|

市場調查報告書

商品編碼

2063858

銀行、金融服務和保險 (BFSI) 市場的人才招聘:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)Talent Acquisition In BFSI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

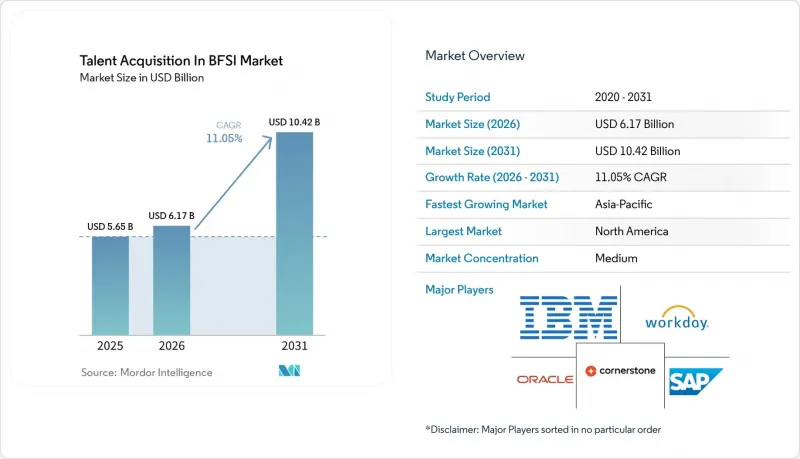

據 Mordor Intelligence 稱,2025 年 BFSI 市場中的人才招聘市場價值 57 億美元,預計在預測期(2026-2031 年)內將以 11.05% 的複合年成長率成長,從 2026 年的 62 億美元成長到 2031 億美元的 1041 億美元。

本報告按元件(軟體解決方案[應徵者追蹤系統 (ATS)、候選人關係管理 (CRM)、招募和行銷套件、面試和評估工具、入職解決方案]和服務)、部署模式(本地部署和雲端部署)、組織規模(大型企業和中小企業)以及地區進行細分。市場預測以價值(美元)表示。

銀行、金融服務和保險 (BFSI) 市場全球人才招募趨勢與洞察

新銀行強制推行數位化優先的客戶註冊流程。

在銀行、金融和保險(BFSI)產業中,新銀行在招募科技應用方面最為積極主動。這不僅是因為它們招募速度快,還因為它們以合規為先的組織架構要求從銀行牌照啟動之日起,就必須建立一套完全可審計且數位化整合的入職流程。 Revolut於2024年中期獲得英國銀行牌照,隨後在2025年啟動了一項在西歐招募400人的宣傳活動。這些職位大多與合規、風險管理和金融犯罪預防有關,而此次宣傳活動顯然與Revolut在巴黎申請銀行牌照以及相關的監管人員配備要求密切相關。荷蘭新銀行Bunq在2024年將全球員工人數擴大了70%,目標是在三大洲的九個城市招募專業人才。這需要建立一套跨國人才招募基礎設施作為前提。 Monzo於2025年12月透過愛爾蘭中央銀行獲得歐盟全面銀行牌照後,計劃在2027年中期將其在愛爾蘭的員工人數增加近一倍,達到70人。每家新銀行獲得執照,都使得數位化人才招聘平台不再只是生產力工具,而是幾乎不可或缺的監管基礎設施。這一趨勢正在推動對新銀行招聘項目的結構性需求,使其不再受整體經濟週期的影響。

