|

市場調查報告書

商品編碼

2063857

醫療保健產業人才招聘:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Talent Acquisition In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

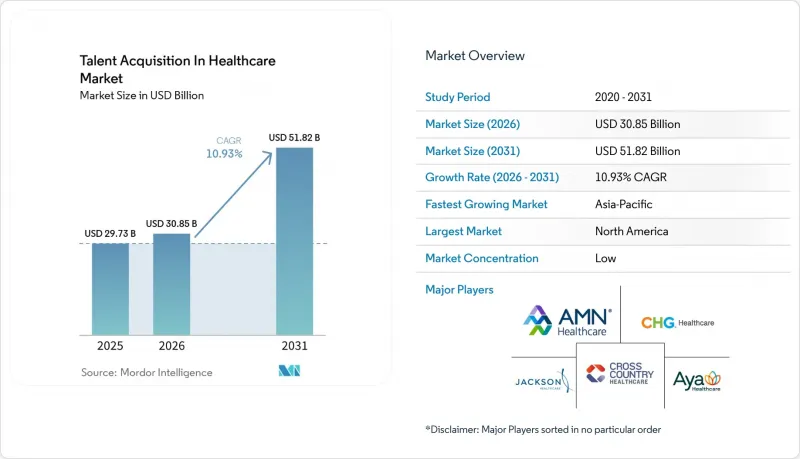

據 Mordor Intelligence 稱,2025 年醫療保健人才招聘市場價值 297.3 億美元,預計在預測期(2026-2031 年)內將以 10.93% 的複合年成長率成長,從 2026 年的 308.5 億美元成長到 2031 年的 518.2 億美元。

本報告按技術(應徵者追蹤系統、候選人關係管理平台等)、服務類型(永久性招聘服務、託管服務供應商等)、最終用戶(醫院和醫療保健系統等)、模式(內部招聘等)和地區進行細分。市場預測以美元計價。

全球醫療保健人才招聘市場的趨勢與洞察

醫療保健相關行業的人員短缺問題日益嚴重。

醫療保健相關領域職缺短缺迫使醫院向臨時工支付高薪,這給醫院的營運利潤率帶來壓力,並促使醫院加大招聘投入。美國醫院協會 (AHA) 在 2025 年的報告中指出,94% 的醫院高層認為人才招募是他們面臨的最大營運挑戰,並指出呼吸治療師和放射技師的年離職率超過 30%。 2020 年至 2024 年間,醫療保健相關培訓計畫的入學人數下降了 8%,而同期門診診斷的需求卻激增了 17%。儘管醫療系統正在推出實習生培訓項目,但這些項目需要 3 到 5 年才能培養出合格的專業人員,導致人才嚴重短缺。人力資源公司正利用這一缺口,提供按日計酬的臨時職位。由於臨床醫生為了尋求更高的薪水而湧向都市區,農村醫療機構受到的衝擊最大,迫使小規模的醫院依賴臨時工,而臨時工的成本比正式員工高出 40% 至 60%。因此,在醫療領域的人才招聘市場中,如何在填補眼前的人才缺口和長期的人才發展之間取得平衡,變得至關重要。

加速醫院人力資源職能的數位轉型

醫院人力資源部門的數位轉型正從後勤部門自動化向策略性人才需求預測演進。費城兒童醫院在2024年實施了一套人工智慧驅動的應徵者追蹤系統後,將護理招募時間從62天縮短至38天,預計每年可節省420萬美元的成本。最新的平台現已與電子健康記錄整合,能夠在頂尖臨床醫生進入就業市場之前就將其識別出來,從而將每次招聘成本降低30%至40%。 Propelus等認證供應商正在將入職培訓時間從45天縮短至15天,使醫院能夠在季節性需求高峰期快速擴充員工。美國國家品質保證委員會(NCQA)將於2025年強制要求每月進行處罰監控,這將推動醫療機構實現合規自動化。這些突破性的進步正在強化一種數據驅動型文化,並重新定義醫療保健領域的人才招聘市場。

候選人資料極易受到網路安全漏洞的攻擊。

招聘平台儲存著諸如社會安全號碼、執照記錄和醫療事故記錄等敏感訊息,使其成為勒索軟體的主要攻擊目標。 2024年2月,Change Healthcare遭受的網路攻擊導致超過1億人的個人資訊洩露,恢復成本估計高達23億美元。根據《健康保險互通性與課責法案》(HIPAA),安全措施不足可能導致每次違規最高150萬美元的罰款。如今,醫院要求供應商獲得SOC 2 II型認證並進行年度穿透測試,這增加了合規成本,尤其對於小規模的醫療機構。這些網路風險正在抑制對醫療保健人才招聘市場的投資。

