|

市場調查報告書

商品編碼

2061794

德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Germany Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

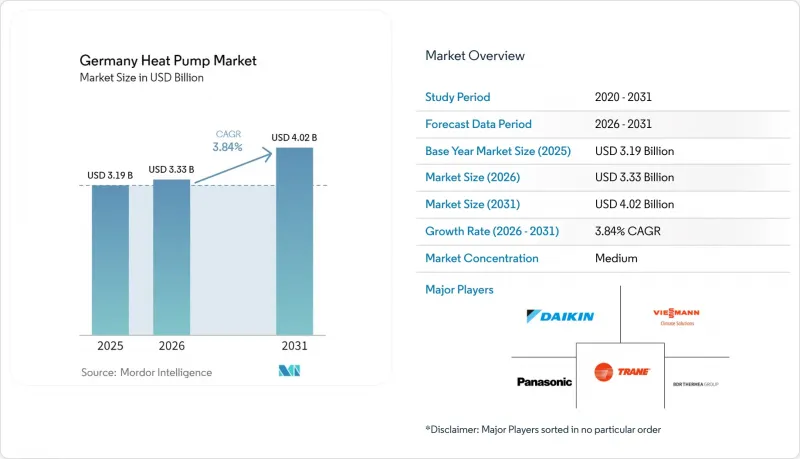

根據 Mordor Intelligence 預測,德國熱泵市場預計將從 2025 年的 31.9 億美元成長到 2026 年的 33.3 億美元,到 2031 年達到 40.2 億美元,2026 年至 2031 年的複合年成長率預計為 3.84%。

本報告按熱源類型(空氣源、水源等)、技術(空氣-空氣、空氣-水等)、容量(小於10kW、10-50kW等)、應用(空間供暖、工業/工藝供暖等)、最終用戶(住宅、商業設施等)、安裝類型(新建、維修)和地區進行分類。市場預測以美元計價。

德國熱泵市場趨勢與洞察

全面的聯邦和州補貼及稅額扣抵計劃

德國的BEG計畫在2025年提供了38億歐元(43億美元)的熱泵補貼,補貼範圍涵蓋參與家庭合格的費用的70%。投資回收期縮短至4-6年,成本優勢也顯著優於燃氣鍋爐。巴登-符騰堡州和巴伐利亞州的額外補貼進一步提升了地熱和區域供熱系統的經濟可行性。將獎勵與建築外圍護結構維修和屋頂太陽能發電相結合,每個項目的總總合額可能超過5萬歐元(5.65萬美元),如此高的補貼額度催生了一個利基市場,即專門協助客戶應對複雜核准流程的諮詢公司。儘管行政核准流程仍存在一些摩擦,但這項津貼計畫的規模和持續時間為未來十年支撐市場需求奠定了基礎。

對高效供暖和製冷系統的需求不斷成長。

適應氣候變遷如今已成為重要的購買動機。預計到2026年,冷暖一體機將佔住宅安裝量的38%,高於兩年前的22%。在南部各州,高溫天氣頻繁,氣溫超過攝氏35度,因此季節能源效率係數(SPF)為4.5或更高的空氣源熱泵機型更受青睞。商業用戶則傾向於選擇變速壓縮機,這種壓縮機能夠實現更精確的區域控制,同時將尖峰負載降低近30%。與傳統的R410A系統相比,丙烷系統能源效率提升8-12%,並符合ESG評估標準。隨著生態設計標準於2027年生效,這些性能提升將成為監管規定的最低要求。

嚴格的氟化氣體和安全合規要求

隨著全球暖化潛勢(GWP)超過150的冷媒禁令將於2027年到期,轉向使用被歸類為高度易燃的丙烷勢在必行。這將導致每台設備額外增加300至500歐元(339至565美元)的成本,用於遵循成本安全要求和安裝人員認證。小規模原始設備製造商(OEM)缺乏快速重新設計的技術能力,迫使它們進行合併和退出市場,從而縮小了消費者的選擇範圍。德國職業安全機構正在強制要求進行額外的培訓並安裝洩漏檢測設備,這進一步加劇了安裝人員的應對壓力。隨著生產配額的逐步取消,傳統的R410A和R32系統面臨停產的風險,將抑制短期維修需求。在R290的供應鏈恢復正常之前,合規成本的增加將抑制德國熱泵市場的成長動能。

