|

市場調查報告書

商品編碼

2063909

義大利有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Italy Organic Waste Collection Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

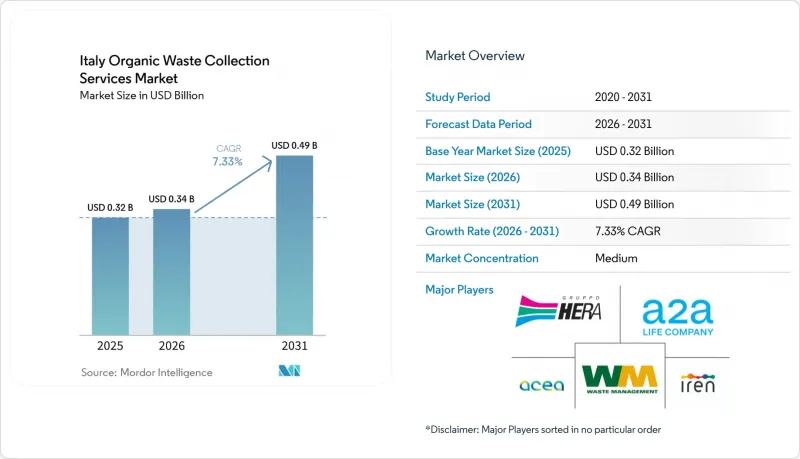

據 Mordor Intelligence 稱,2025 年義大利有機廢棄物收集服務市值為 3.2 億美元,預計到 2031 年將達到 4.9 億美元,而 2026 年為 3.4 億美元,預測期(2026-2031 年)的複合年成長率為 7.33%。

本報告按廢棄物類型(食物廢棄物、園林綠化廢棄物等)、最終用戶(住宅、商業、工業、其他)、收集方式(路邊收集、投放點等)、技術和設備(手動、半自動等)以及地區進行細分。市場預測以價值(美元)和數量(噸)表示。

義大利有機廢棄物收集服務市場的趨勢與洞察

義大利各市鎮對「Raccolta Differenziata」(垃圾分類收集)目標的遵守率很高。

義大利在2024年實現了全國67.7%的垃圾分類率,鞏固了在提高分類系統中有機廢棄物回收率方面取得的進展。Emilia-Romagna和威尼託等地區領先,其表現一直高於全國平均水平,從而提高了可用於堆肥和厭氧消化的有機物的質量和數量。這些成就得益於入戶收集流程的標準化以及包含原料品管的長期綜合服務契約,從而改善了高合規率地區收集運營商的經營環境。在收集密度高、複雜性高的大城市,結合基礎設施、使用者工具和RFID技術,可以提高有機廢棄物容器的可追溯性,同時減少殘留物的比例。分類率高於平均且投資於厭氧消化設施的地區往往擁有更高的生物甲烷工廠位置,從而加強了上游服務設計與下游能源價值之間的連結。因此,義大利有機廢棄物收集服務市場的企業擁有更強大的有機材料基礎,從而支持規模經濟和收入來源多元化,從收集到處理。

義大利北部堆肥基礎建設

義大利北部生物處理設施的運作多於南部,因此人均收集和運輸成本較低。相較之下,由於基礎設施不足和運輸距離長,義大利中部的人均管理成本位居全國最高。義大利南部除了面臨類似的成本壓力外,處理能力也較低。目前的發展進展反映出,生物處理正從獨立的堆肥製程向厭氧消化與好氧穩定化相結合的綜合製程轉變,這種製程在利用相同原料生產堆肥的同時,提高了能源收入。利古里亞Liguria近期產能的擴張清晰地反映了這一趨勢。其中一座生物消化池的處理能力加倍,不僅向國家電網供應生物甲烷,還生產出經認證可用於農業的堆肥。該生物消化池策略性位置靠近農業和工業叢集,可聯合消化各種廢棄物,從而提高沼氣產量,並全年穩定工廠的盈利。由於北部地區在基礎設施密度方面繼續保持主導地位,服務提供者可以圍繞附近的設施規劃收集路線,從而降低單位成本並減輕運輸風險。這一趨勢仍然是義大利有機廢棄物收集服務市場中各市政當局的優先事項。從中長期來看,服務不足的農村地區的新消化和堆肥計畫有望在糾正區域間有機廢棄物流動的平衡和減少長途運輸方面發揮作用。

