates to NFPA 72 are being referenced as a performance benchmark by engineers and multinational occupiers that expect common standards across geographies. That matters in South America because many international tenants want the same maintenance discipline from regional service providers that they require in North America or Europe. As a result, hard FM proposals that combine engineering depth, compliance capability, and monitoring tools are gaining more weight in competitive bids.

The hard FM opportunity is widening further because asset management is moving beyond preventive maintenance into longer-term planning supported by software and remote data. Telefonica is deploying AI-powered digital twins for cooling optimization at its Sao Paulo data centers and estimated potential energy reductions of 15% to 20%, which gives a practical example of how technical FM is moving into continuous optimization rather than reactive repair. Leadec also reported strong performance in the Americas in FY2025 and highlighted Green Factory Solutions revenue of EUR 140 million (USD 158 million) from energy management, battery storage, photovoltaic, and smart factory maintenance activities that align closely with hard FM demand. These examples show that the South America integrated facility management industry is assigning greater value to technical service lines that improve reliability, energy use, and life-cycle outcomes. Hard FM therefore has the strongest forward momentum even though soft FM continues to hold the larger revenue base in the South America integrated facility management market.

List of Companies Covered in this Report:

- Leadec Brasil

- ISS A/S

- Sodexo S.A.

- Compass Group PLC

- Grupo Eulen S.A.

- GDI Integrated Facility Services Inc.

- CBRE Group Inc.

- Jones Lang LaSalle Incorporated (JLL)

- Cushman & Wakefield PLC

- Aramark Corporation

- Apleona GmbH

- OCS Group Ltd.

- Mitie Group PLC

- Manserv Facilities

- Grupo Verzani & Sandrini S/A

- Brasanitas Servicos Integrados

- Allonda Ambiental S.A.

- Grupo GPS Participacoes e Empreendimentos S.A.

- Quifel Holdings S.A. (Ecotrade)

- Engie SA (IFM Division)

- Veolia Environnement S.A. (FM Division)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Smart-Building Platforms

- 4.2.2 Growing Emphasis on Energy-Efficient Facilities

- 4.2.3 Post-Pandemic Hybrid Work Models Demanding Flexible IFM

- 4.2.4 Rising Private-Equity Investments in FM Service Vendors

- 4.2.5 Accelerated Digital Twin Deployments for Asset Optimization

- 4.2.6 Government-Backed Infrastructure Modernization Programs

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Multidisciplinary Technicians

- 4.3.2 Fragmented Local Vendor Landscape Limiting Standardization

- 4.3.3 Currency Volatility Inflating Service Contract Costs

- 4.3.4 Low End-User Awareness Outside Tier-1 Cities

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial (BFSI, IT and telecom, retail and warehouses)

- 5.2.2 Hospitality (eateries, restaurants and large-scale hotels)

- 5.2.3 Institutional and Public Infrastructure (government, education, airports, railways)

- 5.2.4 Healthcare (public and private facilities)

- 5.2.5 Industrial and Process Sector (manufacturing, energy, mining)

- 5.2.6 Other End-User Industries (multi-house residential, entertainment, sports and leisure)

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Leadec Brasil

- 6.4.2 ISS A/S

- 6.4.3 Sodexo S.A.

- 6.4.4 Compass Group PLC

- 6.4.5 Grupo Eulen S.A.

- 6.4.6 GDI Integrated Facility Services Inc.

- 6.4.7 CBRE Group Inc.

- 6.4.8 Jones Lang LaSalle Incorporated (JLL)

- 6.4.9 Cushman & Wakefield PLC

- 6.4.10 Aramark Corporation

- 6.4.11 Apleona GmbH

- 6.4.12 OCS Group Ltd.

- 6.4.13 Mitie Group PLC

- 6.4.14 Manserv Facilities

- 6.4.15 Grupo Verzani & Sandrini S/A

- 6.4.16 Brasanitas Servicos Integrados

- 6.4.17 Allonda Ambiental S.A.

- 6.4.18 Grupo GPS Participacoes e Empreendimentos S.A.

- 6.4.19 Quifel Holdings S.A. (Ecotrade)

- 6.4.20 Engie SA (IFM Division)

- 6.4.21 Veolia Environnement S.A. (FM Division)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)