|

市場調查報告書

商品編碼

2063822

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Heat Pump Dryer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

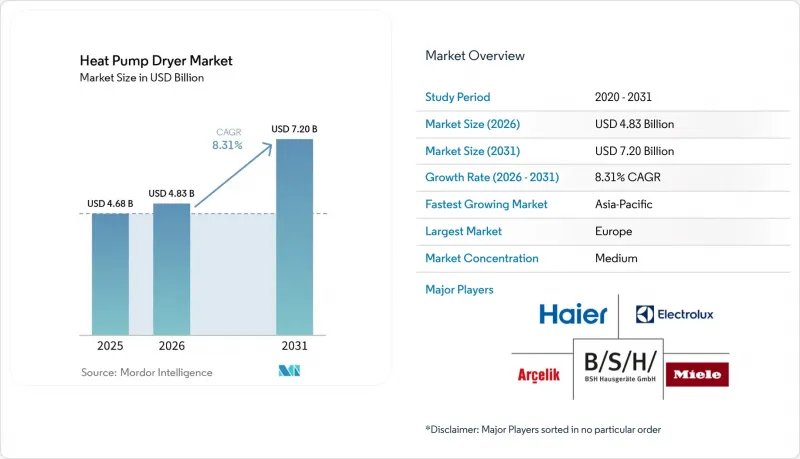

根據 Mordor Intelligence 預測,全球熱泵乾燥機市場規模將從 2025 年的 46.8 億美元成長到 2026 年的 48.3 億美元,到 2031 年將達到 72 億美元,2026 年至 2031 年的複合年成長率預計為 8.31%。

本報告按產品類型(冷凝式、通風式、一體式)、容量(8公斤以下、9-10公斤、11公斤以上)、最終用戶(住宅、商業、工業)、分銷管道(B2C/零售、B2B/直銷)和地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測以美元計價。

全球熱泵乾燥機市場趨勢及洞察

能源效率標準和標籤要求正在加速熱泵的普及。

自2025年7月1日起,歐盟市場將只允許採用熱泵技術的滾筒式乾衣機銷售,排氣式電乾衣機和電阻式冷凝乾衣機將被淘汰。研發重點將轉向設計高效的封閉回路型烘乾系統。歐盟也將其能源效率標籤系統重新分類為A至G等級,最高等級代表能源效率最高的型號,此舉旨在重新定義消費者預期,並改善全球熱泵乾衣機市場的銷售點資訊。在美國,能源部發布了一項最終規則,引入了總能效(CEF)閾值,合規期限為2028年3月1日。這將鼓勵不符合標準的傳統電動乾衣機和緊湊型無排氣乾衣機向熱泵或混合動力配置轉型,從而降低整個產品系列的碳足跡。能源之星規範草案2.0版提案的CEF(總能效)閾值和循環時間限制均高於美國能源部的最低標準,為高CEF、高能源效率的乾衣機平台獲得高級認證和在零售店醒目展示鋪平了道路。 IEC 60335-2-11:2024安全標準規定了使用易燃冷媒的家用電器的要求,包括檢測、氣密性和遠端控制等方面的規定。這將有助於R290在全球熱泵乾衣機市場中得到更廣泛的應用,同時保護家居環境。

公共產業獲得的補貼和獎勵可以縮短投資回收期。

經能源之星認證的熱泵乾衣機在銷售點可享有直接折扣,降低購買門檻,使全球熱泵乾衣機市場中眾多家庭能夠即時享受到價格優勢,從而節省長期成本。各州允許使用者自行安裝電暖器改造專案的計畫正在擴大適用範圍並降低人事費用,加速在建築條件允許的情況下推廣無廢氣排放的便捷型乾衣機。喬治亞亞州的計畫除了提供自行安裝選項外,還提供線路和配電盤安裝補貼,使電力基礎設施老舊的家庭能夠以獎勵價格購買節能乾衣機。來自明尼蘇達電力公司和DTE能源公司等電力公司的補貼可以與聯邦撥款疊加使用,增加補貼總合,擴大全球熱泵乾衣機市場中能夠輕鬆轉向熱泵乾衣機的買家群體,讓他們在不增加預算負擔的情況下也能享受到優惠。 SMUD針對多用戶住宅的項目,例如燃氣系統改造為電力系統的獎勵,直接針對共享洗衣房和物業組合,幫助機構投資者實現綠色技術的標準化並降低營運成本。

