|

市場調查報告書

商品編碼

2063866

北美人才招聘軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Talent Acquisition Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

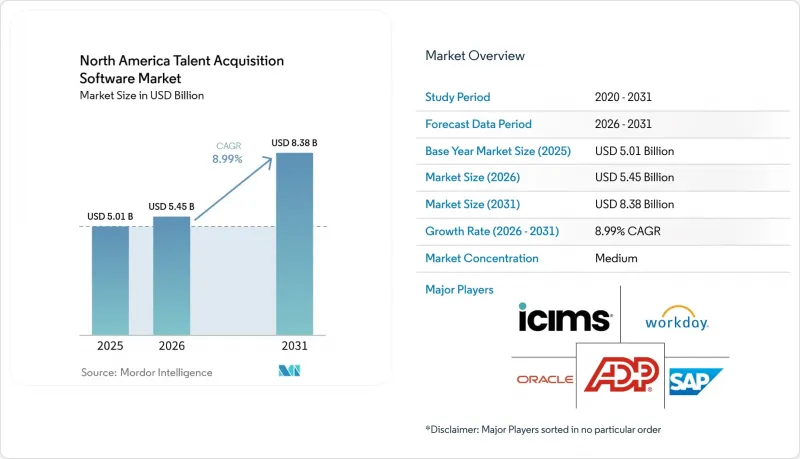

根據 Mordor Intelligence 預測,北美人才招聘軟體市場規模將從 2025 年的 51.1 億美元和 2026 年的 54.5 億美元成長到 2031 年的 83.8 億美元,2026 年至 2031 年的複合年成長率為 8.99%。

本報告按部署模式(雲端、本地部署、混合部署)、應用領域(應徵者追蹤系統、候選人關係管理(CRM)等)、公司規模(大型企業、中小企業)、產業(資訊科技和電信、醫療保健等)以及地區進行細分。市場預測以美元計價。

北美人才招聘軟體市場的趨勢與洞察

人工智慧招募工具的廣泛應用

在北美人才招募軟體市場,人工智慧驅動的篩檢、尋源和配對工具幾乎已成為買家的標準配備。一項調查顯示,78%的高成長型人力資源機構已將人工智慧整合到其ATS(申請者追蹤系統)工作流程中,46%的機構表示人工智慧已將候選人篩檢時間縮短了一半以上。然而,只有10%的機構在其整個工作流程中實施了基於代理的人工智慧,這凸顯了基礎部署與全面整合之間存在的明顯差距。為了彌補這一差距, Oracle於2026年4月在Oracle Fusion Cloud HCM中推出了八款新的人工智慧代理應用程式。另一項調查發現,雖然52%的人力資源主管計劃在2026年部署自主人工智慧代理,但只有22%的人認為他們的組織已準備好管理人機團隊,這推動了北美人才招聘軟體市場對管治和轉型支援的持續投資。

對數據驅動型招募決策的需求日益成長

隨著企業評估招募延遲、人才獲取不足和早期員工留存率低等相關成本,北美人才招募軟體市場正吸引經營團隊的注意。 85%使用人工智慧進行招募的人力資源經理表示,與未使用人工智慧的人力資源經理(70%)相比,他們更容易受到經營團隊的影響。這種轉變推動了對結合工作流程自動化、預測分析和績效追蹤的平台的需求。將候選人屬性與入職後績效關聯起來的供應商正在建立競爭對手難以複製的獨特資料集。這使得數據深度和功能廣度成為北美人才招聘軟體市場中更具競爭力的因素。

資料隱私和合規性的複雜性

隱私和自動化決策的法規正在減緩北美人才招聘軟體市場採購流程的部分環節。加州關於自動化決策技術的法規將於2026年1月1日生效,該法規直接適用於制定或實質影響招募決策的人工智慧系統。如今,買家在批准軟體採購前,要求供應商提供清晰的審計追蹤、透明的資訊揭露、候選人通知和同意管理。在安大略省,隨著《第四項工人權益法案》(Working for Workers Four Act)於2026年1月1日實施,合規要求進一步加強,該法案強制要求披露在招聘過程中使用人工智慧的情況。因此,市場需求並未減弱,北美人才招聘軟體市場顯然更青睞那些能夠證明其「從設計階段就已將合規性融入產品」的供應商。

