|

市場調查報告書

商品編碼

2061798

菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Philippines Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

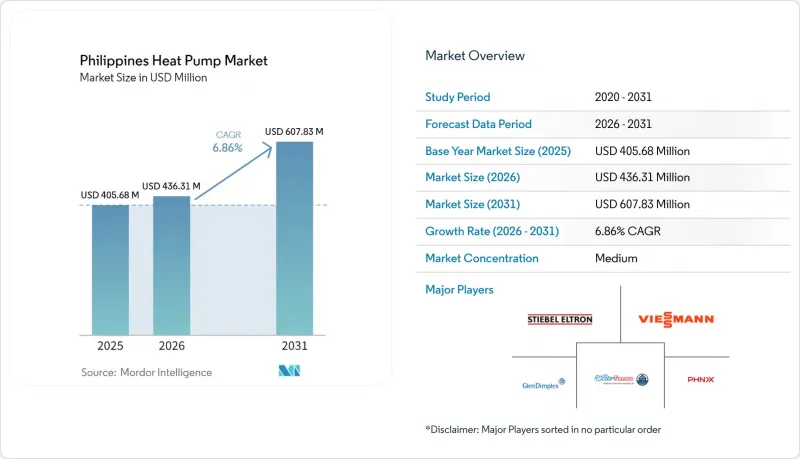

根據 Mordor Intelligence 預測,菲律賓熱泵市場規模將從 2025 年的 4.0568 億美元和 2026 年的 4.3631 億美元成長到 2031 年的 6.0783 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.86%。

本報告按供熱來源(空氣源、水源等)、技術(空氣-空氣、空氣-水等)、容量(小於10kW、10-50kW等)、應用(空間供暖、工業/工藝供暖等)、最終用戶(住宅、商業等)、安裝類型(新安裝等)和地區進行細分。市場預測以美元計價。

菲律賓熱泵市場趨勢與洞察

將熱泵的應用範圍擴展到傳統暖氣、通風和空調(HVAC)應用之外。

在大規模低溫運輸設施中,工業熱泵被用於維持從冰淇淋所需的-25 度C到香蕉催熟所需的13 度C等各種溫度,這表明其應用已超越製冷範疇,拓展至提升舒適度領域。位於棉蘭老島的一座容量為11,728個托盤的倉庫於2026年3月投入運作,該倉庫透過其「綠色能源選擇計畫」整合了可再生能源,展現了該技術在高能耗物流運營中的潛力。像克拉克公園飯店這樣的飯店設施透過實施集中管理系統,每年可節省24萬千瓦時的能源,這充分體現了降低飯店營運成本的優勢。經濟特區內的承包工程廠房開發商正在將熱泵作為標準公用設施基礎設施,以吸引出口製造商。隨著應用範圍的不斷擴大,菲律賓熱泵市場正從單一用途產品線轉型為跨產業解決方案。

政府對使用可再生能源供暖的獎勵的實施

一份關於「永續綠色工業園區」的合作備忘錄為安裝節能設備的工廠提供稅收優惠和關稅豁免,這立即促使投資決策轉向熱泵。能源部於2025年啟動的關於更嚴格的最低能源效率標準的諮詢表明,住宅和商用熱水器很快將面臨強制性的最低能源效率標準。雖然目前沒有直接向消費者提供補貼,但「綠色能源選擇計畫」正在降低高負載用戶的電力供應成本,並縮小與液化石油氣(LPG)熱水器的價格差距。菲律賓綠色建築委員會正在努力製定修訂後的《國家建築標準法》,該法案將強制要求在10層或以上的中高層建築項目中安裝集中式熱泵熱水器,從而有效地使未來大多數公寓大樓強制採用這項技術。總而言之,這些政策為菲律賓熱泵市場提供了可預測的需求前景,使本地經銷商和跨國製造商都從中受益。

