|

市場調查報告書

商品編碼

2063844

有機廢棄物收集:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Organic Waste Collection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

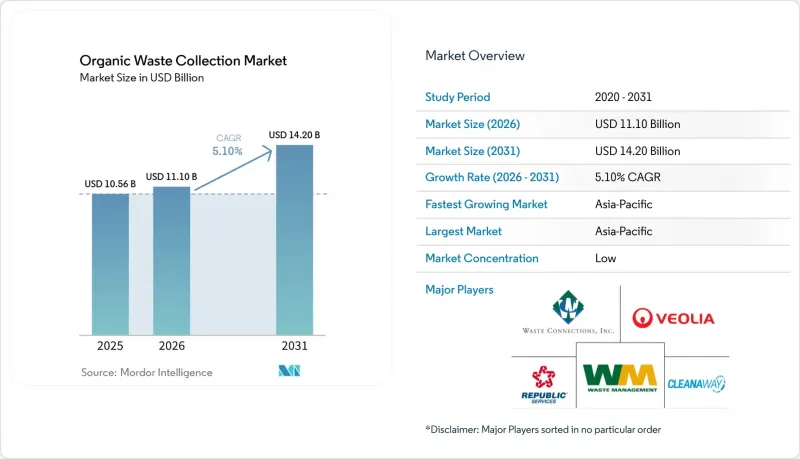

根據 Mordor Intelligence 預測,有機廢棄物收集市場規模將從 2025 年的 105.6 億美元成長到 2026 年的 111 億美元,到 2031 年將達到 142 億美元,2026 年至 2031 年的複合年成長率為 5.10%。

本報告按廢棄物類型(食物廢棄物、園林廢棄物等)、最終用戶(住宅、商業餐飲服務業等)、收集方式(路邊收集、投放點、散裝收集等)、技術(人工、半自動、全自動)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測(價值:十億美元,數量:噸)。

全球有機廢棄物收集市場趨勢與洞察

政府制定了嚴格的法規,強制要求對有機廢棄物進行分類,並避免將其掩埋處理。

監管要求強制規定對廚餘垃圾進行分類收集並減少食物廢棄物,從而避免掩埋。歐盟的《廢棄物框架指令》將於2025年10月16日生效,該指令要求到2030年,加工和製造階段的食物廢棄物減少10%,零售和消費階段的人均食物垃圾減少30%,並要求所有成員國統一收集廚餘垃圾。在美國,於2025年2月制定的《減少食物損失和廢棄物國家戰略》撥款2.75億美元用於有機物回收基礎設施建設,該戰略隸屬於“固態廢棄物回收基礎設施”框架,並輔以教育和宣傳津貼。法國計劃從2026年起要求天然氣供應商取得沼氣生產證書,從而確保對有機廢棄物衍生生物甲烷的需求。荷蘭從2026年起強制在其系統中使用生物甲烷,這將刺激基礎設施投資,並優先使用污染較少的原料。然而,執行情況並不一致。 2022年至2023年間進行的審計顯示,四個歐盟成員國中有三個的有機廢棄物回收率較低,凸顯了加強執法、基礎建設和公民參與的必要性。

都市化進程正在推動城市有機廢棄物產生量的增加。

大都會地區的人口成長使得有機廢棄物流向那些按路線收集模式在營運上可行且資本支出合理的區域,從而擴大了有機廢棄物收集市場的潛在基本客群。聯合國經濟和社會事務部(UN DESA)的報告顯示,到2025年,近一半的人類將居住在都市區,而且自1975年以來,人均城市土地面積一直在增加。這帶來了新的位置挑戰,需要更長的運輸距離、有效率的路線規劃和精心設計的轉運點。預計亞洲特大城市的擴張將增加廢棄物產生量,使得在人口密集的多戶住宅區,全自動側裝式垃圾車、智慧垃圾箱和基於結果的服務合約更具經濟效益。世界銀行一項關於固態廢棄物管理的研究表明,低收入地區的未收集廢棄物率很高,這表明在城市成長速度超過公共預算和收集區域擴張速度的地區,迫切需要擴充性、低成本的有機廢棄物收集模式。隨著都市化過程超過人口成長速度,市政當局需要預見更長的運輸距離和更大的臨時倉儲設施需求。這進一步凸顯了污染控制措施和可預測的調度安排的重要性,以確保堆肥和厭氧消化設施所需原料的品質。因此,城市化快速發展且政策推動力度大的地區最有利於新建或擴大相關項目,從而為有機廢棄物收集市場帶來更大規模、更穩定的項目儲備。