收集的有機廢棄物流中存在高濃度的污染物

儘管義大利的垃圾分類率已達到67.7%,但廢棄物的純度仍參差不齊,這構成了一項挑戰。產業監測表明,有機垃圾中仍然存在塑膠薄膜、玻璃碎片和金屬,尤其是在居民分類遵守情況因地區而異的大都會圈。這些雜質需要額外的預處理步驟,例如篩選、磁选和光學分選,這增加了每噸垃圾的能源消耗,並降低了企業的淨堆肥產量。人工智慧驅動的監控正成為分類廠和收集路線中切實可行的解決方案。電腦視覺技術可以識別污染的類型和模式,從而實現營運響應並向居民進行有針對性的信息傳播。在大型設施中的應用表明,即時成分分析可以提高紙質纖維的質量,這充分展現了人工智慧和感測器在多種含有有機物的垃圾流中帶來的顯著變化。由行業供應商提供的廢棄物排放攝影機和收集路線分析技術的應用,也提高了企業環境中的垃圾純度,這表明隨著市政當局尋求加強多級定價體系並調整污染物附加費,其應用範圍將進一步擴大。未來,資金籌措的可用性將決定小規模市政當局採用污染物管理技術的速度,進而影響義大利有機廢棄物收集服務市場的成本回收和定價。

細分市場分析

預計到2025年,食物廢棄物將佔垃圾收集業務收益的76.1%。這主要得益於強制對家庭和商業有機垃圾進行分類,以及實施上門收集計畫的城市的高收集率。 2020年第116號政府法令規定的監管義務不斷鞏固有機垃圾在城市固態廢棄物中的重要性,而經認證的可堆肥垃圾袋和公眾宣傳活動則維持了上門收集計劃的參與度。食物廢棄物是最大的垃圾類別,預計在主要垃圾類型中成長最快,到2031年複合年成長率預計為8.21%。這反映了分類義務的持續擴大和生物甲烷獎勵越來越受歡迎,因為它既能最大限度地提高能源產出,又能滿足土壤產品的農業化學品標準,目前這種方法已在重點地區得到廣泛應用。位於開羅蒙特諾特的擴建式生物消化器等設施展示瞭如何將城市固態廢棄物中的有機垃圾和綠色廢棄物轉化為生物甲烷和堆肥,從而創造雙重收入來源,並帶來更穩健的處理經濟效益,進而保障收集合約的穩定性。雖然餐飲服務業會產生大量有機廢棄物,但在旺季期間,每日收集仍然有效,而且收費系統也根據廢棄物產生情況調整成本,從而恰當地反映了這種高廢棄物密度。因此,義大利有機廢棄物收集服務市場以城市廢棄物中的有機垃圾為核心,收集路線、容器設計和污染物管理對原料品質和合約履行有著至關重要的影響。

修剪廢棄物和園林綠化廢棄物是第二大廢棄物來源,其季節性波動較大,對公園和住宅的物流和服務水準構成挑戰。專用堆肥設施對於高木質素含量的物料仍然至關重要,而合作厭氧消化則用於處理在厭氧消化器中碳氮平衡更佳的混合物。從政策角度來看,鼓勵對農產品和工業產品進行合作厭氧消化,以實現原料來源多樣化,並穩定全年能源生產。 《國家生物經濟計畫》明確支持南部地區的厭氧消化,在合約和物流條件允許的情況下,將農場殘餘物納入都市區收集系統的進程可能會加快。隨著新的消化設施確保可靠的供應管道,以及社區合作社加強參與有機物管理,農業殘餘物收集服務的收入預計將會增加。對於執行嚴格納入和排放標準的市政當局而言,諸如市場廢棄物等特殊廢棄物來源提供了選擇性的商業機會,因為高純度分類可以獲得更高的接收費。