細分市場分析

預計到2025年,雲端解決方案將佔據北美人才招聘軟體市場68.43%的佔有率,而混合解決方案預計到2031年將以11.21%的複合年成長率成長。這表明,由於市場規模、訂閱定價模式和頻繁的功能更新,雲端產品仍然備受歡迎。雲端平台也支援人工智慧的快速部署,因為它們允許供應商在不改變本地基礎架構的情況下引入新的模型和工作流程工具。 UKG於2026年4月將Google雲端的Gemini Agent Gallery整合到UKG Pro中,進一步強化了這個發展方向。

混合成長仍然至關重要,因為一些雇主仍然需要在本地管理部分資料環境。在政府相關招聘、國防相關營運以及某些銀行、金融和保險 (BFSI) 行業,這種情況尤其突出,因為這些行業採用公共雲端可能受到限制。隨著企業業務遍及美國、加拿大和墨西哥,每個地區的數據處理需求各不相同,北美人才招聘軟體市場對混合部署的需求正在不斷成長。隨著企業將核心招募業務遷移到雲端原生系統,他們會累積難以遷移的歷史招募資料、既定的評分邏輯和技能分類系統。這有助於提高北美人才招聘軟體市場早期平台領導者的客戶維繫率。

截至2025年,應徵者追蹤系統(ATS)佔據了北美人才招募軟體市場31.61%的市場佔有率,但預計到2031年,招聘行銷將以12.42%的複合年成長率成長。 ATS之所以仍是領先系統,是因為它能夠集中管理候選人、工作流程、核准和合規文件。隨著企業在正式發布職缺之前就開始建立未來候選人才庫,客戶關係管理(CRM)工具的重要性日益凸顯。入職、面試管理、評估及相關工具也擴大被整合到招募流程中,而不是作為獨立的人力資源職能部門運作。

招募行銷的成長正在加速,因為雇主越來越將候選人獲取視為與客戶獲取類似的過程。隨著人工智慧生成的申請的興起,企業需要更強力的品牌訊息來吸引符合職位和企業文化的優秀人才。 2025年3月,Employ Inc.收購了Pillar,並報告試點用戶招募週期縮短了26%,這一轉變進一步鞏固了招募行銷的趨勢。未來,隨著能夠追蹤從求職網站訪問到最終接受錄用通知整個流程的供應商獲得獨特的數據優勢,招聘行銷將在北美人才招聘軟體市場中扮演更加重要的戰略角色。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人工智慧招募工具的廣泛應用。

- 對數據驅動型招募決策的需求日益成長

- 一個靈活的人員配置平台,以滿足零工經濟日益成長的需求。

- 遠距和混合辦公室模式的擴展

- 技能發展計劃旨在促進內部轉移解決方案

- 資金籌措湧入人力資源科技新創企業

- 市場限制因素

- 資料隱私和合規性的複雜性(CCPA、CPRA)

- 與傳統人力資源資訊系統平台整合的挑戰

- 經濟放緩對招聘預算的影響

- 人才招聘軟體供應商市場已經飽和。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 雲

- 現場

- 混合

- 透過使用

- 應徵者追蹤系統(ATS)

- 候選人關係管理(CRM)

- 招募行銷

- 入職

- 面試管理和評估

- 其他人才招聘申請

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 按最終用戶:按公司/行業

- 資訊科技(IT)和通訊

- 銀行、金融服務和保險(BFSI)

- 醫療保健和生命科學

- 工業製造

- 零售與電子商務

- 政府/公共部門

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday Inc.

- SAP SE

- Oracle Corporation

- iCIMS Inc.

- IBM Corporation

- Automatic Data Processing Inc.

- Ceridian HCM Holding Inc.

- SmartRecruiters Inc.

- Greenhouse Software Inc.

- Lever Inc.

- Jobvite Inc.

- Phenom People Inc.

- Cornerstone OnDemand Inc.

- ClearCompany HRM Inc.

- BambooHR LLC

- Zoho Corporation Pvt. Ltd.

- UKG Inc.

- Bullhorn Inc.