有機廢棄物流受到污染會降低處理效率。

污染會增加預處理要求,降低產品質量,並限制其在終端市場的使用。因此,堆肥和消化殘渣的價值受到限制,如果處理設施拒絕接收這些廢棄物,處置風險也會增加。全國範圍的調查顯示,食物廢棄物和園林廢棄物的污染是一個挑戰,近年來這一趨勢還在加劇。這凸顯了進行有針對性的宣傳活動、制定收集容器標準和建立回饋機制來解決此問題的必要性。美國的實地經驗證實,有針對性的工人干預和貼標籤可以顯著減少收集過程中的污染,從而使下游處理設施受益,並在市政垃圾管理實踐中將集中消化和堆肥納入其中時,支持穩定的運營。處理設施營運商表示,可接受的污染水平是決定是否接收廢物的關鍵因素,而嚴格的源頭分類和明確的服務合約材料標準對於避免代價高昂的退貨和繞路至關重要。聯邦機構指出,塑膠和持久性化學物質仍然是持續存在的障礙,並正在努力整合科學知識並提供技術支援。這將有助於在不同司法管轄區內建立更統一的實務和標準。這些趨勢將使那些結合服務設計、數據驅動的宣傳活動和清晰的客戶回饋的營運商受益,並有望在長期內帶來可衡量的污染減少和更高的附加價值。

細分市場分析

截至2025年,園林綠化廢棄物將佔有機廢棄物收集市場的52.2%,反映出戶外綠色垃圾流的污染程度相對較低,這些垃圾透過長期實施的季節性項目和完善的市政收集路線進行收集。隨著歐盟成員國和英國更多地方政府逐步完善並擴大食物廢棄物分類要求,預計到2031年,食物廢棄物(包括生產前和消費後來源)將以5.78%的複合年成長率成長。這將增加透過專用收集路線和收集日處理的易腐垃圾的比例。在印度,將於2026年生效的法規強制要求將垃圾源頭分為四類,並將廚餘垃圾作為城市規劃中的一個特定類別,隨著法規的逐步落實,食物廢棄物的收集量也將逐步增加。農業殘餘物在區域範圍內為畜牧業和種植業生產系統創造了巨大的商機。目前正在進行的專案旨在透過在受控環境下,結合畜禽糞便和作物殘餘物,並在穩定的原料供應合約下生產沼氣和堆肥級產品。生物污泥和污水有機物繼續作為水資源回收設施中公共消化的整合點,並且在工廠設計和許可條件允許的範圍內,收集的食物廢棄物也可以進行處理以提高沼氣產量。

隨著城市範圍內住宅垃圾處理項目的擴展以及強制性商業有機垃圾處理(該處理規定了餐飲企業的收集服務要求和報告頻率),食物廢棄物的增加將有助於保持成長勢頭,儘管在許多地區,花園廢棄物仍然是最大的廢棄物來源。為了應對不斷成長的食物廢棄物量,需要建造專門的消化設施和長期堆肥場。這將有利於那些已預先協商收集地點或持有本地處理能力股份以穩定處置費用風險的收集商和市政當局。非食品相關的商業有機廢棄物雖然數量不多,但價值很高。這是因為這類垃圾通常是同質的單一來源垃圾,易於處理,並且可以簽訂穩定的契約,從而提高收集路線密度和車輛運轉率。隨著法規的生效和執法力度的加強,有機廢棄物收集產業將優先考慮能夠減少污染並提高下游產品處理能力和價值的服務等級、容器標準和包裝控制措施。

到2025年,住宅垃圾將佔總垃圾收集量的54.1%。這反映出市政當局擴大採用上門收集系統和垃圾桶收集方案,這些方案統一了全部區域的垃圾收集標準,並透過簡單的規則和顏色清晰的垃圾桶鼓勵居民定期參與。商業餐飲服務業是成長最快的終端用戶群,預計2031年將達到6.23%的複合年成長率。這是因為餐廳、餐廳食堂和飯店等場所透過將大量廢棄物集中到更少的收集點,並透過員工培訓和帳戶回饋來改善垃圾處理流程,從而降低了每噸垃圾的服務成本。在那些對大型廢棄物產生者進行界定並強制要求現場處理或檢驗的異地分流的地區,合規主導的需求將會出現,從而確保餐飲服務業和機構環境中的大型垃圾產生者獲得定期服務、記錄處理量並進行污染物監測。有機廢棄物收集市場將受益於這些法規,因為它們創造了穩定的需求和可衡量的績效。這證明了對能夠隨著時間推移提高收益和數據品質的航線以及員工培訓進行投資的合理性。