細分市場分析

到2025年,應徵者追蹤系統將佔總支出的38.28%,並繼續成為大多數醫院的核心系統。然而,隨著買家優先考慮能夠與薪資核算、排班和電子健康記錄整合的平台,該領域的成長正在放緩。人工智慧驅動的人才招募和候選人關係管理解決方案正以每年12.19%的速度成長,重新定義人才招聘市場在技術層面的發展。已實施這些工具的醫院報告稱,招聘時間縮短了20-30%,並且「失聯」率也有所下降,這得益於能夠透過自動提醒與候選人互動的機器學習引擎。

隨著醫院尋求能夠在單一工作流程中完成犯罪記錄核查、執照驗證和身份驗證的整合解決方案,傳統的背景調查軟體在人才招聘市場的佔有率正在下降。視訊面試仍然是遠端醫療招聘的常用方式,但激烈的價格競爭正在推動行業整合。那些利用預測分析技術脫穎而出的供應商,例如根據區域基準數據推薦具有競爭力的薪資範圍,正在獲得更多支持,尤其是在每年招聘數千名臨床醫生的大規模醫療系統中。

到2025年,永久性員工將佔收入的41.43%,反映出對常駐臨床醫生的持續需求。然而,隨著醫師職業倦怠的加劇,臨時執業服務正以11.43%的複合年成長率成長,如今已成為遠距醫療機構至關重要的安全閥。這種成長正在影響醫療人才招聘市場,因為短期合約支付的薪資高於通貨膨脹率。

管理服務提供者 (MSP) 和招募流程外包 (RPO) 透過打包式人員配備、合規性監控和供應商整合,持續擴大市場佔有率。使用 MSP 的醫院報告稱,由於將計費管理和資格追蹤整合到單一控制面板中,其管理成本降低了 15-20%。同時,醫療保健專業人員的臨時人員配備範圍正從呼吸治療擴展到診斷影像和臨床實驗室工作等專業領域,從而拓寬了醫療保健人才招聘市場的範圍。

區域分析

預計到2025年,北美將佔全球收入的37.21%,這主要受美國多州執業許可製度的複雜性、臨床醫生薪資上漲以及維持高收費率的支付方結構等因素驅動。儘管護理師執業互認協議(Nurse Licensure Compact)已在41個州擴展,促進了護理人員的流動,但加州和紐約州仍保留各自的流程,延長了招募過程。預計2025年,加拿大將接收4,200名海外醫學院畢業生,比2023年成長18%,進而加強其區域醫療保健體系。墨西哥邊境地區私人醫院的激增吸引了雙語醫療團隊,並將跨境人才招聘資金注入醫療保健人才市場。

預計到2031年,亞太地區的複合年成長率將達到10.94%,成為成長最快的地區。到2025年,印度將出現14萬名護理師的過剩,這推動了向海灣合作理事會國家和澳洲的海外派遣管道擴大。波灣合作理事會的「2030願景」醫院建設計畫以及阿拉伯聯合大公國專科診所數量的增加,進一步刺激了全部區域的需求。日本正面臨人口老化問題,預計2025年,其65歲以上人口將佔總人口的28.7%。這促使日本加大對機器人技術和任務共享的投資,以應對護理人員短缺問題。儘管中國的私立醫院產業正以每年12%的速度成長,但省級執業許可製度和戶籍限制阻礙了全國性人才輸送平台的建立,限制了區域醫療人才獲取的規模經濟效益。

儘管歐盟的《人員自由流動指令》理論上簡化了資格互認流程,但德國、法國和義大利的語言和技能測試仍然是瓶頸。德國計劃在2025年聘用12,400名外國護士,主要來自菲律賓和印度,以緩解人口壓力。英國國家醫療服務體系(NHS)計劃在2025年透過聘用外國護理師填補35%的護理職缺。然而,來自海灣國家更高的薪資競爭正在削弱其吸引力。雖然南美洲市場的滲透率仍然較低,但巴西和阿根廷私立醫院連鎖機構引入的系統化供應商管理表明,醫療保健人才招聘市場未來存在成長機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速醫院人力資源職能的數位轉型