風險與合規領域專業人才短缺

由於風險和合規領域專業人才短缺是銀行、金融服務和保險(BFSI)市場人才招募最強勁的成長要素之一,因為這是結構性問題而非週期性問題。近90%的金融服務合規主管表示,過去三年他們的職責增加,超過半數的人預計未來12個月內,其專業領域將出現技能短缺。在新加坡,新加坡金融管理局(MAS)正與本地及全球銀行合作,提升反洗錢(AML)標準並解決人才短缺問題,這表明人才短缺問題已從內部人力資源問題轉變為監管層面的問題。研究發現,擁有成熟人才流動能力的機構在應對中期人才短缺方面效率高出3.7倍,這促使BFSI機構在現代招聘平台上實施內部技能映射和繼任計畫。在香港和新加坡,2026年的薪酬數據顯示,新加坡金融管理局(MAS)監管報告和數位資產合規等專業的薪酬溢價為3-6%,凸顯了主動建構人才儲備而非被動發布招聘資訊的重要性。因此,BFSI 市場的人才招募受到可用候選人與職缺中的監管複雜性之間狹窄但持續存在的不匹配的影響。

傳統核心銀行系統阻礙了系統整合。

許多金融機構仍在使用基於傳統架構構建的薪資核算、人力資源和合規系統,這些架構是針對每個國家/地區量身定做的,這使得傳統的核心銀行基礎設施成為金融服務業(BFSI)人才招聘的一大障礙。金融機構通常面臨著由上世紀90年代或更早時期建構的系統所形成的碎片化資料環境,這使得透過API主導與現代人才平台整合變得困難。丹麥銀行目前正在遷移到一個整合了四家北歐薪資核算供應商的雲端解決方案(計劃於2026年底在芬蘭投入運作),這表明即使是資源充足的金融機構也面臨著長達數年的現代化改造計畫。對於中型銀行、合作社和區域性保險公司而言,這種障礙更為突出,因為它們的IT團隊通常缺乏同時實現核心系統現代化和整合新招募工具的能力。人力資源部門和IT部門之間的管治差距也加劇了延誤,因為資料所有權、配置標準和系統優先順序往往不明確。這使得在那些仍然普遍存在老舊、高度客製化銀行架構的地區,進入金融服務業(BFSI)人才招募市場變得更加困難。

細分市場分析

2025年,軟體解決方案在銀行、金融服務和保險(BFSI)市場的人才招募解決方案中佔比高達84.2%。這反映出金融機構高度依賴可配置平台,這些平台能夠在單一營運層內支援人才搜尋、篩檢、評估和入職等流程。 2025年,應徵者追蹤系統(ATS)佔整體市場的34.5%,證實ATS平台仍是建構候選人關係管理、面試工具、招募行銷和入職模組的基礎。這項基礎對於BFSI市場的人才招募至關重要,因為金融機構希望在擴展到更高價值的智慧層之前,先建立系統控制、工作流程一致性和稽核準備。隨著招募團隊從被動發布職位轉向為合規和風險管理等難以招募的職位建立長期人才儲備,候選人關係管理平台的重要性日益凸顯。此外,隨著人工智慧驅動的結構化面試為受監管的雇主提供更完善的流程文件和一致的決策記錄,面試和評估工具的價值也在不斷提升。

預計到2031年,服務市場將以11.8%的複合年成長率成長,成為銀行、金融服務和保險(BFSI)市場人才招募領域成長最快的組成部分。這反映出一個明顯的實施差距,因為許多BFSI人力資源團隊仍需要協助,才能將軟體功能轉化為實際的流程設計、負責人工作流程和管治管理。一項2025年關於人才招募技術的調查發現,56%的組織仍主要將人工智慧視為生產力工具,而不是轉型驅動力。這凸顯了採用和轉型支援的必要性。在2025年9月收購後,SAP於2026年3月加強了與SAP SuccessFactors中SmartRecruiters的整合。這表明平台供應商正擴大將更緊密的服務和實施支援整合到產品本身。因此,BFSI市場的人才招募不再僅由軟體需求驅動,因為服務合作夥伴對於實施的品質和速度正變得至關重要。