細分市場分析

在德國熱泵市場,預計到2025年,地源熱泵機組將佔總銷售量的67.78%,憑藉其相對較低的初始成本和簡便的安裝方式(適用於大多數維修項目),繼續保持領先地位。結合地源模組和冷凝燃氣鍋爐的混合系統預計將以每年5.61%的最高成長率運作。這是因為它們既滿足了65%可再生能源供熱利用率的要求,又能幫助用戶規避電費飆升的風險。雖然水源和地源熱泵解決方案目前仍處於小眾市場,但聯邦政府對地源熱泵系統的補貼正在縮小成本差距,並吸引了人口密集地區市政當局的關注,這些地區需要基本負載供熱。

混合系統的發展動能也反映了技術的進步。魏蘭特(Weilandt)的「aroTHERM plus」系統能夠即時調節燃料切換,而大金(Daikin)的系統則將出水溫度提升至70°C,從而無需更換老舊住宅的散熱器。政策制定者正在推動這一趨勢,他們允許雙燃料系統在熱泵滿足全年三分之二負載的情況下獲得全額德國津貼(BEG),這實際上將傳統鍋爐降級為備用設備。因此,儘管純空氣源熱泵機組仍佔據整體出貨量的主導地位,但預計到2031年,混合系統將逐年提升德國熱泵的市場佔有率。

2025年,空氣-水空調系統佔總銷售額的59.31%,這主要得益於成熟的供應鏈和安裝人員的熟悉程度。然而,由於區域供熱供應商將數百棟建築連接到共用鑽井平台,顯著降低了鑽井成本,預計地下水空調系統的年成長率將達到5.02%,高於3.84%的總體平均水平。水-水空調系統在工藝熱和游泳池相關行業佔據了一定的細分市場,而空氣-空氣分離式空調系統則在需要低噪音外牆機組的多用戶住宅維修中越來越受歡迎。

季節性能係數超過 4.0 的地熱系統將獲得額外 5 個百分點的聯邦補貼,最高可補貼計畫成本的 70%。漢堡的 4 兆瓦空氣源熱泵廠和科隆的 150 兆瓦地熱合約便是城市公共產業如何利用各種技術實現現有蒸氣管網脫碳的典範。儘管分階段升級(例如威斯曼 Vitocal 系列的 R290 改進)有助於現有空氣源熱泵製造商維持市場佔有率,但區域供熱管網的長期擴張正推動德國熱泵市場向以地熱為中心的架構轉型。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全面的聯邦和州補貼及稅額扣抵計劃

- 對高效供暖和製冷系統的需求不斷成長。

- 歐盟的「適合55歲」脫碳目標和電氣化推廣

- 多用戶住宅維修對低噪音空氣源熱泵的需求激增。

- 德國輸電系統營運商(TSO)的智慧電網需量反應獎勵

- 歐盟零件近岸外包受供應鏈韌性政策推動

- 市場限制因素

- 對氟氯化碳和安全有嚴格的合規要求。

- 持證安裝人員及暖通空調技術人員短缺

- 本地配電網路壅塞

- 丙烷(R290)冷媒供應瓶頸

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按供應來源

- 空氣源

- 水源

- 地熱

- 混合

- 透過技術

- 空對空

- 空氣中的水

- 水-水

- 來自地下的水(土壤)

- 按產能

- 小於10千瓦

- 10~50 kW

- 50~200 kW

- 超過200千瓦

- 透過使用

- 空間暖氣

- 空間冷卻

- 家用和衛生熱水

- 工業和製程加熱

- 其他用途

- 最終用戶

- 住宅

- 商業

- 產業

- 按安裝類型

- 新安裝

- 改裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Daikin Industries Ltd.