- 醫療保健相關行業的人員短缺問題日益嚴重。

- 向靈活的零工製臨床人員編制模式過渡

- 監管機構對資質驗證自動化施加了越來越大的壓力。

- 引進人工智慧驅動的招募方式,縮短招募時間。

- 遠端醫療的擴張正在推動全球人才庫的發展。

- 市場限制因素

- 候選人資料極易受到網路安全漏洞的攻擊。

- 美國各州和歐盟國家的許可法規有差異

- 工會主導的對演算法選擇工具的抵制

- 地方預算限制和安全網設施

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過技術

- 應徵者追蹤系統(ATS)

- 候選人關係管理平台

- 人工智慧驅動的招募工具

- 影片其他平台

- 背景調查軟體

- 其他技術

- 按服務類型

- 全職員工安置服務

- 人員配備服務

- 招募流程外包(RPO)

- 託管服務提供者 (MSP)

- 臨時工聘用人員編制

- 其他服務類型

- 最終用戶

- 醫院和醫療系統

- 門診手術中心

- 護理機構及長期照護機構

- 家庭醫療保健服務提供者

- 診斷檢查室

- 其他醫療保健提供者

- 按模式

- 內部招聘

- 基於外包的人才招聘

- 混合模式

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AMN Healthcare Services Inc.

- CHG Healthcare Services Inc.

- Cross Country Healthcare Inc.

- Encompass Health Corporation

- MEDNAX Services Inc.

- Jackson Healthcare LLC

- Maxim Healthcare Group

- Aya Healthcare Inc.

- HealthTrust Workforce Solutions LLC

- LocumTenens.com LLC

- 24Hr HomeCare Inc.

- Trustaff Management Inc.

- TeamHealth Holdings Inc.

- Syneos Health Inc.

- Ingenovis Health Inc.

- Curative Talent LLC

- Health Carousel LLC

- Medical Solutions LLC

- Heatlhcare Australia Holdings Pty Ltd

- Randstad NV(Healthcare Division)

第7章 市場機會與未來展望

According to Mordor Intelligence, the talent acquisition in the healthcare market was valued at USD 29.73 billion in 2025 and is estimated to grow from USD 30.85 billion in 2026 to USD 51.82 billion by 2031, at a CAGR of 10.93% during the forecast period (2026-2031).

This report is Segmented by Technology (Applicant Tracking Systems, Candidate Relationship Management Platforms, and More), Service Type (Permanent Staffing Services, Managed Service Providers, and More), End User (Hospitals and Health Systems, and More), Mode (In-House Talent Acquisition, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Talent Acquisition In Healthcare Market Trends and Insights

Intensifying Workforce Shortages in Allied Health Roles

Allied health vacancies are compelling hospitals to pay premium rates for temporary staff, straining operating margins and fueling aggressive recruitment investments. The American Hospital Association reported in 2025 that 94% of executives ranked staffing as their top operational issue, with annual turnover for respiratory therapists and radiology technicians exceeding 30%. Enrollment in allied health programs fell 8% between 2020 and 2024, while outpatient diagnostics demand jumped 17% over the same span. Health systems are launching apprenticeship pipelines, but those programs take three to five years to produce certified workers, leaving an acute gap that staffing agencies exploit through per-diem placements. Rural providers are hit hardest because clinicians cluster in cities for higher wages, forcing small hospitals to rely on travelers whose costs are 40-60% higher than those of permanent staff. Consequently, talent acquisition in the healthcare market must balance immediate stopgaps with long-term workforce development.

Accelerating Digital Transformation of Hospital HR Functions

Hospital HR digitization is evolving from back-office automation to strategic workforce forecasting. Children's Hospital of Philadelphia cut nursing time-to-hire from 62 to 38 days after rolling out an AI-enabled applicant tracking system in 2024, saving an estimated USD 4.2 million annually. Modern platforms now integrate with electronic health records to flag high-performing clinicians before they enter the job market, lowering cost-per-hire by 30-40%. Credentialing vendors such as Propelus compress onboarding from 45 to 15 days, allowing hospitals to ramp capacity faster during seasonal spikes. The National Committee for Quality Assurance mandated monthly sanction monitoring in 2025, pushing facilities toward automated compliance. These breakthroughs reinforce a data-driven culture that is redefining how talent acquisition in the healthcare market operates.