區域分析

截至2026年初,北美將佔銀行、金融服務和保險(BFSI)行業人才招聘的38.6%,繼續保持領先地位,這得益於多種因素的共同作用,包括大型金融機構的存在、對成熟的人力資源技術的投資以及持續的合規人才招聘壓力。美國的需求依然強勁,預計2024年至2034年間,每年將新增33,300名合規負責人。這為銀行、保險公司和投資公司不斷更新和擴展其平台提供了支持。監管也影響供應商的選擇,例如紐約市第144號地方法律規定,對人工智慧驅動的篩檢工具進行年度偏見審計,實際上已成為許多買方評估的必要條件。在加拿大,大型銀行擴大將外部招聘與內部調動相結合,例如豐業銀行對人才發展的投資以及對廣泛技能的重視。墨西哥和其他北美國家對市場的貢獻仍然較小,但隨著該地區金融科技活動的活性化數位化和合規人才的需求不斷成長,它們的重要性也日益凸顯。

預計到2031年,亞太地區將以13.8%的複合年成長率成長,成為銀行、金融服務和保險(BFSI)市場人才招募成長最快的地區。數位銀行、合規人才的嚴重短缺以及監管現代化正在推動新加坡、香港、中國、印度、日本、韓國和澳洲等地對相關平台的需求。新加坡監管機構支持的反洗錢(AML)工作小組以及2026年區域招聘中心合規和數位資產專家的薪酬溢價(3-6%)表明,人才短缺正促使雇主採用積極主動的人才招聘系統。平安保險於2025年3月推出其自主研發的人工智慧招募系統,進一步凸顯了區域領導者正在積極提升市場整體技術水平,而非等待供應商成熟。

2025年,歐洲仍將是吸引人才進入銀行、金融服務和保險(BFSI)市場的重要力量,其中英國、德國和法國仍是主要的需求中心。在英國,隨著企業應對消費者責任、營運韌性、非金融不當行為以及新興人工智慧管治需求,合規人才的招募模式在2026年從企劃為基礎合約轉向業務永續營運僱用。歐盟的《企業永續性發展報告指令》推動了對能夠系統展現員工多樣性、薪資差距和培訓資料(這些資料往往被傳統工具忽略)的系統的需求。在中東,根據阿拉伯聯合大公國中央銀行的報告,截至2025年12月31日,共有23,364名阿拉伯聯合大公國國民在銀行、金融和保險業就業,阿拉伯聯合大公國公民佔比為31%。相較之下,銀行業已設定目標,到2026年底達到45%,並要求許可機構的合規率達到97%。在沙烏地阿拉伯,自2026年4月7日起,100%沙烏地阿拉伯化政策將擴展至69個工作類別,這將對具備在地化追蹤、工資合規和審計報告功能的招募系統產生類似的需求。同時,在非洲和南美洲,由該地區最大的銀行集團和金融科技公司主導的新興商業機會依然存在。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新銀行強制推行數位化優先的客戶註冊流程。

- 風險與合規領域專業人才短缺

- 透過在甄選過程中運用人工智慧,我們縮短了招募時間。

- 嵌入式金融的興起與人才招募的擴張

- 監管部門推動海灣合作理事會成員國勞動力本地化。

- ESG報告要求提高了人力資源領域的透明度。

- 市場限制因素

- 傳統的核心銀行系統阻礙了系統整合。

- 人們越來越關注資料安全和隱私問題

- 波動劇烈的金融科技資金籌措週期

- 招募技術投資報酬率難以量化。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體解決方案

- 應徵者追蹤系統(ATS)

- 候選人關係管理(CRM)

- 招募行銷套件

- 面試和評估工具

- 入職解決方案

- 服務

- 軟體解決方案

- 部署模式

- 現場

- 雲

- 按組織規模

- 大公司

- 小型企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday Inc.

- SAP SE

- Oracle Corporation

- International Business Machines Corporation

- Cornerstone OnDemand Inc.

- Automatic Data Processing Inc.

- Ceridian HCM Holding Inc.

- iCIMS Inc.

- SmartRecruiters Inc.

- Greenhouse Software Inc.

- Lever Inc.

- Jobvite Inc.

- HireVue Inc.

- Eightfold AI Inc.

- Phenom People Inc.

- ClearCompany LLC

- Avature Ltd.

- Pymetrics Inc.