與通風/冷凝式機組相比,初始成本較高。

與通風式或電阻式冷凝式乾衣機相比,熱泵乾衣機較高的初始價格仍然是成本敏感型家庭的一大障礙。然而,生命週期成本的降低和補貼正在縮小全球熱泵乾衣機市場許多地區的差距。銷售點補貼和公共產業獎勵,以及可與聯邦項目結合使用的補貼,可以將長期節省轉化為符合條件的買家的即時折扣,從而擴大節能乾衣機的覆蓋範圍。企業客戶也在權衡降低營運成本的益處與資本投資預算和產能需求,因此會因預算限制而延遲更換。隨著越來越多的品牌提供在保持成本績效的同時精簡不必要功能的經濟型配置,價格差距正在進一步縮小,推動全球熱泵乾衣機市場各個收入階層的消費者接受度不斷提高。

細分市場分析

到2025年,冷凝式熱泵乾衣機將佔據全球熱泵乾衣機市場76.91%的佔有率,並憑藉其封閉回路型乾燥系統保持主導地位。該系統簡化了維修,並為各種類型的住宅提供無排氣便利。目前,熱泵技術在歐盟已成為一項監管標準,並在北美市場呈現明顯的優質化趨勢。領導品牌已將自清潔冷凝器、變頻壓縮機和應用程式控制功能作為標準配置,以滿足消費者對節能乾衣機的期望。排氣式熱泵乾衣機仍屬於小眾產品,因為主要地區的能源標籤和建築規範更重視封閉回路型系統的效率和冷凝性能,銷售空間和獎勵也主要集中在冷凝式配置上。

到2031年,成長最快的類型將是嵌入式烘乾機。由於高階消費者青睞基於感測器的烘乾功能、濕度感測器和混合烘乾系統(這些功能在提升性能的同時又不影響美觀),預計嵌入式烘乾機的複合年成長率將達到8.72%。全球熱泵烘乾機市場正經歷產品線整合,冷凝式和整合式機型共用壓縮機、感測器和基板,而差異化則主要體現在外觀品質、安裝複雜性和噪音性能。歐盟(EU)認證標準制定了明確的標準,而提案的能源之星(ENERGY STAR)標準進一步完善了美國的高階標準。這些標準使得能源效率指標在零售店和線上管道都能清晰可見。因此,全球熱泵烘乾機市場越來越依賴使用者體驗、衣物保護和全生命週期服務能力,以在核心能源效率聲明之外實現差異化競爭。

到2025年,9-10公斤容量的乾衣機將佔全球熱泵乾衣機市場的42.83%。這反映了市場對標準安裝方式的核心需求,以滿足典型的家庭洗衣量、均衡的處理能力和衣物保護,同時無需通風,方便快速。隨著歐盟A-G能源效率標籤和北美能源之星認證產品市場佔有率的不斷成長,這一容量級別的乾衣機通常能夠在不佔用過多空間或電力的情況下提供卓越的面積,從而在全球熱泵乾衣機市場中保持其核心地位。 8公斤以下的緊湊型乾衣機和洗烘一體機在公寓和度假屋中發揮著至關重要的作用,因為在這些地方,120V電壓和小巧的佔地面積比最大容量更為重要。所有尺寸的乾衣機都配備了人工智慧控制和混合烘乾系統,可在保持溫和溫度範圍的同時縮短烘乾週期,從而保護衣物並提升用戶滿意度。

容量在11公斤及以上的大容量機種是成長最快的容量組別,預計複合年成長率將達到8.41%。這主要得益於北美地區普通家庭和小規模商業用戶的需求,他們希望在不延長工作時間的情況下處理厚重的床上用品和大量混合衣物。變頻調速技術可減少預熱時間,而增強型濕度感測器即使在滾筒負載波動的情況下也能防止過度烘乾,從而提高效率並保護衣物。 9-10公斤容量範圍仍然是全球熱泵乾衣機市場的核心,在高性能和安裝空間限制之間取得了平衡。同時,緊湊型機型在空間有限或電源改造等原因無法安裝大型機型的建築物中仍然很受歡迎。這種三種容量範圍的結構將支撐全球熱泵乾衣機市場在2031年之前保持穩步成長。