High Sensitivity of Candidate Data to Cyber-Security Breaches

Recruitment platforms store Social Security numbers, license records, and malpractice histories, making them prime targets for ransomware. The February 2024 attack on Change Healthcare exposed data on over 100 million individuals and cost USD 2.3 billion in remediation. Under the Health Insurance Portability and Accountability Act, inadequate safeguards can result in fines of up to USD 1.5 million per violation. Hospitals now require vendors to obtain SOC 2 Type II certification and undergo annual penetration tests, which are inflating compliance costs, especially for small agencies. These cyber risks temper investment appetite in talent acquisition in the healthcare market.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Flexible Gig-Based Clinical Staffing Models

- Adoption of AI-Powered Sourcing to Reduce Time-to-Hire

- Fragmented Licensing Rules Across US States and EU Nations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Applicant tracking systems accounted for 38.28% spending in 2025 and remain the system of record for most hospitals. Yet the segment's growth is moderating as buyers prioritize platforms that mesh with payroll, scheduling, and electronic health records. AI-enabled sourcing and candidate relationship management solutions, growing 12.19% annually, are redefining how talent acquisition in the healthcare market evolves at the technology layer. Hospitals deploying these tools report time-to-hire reductions of 20-30% and lower "ghosting" rates, because machine-learning engines nudge candidates with automated reminders.

The talent acquisition market share for traditional background screening software is shrinking as hospitals seek unified stacks that conduct criminal checks, license verification, and reference checks in a single workflow. Video interviewing remains commonplace for telehealth roles, but pricing compression is driving consolidation. Vendors differentiating on predictive analytics, such as recommending competitive pay bands based on regional benchmark data, are gaining traction, especially among large systems that hire thousands of clinicians yearly.

Permanent staffing delivered 41.43% of 2025 revenue, reflecting ongoing demand for full-time clinicians. Yet rising physician burnout propels an 11.43% CAGR for locum tenens services, which now represent a critical pressure valve for facilities in remote geographies. This growth influences the talent acquisition in the healthcare market, as episodic contracts fetch premium bill rates that outpace inflation.

Managed service providers (MSPs) and recruitment process outsourcing (RPO) continue to gain share by offering bundled contingent labor, compliance monitoring, and vendor consolidation. Hospitals using MSPs report administrative savings of 15-20% because a single dashboard unifies invoicing and credential tracking. Meanwhile, temporary allied health staffing is broadening beyond respiratory therapy into imaging and laboratory specialties, widening the scope of talent acquisition in the healthcare industry.

Geography Analysis

North America generated 37.21% revenue in 2025, anchored by the United States' multistate licensing complexity, elevated clinician wages, and a payer mix that sustains premium bill rates. Enhanced Nurse Licensure Compact adoption across 41 states eases nurse mobility, but California and New York maintain independent processes that prolong onboarding. Canada bolsters rural coverage by importing 4,200 international medical graduates in 2025, an 18% jump from 2023. Mexico's private hospital boom along the border attracts bilingual care teams, funneling cross-border recruitment dollars into the healthcare talent acquisition market.

Asia-Pacific posts the fastest regional trajectory with a 10.94% CAGR to 2031. India's surplus of 140,000 nurses in 2025 feeds outbound staffing pipelines to Gulf Cooperation Council nations and Australia. Saudi Arabia's Vision 2030 hospital build-out and the United Arab Emirates' specialty clinic growth amplify regional demand. Japan faces an aging population, with 28.7% of the population over 65 in 2025, prompting investments in robotics and task-shifting to offset nursing shortages. China's private hospital segment grows 12% annually, but provincial licensing and Hukou restrictions impede national staffing platforms, limiting scale advantages in regional healthcare talent acquisition.

Europe's free-movement directive, in theory, simplifies credential portability, yet language and competency tests in Germany, France, and Italy create bottlenecks. Germany hired 12,400 foreign nurses in 2025, largely from the Philippines and India, to mitigate demographic pressures. The United Kingdom's National Health Service filled 35% of nursing vacancies with international recruits in 2025, but competition from Gulf countries offering higher wages is eroding its pull factor. South America remains under-penetrated, though private hospital chains in Brazil and Argentina are beginning to adopt structured vendor management, hinting at future growth opportunities for talent acquisition in the healthcare market.

- AMN Healthcare Services Inc.

- CHG Healthcare Services Inc.

- Cross Country Healthcare Inc.

- Encompass Health Corporation

- MEDNAX Services Inc.

- Jackson Healthcare LLC

- Maxim Healthcare Group

- Aya Healthcare Inc.

- HealthTrust Workforce Solutions LLC

- LocumTenens.com LLC

- 24Hr HomeCare Inc.

- Trustaff Management Inc.

- TeamHealth Holdings Inc.

- Syneos Health Inc.

- Ingenovis Health Inc.