- SeekOut Inc.

- Beamery Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the talent acquisition in the BFSI market was valued at USD 5.7 billion in 2025 and is estimated to grow from USD 6.2 billion in 2026 to USD 10.4 billion by 2031, at a CAGR of 11.05% during the forecast period (2026-2031).

This report is Segmented by Component (Software Solutions [Applicant Tracking System (ATS), Candidate Relationship Management (CRM), Recruitment Marketing Suite, Interview and Assessment Tools, and Onboarding Solutions], and Services), Deployment Mode (On-Premises, and Cloud), Organization Size (Large Enterprises, and SMEs), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Talent Acquisition In BFSI Market Trends and Insights

Digital-First Onboarding Mandates by Neobanks

Neobanks are among the most prolific buyers of recruitment technology in BFSI, not simply because they hire at velocity, but because their compliance-first organizational structures require onboarding workflows that are fully auditable and digitally integrated from day one of any banking license activation. Revolut, which received its UK banking license in mid-2024, subsequently launched a 400-role Western European recruitment drive in 2025, with compliance, risk management, and financial crime prevention dominating the open positions, a campaign explicitly tied to its Paris banking license application and the regulatory staffing requirements that accompany it. Dutch neobank Bunq expanded its global headcount by 70% in 2024, targeting specialized talent across nine cities and three continents, requiring a multi-jurisdictional talent-acquisition infrastructure as a prerequisite. Monzo is committed to nearly doubling its Irish headcount to 70 employees by mid-2027, driven by its December 2025 acquisition of a full EU banking license through the Central Bank of Ireland. Each neobank licensing event effectively mandates digital talent acquisition platforms as regulatory infrastructure rather than optional productivity tooling, a dynamic that makes neobank hiring programs a structural demand driver independent of broader economic cycles.

Shortage of Niche Risk and Compliance Talent

The shortage of niche risk and compliance talent remains one of the strongest growth drivers for talent acquisition in the BFSI market, as it is structural rather than cyclical. Nearly 90% of financial services compliance executives reported their responsibilities had increased over the prior three years, while more than half expected a skills shortage in specialist areas within the next 12 months. In Singapore, the Monetary Authority of Singapore worked with local and global banks to improve AML standards and address staffing gaps, showing that the talent shortage had moved from an internal HR issue to a regulatory concern. Organizations with mature talent mobility functions were found to be 3.7 times more effective at addressing medium-term shortages, prompting BFSI institutions to adopt internal skills mapping and succession planning within modern hiring platforms. In Hong Kong and Singapore, salary data for 2026 pointed to 3-6% premiums for specialist roles such as MAS regulatory reporting and digital assets compliance, reinforcing the case for proactive pipelining rather than reactive posting. As a result, the talent acquisition in the BFSI market is being shaped by a narrow but persistent mismatch between available candidates and the regulatory complexity of open roles.

Legacy Core Banking Systems Limit Integration

Legacy core banking infrastructure continues to slow the talent acquisition in BFSI market because many institutions still run payroll, HR, and compliance systems built on old architectures with country-level customizations. Financial institutions often work with fragmented data environments shaped by systems built in the 1990s or earlier, which makes API-led integration with modern talent platforms difficult. Danske Bank's ongoing effort to consolidate four Nordic payroll vendors into a unified cloud solution, with Finland planned to go live in late 2026, shows how even well-resourced institutions face multi-year modernization timelines. The barrier is sharper in mid-tier banks, cooperative institutions, and regional insurers because IT teams often do not have the capacity to modernize core systems and connect new recruiting tools at the same time. Governance gaps between HR and IT also add delay when data ownership, configuration standards, and system priorities are unclear. This makes the talent acquisition in BFSI market harder to penetrate in regions where older and highly customized banking structures remain common.