2025年,住宅用戶將佔比最高,達68.9%。這反映出義大利有機廢棄物收集服務市場中許多城市普遍採用分類收集方案和路邊收集服務。一項「按需收費」試點計畫證實,家庭用戶對清晰的浮動價格反應良好,從而將一般廢棄物的比例轉向有機物和可回收物。將該項目與RFID標籤垃圾桶和資訊宣傳相結合,可在短短幾週內提高收集率。在多用戶住宅中,通常需要個人化的解決方案,例如具有用戶身份驗證功能的門禁共享容器,以控制處理量並降低污染風險。家庭堆肥是另一種將部分家庭有機廢棄物從收集方案轉移到當地土壤的補充手段,產業監測表明,這將顯著減少市政層面的處理量。在表現優異的地區,隨著專案接近飽和,成長速度正在放緩,重點轉向污染控制和收集路線的效率。總體而言,在義大利整體有機廢棄物收集服務市場中,住宅有機廢棄物仍然是收集量的主要組成部分,支撐著處理預約和生物甲烷生產計畫。

預計商用餐飲服務業的成長速度將超過住宅餐飲業,在預測期內複合年成長率將達到7.86%。這主要得益於定價因素基於廢棄物產生量,以及市政當局擴大了餐廳和餐飲服務商的專用垃圾收集路線。利用無線射頻識別(RFID)和物聯網(IoT)技術測量客戶安裝情況的收費,能夠增強課責,並使可變定價能夠直接反映在現場營運調整中。歐盟資助的試點計畫表明,對商業用戶引入「按量付費」模式可以提高垃圾分類率並減少殘餘廢棄物,從而為針對特定行業的合約提供了商業案例。農產品加工產業的工業排放正擴大融入協同厭氧消化框架,工廠與生產商合作,以確保有機殘餘物的穩定供應。對於營運商而言,這些細分終端用戶市場拓展了義大利有機廢棄物收集服務產業的業務範圍,使其涵蓋更複雜的項目,這些項目需要更嚴格的進度安排和品管,以防止污染。隨著專案的擴展,更完善的數據系統和關於污染費的合約條款的明確規定,將是維持獲利能力的關鍵。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 義大利各市鎮在實現「差異化收集」目標方面取得了很高的成就率

- 義大利北部堆肥基礎建設

- 避免掩埋的目標在於促進有機廢棄物。

- 義大利各市鎮引進計量型垃圾收集(PAYT)

- 歐盟的循環經濟目標正在加速有機廢棄物的商業化。

- 鼓勵生產生物甲烷的獎勵將促進有機廢棄物。

- 市場限制因素

- 收集的有機廢棄物流中存在高濃度的污染物

- 營運成本上升

- 南部地區的加工能力受限

- 地方政府間徵收方式的標準化程度不足。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 用於廢棄物追蹤的RFID智慧垃圾桶

- 人工智慧正在徹底改變廢棄物分類方式。

- 利用物聯網最佳化車輛路線

- 波特五力模型

- 廢棄物收集車輛的現代化和電氣化

- 生物甲烷對有機廢棄物收集的影響分析

第5章 市場規模及成長預測(價值:美元,數量:噸)

- 廢棄物類型

- 食物廢棄物(生產和消費階段)

- 園林綠化廢棄物

- 農業殘餘物

- 其他

- 最終用戶

- 住宅

- 商業(飯店餐飲、零售)

- 工業(食品加工和製造)

- 其他(農業廢棄物)

- 透過收集方法

- 上門收集

- 投放和回收系統

- 其他

- 按下技術/設備

- 人工收集系統

- 半自動系統

- 全自動系統

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Gruppo Hera

- A2A Group

- Gruppo Iren

- Waste Management, Inc.

- Acea Group

- Vivilab

- Veolia Environnement

- REMONDIS SE & Co.

- PreZero Stiftung & Co. KG

- Sogliano Ambiente

- Porcarelli Group

- Contarina SpA

- Gruppo Veritas

- RAP Palermo

- Blue Wings Composting

- Biorepack Consortium

- FCC Environment

- Urbaser

- Indaver

- Valli Gestioni Ambientali

第7章 市場機會與未來展望

According to Mordor Intelligence, the italy organic waste collection services market size was valued at USD 0.32 billion in 2025 and is estimated to grow from USD 0.34 billion in 2026 to reach USD 0.49 billion by 2031, at a CAGR of 7.33% during the forecast period (2026-2031).