食品加工和製造業會產生大量同質廢棄物。這些廢棄物易於分類和收集,如果從源頭控制污染,就能確保穩定的共消化產量和持續的堆肥原料供應。零售和食品雜貨網路正在建立正式的合作夥伴關係,以實現廢棄物的再分配、用作動物飼料和堆肥,從而減少食物廢棄物,同時將非食品材料轉移到依賴可靠收集和可預測收集時間表的再利用途徑。學校和其他公共機構正在利用專案津貼來減少食物廢棄物,這些撥款可以支付收集容器、培訓和初始收集服務的費用,從而將試點計畫過渡到具有可衡量成果的永久性計畫。隨著各行業的報告要求日益嚴格,有機廢棄物收集行業將透過結合上門收集或投放點收集、數位化檢驗、污染警報和基礎分析(這些分析將培訓與更高的廢棄物再利用率聯繫起來),為最終用戶創造價值。

區域分析

預計到2025年,亞太地區將佔全球有機廢棄物收集市場規模的33.2%,並將成為成長最快的地區,到2031年複合年成長率將達到7.54%。這主要得益於亞太地區大規模、排放源強制分類以及國家層級的生物甲烷摻混義務,這些都正式規定了有機廢棄物的收集路線。中國和印度的政策發展正在加強收集項目與下游氣體市場之間的聯繫,並推動對厭氧消化設施的投資,因為城市正在擴大路邊和商業收集的覆蓋範圍,以匹配設施的處理能力。日本企業在減少食物廢棄物方面取得的進展表明,強制性計量和明確的目標如何能夠推動私人投資、塑造供應商預期,並使能夠提供一致收集服務和準確報告的運營商受益。亞洲各大特大城市的快速發展正在增加收集路線的密度,並推動技術驅動型車輛的普及,這很可能促使全自動車輛和用於收集容器的感測器在預測期內從試點項目走向標準實踐。

在歐洲,成熟的法規和對生物甲烷生產及堆肥能力的積極投資,正向市政當局和私人垃圾收集商發出強烈的訊號,敦促他們擴大垃圾分類收集範圍,減少污染。修訂後的《廢棄物框架指令》設定了減少食物廢棄物和廚餘垃圾收集的目標,這為住宅和商業領域有機垃圾處理項目的發展奠定了基礎,並在地方層面建立了一套與不斷提升的處理能力相匹配的廢棄物系統。產業數據支持生物甲烷工廠的快速建設和長期投資承諾。然而,要實現2030年的目標,仍需加速生產和處理能力的提升,建議繼續提供政策支援和認證機制,以彌補差距。審計結果顯示,各成員國在執行上存在差異,並指出,必須加強執法、提高掩埋費和成本回收機制,才能最大限度地發揮有機廢棄物收集市場的潛力。這些發現表明,有必要擴大收集範圍、進行公眾宣傳活動,並重點投資減少污染,以實現法律目標,並確保向消化器和堆肥設施穩定供應原料。

在北美,各州強力的強制性規定、聯邦津貼支持和自願性框架共同作用,導致各州的計畫成熟度不一,但覆蓋範圍正在擴大。美國聯邦政府透過「固態廢棄物回收基礎設施計畫」提供的資金包括用於有機物回收基礎設施的撥款,這降低了資金門檻,使城市能夠利用更好的設施和處理合約來擴大收集服務。大型城市的實施案例表明,如果人員配備、收集車輛和處理系統協調得當,並且持續開展公眾宣傳活動,大規模運營是可行的,這為未來在所有地區大規模採用上門有機物收集服務奠定了基礎。在加拿大,一些重點省份正透過長期氣體提取合約支持的夥伴關係來提高厭氧消化能力,隨著新設施的投入運作,基於合約的有機物收集服務市場預計將會增強。在中東和非洲,管理不善的比例很高,回收和堆肥工作也十分有限。儘管如此,旨在實現能源供應多元化和減少食物廢棄物的區域策略正在逐步形成,為有針對性的都市區項目鋪平了道路。這些項目將有機廢物的收集和厭氧消化與補貼上網電價和清潔烹飪政策相結合。在南美洲,法律體制旨在將生物甲烷貨幣化並將垃圾掩埋氣和有機廢物納入可再生能源和脫碳法規框架的法律框架正在製定中,從而使擴大市政垃圾收集規模與長期燃料需求保持一致。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府制定了嚴格的法規,強制要求對有機廢棄物進行分類,並避免將其掩埋處理。

