|

市場調查報告書

商品編碼

2061795

新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Singapore Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

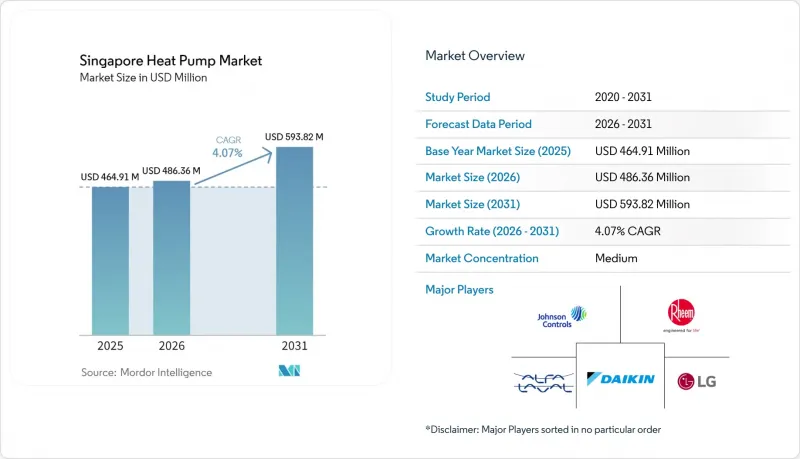

根據 Mordor Intelligence 預測,新加坡熱泵市場規模預計在 2025 年達到 4.6491 億美元,2026 年達到 4.8636 億美元,到 2031 年達到 5.9382 億美元,2026 年至 2031 年的複合年成長率為 4.07%。

本報告按熱源類型(空氣源、水源等)、技術(空氣-空氣、空氣-水等)、容量(小於10kW、10-50kW等)、應用(空間供暖、工業/工藝供暖等)、最終用戶(住宅、商業設施等)、安裝類型(新建、維修)和地區進行分類。市場預測以美元計價。

新加坡熱泵市場趨勢與洞察

「新加坡綠色計畫2030」下公共部門維修津貼激增

政府已撥款6300萬新元(約4700萬美元)用於“現有建築節能津貼2.0”,以幫助商業和市政業主升級其暖通空調系統,並將申請資格延長至2027年3月。津貼的項目將優先考慮包含熱泵、建築管理軟體和冷卻器更換的綜合方案,提供承包維修的供應商將獲得優先考慮。由於符合資格的占地面積集中在中央商務區(CBD)和新興的多極樞紐地區,在這些地區擁有良好業績記錄的承包商正優先獲得訂單。業主也優先考慮能夠順利完成綠色建築認證申請和能源性能檢驗,並滿足補貼資格要求的合作夥伴。由於供應商擁有多年的訂單儲備,為期三年的實施期加劇了對大容量空氣源熱泵機組的競爭。

強制性能源標籤將促進高效率熱泵的發展。

韓國國家環境局自2025年4月1日起推出五級能源效率等級標籤,並規範熱水器的能源效率測試。熱泵熱水器通常能達到四級或五級能源效率等級,而傳統電阻式電熱水器很少能達到兩級能源效率等級,這引導消費者選擇更高能源效率的產品。製造商必須在銷售前向該機構註冊其產品型號,這為沒有認證測試實驗室的小規模品牌設定了准入門檻。透明的標籤檢視強調了產品在整個生命週期內的成本節約,縮小了先前阻礙高投入熱泵熱水器銷售的資訊鴻溝。因此,經銷商報告稱,在4月截止日期前,訂單模式發生了變化,尤其是尋求永續性切實證明的連鎖飯店的需求有所增加。

與燃氣熱水器相比,初始投資較高

一台60公升的住宅熱泵熱水器售價約為3,400新元(2,520美元),而瓦斯熱水器的價格則不到1,000新元(740美元)。額外的佈線、排水和通風工程可能需要額外花費500至1000新元(370至740美元)。由於個人住宅無法享受節能津貼,因此沒有補貼可以縮短投資回收期,許多業主仍然選擇價格較低的燃氣熱水器。二手公寓和公寓管理協會的居住者通常會等到熱水器故障才進行升級,儘管10千瓦以下的熱水器在三年內可以節省500新元(370美元)的營業成本,但其年銷量仍然低迷。