This report is Segmented by Waste Type (Food Waste, Yard & Landscape Waste, and More), by End-User (Residential, Commercial, Industrial, and Others), by Collection Method (Door-To-Door, Drop-Off / Bring Systems, and Others), by Technology and Equipment (Manual, Semi-Automated, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Italy Organic Waste Collection Services Market Trends and Insights

High Municipal Compliance with Italy's "Raccolta Differenziata" Targets

Italy reached a 67.7% national separate collection rate in 2024, consolidating progress toward higher diversion of organic streams within differentiated collection systems. Regional leaders such as Emilia-Romagna and Veneto maintained performance levels above the national average, which enhances the quality and quantity of organic feedstock available for composting and anaerobic digestion. These outcomes are reinforced by long-term integrated service contracts that standardize door-to-door protocols and embed feedstock quality controls, which improve the operating environment for collection firms in high-compliance zones. In large cities where collection density and complexity are high, pairing infrastructure with user-facing tools and RFID helps reduce residual fractions while improving traceability of organic bins. Regions that combine higher-than-average separate collection with investment in digestion assets tend to host more biomethane plants, which tightens the link between upstream service design and downstream energy valorization. The cumulative effect is a more resilient base of captured organic material for operators in the Italy organic waste collection services market, which supports scale economics and revenue diversity across collection and treatment.

Expansion of Composting Infrastructure in Northern Italy

Northern regions operate more biological treatment sites than Southern territories, resulting in lower per-capita collection and transfer costs. In contrast, Central Italy records the country's highest per-capita management costs due to infrastructure gaps and longer transport distances, while Southern regions face similar cost pressures alongside lower treatment capacity. The current build-out trajectory reflects a continued shift from standalone composting toward integrated anaerobic digestion with aerobic stabilization, which increases energy revenues while preserving compost outputs from the same feedstock. A recent capacity expansion in Liguria illustrates the direction of travel, with a biodigester doubling its throughput, injecting biomethane into the national grid, and producing certified compost for agriculture. Strategic siting near agro-industrial clusters supports co-digestion of residues, boosting biogas yields and stabilizing plant economics year-round. As the North continues to lead on infrastructure density, service operators can plan collection routes around nearer facilities, which lowers unit costs and mitigates transport risks, a dynamic that remains a priority for municipalities in the Italy organic waste collection services market. Over the medium term, new digestion and composting projects in underserved provinces are positioned to rebalance regional flows of organics and reduce long-haul transfers.

High Contamination Levels in Collected Organic Waste Streams

Despite Italy's 67.7% separate collection rate, variations in purity remain a challenge. Industry monitoring indicates persistent contamination of the organic fraction with plastic films, glass fragments, and metals, particularly in large metropolitan areas where resident compliance varies. These impurities add pre-processing stages such as sieving, magnetic separation, and optical sorting, which raise energy inputs per tonne and reduce net compost yields for operators. AI-enabled monitoring is emerging as a practical response at sorting plants and along collection routes, where computer vision flags contamination types and patterns that can be acted on operationally and through targeted resident communications. Deployments at large facilities demonstrate how real-time compositional analysis improves fiber quality for paper grades, illustrating the step-change AI and sensors can deliver across multiple material streams, including organics. Point-of-disposal cameras and route-level analytics from industry suppliers are also demonstrating higher purity in corporate settings, which signals broader applicability as municipalities aim to scale variable tariffs and contamination fee adjustments. Over time, capital availability will determine the pace of adoption of contamination-control technologies in smaller municipalities, thereby influencing cost recovery and pricing in the Italian organic waste collection service market.