- 日益增強的環保意識和企業永續發展舉措

- 擴大循環經濟原則和垃圾焚化發電舉措的實施範圍

- 由於都市化進程的推進,都市區產生的有機廢棄物量不斷增加。

- 有機廢棄物管理計劃的經濟獎勵和補貼

- 擴大堆肥基礎設施和沼氣生產設施

- 市場限制因素

- 回收基礎設施和加工設施所需的初始資本投資相對較高。

- 公眾意識薄弱,垃圾分類計畫參與率低。

- 由於摻入有機廢棄物,處理效率降低。

- 遍遠地區缺乏經濟有效的收集和運輸解決方案

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 利用人工智慧進行路線最佳化的投資報酬率

- 利用物聯網感測器進行貨櫃監控

- 利用區塊鏈技術進行廢棄物追蹤和積分結算

- 行動應用普及對客戶維繫的影響

- 波特五力模型

- 人工智慧驅動的廢棄物收集對服務供應商收入成長的影響

- 消費者意識向零浪費生活方式的轉變正在影響對服務的需求。

第5章 市場規模與成長預測

- 廢棄物類型

- 食物廢棄物(生產和消費階段)

- 園林綠化廢棄物

- 農業殘餘物

- 生物污泥和污水有機物

- 商業有機物(非食品)

- 其他

- 最終用戶

- 住宅

- 商用食品服務業

- 食品加工/製造

- 零售和雜貨

- 其他

- 透過收集方法

- 上門收集

- 集中收集

- 大量收集

- 地下收藏

- 其他

- 按下技術/設備

- 人工收集系統

- 半自動系統

- 全自動系統

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Republic Services

- Veolia

- Waste Management(WM)

- Waste Connections

- Cleanaway

- Sanimax

- Shapiro(Skip Shapiro Enterprises)

- Biotic Waste Limited

- Compost Crew

- Circular Services

- Emterra USA

- Keenan Recycling(Biffa Company)

- Grundon

- GAP Organics

- Monster Organics

- Recology

- Royal Waste Services

- Total Organics Recycling

- Groot Industries

- Denali

第7章 市場機會與未來展望

According to Mordor Intelligence, the organic waste collection market size is expected to grow from USD 10.56 billion in 2025 to USD 11.10 billion in 2026 and is forecast to reach USD 14.20 billion by 2031 at 5.10% CAGR over 2026-2031.

This report is Segmented by Waste Type (Food Waste, Yard Waste, and More), End-User (Residential, Commercial Food Service, and More), Collection Method (Door-To-Door, Drop-Off, Bulk, and Others), Technology (Manual, Semi-Automated, Fully Automated), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts in Value USD Billion and Volume (Tons)

Global Organic Waste Collection Market Trends and Insights

Stringent Government Regulations Mandating Organic Waste Segregation and Diversion from Landfills

Regulatory mandates are driving organics diversion by requiring separate biowaste collection and food waste reduction. The European Union's Waste Framework Directive, effective October 16, 2025, mandates a 10% reduction in food waste during processing and manufacturing and a 30% per capita reduction at retail and consumption by 2030, alongside consistent biowaste collection across Member States. In the United States, the February 2025 National Strategy for Reducing Food Loss and Waste allocates USD 275 million for organics recycling infrastructure under the Solid Waste Infrastructure for Recycling framework, supported by education and outreach grants. France will require gas suppliers to source biogas production certificates from 2026, ensuring demand for biomethane from organic waste. The Netherlands' 2026 biomethane grid-blending obligation will drive infrastructure investment, favoring low-contamination feedstock. However, uneven implementation persists, as an audit found low biowaste collection rates in three of four European Union Member States in 2022-2023, highlighting the need for enforcement, infrastructure, and public engagement.