Other drivers and restraints analyzed in the detailed report include:

- AI-Powered Screening Reduces Time-to-Hire

- Rise of Embedded Finance Expanding Hiring Pools

- High Data Security and Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software solutions accounted for 84.2% of talent acquisition in the BFSI market in 2025, reflecting the heavy reliance of financial institutions on configurable platforms that support sourcing, screening, assessment, and onboarding within a single operating layer. Applicant tracking systems captured 34.5% of the overall market in 2025, confirming that ATS platforms remain the foundation on which candidate relationship management, interview tools, recruitment marketing, and onboarding modules are built. Within the talent acquisition in the BFSI industry, that foundation matters because institutions want system control, workflow consistency, and audit readiness before they expand into higher-value intelligence layers. Candidate relationship management platforms are gaining importance as hiring teams move away from reactive job posting and toward long-cycle talent pipelining for hard-to-fill compliance and risk positions. Interview and assessment tools are also rising in value as AI-enabled structured interviews create stronger process documentation and more consistent decision trails for regulated employers.

Services are projected to grow at a 11.8% CAGR through 2031, making them the fastest-growing component of talent acquisition in the BFSI market. This reflects a clear execution gap, as many BFSI HR teams still need help translating software capabilities into live process design, recruiter workflows, and governance controls. A 2025 review of talent acquisition technology found that 56% of organizations still viewed AI mainly as a productivity tool rather than a transformation enabler, which supports the case for implementation and change support. SAP deepened its SmartRecruiters integration within SAP SuccessFactors in March 2026 after its September 2025 acquisition, demonstrating how platform vendors are integrating closer service and deployment support into the product stack itself. As a result, talent acquisition in the BFSI market is not driven solely by software demand, because service partners are becoming essential to the quality and speed of adoption.

Geography Analysis

North America held 38.6% of the talent acquisition in the BFSI market share at the start of 2026, keeping it in the lead because the region combines large financial institutions, mature HR technology spending, and persistent compliance hiring pressure. The United States continues to provide a strong demand base, with projected annual openings of 33,300 compliance officers from 2024 through 2034, which supports ongoing platform renewal and expansion across banks, insurers, and investment firms. Regulatory scrutiny is also shaping vendor selection, as New York City's Local Law 144 has made annual bias audits a practical requirement for AI-enabled screening tools in many buyer evaluations. In Canada, large banks are increasingly blending external recruitment with internal mobility, as seen in Scotiabank's workforce development spending and broader skills focus. Mexico and the rest of North America remain smaller contributors, but they are gaining relevance as regional fintech activity expands demand for digital and compliance talent.

Asia-Pacific is set to expand at a 13.8% CAGR through 2031, making it the fastest-growing geography in the BFSI talent acquisition market. Digital banking, acute shortages of compliance talent, and regulatory modernization are all driving platform demand across Singapore, Hong Kong, China, India, Japan, South Korea, and Australia. Singapore's regulator-backed AML working group and 2026 salary premiums of 3-6% for compliance and digital assets specialists in regional hiring hubs show how scarcity is pushing employers toward proactive sourcing systems. Ping An Insurance's March 2025 launch of its in-house AI recruitment system further showed that leading regional incumbents are not waiting for vendor maturity and are actively raising the technology baseline across the market.

Europe retained a significant position in the talent acquisition in the BFSI market in 2025, with the United Kingdom, Germany, and France remaining the main demand centers. In the UK, compliance hiring shifted in 2026 from project-based contracting toward permanent hiring as firms responded to Consumer Duty, operational resilience, non-financial misconduct, and emerging AI governance needs. The European Union's Corporate Sustainability Reporting Directive is adding pressure for systems that can capture workforce diversity, pay equity, and training data in a structured form that legacy tools often miss. In the Middle East, the Central Bank of the UAE reported that 23,364 UAE nationals were working across banking, financial, and insurance activities as of December 31, 2025, representing a 31% Emiratisation rate, against a banking-sector target of 45% by the end of 2026 and 97% compliance among licensed institutions. Saudi Arabia's widened 100% Saudization mandate across 69 job categories, effective from April 7, 2026, is creating a similar need for recruitment systems with localization tracking, wage compliance, and audit reporting, while Africa and South America remain earlier-stage opportunities led by the region's largest banking groups and fintech firms.