細分市場分析

2025年,空氣源熱泵機組佔新加坡熱泵市場佔有率的48.78%。室外溫度高於攝氏25度C的暖空氣可全年維持穩定的能源效率比(COP),無需高成本的鑽孔或海水取水。由於初始成本相近且核准流程更簡便,這種配置已成為住宅維修和小規模辦公室的首選。在混合式部署中,設施管理人員將空氣源熱泵與備用燃氣鍋爐或電暖器結合使用,預計到2031年,透過價格套利交易,其複合年成長率將達到4.81%。水源熱泵適用於一些特殊地區,例如擁有豐富海水的沿海地區和石化工廠,但其部署規模受到防腐蝕成本和廢水排放法規的限制。地熱能仍然是罕見的選擇,因為在土地資源有限的地區,垂直鑽井的成本過高。獲得新加坡建設局 (BCA) 認證的審計師通常傾向於建議空氣源熱泵,進一步加強了現有系統的動力。

系統供應商正擴大預裝智慧控制器,以調節風扇轉速和除霜循環,從而應對新加坡的高濕度,減少返修次數。諸如Copeland等組件製造商正在推出專為熱帶氣候最佳化的數位渦捲式壓縮機,提升了市場對更高SE-ef能源效率等級產品的接受度。然而,據服務公司稱,客戶仍然對豎井和屋頂設備的冷媒充填量限制保持謹慎,這使得老舊高層建築的維修速度低於預期水準。

預計到2025年,空氣-水平台將佔總收入的51.31%,並預計在2031年之前以5.02%的複合年成長率成長,成為該技術領域中成長最快的。由於濱海灣和裕廊湖區的區域供冷網路採用冷凍水,因此空氣-水熱泵可以透過單一殼管式熱交換器同時提供空間冷卻和60°C的熱水負荷,從而減少設備重複。在公共住宅的走廊中,由於陽台上已經安裝了分離式空調機組仍然很常見,但在高階辦公大樓中,由於業主優先考慮熱回收,空氣-空氣式空調機組的市場佔有率正在被熱水系統蠶食。水-水和地下-地下系統雖然理論上效率更高,但需要海水許可證和鑽井作業,這可能會使專案延誤數月,因此對於工期緊張的開發商來說,這些系統是一個需要考慮的問題。

目前,製造商正在交付模組化撬裝設備,這些設備可安裝在空間有限的機房內,並能以50kW為增量進行擴展,使其成為混合用途項目擴建階段的理想選擇。根據國家環境署的產品註冊資料庫,使用R290和R1234ze冷媒的空氣-水製冷機組的註冊數量預計將在2025年後成長兩倍,這凸顯了該技術在監管合規方面的強勁發展勢頭。設計新型平台式機房的工程師也意識到,空間往往是決定性因素,因為單一多功能模組即可提供足夠的屋頂空間來安裝太陽能電池陣列,從而提高綠色環保標誌評分,並幫助企業實現淨零排放目標。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 「新加坡綠色計畫2030」下公共部門維修津貼激增

- 強制性能源標籤制度正在促進高效能熱泵的普及。

- 商業和公共區域空調擴建(濱海灣、裕廊湖區、TENGA)

- 碳排放稅不斷提高的趨勢正在加速空調系統的電氣化。

- 高能源效率比熱泵、浮體式太陽能發電和儲熱系統整合示範專案。

- 隨著 2028 年分階段減少 HFC 的計劃臨近,對超低 GWP 冷媒系統的需求正在增加。

- 市場限制因素

- 與燃氣熱水器相比,初始設備投資較高

- 缺乏安裝和技術專業知識

- 高層建築屋頂和設施空間短缺

- 空調使用尖峰時段電網儲備不足。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按供應來源

- 空氣源

- 水源

- 地熱

- 混合

- 透過技術

- 空對空

- 從空氣到水

- 水-水

- 來自地下的水(土壤)

- 按產能

- 小於10千瓦

- 10~50 kW

- 50~200 kW

- 超過200千瓦

- 透過使用

- 空間暖氣

- 空間冷卻

- 家用和衛生熱水

- 工業和製程加熱

- 其他用途

- 最終用戶

- 住宅

- 商業

- 產業

- 按安裝類型

- 新安裝

- 改裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Johnson Controls International plc

- Rheem Manufacturing Company

- Alfa Laval AB

- Daikin Industries, Ltd.