Rising Urbanization Driving Higher Volumes of Municipal Organic Waste Generation

Population growth in large cities is concentrating organic waste streams in areas where route-based collection is operationally feasible, and capital spending can be justified, thereby expanding the addressable base for the organic waste collection market. UN DESA reports that cities housed nearly half of humanity in 2025, and that urban land area per person has expanded since 1975, which increases haul distances and creates new siting challenges that favor efficient routing and well-planned transfer points. The expected expansion of megacities across Asia increases waste generation, strengthening the economics of fully automated side-loading vehicles, smart containers, and performance-based service contracts in dense multi-user districts. The World Bank's work on solid waste management documents high levels of uncollected waste in lower-income settings, suggesting that the need for scalable, lower-cost organics collection models is most acute where city growth outpaces public budgets and collection coverage. As built-up areas expand faster than population, municipalities must plan for longer transport legs and more intermediate storage, which increases the value of contamination control and predictable scheduling to maintain feedstock quality for composting and digestion facilities. Regions with rapid urban growth and policy momentum, therefore, present the strongest conditions for new or expanded programs, which leads to a larger and more stable pipeline for the organic waste collection market.

Contamination of Organic Waste Streams Reducing Processing Efficiency

Contamination increases preprocessing requirements, reduces product quality, and constrains end-market applications, thereby limiting the value captured from compost and digestate and increasing disposal risk if facilities reject loads. Evidence from national studies shows that food and garden waste streams face contamination challenges that have trended upward in recent years, underscoring the need for targeted outreach, bin standards, and feedback loops to address behaviors. Local experience in the United States confirms that targeted crew intervention and tagging can significantly reduce curb contamination, benefit downstream facilities, and support steady operations when co-digestion or composting is part of the municipal treatment mix. Processing operators communicate that contamination thresholds drive acceptance decisions, which places a premium on reliable source segregation and clear material standards within service agreements to avoid expensive rejections and re-routing. Federal agencies flag plastics and persistent chemicals as ongoing barriers, and they are working to synthesize science and provide technical assistance, which should support more consistent practices and standards across jurisdictions. These dynamics favor providers that combine service design with data-driven outreach and clear customer feedback, which can produce measurable reductions in contamination and higher-value outputs over time.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Circular Economy Principles and Waste-to-Energy Initiatives

- Growing Environmental Awareness and Corporate Sustainability Commitments

- Lack of Public Awareness and Low Participation Rates in Source Segregation Programs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Yard and Landscape Waste accounted for 52.2% of the organic waste collection market in 2025, reflecting long-standing seasonal programs and the relatively lower contamination inherent to outdoor green waste streams collected through well-understood municipal routes. Food Waste, covering pre-consumer and post-consumer sources, is projected to grow at a 5.78% CAGR through 2031 as separate food waste collection requirements in European Member States and the United Kingdom mature and expand to more local jurisdictions, increasing the share of putrescible material served by dedicated routes and service days. India has mandated four-stream source segregation under rules that take effect in 2026, elevating wet waste to a specific category in city plans and gradually scaling food waste capture as compliance increases. Agricultural Residues create sizable regional opportunities tied to livestock and crop systems, with projects that combine manure and crop wastes to produce biogas and compost-grade outputs under controlled conditions and steady feedstock contracts. Bio-Sludge and Wastewater Organics continue to provide integration points for co-digestion at water resource recovery facilities, which can absorb collected food waste to increase gas yields where plant design and permit conditions allow.

Food Waste growth will be supported by the expansion of citywide residential programs and by commercial organics mandates that define collection service expectations and reporting cadence for food service operators, helping maintain growth momentum even as yard waste remains the largest stream by volume in many jurisdictions. Dedicated digestion assets and long-term composting outlets are needed to handle forecast increases in Food Waste tonnage, which favors haulers and municipalities that pre-negotiate off take or maintain equity in local processing capacity to stabilize tipping fee exposure. Commercial Organics that are not food-related remain small but valuable, since they often consist of homogeneous, single-source streams that are easier to process and can be contracted on stable schedules, thereby improving route density and fleet utilization. As mandates settle and enforcement increases, the organic waste collection industry will likely prioritize service tiers, container standards, and packaging controls that reduce contamination and increase the throughput and value of downstream products.

