|

市場調查報告書

商品編碼

2061797

馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Malaysia Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

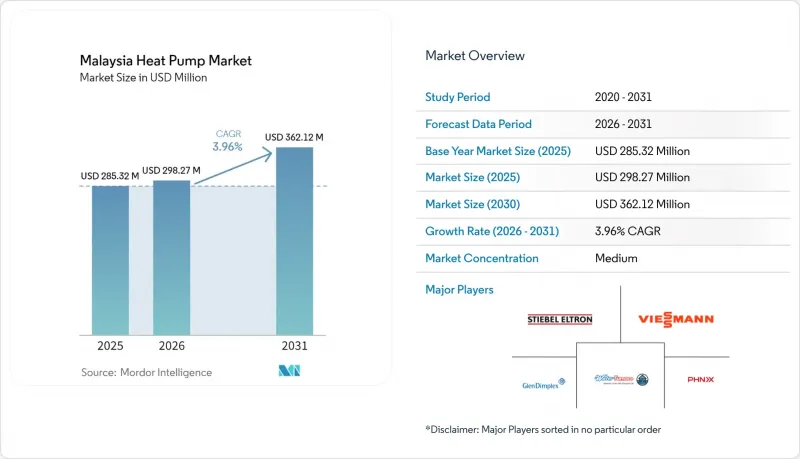

根據 Mordor Intelligence 預測,馬來西亞熱泵市場規模將從 2025 年的 2.8532 億美元和 2026 年的 2.9827 億美元成長到 2031 年的 3.6212 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 3.96%。

本報告依供熱來源(空氣源、水源等)、技術(空氣-空氣、空氣-水等)、容量(小於10kW、10-50kW等)、應用(空間供暖、工業/製程供暖等)、最終用戶(住宅、商業等)、安裝類型(新建、維修)和地區進行細分。市場預測以美元計價。

馬來西亞熱泵市場趨勢與洞察

熱帶地區熱泵熱水器的快速普及

在環境溫度超過 26 度C的情況下,空氣源熱泵熱水器的性能係數 (COP) 可超過 4.0,與電阻式熱水器相比,節能高達 60-75%。現場測試表明,天然冷媒熱水器具有明顯的效率優勢,例如 Rheem 的 RHP-5207C 的 COP 為 4.2,Summer A-TEC 的 R290 型號的 COP 為 4.45。飯店和醫院的營運預算中有 15-20% 用於熱水,因此正在加快維修專案。例如,Carrier Malaysia 與 Pelaburan Hartanah Berhad 簽訂了為期五年的契約,負責在全國範圍內維修24 棟建築。雖然住宅用戶對價格仍然比較敏感,但一項 1500 萬美元的聯邦補貼計劃以及計劃於 2026 年實施的家用電器能源效率標準,將把投資回收期縮短至四年以內,從而擴大獨棟住宅的潛在用戶群體。

綠色技術定序計畫3.0的實施

綠色技術定序計畫3.0透過提供2%的利息補貼和高達1億馬幣(約2400萬美元)貸款的60%聯邦擔保,降低了大規模商業熱泵項目的資本成本。 2025年10月,檳城透過其州級氣候變遷減緩基金擴展了這一理念,實現了混合融資,使專案的內部收益率提高了150至200個基點。 10至12年的長期貸款期限使得折舊計劃能夠與設備生命週期相匹配,從而促進了地熱能和大容量裝置的採用。這項資金籌措框架正在加速製造業、旅館業和醫療保健綜合體採用集中式冷卻器機組熱泵系統,降低了馬來西亞熱泵市場對開發商財務實力的依賴程度。

地熱系統初始資本投入高

一套50kW的地熱系統安裝成本在15萬至40萬馬來西亞馬幣(約3.6萬至9.7萬美元)之間,是同等規模空氣源地熱系統成本的兩倍多。熱帶土壤的熱傳導率約為1.1 W·m⁻¹· 度C,比溫帶地區的基準值低30%至40%,這需要建造規模龐大的鑽孔陣列,從而增加成本並將投資回收期延長至10至15年。全年冷氣負載會提高地溫,除非加裝混合式餘熱場,否則會降低長期效率,但加裝餘熱場又會進一步增加資本投入。因此,目前地熱系統僅限於大學校園和津貼的先導計畫,限制了馬來西亞熱泵市場這一領域的成長。