- Viessmann Climate Solutions SE

- Panasonic Holdings Corporation

- Trane Technologies plc

- BDR Thermea Group BV

- Heliotherm GmbH

- Robert Bosch GmbH

- Systemair AB

- Ariston Holding NV

- Alpha Innotec GmbH

- Stiebel Eltron GmbH and Co. KG

- Glen Dimplex GmbH

- Johnson Controls International plc

- Vaillant Group

- Max Weishaupt GmbH

- Wolf GmbH

- Waterkotte GmbH

- Elco GmbH

- Mitsubishi Electric Corporation

- Qvantum Energi AB

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany heat pump market size is expected to increase from USD 3.19 billion in 2025 to USD 3.33 billion in 2026 and reach USD 4.02 billion by 2031, growing at a CAGR of 3.84% over 2026-2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Industrial and Process Heating, and More), End User (Residential, Commercial, and More), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Germany Heat Pump Market Trends and Insights

Robust Federal and State Subsidies, Tax-Credit Schemes

Germany's BEG program disbursed EUR 3.8 billion (USD 4.3 billion) in heat-pump grants during 2025, underwriting up to 70% of eligible costs for qualifying households. Payback periods compressed to four-to-six years, tipping the cost equation decisively away from gas boilers. State top-ups in Baden-Wurttemberg and Bavaria further sweeten the economics for ground-source and district-connected systems. Bundling incentives with building-envelope upgrades and rooftop photovoltaics can push combined subsidies past EUR 50,000 (USD 56,500) per project, a level that has spawned a consultancy niche to navigate the complex approval pipeline Although administrative friction remains, the magnitude and duration of the grant architecture underpin demand through the decade.

Rising Demand for High-Efficiency Heating and Cooling

Climate adaptation is now a mainstream buying trigger: dual-use units capable of cooling captured 38% of residential installs in 2026, up from 22% two years earlier. Southern states enduring heatwaves above 35 °C favor air-to-air models with seasonal performance factors over 4.5. Commercial buyers specify variable-speed compressors that slice peak load by nearly 30% while sharpening zone control. Propane-charged systems add another 8-12% efficiency lift versus R410A predecessors, satisfying ESG scorecards. Impending 2027 Ecodesign thresholds will lock these performance gains into regulatory minimums.

Stringent F-Gas and Safety Compliance Requirements

The 2027 ban on refrigerants with GWP above 150 forces a pivot to propane, classified as highly flammable, adding EUR 300-500 (USD 339-565) per unit in compliance outlays for safety features and installer certifications. Smaller OEMs lack the engineering depth to redesign quickly and are instead merging or exiting, narrowing consumer choice. Germany's occupational-safety authority mandates extra training and leak-detection gear, stretching installer capacity still further. Legacy R410A and R32 systems risk becoming orphaned as production quotas ratchet down, a prospect that dampens near-term retrofit demand. Until supply chains normalize around R290, compliance drag will shave momentum from the Germany heat pump market.

Other drivers and restraints analyzed in the detailed report include:

- EU Fit-for-55 Decarbonization Targets and Electrification Push

- Surge in Low-Noise Air-to-Air Heat Pumps for Multi-Family Retrofits

- Shortage of Certified Installers and HVAC Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-source units produced 67.78% of 2025 revenue in the Germany heat pump market, retaining pole position through a mix of moderate upfront cost and straightforward installation that suits most retrofit projects . Hybrids pairing an air-source module with a condensing gas boiler are forecast to deliver the fastest 5.61% annual growth, because they meet the 65% renewable-heat rule while insulating owners from potential electricity-price spikes. Water-source and ground-source solutions remain niche, yet the federal subsidy bonus for geothermal systems narrows the cost gap and is drawing interest from municipalities that need baseload heat for dense districts.

