|

市場調查報告書

商品編碼

2063899

美國海運貨運代理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)United States Sea Freight Forwarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

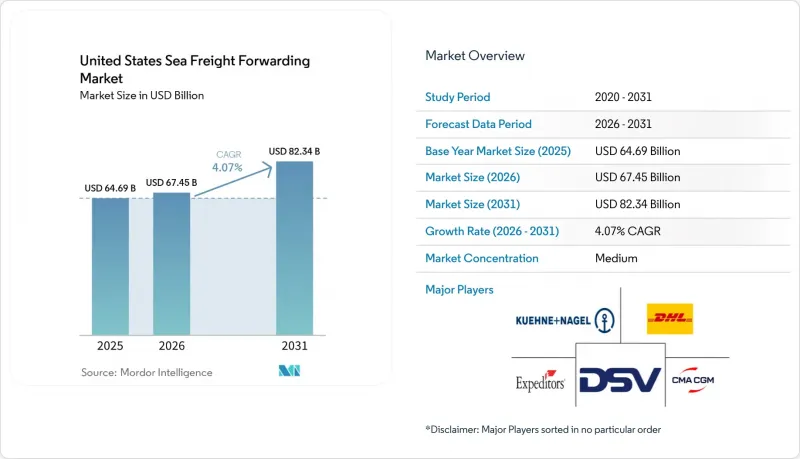

根據 Mordor Intelligence 預測,美國海運貨運代理市場規模將從 2025 年的 646.9 億美元和 2026 年的 674.5 億美元成長到 2031 年的 823.4 億美元,2026 年至 2031 年的複合年成長率為 4.07%。

這一成長得益於亞洲進口需求的持續成長、港口自動化程度的逐步提高以及對靈活運輸方式日益成長的需求。本報告按服務類型(整箱、拼箱)、貨物類型(乾貨/雜貨、冷藏貨)、終端用戶行業(電子及半導體、化工及石化、食品飲料、醫藥及醫療、其他)和地區(東北、東南、中西部、西南部、西部)進行細分。市場預測以美元計價。

美國海運貨運代理市場趨勢與洞察

美國從亞洲的進口增加

來自亞洲的貨櫃進口仍然是美國海運貨運代理市場的重要收入來源。目前,貨物主要集中在半導體、醫療設備和電動車零件領域,這些產業由於重視交貨時間的可靠性,願意支付更高的運費。貨運代理商將業務從傳統的洛杉磯-長灘地區擴展到薩凡納、休士頓和紐約,從而降低了客戶的擁塞風險。即使某些沿海地區因勞動力或天氣問題而中斷,採用多門戶策略也有助於維持市場佔有率。

港口基礎設施改善和自動化項目

自動化起重機和24小時閘口營運正在縮短貨物停留時間,並提高碼頭處理能力。薩凡納港花園城區域的維修以及洛杉磯400號碼頭的機器人裝卸系統,顯著提升了進入許可權優先泊位的貨運代理商的處理速度。 《基礎建設投資與就業法案》撥款170億美元用於水路現代化改造,雖然行動迅速的公司能夠更快地從中受益,但依賴老舊設施的競爭對手則面臨著卡車週轉時間延長的挑戰。

港口擁擠和勞動力短缺

2024年的罷工以及隨後61.5%的薪資上漲,將增加的成本轉嫁給了所有途經東海岸和墨西哥灣沿岸港口的貨櫃。到2025年底,洛杉磯和長灘的平均卡車停留時間穩定在三天或更短,這有助於貨運代理商管理日常帳單。雖然港口多元化有助於降低未來的風險,但也增加了複雜性並削弱了規模經濟。托運人正在密切關注擁塞指標,並重視那些能夠在出現瓶頸時迅速安排替代路線的合作夥伴。

細分市場分析

預計到2025年,美國海運貨運代理市場中,整箱貨運(FCL)服務將佔總收入的73.11%。在需求可預測且托運人能夠以40英尺貨櫃裝載電子產品、機械或汽車零件的地區,整箱貨運佔據主導地位。拼箱貨運(LCL)服務雖然規模較小,但正以6.79%的複合年成長率快速成長,這反映了零售業向更頻繁、小規模的補貨模式轉變的趨勢。

熟悉拼箱(LCL)運輸的貨運代理會將來自多個托運人的訂單合併,從而降低單位成本並賺取高額手續費。倉庫管理系統(WMS)與運輸管理系統(TMS)整合,實現裝載計劃自動化並減少錯誤。成功的供應商還會整合清關和國內卡車運輸,為經銷商提供無縫的門到門解決方案。數位化預訂平台減輕了行政負擔,使員工能夠專注於異常情況的處理。因此,即使貨運量不斷成長,拼箱運輸的利潤率也穩定提高。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 亞洲對美國的進口擴大