區域分析

到2025年,歐洲將佔全球銷售額的44.93%,凸顯其在生態設計和標籤檢視法規方面的先鋒作用,這些法規正引導全球熱泵乾衣機市場向A級封閉回路型乾燥系統設計邁進。將於2025年7月1日生效的歐盟法規2023/2533及其重新定義的A-G標籤,確立了明確的最低標準和便於消費者理解的指標,從而擴大了高效乾衣機產品在零售商店和電器平台的市場佔有率。基於國際電工委員會(IEC)60335-2-11:2024標準的協調統一,使得R290冷媒的採用成為可能;而對檢測和氣密性要求的明確,則使歐洲製造商能夠選擇在追求低碳排放的同時優先考慮安全性的冷媒。

亞太地區是成長最快的地區,預計複合年成長率將達到9.57%。這主要歸功於政策框架和都市區住宅條件的趨同,使得全球熱泵乾衣機市場更加重視緊湊、無排放和便利的平台。日本的「Top Runner」計畫和韓國的節能計畫持續鼓勵國內主要製造商推出高性能的感測器乾衣機產品,這些產品通常在國內市場率先領先,隨後才會推廣到其他地區。中國的垂直整合正在加速降低成本,並擴大節能乾衣機的選擇範圍,進而影響全球的價格和功能預期。隨著城市密度影響安裝空間標準和消費者期望,7-10公斤容量和先進濕度感測器的組合使亞太地區的消費者即使在有限的空間內也能在全球熱泵乾衣機市場中保護衣物。

北美市場的成長軌跡取決於以下幾個關鍵因素:2028年3月1日前聯邦標準的統一;120V和組合式平台的廣泛應用;以及一項旨在為全球熱泵乾衣機市場目標家庭提供統一價格的節能型乾衣機的綜合獎勵計劃。提案的「能源之星」(ENERGY STAR)標準將引導積分制消費者選擇具有設定循環時間上限的高總能效(CEF)產品,這將指南零售商的庫存管理和線上銷售策略。各州推出的銷售點返利和DIY電改電方案將擴大熱泵乾衣機在老舊住宅中的普及率,這些房屋無需對配電盤進行徹底維修;緊湊型組合式乾衣機將使許多公寓的室內洗衣房也能使用熱泵乾衣機。這些因素將推動全球熱泵乾衣機市場在預測期內持續成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 節能法規和標籤檢視將加速熱泵的普及。

- 電力公司提供的回扣和獎勵可以縮短投資回收期。

- 都市區多用戶住宅的限制正在推動無廢氣烘乾機的普及。

- OEM創新提高了生產週期、噪音和可靠性。

- 從高階價格區間轉向中端價格區間,將擴大目標客戶群。

- 商用洗衣房電氣化與ESG目標

- 市場限制因素

- 與通風/冷凝式機組相比,初始成本較高。

- 在特定條件下延長平均週期時間

- 改用冷媒(R290)將增加重新設計和認證的負擔。

- 由於舊建築的電力容量有限,維修工程延誤了。

- 產業價值鏈分析

- 波特五力模型

- 洞察最新產業趨勢與創新

- 近期產業趨勢分析(新產品發布、策略性舉措、投資、合作、合資、業務擴張、併購等)

- 對主要地區的法律規範和能源效率標準進行研究。

第5章 市場規模與成長預測

- 依產品類型

- 冷凝式熱泵乾燥機

- 排氣式熱泵乾燥機

- 內置熱泵烘乾機

- 按產能

- 8公斤或以下

- 9~10 kg

- 11公斤或以上

- 最終用戶

- 住宅

- 商用(自助洗衣店、旅館、醫療機構、多用戶住宅)

- 工業(輕型洗衣/加工,如適用)

- 透過分銷管道

- B2C/零售通路

- 多品牌商店

- 品牌自營店

- 線上

- 其他分銷管道

- B2B/直銷

- B2C/零售通路

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BSH Hausgerate GmbH(Bosch, Siemens)

- Electrolux Group(Electrolux, AEG, Zanussi)