- LG Electronics Inc.

- Carrier Global Corporation

- Mitsubishi Electric Asia Pte. Ltd.

- Copeland LP

- Panasonic Holdings Corporation

- AOS Bath Pte. Ltd.

- DENSO Corporation

- Danfoss A/S

- Temperzone Ltd.

- Gree Electric Appliances, Inc. of Zhuhai

- Trane Technologies plc

- Risen Thermohygro Services Pte. Ltd.

- Midea Group Co., Ltd.

- Ariston Holding NV

- Samsung Electronics Co., Ltd.

- Robert Bosch GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the singapore heat pump market size is projected to be USD 464.91 million in 2025, USD 486.36 million in 2026, and reach USD 593.82 million by 2031, growing at a CAGR of 4.07% from 2026 to 2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Industrial and Process Heating, and More), End User (Residential, Commercial, and More), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Singapore Heat Pump Market Trends and Insights

Surge in Public Sector Retrofit Grants Under Singapore Green Plan 2030

The Government earmarked SGD 63 million (USD 47 million) for the Grant for Energy Efficient Measures in Existing Buildings 2.0, extended to March 2027, to help commercial and municipal owners upgrade HVAC systems. Grant-related projects prioritize comprehensive packages that couple heat pumps with building-management software and chiller replacements, rewarding vendors that can deliver turnkey retrofits. Because eligible floor space is concentrated in the Central Business District and emerging polycentric hubs, contractors with prior relationships in those zones are winning early orders. Building owners also lean on partners that can navigate Green Mark paperwork and energy-performance verification to unlock disbursements. The three-year runway allows suppliers to lock in multiyear pipelines, tightening competition for high-capacity air-to-water units.

Mandatory Energy-Labeling Pushing Premium-Efficiency Heat Pumps

The National Environment Agency introduced a five-tick label and a uniform energy-factor test for water heaters effective 1 April 2025. Heat-pump water heaters consistently achieve four or five ticks, while conventional electric resistance units rarely reach two ticks, guiding buyers toward premium efficiency. Because manufacturers must lodge models with the agency before sales, smaller brands without accredited laboratories face entry barriers. Transparent labels highlight lifecycle savings and shrink the information gap that once made capital-intensive heat pumps a hard sell. As a result, distributors report a pivot in ordering patterns ahead of the April deadline, especially from hospitality chains seeking visible sustainability credentials.

High Initial Capex Versus Gas Water Heaters

Residential heat-pump water heaters cost about SGD 3,400 (USD 2,520) for a 60-liter unit against gas heaters under SGD 1,000 (USD 740). The extra wiring, drainage, and ventilation work adds another SGD 500 to 1,000 (USD 370 to 740). Because the Energy Efficiency Grant excludes individual homeowners, no offsetting subsidy shortens payback, so many owners still choose cheaper gas models. Resale-flat dwellers and condominium management committees often postpone upgrades until failures occur, constraining annual unit sales in the sub-10 kW class, even though operating savings reach SGD 500 (USD 370) over three years.

Other drivers and restraints analyzed in the detailed report include:

- Commercial and Municipal District-Cooling Expansion

- Growing Demand for Ultra-Low-GWP Refrigerant Systems Ahead of 2028 HFC Phase-Down

- Limited Roof and Plant Space in High-Rise Buildings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-source units delivered 48.78% of the Singapore heat pump market share in 2025. Warm ambient air of 25 °C and above supports stable year-round coefficients of performance while avoiding costly boreholes or seawater intakes. Comparable upfront pricing and simpler permitting make the format the default for residential retrofits and small offices. In hybrid deployments, facility managers pair an air-source heat pump with a back-up gas boiler or electric element to arbitrage tariff fluctuations, driving a 4.81% CAGR forecast up to 2031. Water-source models serve niche maritime and petrochemical sites where seawater is plentiful, yet anti-corrosion expenses and discharge rules cap volume. Ground-source options remain rare because vertical drilling is price-prohibitive on land-scarce plots. Auditors certified under the Building and Construction Authority scheme often default to air-source recommendations, reinforcing incumbent momentum.