Hybrid momentum also reflects technological refinements: Vaillant's aroTHERM plus calibrates fuel switching in real time, while Daikin's flow-temperature boost to 70 °C removes the need for radiator changes in older homes. Policymakers amplify the trend by allowing dual-fuel systems to qualify for full BEG grants once the heat pump supplies two-thirds of annual load, effectively pushing legacy boilers into backup status. As a result, hybrids are expected to lift their Germany heat pump market share each year through 2031, even while pure air-source units keep dominating overall shipments.

Air-to-water systems controlled 59.31% of 2025 sales, underpinned by mature supply chains and installer familiarity. Yet ground-to-water units are projected to grow 5.02% per year, faster than the 3.84% aggregate, because drilling costs fall sharply when district-heating operators connect hundreds of buildings to a shared bore-field. Water-to-water designs occupy an industrial niche tied to process heat and swimming pools, whereas air-to-air splits are winning multi-family retrofits that need low-noise facade units.

Federal subsidies add five extra percentage points for geothermal systems that achieve seasonal performance factors above 4.0, bringing total support to as high as 70% of project cost. Hamburg's 4 MW air-source plant and Cologne's 150 MW geothermal contract exemplify how city utilities are scaling diverse technologies to decarbonize legacy steam networks. Incremental upgrades, such as Viessmann's R290 revision of its Vitocal line, help air-to-water incumbents defend share, but the longer-term upswing in district networks tilts incremental Germany heat pump market size toward ground-centric architectures.

List of Companies Covered in this Report:

- Daikin Industries Ltd.

- Viessmann Climate Solutions SE

- Panasonic Holdings Corporation

- Trane Technologies plc

- BDR Thermea Group B.V.

- Heliotherm GmbH

- Robert Bosch GmbH

- Systemair AB

- Ariston Holding N.V.

- Alpha Innotec GmbH

- Stiebel Eltron GmbH and Co. KG

- Glen Dimplex GmbH

- Johnson Controls International plc

- Vaillant Group

- Max Weishaupt GmbH

- Wolf GmbH

- Waterkotte GmbH

- Elco GmbH

- Mitsubishi Electric Corporation

- Qvantum Energi AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust Federal and State Subsidies, Tax-Credit Schemes

- 4.2.2 Rising Demand for High-Efficiency Heating and Cooling

- 4.2.3 EU Fit-for-55 Decarbonization Targets and Electrification Push

- 4.2.4 Surge in Low-Noise Air-to-Air Heat Pumps for Multi-Family Retrofits

- 4.2.5 Smart-Grid Demand-Response Incentives from German TSOs

- 4.2.6 EU Component Near-Shoring Driven by Supply-Chain Resilience Policies

- 4.3 Market Restraints

- 4.3.1 Stringent F-Gas and Safety Compliance Requirements

- 4.3.2 Shortage of Certified Installers and HVAC Technicians

- 4.3.3 Rural Distribution-Grid Congestion

- 4.3.4 Propane (R290) Refrigerant Supply Bottlenecks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries Ltd.

- 6.4.2 Viessmann Climate Solutions SE

- 6.4.3 Panasonic Holdings Corporation

- 6.4.4 Trane Technologies plc

- 6.4.5 BDR Thermea Group B.V.

- 6.4.6 Heliotherm GmbH

- 6.4.7 Robert Bosch GmbH

- 6.4.8 Systemair AB

- 6.4.9 Ariston Holding N.V.

- 6.4.10 Alpha Innotec GmbH

- 6.4.11 Stiebel Eltron GmbH and Co. KG

- 6.4.12 Glen Dimplex GmbH

- 6.4.13 Johnson Controls International plc

- 6.4.14 Vaillant Group

- 6.4.15 Max Weishaupt GmbH

- 6.4.16 Wolf GmbH

- 6.4.17 Waterkotte GmbH

- 6.4.18 Elco GmbH

- 6.4.19 Mitsubishi Electric Corporation

- 6.4.20 Qvantum Energi AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)