|

市場調查報告書

商品編碼

2061772

印尼熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Indonesia Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

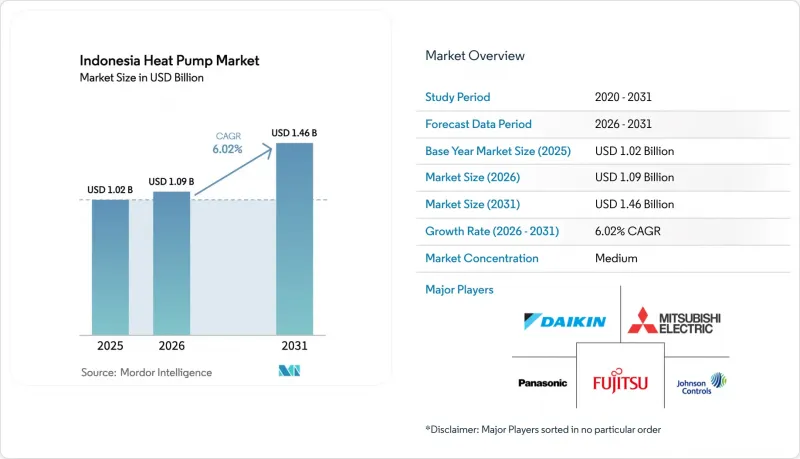

根據 Mordor Intelligence 預測,印尼熱泵市場規模預計到 2025 年將達到 10.2 億美元,到 2026 年將達到 10.9 億美元,到 2031 年將達到 14.6 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 6.02%。

本報告按供應來源(空氣源、水源等)、技術(空氣對空氣、空氣對水等)、容量(小於10kW、10-50kW等)、應用(空間供暖、空間製冷等)、最終用戶(住宅、商業、工業)、安裝類型(新建、維修)和地區進行細分。市場預測以美元計價。

印尼熱泵市場趨勢與洞察

政府獎勵推廣熱泵

修訂後的節能法規降低了強制性能源管理基準值,並將審計範圍擴大到包括工廠、購物中心和酒店在內的更多設施。目前,審計優先考慮熱泵維修而非電阻式加熱器。綠色氣候基金 (GCF) 提供的混合融資方案新增了 1.05 億美元的優惠資本和 1.427 億美元的聯合融資,降低了此前不願為節能現金流項目提供貸款的銀行的專案風險。印尼熱泵市場正直接受益,因為審計發現熱水、洗衣和製程熱負荷的投資回收期不到五年。違規行為的處罰也促使經營團隊在執法措施加強之前進行投資。儘管主要挑戰仍然是認證能源服務公司數量有限,但該框架展示了其他貸款機構可能會效仿的可貸款應用案例。

快速的都市化和節能建築的增加

目前,建築能耗已佔印尼最終能源消耗的23%,如果節能措施延遲實施,到2030年這一比例可能達到40%。在2025年4月舉行的雅加達綠色成長論壇上,165位業主自願承諾排放10%,顯示市場對升級至認證暖通空調系統的需求日益成長。照明和暖通空調的最低能源效率標準承諾,到2030年每年可節省相當於1.9兆印尼幣(約1.21億美元)的能源,並減少8,400萬噸二氧化碳排放,這將加大開發商的資本市場壓力。一項旨在2030年建造或維修100萬套綠色住宅的國家計畫強制要求採用高效熱水解決方案,從而將印尼的熱泵市場納入住宅政策。儘管實施過程中仍存在挑戰,到2025年僅1.45%的建築達到能源管理標準,但中期方向明確,並支持長期需求成長。

前期實施成本高,且資金籌措管道有限。

熱泵熱水器的成本仍比電熱水器高出約10倍,而且大多數商業貸款的期限最長為7年,利率在7%至12%之間,這使得融資困難的買家望而卻步。截至2024年,全國僅有約25家能源服務公司,限制了專案整合和績效合約解決方案的實施,而這些方案本來可以抵銷高昂的資本投入。由於銀行很少接受節能現金流作為抵押品,印尼熱泵市場依賴捐助者的支持項目,例如「節能保險」(保證性能並提供初始資金)和大華銀行的「U-Energy」平台。雖然這些方案前景可期,但與全國需求相比規模較小,這意味著短期內成本障礙可能仍然存在。

細分市場分析

預計到2025年,空氣源熱泵將佔印尼熱泵市場價值的46.78%,憑藉其能夠應對熱帶氣候溫和的溫度波動以及相對簡便的安裝方式,在印尼熱泵市場佔據領先地位。加查馬達大學和PT Geoenergis公司主導的試點計畫表明,利用印尼估計23,766兆瓦的淺層地熱資源,地源熱泵市場仍有7.31%的年成長空間。兩個水平迴路示範項目的性能係數接近4,與分離式空調相比,節能21%至45%。