- Haier Smart Home(Haier, Candy, Hoover, GE Appliances)

- LG Electronics

- Samsung Electronics

- Whirlpool Corporation(incl. Indesit, Maytag, Hotpoint brands where applicable)

- Miele & Cie. KG

- Beko(Arcelik AS)/Grundig

- Gorenje(Hisense Europe)/Hisense

- Fisher & Paykel

- ASKO Appliances

- GE Appliances

- Electrolux Professional

- Alliance Laundry Systems(Speed Queen, Huebsch)

- Girbau

- Panasonic

- Vestel(selected OEM/brands)

- Smeg SpA

- Candy Hoover Group Srl

- Midea Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the global heat pump dryer market size is expected to increase from USD 4.68 billion in 2025 to USD 4.83 billion in 2026 and reach USD 7.20 billion by 2031, growing at a CAGR of 8.31% over 2026-2031.

This report is Segmented by Product Type (Condenser, Vented, Integrated), Capacity (≤8 Kg, 9-10 Kg, ≥11 Kg), End User (Residential, Commercial, Industrial), Distribution Channel (B2C/Retail, B2B/Direct), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Heat Pump Dryer Market Trends and Insights

Efficiency Mandates and Labeling Accelerate Heat-Pump Adoption

From July 1, 2025, only tumble dryers using heat pump technology may be placed on the EU market, eliminating vented electric and resistance-heated condenser alternatives and channeling R&D toward high-efficiency, closed-loop drying system designs. The EU also rescaled labels to an A-G range that preserves the top classes for the most efficient models, resets shopper expectations, and improves signaling at the point of sale across the global heat pump dryer market. In the United States, the Department of Energy's direct final rule sets a March 1, 2028, compliance date with combined energy factor thresholds that pull lagging standard electric and compact ventless models toward heat pump or hybrid configurations, thereby supporting a low-carbon footprint at fleet scale. ENERGY STAR's draft version 2.0 specification proposes CEF thresholds above DOE minimums and a cycle time cap, making high-CEF, Energy-efficient dryer platforms the credible path to premium labeling and retailer prominence. Safety standards in IEC 60335-2-11:2024 define requirements for appliances using flammable refrigerants, including detection, tightness, and remote operation provisions, enabling broader use of R290 while protecting household environments in the global heat pump dryer market.

Utility Rebates and Incentives Shorten Payback

Point-of-sale rebates for ENERGY STAR-certified heat pump clothes dryers apply discounts directly at checkout, reducing decision friction and turning long-run savings into immediate price parity for a wide range of households in the global heat pump dryer market. State programs that permit do-it-yourself installation for electric-to-electric replacements expand eligibility and cut labor overhead, speeding adoption of ventless convenience where building conditions allow. Georgia's program adds a DIY pathway and wiring or panel allowances, which helps households with older electrical infrastructure reach energy-efficient dryer price points after incentives. Utility rebates from providers like Minnesota Power and DTE Energy stack with federal benefits, raising the combined value and broadening the pool of buyers who can switch to heat pumps without budget tension in the global heat pump dryer market. Multifamily-oriented programs, such as SMUD's incentives for gas-to-electric conversions, directly target shared laundry rooms and property portfolios, helping institutional owners standardize green technology and reduce operating costs.

Higher Upfront Price Versus Vented/Condenser Units

Initial price premiums versus vented or resistance-heated condenser dryers remain a barrier for cost-sensitive households, even as lifecycle savings and rebates narrow gaps in many regions of the global heat pump dryer market. Point-of-sale rebates and utility incentives that stack with federal programs convert long-term savings into on-receipt discounts for qualifying buyers, which raises the addressable base for Energy-efficient dryer adoption. Commercial buyers also weigh capital budgets and throughput needs against operating savings, which can defer replacements to coordinated budget windows. As more brands deliver value configurations that preserve core efficiency while trimming extras, the premium narrows further, and adoption improves across income tiers in the global heat pump dryer market.