- Avature Limited

- Paycor Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america talent acquisition software market size is projected to expand from USD 5.11 billion in 2025 and USD 5.45 billion in 2026 to USD 8.38 billion by 2031, registering a CAGR of 8.99% between 2026 and 2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Application (Applicant Tracking System, Candidate Relationship Management (CRM), and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Information Technology and Telecom, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America Talent Acquisition Software Market Trends and Insights

Increasing Adoption Of AI-Based Recruiting Tools

AI screening, sourcing, and matching tools are now close to baseline expectations for buyers in the North America talent acquisition software market. Research showed that 78% of high-growth staffing firms had embedded AI in ATS workflows, and 46% said AI reduced candidate screening time by half or more. The same findings revealed that only 10% had implemented agentic AI across the full workflow, leaving a clear gap between basic adoption and full orchestration. In April 2026, Oracle introduced eight new AI agent applications within Oracle Fusion Cloud HCM to address that gap. Another survey found that 52% of talent leaders plan to deploy autonomous AI agents in 2026, while only 22% believe their organizations are ready to manage human-AI teams, supporting continued spending on governance and change support in the North America talent acquisition software market.

Rising Demand For Data-Driven Hiring Decisions

The North America talent acquisition software market is gaining board-level attention as employers measure the cost of slow hiring, weak sourcing, and poor early retention. Talent leaders using AI in hiring were more likely to report C-suite influence, at 85% versus 70% for non-AI users. That shift is raising demand for platforms that combine workflow automation with predictive analytics and outcome tracking. Vendors that connect candidate attributes with post-hire performance are building proprietary datasets that are hard to replicate. This is making data depth a stronger competitive factor in the North America talent acquisition software market than feature breadth alone.

Data Privacy And Compliance Complexities

Privacy and automated decision-making rules are slowing parts of the buying cycle in the North America talent acquisition software market. California's automated decision-making technology rules, effective January 1, 2026, apply directly to AI systems that make or substantially inform hiring decisions. Buyers now want clear audit trails, transparency disclosures, candidate notices, and consent controls before approving software purchases. Ontario added a second compliance layer when its Working for Workers Four Act took effect on January 1, 2026, requiring disclosure of AI use in hiring processes. The result is not weaker demand, but a clear preference in the North America talent acquisition software market for vendors that can prove compliance by design.

Other drivers and restraints analyzed in the detailed report include:

- Growing Gig Economy Requiring Agile Staffing Platforms

- Expansion Of Remote And Hybrid Work Models

- Integration Challenges With Legacy HRIS Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud held 68.43% of the North America talent acquisition software market share in 2025, while hybrid is projected to grow at 11.21% CAGR through 2031. This shows the market still favors cloud delivery for scale, subscription pricing, and frequent feature updates. Cloud platforms also support faster AI rollouts because vendors can deploy new models and workflow tools without local infrastructure changes. UKG reinforced that direction in April 2026 by integrating Google Cloud's Gemini Agent Gallery into UKG Pro.

Hybrid growth remains important because some employers still need local control over parts of their data environment. That is especially relevant in government-linked hiring, defense-related work, and selected BFSI use cases where public cloud adoption can remain limited. The North America talent acquisition software market for hybrid deployments is expanding as organizations operate across the United States, Canada, and Mexico and face varying data-handling obligations in each location. Once firms move core recruiting into cloud-native systems, they also accumulate historical hiring data, configured scoring logic, and skills taxonomies that are hard to migrate, which increases retention for early platform leaders in the North America talent acquisition software market.

Applicant tracking systems accounted for 31.61% of the market value in 2025, while recruitment marketing is forecast to expand at a 12.42% CAGR through 2031 in the North America talent acquisition software market. ATS remains the system of record because it manages candidates, workflows, approvals, and compliance documentation in one place. CRM tools are gaining relevance as employers build pools of future candidates before roles formally open. Onboarding, interview management, assessment, and related tools are also moving closer to the recruiting stack instead of operating as separate HR functions.

Recruitment marketing is growing faster because employers now treat candidate attraction more like customer acquisition. As AI-generated applications increase overall volume, stronger brand signals are needed to attract qualified applicants who fit the role and culture. This shift was reinforced in March 2025 when Employ Inc. acquired Pillar and reported a 26% reduction in time-to-fill among pilot users. Over time, vendors that track the link from career site visit to accepted offer can build proprietary data advantages, giving recruitment marketing a more strategic role in the North America talent acquisition software market.