System suppliers increasingly pre-install smart controllers that modulate fan speeds and defrost cycles to handle Singapore's high humidity, reducing maintenance callbacks. Component makers such as Copeland rolled out digital scroll compressors fine-tuned for the tropical envelope, nudging market acceptance of higher-se efficiency classes. Even so, service companies report that customers remain cautious about refrigerant-charge limits inside shafts and rooftops, which keeps retrofit penetration below potential in older tower blocks.

Air-to-water platforms represented 51.31% of 2025 revenue and are set for a 5.02% CAGR through 2031, the quickest pace among technology groups. District-cooling networks in Marina Bay and Jurong Lake District distribute chilled water, so an air-to-water heat pump can supply both space-cooling and 60 °C domestic hot-water loads from a single shell-and-tube exchanger, cutting duplicate equipment. Air-to-air units remain common in public-housing corridors where split-unit air conditioners already populate balconies, but they lose share to hydronic systems in premium offices where owners value heat recovery. Water-to-water and ground-to-water selections, despite higher theoretical efficiencies, demand either seawater permits or boreholes that can delay projects for months, unsettling developers working on tight construction calendars.

Manufacturers now ship modular skids that fit inside constrained mechanical rooms and scale upward in 50 kW steps, an attractive feature for expansion phases in mixed-use projects. The National Environment Agency product-registration database shows a threefold increase in R290 and R1234ze air-to-water listings since 2025, confirming the technology's compliance momentum. Engineers who specify new podium plantrooms confess the deciding factor is often spatial: one multi-service module frees enough roof for PV arrays that boost Green Mark scores, satisfying corporate net-zero declarations.

List of Companies Covered in this Report:

- Johnson Controls International plc

- Rheem Manufacturing Company

- Alfa Laval AB

- Daikin Industries, Ltd.

- LG Electronics Inc.

- Carrier Global Corporation

- Mitsubishi Electric Asia Pte. Ltd.

- Copeland LP

- Panasonic Holdings Corporation

- AOS Bath Pte. Ltd.

- DENSO Corporation

- Danfoss A/S

- Temperzone Ltd.

- Gree Electric Appliances, Inc. of Zhuhai

- Trane Technologies plc

- Risen Thermohygro Services Pte. Ltd.

- Midea Group Co., Ltd.

- Ariston Holding N.V.

- Samsung Electronics Co., Ltd.

- Robert Bosch GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Public Sector Retrofit Grants under Singapore Green Plan 2030

- 4.2.2 Mandatory Energy-labeling Pushing Premium-Efficiency Heat Pumps

- 4.2.3 Commercial and Municipal District-Cooling Expansion (Marina Bay, Jurong Lake District, Tengah)

- 4.2.4 Rising Carbon-Tax Trajectory Incentivizing Electrified HVAC

- 4.2.5 Integration of High-COP Heat Pumps with Floating PV and Thermal Storage Pilots

- 4.2.6 Growing Demand for Ultra-Low-GWP Refrigerant Systems Ahead of 2028 HFC Phase-Down

- 4.3 Market Restraints

- 4.3.1 High Initial Capex Versus Gas Water Heaters

- 4.3.2 Installation and Technical Expertise Gaps

- 4.3.3 Limited Roof and Plant Space in High-Rise Buildings

- 4.3.4 Seasonal Grid-Reserve Margin Shortfalls during Peak Cooling Hours

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Johnson Controls International plc

- 6.4.2 Rheem Manufacturing Company

- 6.4.3 Alfa Laval AB

- 6.4.4 Daikin Industries, Ltd.

- 6.4.5 LG Electronics Inc.

- 6.4.6 Carrier Global Corporation

- 6.4.7 Mitsubishi Electric Asia Pte. Ltd.

- 6.4.8 Copeland LP

- 6.4.9 Panasonic Holdings Corporation

- 6.4.10 AOS Bath Pte. Ltd.

- 6.4.11 DENSO Corporation

- 6.4.12 Danfoss A/S

- 6.4.13 Temperzone Ltd.

- 6.4.14 Gree Electric Appliances, Inc. of Zhuhai

- 6.4.15 Trane Technologies plc

- 6.4.16 Risen Thermohygro Services Pte. Ltd.

- 6.4.17 Midea Group Co., Ltd.

- 6.4.18 Ariston Holding N.V.

- 6.4.19 Samsung Electronics Co., Ltd.

- 6.4.20 Robert Bosch GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)