Other drivers and restraints analyzed in the detailed report include:

- Urban Multifamily Housing Constraints Favor Ventless Dryers

- OEM Innovation Improves Cycle Time, Noise, and Reliability

- Longer Average Cycle Times in Certain Conditions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Condenser heat pump dryers held 76.91% of the global heat pump dryer market share in 2025, and the segment continues to lead due to a closed-loop drying system that simplifies retrofits and supports ventless convenience in a wide range of dwellings. With heat pump technology now the regulatory baseline in the European Union and the clear premium pathway in North America, leading brands feature auto-cleaning condensers, inverter compressors, and app-connected controls as standard, which aligns with Energy-efficient dryer expectations. Vented heat pump models remain a niche as energy labels and building practices across major regions reward closed-loop efficiency and condensation performance, directing shelf space and incentives toward condenser configurations.

Integrated (built-in) models are the fastest-growing type through 2031. They are projected to grow at a 8.72% CAGR as premium buyers align around sensor-based drying, moisture sensors, and hybrid drying systems that improve performance without compromising aesthetics. The global heat pump dryer market is moving toward portfolio convergence, with condenser and integrated lines sharing compressors, sensors, and control boards, while differentiation centers on finish quality, installation complexity, and acoustic targets. European Union labels set a clear bar, and ENERGY STAR's proposed criteria refine the United States' premium thresholds, together making efficiency achievements visible at retail and online. As a result, the global heat pump dryer market relies more on user experience, Fabric protection, and lifecycle service capabilities to differentiate beyond core efficiency claims.

The 9-10 kg bracket captured 42.83% of the global heat pump dryer market in 2025, reflecting the core demand for standard alcove fit, balanced throughput, and fabric protection for typical household loads under ventless convenience. With A-G labeling in the European Union and a rising share of ENERGY STAR-certified products in North America, this capacity range often delivers top performance without imposing space or power burdens, thereby sustaining its central role across the global heat pump dryer market. Compact ≤8 kg dryers and washer dryer combos play a key role in apartments and secondary units where 120V operation and small footprints outweigh maximum capacity. Across sizes, AI controls, and Hybrid Drying Systems are compressing cycles while keeping temperature envelopes gentle, preserving textiles, and increasing real-world satisfaction.

Large-format units rated ≥11 kg are the fastest-growing capacity group, projected to grow at a 8.41% CAGR, as North American households and light commercial users aim to process bulky bedding and high-volume mixed loads without extending total time on task. Inverter speed control reduces the warm-up penalty, and enhanced Moisture Sensors help prevent over-drying even when drum fullness varies, supporting efficiency and fabric protection. The 9-10 kg range remains the center of gravity for the global heat pump dryer market because it pairs top label outcomes with available space constraints, while compact models sustain penetration in buildings that cannot accommodate larger cutouts or power changes. This three-lane capacity structure underpins steady growth in the global heat pump dryer market through 2031.

Geography Analysis

Europe accounted for 44.93% of global revenues in 2025, underscoring the region's role as an early mover on ecodesign and labeling rules that direct the product mix of the global heat pump dryer market toward A-class, closed-loop drying System designs. Regulation (European Union) 2023/2533 and the rescaled A-G label, effective July 1, 2025, set explicit floors and clear consumer cues, which lift the share of energy-efficient dryer products on retail floors and e-commerce listings. With standards harmonization under International Electrotechnical Commission (IEC) 60335 2 11:2024 enabling R290 adoption and clarifying detection and tightness requirements, European manufacturers align refrigerant choices with safety while pursuing a low carbon footprint.

Asia-Pacific is the fastest-growing region, with a projected 9.57% CAGR, as policy frameworks and urban housing realities converge on compact, ventless convenience platforms across the global heat pump dryer market. Japan's TopRunner approach and South Korea's efficiency schemes continue to push domestic champions to release high-performing, Sensor-Based Drying products, often debuting domestically before wider rollout. Vertical integration in China speeds cost curve improvements and supports broader access to Energy-efficient dryer options, which then influence global pricing and feature expectations. With urban density shaping alcove standards and consumer expectations, capacities in the 7-10 kilogram band coupled with advanced moisture sensors help Asia-Pacific buyers match fabric protection to smaller spaces in the global heat pump dryer market.