Other drivers and restraints analyzed in the detailed report include:

- Landfill Diversion Targets Driving Organic Waste Segregation

- Pay-As-You-Throw (PAYT) Adoption by Italian Municipalities

- Rising Operational Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Food waste accounted for 76.1% of collection service revenues in 2025, driven by mandated separation of household and commercial organics and strong capture rates in municipalities with door-to-door programs. Regulatory obligations under D.Lgs. 116/2020 continue to anchor the primacy of the organic fraction of municipal solid waste, with certified compostable bags and resident education sustaining participation in curbside programs. As the largest segment, food waste is also projected to grow fastest among major waste types, with an 8.21% CAGR through 2031, reflecting ongoing expansion of separate collection mandates and biomethane incentives that increase captured volumes. Treatment pathways increasingly favor integrated anaerobic digestion followed by downstream composting to maximize energy output while meeting agronomic criteria for soil products, an approach now widespread across leading regions. Plants such as the expanded biodigester at Cairo Montenotte demonstrate how municipal organic fraction of municipal solid waste and green waste are converted into biomethane and compost, creating dual revenue streams and more resilient processing economics that support collection contract stability. Food service establishments generate dense organic loads that benefit from daily collection during peak seasons, and tariff structures recognize their higher waste intensity by aligning costs with waste-generation profiles. The Italy organic waste collection services market is therefore anchored in the organic fraction of municipal solid waste, where routing, bin design, and contamination control have the largest impact on feedstock quality and contract performance.

Green pruning and landscape waste represent the second-largest stream, characterized by seasonal fluctuations that challenge logistics and service levels in parks and residential neighborhoods. Composting-only facilities remain important for high-lignin fractions, with co-digestion reserved for blends that achieve more favorable carbon-nitrogen balances in anaerobic digestion tanks. Policies encourage the co-digestion of agro-industrial by-products to diversify feedstock sources and stabilize energy output profiles throughout the year. National bioeconomy planning designates support for anaerobic digestion in Southern regions, which may accelerate integration of farm-level residues into municipal collection frameworks where contracts and logistics permit. Collection service revenues for agricultural residues are projected to expand as new digestion sites secure guaranteed feed-in channels and strengthen local cooperatives' participation in organics management. Niche streams such as market waste can command premium gate fees when sorted to high purity, creating selective opportunities for municipalities that enforce robust contamination and set-out standards.

Residential users accounted for the largest share of 68.9% in 2025, reflecting the wide reach of separate collection programs and door-to-door service in many municipalities within the Italy organic waste collection services market. Pay-as-you-throw pilots confirm that households respond to clear variable charges by shifting residual fractions into organics and recyclables, improving capture rates in a matter of weeks when the program is paired with RFID-tagged bins and communications. Multi-family buildings often require tailored solutions, including controlled-access communal containers with user authentication that manage throughput and reduce contamination risks. Domestic composting adds a complementary channel that diverts a portion of household organics from collection programs to local soil benefit, with industry monitoring estimating meaningful tonnage savings at the municipal level. In high-performing provinces, the growth pace moderates as programs approach saturation, which shifts focus to contamination control and route efficiency. Overall, residential organics remain the bedrock of captured volumes that underpin treatment bookings and biomethane production plans across the Italy organic waste collection services market.

Commercial food service is set to grow faster than the residential base, registering a CAGR of 7.86% over the forecast period, as tariff coefficients align costs with waste intensity and as municipalities expand dedicated circuits for restaurants and catering. Programs that meter customer set-ups with RFID and IoT achieve greater accountability, enabling variable tariffs to be translated directly into operating adjustments at the site level. EU-funded demonstrations show that introducing pay-as-you-throw for commercial users can increase separate collection rates and reduce residual waste, validating the business case for segment-specific contracts. Industrial generators in agro-food processing are increasingly integrated into co-digestion frameworks, where plants partner with producers to secure steady streams of organic residues. For operators, these end-user niches expand the Italian organic waste collection service industry footprint into more complex accounts that require tighter scheduling and quality control against contamination. Stronger data systems and clearer contractual clarity on contamination fees are key to protecting margins as programs scale.

List of Companies Covered in this Report:

- Gruppo Hera

- A2A Group

- Gruppo Iren

- Waste Management, Inc.