Residential households accounted for 54.1% of collected volumes in 2025, reflecting the reach of municipal curbside systems and cart-based programs that standardize pickups across neighborhoods and support regular participation through simple rules and clear bin colors. Commercial Food Service is the fastest-growing end-user group, with a 6.23% CAGR through 2031, as restaurants, institutional cafeterias, and hospitality venues consolidate high volumes at fewer pickup points, reducing the per-ton cost of service and supporting cleaner streams through staff training and account-level feedback. Jurisdictions that define bulk waste generators and require onsite processing or verified off site diversion create compliance-driven demand that locks in recurring service days, documented tonnage, and contamination oversight for large generators in food service and institutional settings. The organic waste collection market benefits from these rules because they create regular demand and measurable performance, which justify route investments and staff training that improve yield and data quality over time.

Food Processing and Manufacturing offers high-volume, homogeneous streams that are simpler to segregate and collect, which supports steady co digestion yields and consistent compost inputs when contamination is controlled at the source. Retail and Grocery networks are formalizing partnerships for redistribution, animal feed, and composting, which reduce edible waste while moving inedible materials into diversion channels that depend on reliable collection and predictable pickup windows. Schools and other public institutions are accessing dedicated grants to reduce food waste, which helps pay for bins, training, and initial collection services that transition pilot efforts into standing programs with measurable outcomes. As reporting expectations tighten across sectors, the organic waste collection industry will create value for end users by combining curbside or dockside pickups with digital verification, contamination alerts, and basic analytics that link training to improved diversion rates.

Geography Analysis

Asia-Pacific accounted for 33.2% of the organic waste collection market size in 2025 and is projected to be the fastest growing region at a 7.54% CAGR through 2031, driven by large population centers, mandatory source segregation rules, and national biomethane blending obligations that formalize offtake pathways for collected organics. Policy signals in China and India are strengthening alignment between collection programs and downstream gas markets, encouraging investment in digestion assets as cities build curbside or commercial pickup coverage in step with facility capacity. Japan's progress on food waste reduction in the business sector illustrates how mandatory measurement and clear targets can guide private investment and shape supplier expectations, benefiting service providers that can deliver consistent hauling with accurate reporting. Rapid growth in megacities across Asia supports route density and favors technology-enabled fleets, which raises the likelihood that fully automated vehicles and bin sensors will move from pilots to baseline practice over the forecast period.

Europe combines mature regulation with active investment in biomethane production and composting capacity, which provides strong signals for municipalities and private haulers to expand separate collection coverage and reduce contamination. The revised Waste Framework Directive establishes food waste reduction targets and separate biowaste collection, which anchors growth in residential and commercial organics programs and positions the region to absorb collected streams in line with capacity additions. Sector data confirm a rapid buildout of biomethane plants and long-term investment commitments. However, production and capacity additions need to accelerate to meet 2030 targets, suggesting that continued policy support and certificate systems will help bridge the gap. Audits show uneven implementation across some Member States, suggesting that enforcement, landfill pricing, and cost-recovery mechanisms need to be strengthened to unlock the full potential of the organic waste collection market. These findings support focused investments in collection coverage, communications, and contamination reduction to meet legal targets and stabilize feedstock flows to digesters and compost sites.

North America mixes strong state-level mandates with federal grant support and voluntary frameworks, which yield a patchwork of program maturity across states and provinces that is moving toward broader coverage. U.S. federal funding through the Solid Waste Infrastructure for Recycling program includes allocations for organics recycling infrastructure, which reduces capital hurdles and enables cities to scale collection services with better equipment and processing contracts. Large city rollouts demonstrate operational feasibility at scale when staffing, trucks, and processing are aligned and when resident education is steady, which supports the broader case for universal curbside coverage for organics over time. Canada is adding digestion capacity in key provinces through partnerships backed by long-term gas off take, which should strengthen the market for contracted organics collection services as new sites come online. The Middle East and Africa face higher rates of mismanagement and limited recycling and composting. Still, regional strategies to diversify energy supply and reduce food waste are taking shape, opening the door to targeted projects in urban centers that can combine organic collection with digestion under supportive feed-in tariffs and clean cooking policies. South America is advancing legal frameworks that monetize biomethane and bring landfill gas and organics to market under renewable and decarbonization rules, which aligns municipal collection expansions with long-term fuel demand.