North America's growth path is defined by the harmonization of federal standards by March 1, 2028, expanding availability of 120V and combo platforms, and the execution of stacked incentive programs that bring energy-efficient dryer models to price parity for qualifying households in the global heat pump dryer market. ENERGY STAR's proposed criteria point premium buyers to high-Combined Energy Factor (CEF) products with cycle time caps, which guides retail stocking and online merchandising. State programs with point-of-sale rebates and DIY options for electric-to-electric swaps increase reach in older housing without full panel work, and compact combos unlock in unit laundry for many apartments. These elements provide durable catalysts for the global heat pump dryer market over the forecast window.

- BSH Hausgerate GmbH (Bosch, Siemens)

- Electrolux Group (Electrolux, AEG, Zanussi)

- Haier Smart Home (Haier, Candy, Hoover, GE Appliances)

- LG Electronics

- Samsung Electronics

- Whirlpool Corporation (incl. Indesit, Maytag, Hotpoint brands where applicable)

- Miele & Cie. KG

- Beko (Arcelik A.S.) / Grundig

- Gorenje (Hisense Europe) / Hisense

- Fisher & Paykel

- ASKO Appliances

- GE Appliances

- Electrolux Professional

- Alliance Laundry Systems (Speed Queen, Huebsch)

- Girbau

- Panasonic

- Vestel (selected OEM/brands)

- Smeg S.p.A.

- Candy Hoover Group S.r.l.

- Midea Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Efficiency mandates and labeling accelerate heat-pump adoption

- 4.2.2 Utility rebates and incentives shorten payback

- 4.2.3 Urban multifamily housing constraints favor ventless dryers

- 4.2.4 OEM innovation improves cycle time, noise, and reliability

- 4.2.5 Premium-to-mid price migration expands addressable base

- 4.2.6 Commercial laundry electrification and ESG targets

- 4.3 Market Restraints

- 4.3.1 Higher upfront price versus vented/condenser units

- 4.3.2 Longer average cycle times in certain conditions

- 4.3.3 Refrigerant transition (R290) adds redesign/certification burden

- 4.3.4 Electrical capacity limits in older buildings slow retrofits

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

- 4.6 Insights Into The Latest Trends And Innovations in the Industry

- 4.7 Insights On Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, Etc.) In The Industry

- 4.8 Insights on Regulatory Framework and Energy-Efficiency Standards in Key Geographies

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Condenser Heat Pump Dryers

- 5.1.2 Vented Heat Pump Dryers

- 5.1.3 Integrated (Built-in) Heat Pump Dryers

- 5.2 By Capacity

- 5.2.1 <= 8 kg

- 5.2.2 9-10 kg

- 5.2.3 >= 11 kg

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial (Laundromats, Hospitality, Healthcare, Multi-housing)

- 5.3.3 Industrial (Light-Duty Laundry/Process Where Applicable)

- 5.4 By Distribution Channel

- 5.4.1 B2C/Retail Channels

- 5.4.1.1 Multi-brand Stores

- 5.4.1.2 Exclusive Brand Outlets

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B/Direct Sales

- 5.4.1 B2C/Retail Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East And Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 BSH Hausgerate GmbH (Bosch, Siemens)

- 6.4.2 Electrolux Group (Electrolux, AEG, Zanussi)

- 6.4.3 Haier Smart Home (Haier, Candy, Hoover, GE Appliances)

- 6.4.4 LG Electronics

- 6.4.5 Samsung Electronics

- 6.4.6 Whirlpool Corporation (incl. Indesit, Maytag, Hotpoint brands where applicable)

- 6.4.7 Miele & Cie. KG

- 6.4.8 Beko (Arcelik A.S.) / Grundig

- 6.4.9 Gorenje (Hisense Europe) / Hisense

- 6.4.10 Fisher & Paykel

- 6.4.11 ASKO Appliances

- 6.4.12 GE Appliances

- 6.4.13 Electrolux Professional

- 6.4.14 Alliance Laundry Systems (Speed Queen, Huebsch)

- 6.4.15 Girbau

- 6.4.16 Panasonic

- 6.4.17 Vestel (selected OEM/brands)

- 6.4.18 Smeg S.p.A.

- 6.4.19 Candy Hoover Group S.r.l.

- 6.4.20 Midea Group

7 Market Opportunities & Future Outlook

- 7.1 120V compact heat-pump dryers for North American retrofits (no panel upgrade)

- 7.2 Commercial heat-pump retrofits in multi-housing and hospitality with utility co-financing

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測 德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)