- 港口基礎設施開發和自動化項目

- 數位貨運平台的廣泛應用

- 電子商務中大件商品的物流需求

- 離岸風力發電專案貨物運輸(東海岸)的商業機會

- 托運人更傾向於選擇獲得ESG認證的貨運代理

- 市場限制因素

- 港口擁擠及勞資糾紛

- 船用燃料價格波動劇烈

- 國際海事組織更嚴格的環境法規

- 美國缺乏承保高風險貨物海上保險的能力。

- 法律規範

- 價值鍊和通路分析

- 技術創新的前景

- 波特五力模型

- 票價和附加費趨勢分析

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模及成長預測(價值,2026-2031 年)

- 按服務

- 整箱貨(FCL)

- 拼箱貨物(LCL)

- 按貨物類型

- 乾貨/雜貨

- 冷藏

- 按最終用戶行業分類

- 電子和半導體

- 化工/石油化工

- 飲食

- 藥品和醫療保健

- 零售與電子商務

- 其他

- 按地區

- 東北

- 東南

- 中西部

- 西南

- 西方

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- Kuehne+Nagel

- DHL Global Forwarding

- DSV(包括 DB Schenker)

- 達飛集團(包括CEVA物流)

- Expeditors International

- CH Robinson

- Nippon Express

- GEODIS

- AP Moller-Maersk

- Hellmann Worldwide Logistics

- Kintetsu World Express

- BDP國際(現為PSA國際的一部分)

- Savino Del Bene

- Fracht Group

- Crane Worldwide Logistics

- SEKO Logistics

- Flexport

- AIT Worldwide Logistics

- OEC Group

- Dimerco Express Group

- Mallory Alexander International Logistics

- Radiant Logistics

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states sea freight forwarding market size is projected to expand from USD 64.69 billion in 2025 and USD 67.45 billion in 2026 to USD 82.34 billion by 2031, registering a CAGR of 4.07% between 2026 and 2031.

Persistent demand for Asia-origin imports, gradual port automation, and a growing preference for flexible shipping options underpin the expansion. This report is Segmented by Service (Full-Container-Load, Less-Than-Container-Load), by Cargo Type (Dry/General, Reefer), by End-User Industry (Electronics and Semiconductors, Chemicals and Petrochemicals, Food and Beverage, Pharmaceuticals and Healthcare, and More), and by Geography (Northeast, Southeast, Midwest, Southwest, West). Market Forecasts are Provided in Terms of Value (USD).

United States Sea Freight Forwarding Market Trends and Insights

Expansion of US Import Volumes from Asia

Containerized imports from Asia keep the revenue engine running for the United States sea freight forwarding market. Cargo now skews toward semiconductors, medical devices, and electric-vehicle parts that tolerate premium rates for schedule reliability. Forwarders that diversify beyond the traditional Los Angeles-Long Beach complex to Savannah, Houston, and New York relieve congestion risk for customers. A multi-gateway strategy secures market share when labor or weather disrupts any single coast.

Improvements in Port Infrastructure and Automation Projects

Automated cranes and 24-hour gate operations reduce dwell times and lift terminal throughput. The Port of Savannah's Garden City upgrade and Pier 400's robotic handling in Los Angeles give forwarders with preferred slot access measurable velocity gains. The Infrastructure Investment and Jobs Act earmarks USD 17 billion to modernize waterways, but early movers reap benefits sooner, while competitors reliant on legacy facilities face longer truck turn times.

Port Congestion and Labor Disruptions

The 2024 strikes and the subsequent 61.5% wage increase embedded higher costs into every container that moves through East and Gulf Coast docks. Average truck dwell times at Los Angeles and Long Beach stabilized at under three days in late 2025, helping forwarders manage per-diem bills. Diversifying port calls helps mitigate future risk but adds complexity and reduces economies of scale. Shippers watch congestion metrics closely, rewarding partners that reroute quickly when bottlenecks emerge.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Digital Freight Platforms

- E-Commerce Demand for Bulky-Goods Logistics

- Volatile Bunker-Fuel Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full-container-load services accounted for 73.11% of revenue in the United States sea freight forwarding market in 2025. FCL dominates where predictable demand lets shippers fill a 40-foot box with electronics, machinery, or auto parts. Less-than-Container-Load services, while smaller, are climbing at a 6.79% CAGR, reflecting retail's pivot to frequent, smaller replenishment cycles.