- Republic Services

- Veolia

- Waste Management (WM)

- Waste Connections

- Cleanaway

- Sanimax

- Shapiro (Skip Shapiro Enterprises)

- Biotic Waste Limited

- Compost Crew

- Circular Services

- Emterra USA

- Keenan Recycling (Biffa Company)

- Grundon

- GAP Organics

- Monster Organics

- Recology

- Royal Waste Services

- Total Organics Recycling

- Groot Industries

- Denali

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent government regulations mandating organic waste segregation and diversion from landfills

- 4.2.2 Growing environmental awareness and corporate sustainability commitments

- 4.2.3 Increasing adoption of circular economy principles and waste-to-energy initiatives

- 4.2.4 Rising urbanization driving higher volumes of municipal organic waste generation

- 4.2.5 Economic incentives and subsidies for organic waste management programs

- 4.2.6 Expansion of composting infrastructure and biogas production facilities

- 4.3 Market Restraints

- 4.3.1 High initial capital investment for collection infrastructure and processing facilities

- 4.3.2 Lack of public awareness and low participation rates in source segregation programs

- 4.3.3 Contamination of organic waste streams reducing processing efficiency

- 4.3.4 Limited availability of cost-effective collection and transportation solutions in rural areas

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 AI-powered route optimization ROI

- 4.6.2 IoT sensor-based bin monitoring

- 4.6.3 Blockchain for waste tracking & credits

- 4.6.4 Mobile app adoption & customer retention impact

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of Artificial Intelligence-Powered Waste Collection on Service Providers' Revenue Growth

- 4.9 Consumer behavior shifts toward zero-waste lifestyles influencing service demand

5 Market Size & Growth Forecasts

- 5.1 By Waste Type

- 5.1.1 Food Waste (Pre and Post Consumer)

- 5.1.2 Yard & Landscape Waste

- 5.1.3 Agricultural Residues

- 5.1.4 Bio-Sludge & Wastewater Organics

- 5.1.5 Commercial Organics (Non-Food)

- 5.1.6 Others

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Commercial Food Service

- 5.2.3 Food Processing & Manufacturing

- 5.2.4 Retail & Grocery

- 5.2.5 Others

- 5.3 By Collection Method

- 5.3.1 Door-to-Door Collection

- 5.3.2 Centralized Drop-Off Collection

- 5.3.3 Bulk Collection

- 5.3.4 Underground Collection

- 5.3.5 Others

- 5.4 By Technology & Equipment

- 5.4.1 Manual Collection Systems

- 5.4.2 Semi-Automated Systems

- 5.4.3 Fully Automated Systems

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Republic Services

- 6.4.2 Veolia

- 6.4.3 Waste Management (WM)

- 6.4.4 Waste Connections

- 6.4.5 Cleanaway

- 6.4.6 Sanimax

- 6.4.7 Shapiro (Skip Shapiro Enterprises)

- 6.4.8 Biotic Waste Limited

- 6.4.9 Compost Crew

- 6.4.10 Circular Services

- 6.4.11 Emterra USA

- 6.4.12 Keenan Recycling (Biffa Company)

- 6.4.13 Grundon

- 6.4.14 GAP Organics

- 6.4.15 Monster Organics

- 6.4.16 Recology

- 6.4.17 Royal Waste Services

- 6.4.18 Total Organics Recycling

- 6.4.19 Groot Industries

- 6.4.20 Denali

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion

北美有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

北美有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 升級再造食品配料市場:預測至2034年-按配料類型、功能、分銷管道、應用、最終用戶和地區分類的全球分析

升級再造食品配料市場:預測至2034年-按配料類型、功能、分銷管道、應用、最終用戶和地區分類的全球分析 食品廢棄物管理市場:2026-2032年全球市場預測(依處理技術、來源、服務模式、產品/服務、廢棄物類型和應用分類)

食品廢棄物管理市場:2026-2032年全球市場預測(依處理技術、來源、服務模式、產品/服務、廢棄物類型和應用分類) 2026-2030年全球食品廢棄物管理市場德國有機廢棄物收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)美國有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)義大利有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)日本有機廢棄物收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

2026-2030年全球食品廢棄物管理市場德國有機廢棄物收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)美國有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)義大利有機廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)日本有機廢棄物收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026年全球食品回收市場報告

2026年全球食品回收市場報告