細分市場分析

2025年,空氣源熱泵機組佔馬來西亞熱泵市場的47.83%。這反映了該細分市場資本密集度低、面積小,且易於整合到人口密集都市區建築的分離式空調系統中。混合式配置(將空氣源蒸發器與地下或水循環系統中的廢熱相結合)預計到2031年將以4.82%的複合年成長率成長,其成長動力主要來自工業運營商和超大規模資料中心建設者,他們需要在季風季節濕度急劇上升的情況下穩定性能係數(COP)。此外,這種混合式方案還具有三大優勢:減少除霜循環造成的能量損失、延長壓縮機壽命以及緩解用電高峰,符合目前面臨分時電價的設施業主的需求。

系統整合商正擴大提供模組化冷卻器、液體冷卻器以及監控系統套裝,使設施管理人員能夠即時切換空氣循環和地下循環。柔佛州的一家資料中心設計公司採用了雙路徑冷卻系統,以確保室外盤管的維護不會影響機架的運作。檳城的一個工業園區借鑒了這種模式,利用共用的地下鑽孔來降低工廠的蒸氣成本,同時在停機期間保持空氣源的冗餘。隨著電力監管機構發布更嚴格的季節性能源效率指標,混合式冷卻方案預計將逐步蠶食目前占主導地位的空氣源冷卻方案的市場佔有率,並擴大其在馬來西亞關鍵工藝設施熱泵市場的滲透率。

截至2025年,空氣源熱泵技術將佔馬來西亞熱泵市場規模的40.31%。這主要得益於其易於安裝和無管道的柔軟性,而這些優勢深受住宅和小規模商業設施買家的青睞。地熱水系統預計將以4.39%的複合年成長率成長至2031年,其成長動力主要來自製造商對現有設備進行改造,加裝封閉回路型熱交換器用於預熱鍋爐給水和提供低品位工藝熱。採用R290和R32天然冷媒的機組將有助於工業用戶應對2027年R22的停用,同時減少範圍1的排放。

工業園區現在透過在場地準備階段安裝鑽孔管道並將鑽井成本分攤給多個租戶,來縮短專案投資回收期。棕櫚油煉製產業的先驅正在使用地熱-水模組將冷凝水溫度從50°C提高到80°C,在不重新設計現有蒸氣總管的情況下降低了天然氣消耗。同時,連鎖飯店正在使用空氣-水一體式系統來滿足熱水需求,其能源效率比(COP)超過4.0,取代了先前消耗其營運預算15-20%的電阻式電加熱器。隨著壓縮機和板式熱交換器本地化生產的擴大,技術選擇將越來越取決於設施獨特的熱工特性,而不是進口前置作業時間,這很可能使「地熱-水」系統成為主流選擇。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 熱泵熱水器在熱帶氣候地區的普及

- 綠色技術定序計畫3.0的實施

- 不斷上漲的電費正在加速向高效節能型空調系統的過渡。

- 2027年逐步淘汰R22冷媒

- 資料中心對精密冷卻的需求日益成長

- 獲得淨零能耗建築認證的建築數量增加

- 市場限制因素

- 地熱系統的初始投資成本很高

- 克蘭谷以外地區熟練安裝人員短缺

- 政策執行的斷斷續續正在削弱投資者信心。

- 住宅消費者對生命週期節約的認知不足

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按供應來源

- 空氣源

- 水源

- 地熱

- 混合

- 透過技術

- 從空中到空中

- 從空氣到水

- 從水到水

- 從地熱能到水

- 按產能

- 小於10千瓦

- 10~50 kW

- 50~200 kW

- 超過200千瓦

- 透過使用

- 空間暖氣

- 空間冷卻

- 家用和衛生熱水

- 工業和製程加熱

- 其他用途

- 最終用戶

- 住宅

- 商業

- 產業

- 按安裝類型

- 新安裝

- 改裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- NIBE Industrier AB(NIBE Climate Solutions)

- Glen Dimplex Group

- Daikin Industries Ltd.(Heat Pump Division)

- Panasonic Corporation(Heating and Ventilation A/C Malaysia Sdn Bhd)

- Mitsubishi Electric Corporation(Malaysia Branch)

- PHNIX Eco-Energy Solution Ltd.