- Acea Group

- Vivilab

- Veolia Environnement

- REMONDIS SE & Co.

- PreZero Stiftung & Co. KG

- Sogliano Ambiente

- Porcarelli Group

- Contarina S.p.A.

- Gruppo Veritas

- RAP Palermo

- Blue Wings Composting

- Biorepack Consortium

- FCC Environment

- Urbaser

- Indaver

- Valli Gestioni Ambientali

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Municipal Compliance with Italy's "Raccolta Differenziata" Targets

- 4.2.2 Expansion of Composting Infrastructure in Northern Italy

- 4.2.3 Landfill Diversion Targets Driving Organic Waste Segregation

- 4.2.4 Pay-As-You-Throw (PAYT) Adoption by Italian Municipalities

- 4.2.5 EU Circular Economy Targets Accelerating Organic Waste Valorization

- 4.2.6 Biomethane Incentives Boosting Organic Waste Collection

- 4.3 Market Restraints

- 4.3.1 High Contamination Levels in Collected Organic Waste Streams

- 4.3.2 Rising Operational Costs

- 4.3.3 Limited Processing Capacity in Southern Regions

- 4.3.4 Limited Standardization of Collection Practices Across Municipalities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 RFID Smart Bins for Waste Tracking

- 4.6.2 AI Revolutionizes Waste Sorting

- 4.6.3 IoT Optimizing for Fleet Routes

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Fleet Modernization & Electrification in Waste Collection

- 4.9 Analysis of Biomethane Impact on Organic Waste Collection

5 Market Size & Growth Forecasts (Value in USD & Volume in Tons)

- 5.1 By Waste Type

- 5.1.1 Food Waste (Pre and Post Consumer)

- 5.1.2 Yard & Landscape Waste

- 5.1.3 Agricultural Residues

- 5.1.4 Others

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Commercial (HoReCa, Retail)

- 5.2.3 Industrial (Food Processing & Manufacturing)

- 5.2.4 Others (Agri-waste)

- 5.3 By Collection Method

- 5.3.1 Door-to-Door Collection

- 5.3.2 Drop-Off / Bring Systems

- 5.3.3 Others

- 5.4 By Technology & Equipment

- 5.4.1 Manual Collection Systems

- 5.4.2 Semi-Automated Systems

- 5.4.3 Fully Automated Systems

- 5.4.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Gruppo Hera

- 6.4.2 A2A Group

- 6.4.3 Gruppo Iren

- 6.4.4 Waste Management, Inc.

- 6.4.5 Acea Group

- 6.4.6 Vivilab

- 6.4.7 Veolia Environnement

- 6.4.8 REMONDIS SE & Co.

- 6.4.9 PreZero Stiftung & Co. KG

- 6.4.10 Sogliano Ambiente

- 6.4.11 Porcarelli Group

- 6.4.12 Contarina S.p.A.

- 6.4.13 Gruppo Veritas

- 6.4.14 RAP Palermo

- 6.4.15 Blue Wings Composting

- 6.4.16 Biorepack Consortium

- 6.4.17 FCC Environment

- 6.4.18 Urbaser

- 6.4.19 Indaver

- 6.4.20 Valli Gestioni Ambientali

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion

北美有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

北美有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 升級再造食品配料市場:預測至2034年-按配料類型、功能、分銷管道、應用、最終用戶和地區分類的全球分析

升級再造食品配料市場:預測至2034年-按配料類型、功能、分銷管道、應用、最終用戶和地區分類的全球分析 食品廢棄物管理市場:2026-2032年全球市場預測(依處理技術、來源、服務模式、產品/服務、廢棄物類型和應用分類)

食品廢棄物管理市場:2026-2032年全球市場預測(依處理技術、來源、服務模式、產品/服務、廢棄物類型和應用分類) 2026-2030年全球食品廢棄物管理市場德國有機廢棄物收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)美國有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)日本有機廢棄物收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)有機廢棄物收集:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2026-2030年全球食品廢棄物管理市場德國有機廢棄物收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)美國有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)日本有機廢棄物收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)有機廢棄物收集:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球食品回收市場報告

2026年全球食品回收市場報告