Forwarders that master LCL consolidation blend multiple shipper orders, lowering per-unit costs while capturing premium handling fees. Warehouse management systems link with transportation management systems to automate load planning and reduce errors. Successful providers also integrate customs brokerage and domestic trucking, offering a seamless door-to-door proposition for e-commerce sellers. Digital booking portals lower administrative workload, allowing staff to focus on exception management. The result is steady LCL margin expansion even as cargo pieces proliferate.

List of Companies Covered in this Report:

- Kuehne + Nagel

- DHL Global Forwarding

- DSV (incl. DB Schenker)

- CMA CGM Group (Including CEVA Logistics)

- Expeditors International

- C.H. Robinson

- Nippon Express

- GEODIS

- A.P. Moller - Maersk

- Hellmann Worldwide Logistics

- Kintetsu World Express

- BDP International (now part of PSA International)

- Savino Del Bene

- Fracht Group

- Crane Worldwide Logistics

- SEKO Logistics

- Flexport

- AIT Worldwide Logistics

- OEC Group

- Dimerco Express Group

- Mallory Alexander International Logistics

- Radiant Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.1.1 Expansion of US Import Volumes from Asia

- 4.1.2 Improvements in Port Infrastructure and Automation Projects

- 4.1.3 Rising Adoption of Digital Freight Platforms

- 4.1.4 E-Commerce Demand for Bulky Goods Logistics

- 4.1.5 Offshore-Wind Project-Cargo Opportunities (East Coast)

- 4.1.6 Shipper Preference for ESG-Certified Forwarders

- 4.2 Market Restraints

- 4.2.1 Port Congestion and Labor Disruptions

- 4.2.2 Volatile Bunker-Fuel Prices

- 4.2.3 Stricter IMO Environmental Regulations

- 4.2.4 Limited US Marine-Insurance Capacity for High-Risk Cargo

- 4.3 Regulatory Framework

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Technology Innovations Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Rivalry Among Competitors

- 4.7 Freight-Rate and Surcharges Trend Analysis

- 4.8 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Service

- 5.1.1 Full-Container-Load (FCL)

- 5.1.2 Less-than-Container-Load (LCL)

- 5.2 By Cargo Type

- 5.2.1 Dry/General

- 5.2.2 Reefer

- 5.3 By End User Industry

- 5.3.1 Electronics and Semiconductors

- 5.3.2 Chemicals and Petrochemicals

- 5.3.3 Food and Beverage

- 5.3.4 Pharmaceuticals and Healthcare

- 5.3.5 Retail and E-commerce

- 5.3.6 Others

- 5.4 By Region

- 5.4.1 Northeast

- 5.4.2 Southeast

- 5.4.3 Midwest

- 5.4.4 Southwest

- 5.4.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Kuehne + Nagel

- 6.4.2 DHL Global Forwarding

- 6.4.3 DSV (incl. DB Schenker)

- 6.4.4 CMA CGM Group (Including CEVA Logistics)

- 6.4.5 Expeditors International

- 6.4.6 C.H. Robinson

- 6.4.7 Nippon Express

- 6.4.8 GEODIS

- 6.4.9 A.P. Moller - Maersk

- 6.4.10 Hellmann Worldwide Logistics

- 6.4.11 Kintetsu World Express

- 6.4.12 BDP International (now part of PSA International)

- 6.4.13 Savino Del Bene

- 6.4.14 Fracht Group

- 6.4.15 Crane Worldwide Logistics

- 6.4.16 SEKO Logistics

- 6.4.17 Flexport

- 6.4.18 AIT Worldwide Logistics

- 6.4.19 OEC Group

- 6.4.20 Dimerco Express Group

- 6.4.21 Mallory Alexander International Logistics

- 6.4.22 Radiant Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

新加坡海運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中國海運貨運代理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

新加坡海運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中國海運貨運代理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 貨運代理市場規模:按類型、服務、產業和地區分類(2026-2034 年)

貨運代理市場規模:按類型、服務、產業和地區分類(2026-2034 年) 2026年全球海運市場報告2026年全球生鮮產品海運市場報告海運貨運代理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)海運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2026年全球海運市場報告2026年全球生鮮產品海運市場報告海運貨運代理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)海運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 海運市場規模、佔有率及成長分析(依貨物類型、船舶類型、最終用途及地區分類)-2026-2033年產業預測

海運市場規模、佔有率及成長分析(依貨物類型、船舶類型、最終用途及地區分類)-2026-2033年產業預測 全球海運市場

全球海運市場 海運的全球市場:貨物類別,技術整合,各服務形式,各類服務,各地區,機會,預測,2018年~2032年

海運的全球市場:貨物類別,技術整合,各服務形式,各類服務,各地區,機會,預測,2018年~2032年