前期投入成本高,資金籌措管道有限。

住宅熱泵熱水器的價格從每千台55,000菲律賓披索(約980,000美元)到232,500菲律賓披索(約4,130,000美元)不等,相當於家庭收入中位數的3到12個月,對於絕大多數沒有信貸支持的住宅來說,難以負擔。 Stiebel Eltron的產品比本地品牌貴30%到40%,這使得只有高所得者才能購買。銀行很少向屋主提供綠色技術貸款,因此現金購買是常態,這減緩了菲律賓熱泵市場的成長速度。同時,商業和工業用戶可以透過稅收優惠來抵消成本,進一步擴大了不同細分市場之間的價格差距。在優惠貸款和退稅計畫訂定之前,預計住宅領域的普及率將落後於整體市場的成長速度。

細分市場分析

儘管混合式系統在2025年僅佔很小的市場佔有率,但預計到2031年將以每年7.61%的速度成長,比菲律賓整體熱泵市場高出75個基點。這主要得益於島嶼度假村和農業工業園區為應對每千瓦時16-25披索(0.29-0.45美元)的電費而採取的措施。空氣源熱泵平台憑藉其較低的初始成本和與馬尼拉大都會電力基礎設施的兼容性,將在2025年佔據47.36%的需求佔有率。水源熱泵解決方案正應用於沿海度假村,穩定的進水溫度使其能源效率高於性能係數(COP),但授權流程延長了專案週期。地熱能的應用主要集中在政府主導的旗艦計畫中,例如2025年12月在首都大學醫學中心實施的900千瓦地熱連接計畫。

製造商目前正部署模組化產品線,透過根據現貨電價在空氣源熱泵和太陽能熱泵模式之間切換,最佳化產品全生命週期的能源成本。 LG 在宿霧展示的「Multi V Water 5」機組,其變頻器頻率範圍寬廣,為 20–150 Hz,提高了部分負載下的效率。在菲律賓熱泵市場,空氣源熱泵在住宅領域佔據主導地位,但盈利在高溫高峰期往往會下降。混合式和水基系統可以彌補這一性能差距,但其設計複雜性較高,因此僅適用於技術監管完善的專案。

到2025年,空氣源熱泵將佔菲律賓熱泵市場佔有率的40.14%,這主要是由於公寓開發商傾向於集中式熱水管道系統。地源熱泵技術正以每年7.38%的速度成長,充分利用呂宋島的地熱資源,First Gen公司在呂宋島營運1870兆瓦的裝置容量。空氣源熱泵在住宅分離式空調的替換循環中需求旺盛,在氣候涼爽的高海拔都市區,其價格溢價高達15-20%。水源熱泵目前仍主要應用於需要嚴格溫度控制的工業製程循環。

大金的「MARUTTO」平台整合了變冷劑流量(VRF)系統、熱水供應和建築管理功能,可將資料中心的廢熱回收利用,供鄰近住宅使用。雖然地下循環系統的安裝成本為每千瓦8,000至12,000菲律賓披索(約合143至214美元),會延長專案工期,但其20-25%的季節能源效率提升足以抵銷15年資產計畫中的資本投資成本。因此,儘管空氣-水循環系統在新建築中較為普遍,但對於自用型設施,為了降低長期營運成本,通常會採用地下循環系統。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 將熱泵的應用範圍擴展到傳統暖通空調應用之外

- 政府對使用可再生能源供暖的獎勵的實施

- 快速的都市化和中層住宅的蓬勃發展

- 全國逐步淘汰高全球暖化潛值冷媒

- 經濟特區工業製程加熱電氣化

- 大量離網旅遊度假村開始安裝熱泵系統。

- 市場限制因素

- 前期實施成本高,且資金籌措管道有限。

- 持證熱泵技術人員短缺

- 農村島嶼地區輸電網路的不穩定性

- 售後服務生態系分散

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按供應來源

- 空氣源

- 水源

- 地熱

- 混合

- 透過技術

- 從空中到空中

- 從空氣到水

- 水到水

- 從地熱能到水

- 按產能

- 小於10千瓦

- 10~50 kW

- 50~200 kW

- 超過200千瓦

- 透過使用

- 空間暖氣

- 空調

- 家用和衛生熱水

- 工業和製程加熱

- 其他用途

- 最終用戶

- 住宅

- 商業

- 產業

- 按安裝類型

- 新安裝

- 改裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Mitsubishi Electric Corp.