- Midea Group Co., Ltd.(Malaysia)

- Carrier Global Corporation

- LG Electronics Inc.

- Sanden Holdings Corp.(Heat Pump Div.)

- WaterFurnace International Inc.

- Aermec SpA

- Clivet SpA

- Alpha Innotec GmbH

- Ochsner Warmepumpen GmbH

- Heliotherm Warmepumpentechnik GmbH

- MasterTherm CZ sro

第7章 市場機會與未來展望

According to Mordor Intelligence, the malaysia heat pump market size is projected to expand from USD 285.32 million in 2025 and USD 298.27 million in 2026 to USD 362.12 million by 2031, registering a CAGR of 3.96% between 2026 to 2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Industrial and Process Heating, and More), End User (Residential, Commercial, and More), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Malaysia Heat Pump Market Trends and Insights

Surging Adoption of Heat Pump Water Heaters in Tropical Climates

High ambient temperatures above 26 °C enable air-source heat-pump water heaters to deliver coefficients of performance exceeding 4.0, translating into 60-75% electricity savings compared with resistance heaters. Field trials showed Rheem's RHP-5207C at 4.2 COP and Summer A-TEC's R290 model at 4.45 COP, demonstrating a clear efficiency edge for natural-refrigerant units. Hotels and hospitals, which devote 15-20% of operating budgets to hot water, are accelerating retrofits, as evidenced by Carrier Malaysia's five-year agreement with Pelaburan Hartanah Berhad to upgrade 24 buildings nationwide. Residential uptake remains price sensitive, but a USD 15 million federal rebate pool and planned 2026 appliance efficiency standards shorten payback periods to below 4 years, widening the addressable base for landed homes.

Implementation of Green Technology Financing Scheme 3.0

Green Technology Financing Scheme 3.0 offers a 2% interest subsidy and a 60% federal guarantee on loans up to MLR 100 million (USD 24 million), trimming capital costs for large commercial heat-pump projects. Penang extended the concept with a state-level Climate Mitigation Fund in October 2025, unlocking blended finance that improves project internal rates of return by 150-200 basis points. Longer loan tenors of 10-12 years now align amortization schedules with equipment lifecycles, encouraging ground-source and high-capacity installations. The funding framework is accelerating rollout of centralized chiller-heat-pump plants in manufacturing, hospitality, and healthcare complexes, making Malaysia heat pump market adoption less dependent on developer balance-sheet strength.

High Upfront Capital Expenditure for Ground-Source Systems

Ground-source installations cost MLR 150,000-400,000 (USD 36,000-97,000) for a 50 kW system, more than double an equivalent air-source setup. Tropical soils have thermal conductivity around 1.1 W*m-1*°C-1, 30-40% below temperate benchmarks, forcing oversized borehole arrays that inflate costs and extend payback to 10-15 years. Year-round cooling loads raise ground temperatures, eroding long-term efficiency unless hybrid rejection fields are added, which further boosts capital outlay. As a result, only institutional campuses and grant-backed pilot projects currently opt for ground-source designs, limiting this slice of Malaysia heat pump market growth.

Other drivers and restraints analyzed in the detailed report include:

- Rising Electricity Tariffs Driving Shift to High-Efficiency HVAC

- Mandated Phase-Out of R22 Refrigerant in 2027

- Limited Skilled Installers Outside Klang Valley

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-source units captured 47.83% of Malaysia heat pump market share in 2025, reflecting the segment's lower capital intensity, small physical footprint, and ability to slot into split-system infrastructure in dense urban buildings. Hybrid configurations that marry air-source evaporators with ground- or water-loop heat rejection are projected to grow at a 4.82% CAGR through 2031, driven by industrial operators and hyperscale data-center builders that need to stabilize coefficients of performance during monsoon humidity spikes. The hybrid approach also cuts defrost-cycle energy penalties, extends compressor life, and eases grid-demand peaks, a trio of benefits that resonates with owners now facing time-of-use tariffs.