由於經銷商在全國範圍內儲備備件且核准程序簡便,空氣源熱泵系統仍保持著大規模部署的基礎。然而,隨著政府能源審計要求更加重視生命週期成本指標,預計地下循環系統將在未來醫院和大學的公共採購中佔據主導地位。水源和混合解決方案由於池塘資源有限且控制複雜,目前仍屬於小眾市場。隨著監管機構考慮引入碳定價機制,其顯著的減排潛力可能超過初期成本方面的障礙,預計地下循環系統在印尼熱泵市場的成長動能將有效維持。

預計到2025年,空氣-水冷卻系統將佔總銷售額的42.59%,這表明飯店、醫院和公寓營運商正在優先考慮能夠與現有水循環管道無縫整合的方案。飯店對變冷劑流量(VRF)系統的升級已將冷氣能效比提高至5.40,進一步證明了變頻壓縮機的優越性。地下-水製冷系統反映了地熱能利用的整體利好趨勢,預計年複合成長率將達到7.03%,優於其他冷凍方式。

在冷凍領域,空氣源熱泵正與根深蒂固的分離式空調競爭。儘管分離式空調運作成本較高,但在消費者認知中仍佔主導地位。水源熱泵系統以及結合太陽能和生質能的混合系統目前仍僅限於配備專業技術人員的工業園區。隨著建築規範日益嚴格,建築師正將熱水循環迴路設計視為面向未來的建築設計,預計將使空氣源熱泵系統在印尼整體熱泵市場中保持主導地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府獎勵推廣熱泵

- 快速的都市化和節能建築的日益增多

- 變頻式機組初始成本更低,季節性性能更佳。

- 擴大電力供應範圍,提高電網可靠性。

- 偏遠度假區分佈式太陽能發電和熱泵混合系統的安裝量迅速增加。

- 由於水產品低溫運輸出口需要高效的加工冷卻工藝,因此需求正在擴大。

- 市場限制因素

- 前期實施成本高,且資金籌措管道有限。

- 熟練的熱泵技術人員短缺

- 離島售後服務網分散

- 消費者偏好價格低廉的分離式空調和熱水器套裝。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按供應來源

- 空氣源

- 水源

- 地熱

- 混合

- 透過技術

- 從空中到空中

- 從空氣到水

- 水到水

- 從地熱能到水

- 按產能

- 小於10千瓦

- 10~50 kW

- 50~200 kW

- 超過200千瓦

- 透過使用

- 空間暖氣

- 空間冷卻

- 家用和衛生熱水

- 工業和製程加熱

- 其他用途

- 最終用戶

- 住宅

- 商業

- 產業

- 按安裝類型

- 新安裝

- 改裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Daikin Industries, Ltd.

- Mitsubishi Electric Corp.

- Panasonic Heating and Cooling Solutions

- Fujitsu General Ltd.

- Carrier Global Corp.

- Trane Technologies plc

- Johnson Controls-Hitachi Air Conditioning

- NIBE Industrier AB

- Stiebel Eltron GmbH and Co. KG

- Viessmann Climate Solutions SE

- Vaillant Group

- Glen Dimplex Group(Dimplex)

- PHNIX Eco-Energy Solution Ltd.

- Thermia Heat Pumps AB

- Sanden Holdings Corp.

- Mayekawa Mfg. Co., Ltd.

- Aermec SpA

- Clivet SpA

- Alpha Innotec GmbH

- Ochsner Warmepumpen GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the indonesia heat pump market size is projected to be USD 1.02 billion in 2025, USD 1.09 billion in 2026, and reach USD 1.46 billion by 2031, growing at a CAGR of 6.02% from 2026 to 2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Space Cooling, and More), End User (Residential, Commercial, and Industrial), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Heat Pump Market Trends and Insights

Implementation of Government Incentives for Heat Pump Adoption

Revised Energy Conservation rules lower mandatory energy-management thresholds, bringing a broader mix of factories, malls, and hotels under audit requirements that now emphasize heat-pump retrofits over resistance heaters. Blended-finance from the Green Climate Fund adds USD 105 million of concessional capital and USD 142.7 million of co-financing, trimming project risk for banks that previously hesitated to lend against energy-savings cash flows. The Indonesia heat pump market gains directly because audits identify hot-water, laundry, and process-heat loads where paybacks now fall under five years. Penalties for non-compliance also drive management teams to invest before enforcement actions escalate. The main drag is the limited pool of accredited energy-service companies, but the framework proves bankable use cases that other lenders will replicate.