- Workday Inc.

- SAP SE

- Oracle Corporation

- International Business Machines Corporation

- Cornerstone OnDemand Inc.

- Automatic Data Processing Inc.

- Ceridian HCM Holding Inc.

- iCIMS Inc.

- SmartRecruiters Inc.

- Greenhouse Software Inc.

- Lever Inc.

- Jobvite Inc.

- HireVue Inc.

- Eightfold AI Inc.

- Phenom People Inc.

- ClearCompany LLC

- Avature Ltd.

- Pymetrics Inc.

- SeekOut Inc.

- Beamery Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital-First Onboarding Mandates by Neobanks

- 4.2.2 Shortage of Niche Risk and Compliance Talent

- 4.2.3 AI-Powered Screening Reduces Time-to-Hire

- 4.2.4 Rise of Embedded Finance Expanding Hiring Pools

- 4.2.5 Regulatory Push for Workforce Localization in GCC

- 4.2.6 ESG Reporting Requirements Elevate HR Transparency

- 4.3 Market Restraints

- 4.3.1 Legacy Core Banking Systems Limit Integration

- 4.3.2 High Data Security and Privacy Concerns

- 4.3.3 Volatile Fintech Funding Cycles

- 4.3.4 Difficulty Quantifying ROI on Recruitment Tech

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Solutions

- 5.1.1.1 Applicant Tracking System (ATS)

- 5.1.1.2 Candidate Relationship Management (CRM)

- 5.1.1.3 Recruitment Marketing Suite

- 5.1.1.4 Interview and Assessment Tools

- 5.1.1.5 Onboarding Solutions

- 5.1.2 Services

- 5.1.1 Software Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Egypt

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 International Business Machines Corporation

- 6.4.5 Cornerstone OnDemand Inc.

- 6.4.6 Automatic Data Processing Inc.

- 6.4.7 Ceridian HCM Holding Inc.

- 6.4.8 iCIMS Inc.

- 6.4.9 SmartRecruiters Inc.

- 6.4.10 Greenhouse Software Inc.

- 6.4.11 Lever Inc.

- 6.4.12 Jobvite Inc.

- 6.4.13 HireVue Inc.

- 6.4.14 Eightfold AI Inc.

- 6.4.15 Phenom People Inc.

- 6.4.16 ClearCompany LLC

- 6.4.17 Avature Ltd.

- 6.4.18 Pymetrics Inc.

- 6.4.19 SeekOut Inc.

- 6.4.20 Beamery Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

IT永續發展人才與培訓平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區人才招聘軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031)北美人才招聘軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)醫療保健產業人才招聘:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

IT永續發展人才與培訓平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區人才招聘軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031)北美人才招聘軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)醫療保健產業人才招聘:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 數位人才招募市場:按組件、最終用戶、部署類型、產業和應用程式分類-2026-2032年全球市場預測

數位人才招募市場:按組件、最終用戶、部署類型、產業和應用程式分類-2026-2032年全球市場預測 人才招募技術與服務市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶與功能分類IT人員配備:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)

人才招募技術與服務市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶與功能分類IT人員配備:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年) 醫療保健人員增補市場 - 2026-2031 年預測

醫療保健人員增補市場 - 2026-2031 年預測 人才招募軟體市場規模、佔有率和成長分析(按部署類型、組織規模、垂直產業、功能、定價模式和地區分類)-2026-2033年產業預測全球人力增強服務市場(按人員配備類型、僱用模式、合約期限、服務供應商、產業和公司規模):預測(2025-2030 年)

人才招募軟體市場規模、佔有率和成長分析(按部署類型、組織規模、垂直產業、功能、定價模式和地區分類)-2026-2033年產業預測全球人力增強服務市場(按人員配備類型、僱用模式、合約期限、服務供應商、產業和公司規模):預測(2025-2030 年)