System integrators increasingly bundle modular chillers, liquid coolers, and supervisory controls so facility managers can toggle between air and ground loops in real time. Data-center designers in Johor specify dual-path cooling trains so that maintenance on outdoor coils never jeopardizes rack uptime. Industrial estates in Penang replicate the template by tapping shared bore-fields to trim plant steam bills while retaining air-source redundancy for shutdown periods. As grid regulators publish stricter seasonal-efficiency indices, the hybrid cohort is expected to chip away at the dominant air-source position, broadening Malaysia heat pump market penetration across process-critical facilities.

Air-to-air technology accounted for 40.31% of Malaysia heat pump market size in 2025 because residential and light-commercial buyers prize easy installation and ductless flexibility. Ground-to-water systems are forecast to advance at a 4.39% CAGR to 2031 as manufacturers retrofit closed-loop heat exchangers that pre-heat boiler feedwater or supply low-grade process heat. Natural-refrigerant units using R290 or R32 help industrial users hedge against the 2027 R22 ban while unlocking Scope-1 emission cuts.

Industrial parks now rough-in bore-fields during site grading, spreading drilling costs across multiple tenants and shortening project payback windows. Early adopters in palm-oil refining use ground-to-water modules to lift condensate from 50 °C to 80 °C, trimming natural-gas use without re-engineering existing steam headers. Hotel chains, meanwhile, lean on air-to-water packages to meet hot-water loads at COPs above 4.0, replacing electric resistance heaters that once soaked up 15-20% of operating budgets. As local production of compressors and plate heat exchangers expands, technology choice will hinge less on import lead times and more on plant-specific thermal profiles, cementing ground-to-water as a mainstream option.

List of Companies Covered in this Report:

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- NIBE Industrier AB (NIBE Climate Solutions)

- Glen Dimplex Group

- Daikin Industries Ltd. (Heat Pump Division)

- Panasonic Corporation (Heating and Ventilation A/C Malaysia Sdn Bhd)

- Mitsubishi Electric Corporation (Malaysia Branch)

- PHNIX Eco-Energy Solution Ltd.

- Midea Group Co., Ltd. (Malaysia)

- Carrier Global Corporation

- LG Electronics Inc.

- Sanden Holdings Corp. (Heat Pump Div.)

- WaterFurnace International Inc.

- Aermec S.p.A.

- Clivet SpA

- Alpha Innotec GmbH

- Ochsner Warmepumpen GmbH

- Heliotherm Warmepumpentechnik GmbH

- MasterTherm CZ s.r.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Heat Pump Water Heaters in Tropical Climates

- 4.2.2 Implementation of the Green Technology Financing Scheme 3.0

- 4.2.3 Rising Electricity Tariffs Driving Shift to High-Efficiency HVAC

- 4.2.4 Mandated Phase-Out of R22 Refrigerant in 2027

- 4.2.5 Growing Demand from Data Centers for Precision Cooling

- 4.2.6 Increase in Net-Zero Building Certifications

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure for Ground-Source Systems

- 4.3.2 Limited Skilled Installers Outside Klang Valley

- 4.3.3 Intermittent Policy Enforcement Reducing Investor Confidence

- 4.3.4 Low Awareness Among Residential Consumers of Lifecycle Savings

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Stiebel Eltron GmbH & Co. KG

- 6.4.2 Vaillant Group

- 6.4.3 Viessmann Climate Solutions SE

- 6.4.4 NIBE Industrier AB (NIBE Climate Solutions)

- 6.4.5 Glen Dimplex Group

- 6.4.6 Daikin Industries Ltd. (Heat Pump Division)

- 6.4.7 Panasonic Corporation (Heating and Ventilation A/C Malaysia Sdn Bhd)

- 6.4.8 Mitsubishi Electric Corporation (Malaysia Branch)

- 6.4.9 PHNIX Eco-Energy Solution Ltd.

- 6.4.10 Midea Group Co., Ltd. (Malaysia)

- 6.4.11 Carrier Global Corporation

- 6.4.12 LG Electronics Inc.

- 6.4.13 Sanden Holdings Corp. (Heat Pump Div.)

- 6.4.14 WaterFurnace International Inc.

- 6.4.15 Aermec S.p.A.

- 6.4.16 Clivet SpA

- 6.4.17 Alpha Innotec GmbH

- 6.4.18 Ochsner Warmepumpen GmbH

- 6.4.19 Heliotherm Warmepumpentechnik GmbH

- 6.4.20 MasterTherm CZ s.r.o.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)