- Daikin Industries Ltd.

- Panasonic Holdings Corp.

- LG Electronics Inc.

- Samsung Electronics Co. Ltd.

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- NIBE Industrier AB

- Glen Dimplex Group

- PHNIX Eco-Energy Solution Ltd.

- Haier Group

- Enertech Global LLC

- Ecoforest Geotermia SL

- Alpha Innotec GmbH

- TCL Corporation

- Grundfos Holding A/S

- MasterTherm CZ sro

- Clade Engineering Systems Ltd.

- Calorex Heat Pumps Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the philippines heat pump market size is projected to expand from USD 405.68 million in 2025 and USD 436.31 million in 2026 to USD 607.83 million by 2031, registering a CAGR of 6.86% between 2026 to 2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Industrial and Process Heating, and More), End User (Residential, Commercial, and More), Installation (New Installation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Philippines Heat Pump Market Trends and Insights

Growing Use of Heat Pumps Beyond Traditional Heating, Ventilation, and Air Conditioning Applications

Large cold-chain facilities are specifying industrial-scale heat pumps to maintain temperatures that range from -25 °C for ice cream to 13 °C for banana ripening, underpinning diversification away from comfort cooling. The 11,728-pallet Mindanao warehouse commissioned in March 2026 integrates renewable power through the Green Energy Option Program, proving out the technology in energy-intensive logistics operations. Hospitality properties such as Park Inn Clark realized 240,000 kWh in annual savings after adopting centralized systems, which validates the operating-expense upside for hotels. Developers of turnkey factory shells inside special economic zones now embed heat pumps as standard utility infrastructure to lure export manufacturers. This widening usage spectrum positions the Philippines heat pump market as a cross-sector solution rather than a single-application product line.

Implementation of Government Incentives for Renewable Heating

The memorandum of understanding on Sustainable Green Industrial Parks grants tax holidays and duty exemptions when factories install energy-efficient equipment, immediately tilting capital-spending decisions toward heat pumps. The Department of Energy consultation on stricter minimum energy performance standards, started in 2025, signals that residential and commercial water heaters will soon face mandatory efficiency floors. Although direct consumer rebates are absent, the Green Energy Option Program lowers the delivered cost of power for high-load users, narrowing the price gap with liquefied petroleum gas heaters. The Philippine Green Building Council is lobbying for a revised National Building Code that will require centralized heat pump water heaters in mid-rise projects above 10 floors, effectively mandating the technology for most future condominiums. Taken together, the policy stack offers predictable demand visibility that benefits both local distributors and multinational manufacturers in the Philippines heat pump market.

High Up-Front Installation Cost and Limited Financing

Residential heat pump water heaters range from PHP 55,000 (USD 0.98 million per 1,000 units) to PHP 232,500 (USD 4.13 million per 1,000 units), equal to three to twelve months of median household income and thus out of reach for most families without credit support. Stiebel Eltron units sell at 30-40% above local brands, confining them to upper-income buyers. Banks rarely issue green-technology loans to homeowners, so cash purchases dominate, slowing velocity in the Philippines heat pump market. Commercial and industrial buyers offset costs through tax breaks, widening the affordability gap between segments. Until concessional lending or rebate schemes emerge, residential adoption will underperform the headline market growth.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Urbanization and Mid-Rise Residential Boom

- Nationwide Phase-Out of High Global Warming Potential Refrigerants

- Shortage of Certified Heat Pump Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid systems captured a marginal share in 2025 but are forecast to grow at 7.61% annually through 2031, outperforming the Philippines heat pump market by 75 basis points as island resorts and agro-industrial parks seek resilience against tariffs of PHP 16-25 (USD 0.29-0.45) per kWh. Air source platforms provide 47.36% of 2025 demand by leveraging lower first cost and compatibility with Metro Manila electrical infrastructure. Water source solutions serve coastal resorts where inlet temperatures stabilize efficiency above a 4.0 coefficient of performance, though permitting hurdles lengthen project cycles. Ground source adoption concentrates in institutional flagship projects like the December 2025 900 kW geothermal tie-in at Capitol University Medical Center.