List of Companies Covered in this Report:

- Workday Inc.

- SAP SE

- Oracle Corporation

- iCIMS Inc.

- IBM Corporation

- Automatic Data Processing Inc.

- Ceridian HCM Holding Inc.

- SmartRecruiters Inc.

- Greenhouse Software Inc.

- Lever Inc.

- Jobvite Inc.

- Phenom People Inc.

- Cornerstone OnDemand Inc.

- ClearCompany HRM Inc.

- BambooHR LLC

- Zoho Corporation Pvt. Ltd.

- UKG Inc.

- Bullhorn Inc.

- Avature Limited

- Paycor Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of AI-Based Recruiting Tools

- 4.2.2 Rising Demand for Data-Driven Hiring Decisions

- 4.2.3 Growing Gig Economy Requiring Agile Staffing Platforms

- 4.2.4 Expansion of Remote and Hybrid Work Models

- 4.2.5 Upskilling Initiatives Driving Internal Mobility Solutions

- 4.2.6 VC Funding Surge for HR Tech Startups

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Compliance Complexities (CCPA, CPRA)

- 4.3.2 Integration Challenges with Legacy HRIS Platforms

- 4.3.3 Economic Slowdown Impacting Hiring Budgets

- 4.3.4 Talent Acquisition Software Vendor Saturation

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Application

- 5.2.1 Applicant Tracking System (ATS)

- 5.2.2 Candidate Relationship Management (CRM)

- 5.2.3 Recruitment Marketing

- 5.2.4 Onboarding

- 5.2.5 Interview Management and Assessment

- 5.2.6 Other Talent Acquisition Applications

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End User Enterprise Industry Vertical

- 5.4.1 Information Technology (IT) and Telecom

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Industrial Manufacturing

- 5.4.5 Retail and eCommerce

- 5.4.6 Government and Public Sector

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments, Recent Acquisitions, and SWOT Analysis)

- 6.4.1 Workday Inc.

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 iCIMS Inc.

- 6.4.5 IBM Corporation

- 6.4.6 Automatic Data Processing Inc.

- 6.4.7 Ceridian HCM Holding Inc.

- 6.4.8 SmartRecruiters Inc.

- 6.4.9 Greenhouse Software Inc.

- 6.4.10 Lever Inc.

- 6.4.11 Jobvite Inc.

- 6.4.12 Phenom People Inc.

- 6.4.13 Cornerstone OnDemand Inc.

- 6.4.14 ClearCompany HRM Inc.

- 6.4.15 BambooHR LLC

- 6.4.16 Zoho Corporation Pvt. Ltd.

- 6.4.17 UKG Inc.

- 6.4.18 Bullhorn Inc.

- 6.4.19 Avature Limited

- 6.4.20 Paycor Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

IT永續發展人才與培訓平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區人才招聘軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健產業人才招聘:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)銀行、金融服務和保險 (BFSI) 市場的人才招聘:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)

IT永續發展人才與培訓平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區人才招聘軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健產業人才招聘:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)銀行、金融服務和保險 (BFSI) 市場的人才招聘:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031) 數位人才招募市場:按組件、最終用戶、部署類型、產業和應用程式分類-2026-2032年全球市場預測

數位人才招募市場:按組件、最終用戶、部署類型、產業和應用程式分類-2026-2032年全球市場預測 人才招募技術與服務市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶與功能分類IT人員配備:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)

人才招募技術與服務市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶與功能分類IT人員配備:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年) 醫療保健人員增補市場 - 2026-2031 年預測

醫療保健人員增補市場 - 2026-2031 年預測 人才招募軟體市場規模、佔有率和成長分析(按部署類型、組織規模、垂直產業、功能、定價模式和地區分類)-2026-2033年產業預測全球人力增強服務市場(按人員配備類型、僱用模式、合約期限、服務供應商、產業和公司規模):預測(2025-2030 年)

人才招募軟體市場規模、佔有率和成長分析(按部署類型、組織規模、垂直產業、功能、定價模式和地區分類)-2026-2033年產業預測全球人力增強服務市場(按人員配備類型、僱用模式、合約期限、服務供應商、產業和公司規模):預測(2025-2030 年)