- Curative Talent LLC

- Health Carousel LLC

- Medical Solutions LLC

- Heatlhcare Australia Holdings Pty Ltd

- Randstad N.V. (Healthcare Division)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Digital Transformation of Hospital HR Functions

- 4.2.2 Intensifying Workforce Shortages in Allied Health Roles

- 4.2.3 Shift Toward Flexible Gig-Based Clinical Staffing Models

- 4.2.4 Growing Regulatory Pressures for Credential Verification Automation

- 4.2.5 Adoption of AI-Powered Sourcing to Reduce Time-to-Hire

- 4.2.6 Expansion of Cross-Border Telehealth Driving Global Talent Pools

- 4.3 Market Restraints

- 4.3.1 High Sensitivity of Candidate Data to Cyber-Security Breaches

- 4.3.2 Fragmented Licensing Rules Across US States and EU Nations

- 4.3.3 Union-Led Resistance to Algorithmic Screening Tools

- 4.3.4 Budget Constraints in Rural and Safety-Net Facilities

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Applicant Tracking Systems (ATS)

- 5.1.2 Candidate Relationship Management Platforms

- 5.1.3 AI-Based Recruitment Tools

- 5.1.4 Video Interviewing Platforms

- 5.1.5 Background Screening Software

- 5.1.6 Other Technologies

- 5.2 By Service Type

- 5.2.1 Permanent Staffing Services

- 5.2.2 Temporary Staffing Services

- 5.2.3 Recruitment Process Outsourcing (RPO)

- 5.2.4 Managed Service Providers (MSP)

- 5.2.5 Locum Tenens Staffing

- 5.2.6 Other Service Types

- 5.3 By End User

- 5.3.1 Hospitals and Health Systems

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Nursing Homes and Long-Term Care Facilities

- 5.3.4 Home Healthcare Providers

- 5.3.5 Diagnostic Laboratories

- 5.3.6 Other Healthcare Providers

- 5.4 By Mode

- 5.4.1 In-House Talent Acquisition

- 5.4.2 Outsourced Talent Acquisition

- 5.4.3 Hybrid Model

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AMN Healthcare Services Inc.

- 6.4.2 CHG Healthcare Services Inc.

- 6.4.3 Cross Country Healthcare Inc.

- 6.4.4 Encompass Health Corporation

- 6.4.5 MEDNAX Services Inc.

- 6.4.6 Jackson Healthcare LLC

- 6.4.7 Maxim Healthcare Group

- 6.4.8 Aya Healthcare Inc.

- 6.4.9 HealthTrust Workforce Solutions LLC

- 6.4.10 LocumTenens.com LLC

- 6.4.11 24Hr HomeCare Inc.

- 6.4.12 Trustaff Management Inc.

- 6.4.13 TeamHealth Holdings Inc.

- 6.4.14 Syneos Health Inc.

- 6.4.15 Ingenovis Health Inc.

- 6.4.16 Curative Talent LLC

- 6.4.17 Health Carousel LLC

- 6.4.18 Medical Solutions LLC

- 6.4.19 Heatlhcare Australia Holdings Pty Ltd

- 6.4.20 Randstad N.V. (Healthcare Division)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

IT永續發展人才與培訓平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區人才招聘軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031)北美人才招聘軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)銀行、金融服務和保險 (BFSI) 市場的人才招聘:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)

IT永續發展人才與培訓平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區人才招聘軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031)北美人才招聘軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)銀行、金融服務和保險 (BFSI) 市場的人才招聘:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031) 數位人才招募市場:按組件、最終用戶、部署類型、產業和應用程式分類-2026-2032年全球市場預測

數位人才招募市場:按組件、最終用戶、部署類型、產業和應用程式分類-2026-2032年全球市場預測 人才招募技術與服務市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶與功能分類IT人員配備:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)

人才招募技術與服務市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶與功能分類IT人員配備:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年) 醫療保健人員增補市場 - 2026-2031 年預測

醫療保健人員增補市場 - 2026-2031 年預測 人才招募軟體市場規模、佔有率和成長分析(按部署類型、組織規模、垂直產業、功能、定價模式和地區分類)-2026-2033年產業預測全球人力增強服務市場(按人員配備類型、僱用模式、合約期限、服務供應商、產業和公司規模):預測(2025-2030 年)

人才招募軟體市場規模、佔有率和成長分析(按部署類型、組織規模、垂直產業、功能、定價模式和地區分類)-2026-2033年產業預測全球人力增強服務市場(按人員配備類型、僱用模式、合約期限、服務供應商、產業和公司規模):預測(2025-2030 年)