Manufacturers now roll out modular lines that toggle between air-source and solar-thermal modes based on spot-market power pricing, optimizing lifetime energy spend. LG's Multi V Water 5 unit, demonstrated in Cebu, features a wide 20-150 Hz inverter range, widening partial-load efficiency. Air source heat pumps dominate the residential slice of the Philippines heat pump market size equation but face diminishing returns during peak-temperature months. Hybrid and water-based systems fill that performance gap, although higher engineering complexity restricts uptake to projects with sound technical oversight.

Air-to-water units held 40.14% of the Philippines heat pump market share in 2025, mainly due to condominium developers favoring centralized domestic hot water risers. Ground-to-water technology will advance by 7.38% a year, tapping Luzon's geothermal belt where First Gen operates 1,870 MW of capacity. Air-to-air models play in the residential split-type upgrade cycle, commanding 15-20% price premiums in cooler upland cities. Water-to-water remains confined to industrial process loops requiring tight temperature control.

Daikin's MARUTTO platform integrates variable refrigerant flow, water heating and building management to recycle data-center waste heat into adjacent residences. Installation cost for bore-hole loops ranges from PHP 8,000-12,000 (USD 143-214) per kW and elongates project timelines, but 20-25% higher seasonal efficiency offsets capex in 15-year asset plans. Air-to-water designs therefore dominate new builds, while ground-to-water wins in owner-occupied facilities committing to long-range operating savings.

List of Companies Covered in this Report:

- Mitsubishi Electric Corp.

- Daikin Industries Ltd.

- Panasonic Holdings Corp.

- LG Electronics Inc.

- Samsung Electronics Co. Ltd.

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- NIBE Industrier AB

- Glen Dimplex Group

- PHNIX Eco-Energy Solution Ltd.

- Haier Group

- Enertech Global LLC

- Ecoforest Geotermia S.L.

- Alpha Innotec GmbH

- TCL Corporation

- Grundfos Holding A/S

- MasterTherm CZ s.r.o.

- Clade Engineering Systems Ltd.

- Calorex Heat Pumps Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Use of Heat Pumps Beyond Traditional HVAC Applications

- 4.2.2 Implementation of Government Incentives for Renewable Heating

- 4.2.3 Rapid Urbanization and Mid-Rise Residential Boom

- 4.2.4 Nationwide Phase-Out of High-GWP Refrigerants

- 4.2.5 Electrification of Industrial Process Heating in SEZs

- 4.2.6 Surge in Off-Grid Tourism Resorts Adopting Heat Pump Systems

- 4.3 Market Restraints

- 4.3.1 High Up-Front Installation Cost and Limited Financing

- 4.3.2 Shortage of Certified Heat-Pump Technicians

- 4.3.3 Grid Instability in Rural Islands

- 4.3.4 Fragmented After-Sales Service Ecosystem

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mitsubishi Electric Corp.

- 6.4.2 Daikin Industries Ltd.

- 6.4.3 Panasonic Holdings Corp.

- 6.4.4 LG Electronics Inc.

- 6.4.5 Samsung Electronics Co. Ltd.

- 6.4.6 Stiebel Eltron GmbH & Co. KG

- 6.4.7 Vaillant Group

- 6.4.8 Viessmann Climate Solutions SE

- 6.4.9 NIBE Industrier AB

- 6.4.10 Glen Dimplex Group

- 6.4.11 PHNIX Eco-Energy Solution Ltd.

- 6.4.12 Haier Group

- 6.4.13 Enertech Global LLC

- 6.4.14 Ecoforest Geotermia S.L.

- 6.4.15 Alpha Innotec GmbH

- 6.4.16 TCL Corporation

- 6.4.17 Grundfos Holding A/S

- 6.4.18 MasterTherm CZ s.r.o.

- 6.4.19 Clade Engineering Systems Ltd.

- 6.4.20 Calorex Heat Pumps Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)