Rapid Urbanization and Rising Construction of Energy Efficient Buildings

Buildings already absorb 23% of Indonesia's final energy use and could touch 40% by 2030 if efficiency lags. The Jakarta Green Growth forum in April 2025 secured 165 voluntary commitments from property owners to cut emissions 10%, signaling stronger market pull for certified HVAC upgrades. Minimum Energy Performance Standards for lighting and air conditioning promise savings equal to IDR 1.9 trillion (USD 121 million) per year and prevent 84 million tons of CO2 by 2030, so capital-markets pressure on developers is intensifying. National programs to build or retrofit one million green homes by 2030 mandate efficient hot-water solutions, inserting the Indonesia heat pump market into housing policy. Enforcement gaps persist, only 1.45% of buildings met energy-management standards in 2025, but the medium-term signal is clear and supports long-run demand growth.

High Initial Installation Cost and Limited Financing Options

Heat-pump water heaters still cost roughly ten times electric tanks, and most commercial loans top out at seven-year tenors with 7-12% interest rates, suppressing uptake among cash-constrained buyers. Only about 25 active energy-service companies existed nationwide in 2024, limiting project aggregation and performance-contracting solutions that could offset high capex. Banks rarely accept energy-savings cash flows as collateral, so the Indonesia heat pump market relies on donor-supported programs like Energy Savings Insurance and UOB's U-Energy platform that guarantee performance and front capital. These schemes are promising but remain small relative to nationwide demand, so cost barriers will persist in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Declining Upfront Costs and Higher Seasonal Performance of Inverter Based Units

- Increasing Electricity Access and Grid Reliability

- Shortage of Skilled Heat Pump Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-source heat pumps delivered 46.78% of market value in 2025, demonstrating the Indonesia heat pump market share lead of a technology that balances moderate tropical temperature swings with relatively simple installation. Institutional pilots at Universitas Gadjah Mada and PT Geoenergis point to a 7.31% annual growth runway for ground-source units that tap Indonesia's estimated 23,766 MW shallow geothermal resource. Two horizontal-loop demonstrations recorded coefficients of performance near four, saving 21-45% electricity over split ACs.

Air-source equipment keeps its large installed base because distributors stock spare parts nationwide and permits are minimal. Yet government energy-audit mandates favor lifecycle cost metrics, tilting future public procurements toward ground loops in hospitals and universities. Water-source and hybrid solutions stay niche, limited by available ponds or high control complexity. With regulators considering carbon pricing, deep reductions may outweigh first-cost hurdles, making ground-source momentum structurally durable inside the Indonesia heat pump market.

Air-to-water configurations earned 42.59% of 2025 revenue, illustrating how hotel, hospital, and apartment operators value a package that dovetails with existing hydronic lines. Variable refrigerant flow upgrades in hotels raised cooling energy efficiency ratios to 5.40, further validating inverter compressor advantages. Ground-to-water systems mirror overall ground-source tailwinds, clocking a 7.03% forecast CAGR that is poised to outstrip other formats.

Air-to-air heat pumps contend with the deeply entrenched split-AC culture for cooling, which still dominates consumer mindshare despite higher operating costs. Water-to-water and hybrid solar-thermal or biomass couplings remain confined to industrial estates with specialized engineering staff. As building codes tighten, architects specify hydronic loops that future-proof properties, sustaining air-to-water leadership inside the broader Indonesia heat pump market size narrative.

List of Companies Covered in this Report:

- Daikin Industries, Ltd.

- Mitsubishi Electric Corp.

- Panasonic Heating and Cooling Solutions

- Fujitsu General Ltd.

- Carrier Global Corp.

- Trane Technologies plc

- Johnson Controls-Hitachi Air Conditioning

- NIBE Industrier AB

- Stiebel Eltron GmbH and Co. KG

- Viessmann Climate Solutions SE

- Vaillant Group

- Glen Dimplex Group (Dimplex)

- PHNIX Eco-Energy Solution Ltd.

- Thermia Heat Pumps AB

- Sanden Holdings Corp.

- Mayekawa Mfg. Co., Ltd.

- Aermec S.p.A

- Clivet SpA

- Alpha Innotec GmbH

- Ochsner Warmepumpen GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Implementation of Government Incentives for Heat Pump Adoption

- 4.2.2 Rapid Urbanisation and Rising Construction of Energy-Efficient Buildings

- 4.2.3 Declining Upfront Costs and Higher Seasonal Performance of Inverter-Based Units

- 4.2.4 Increasing Electricity Access and Grid Reliability

- 4.2.5 Surge in Distributed Solar-Heat Pump Hybrid Installations in Remote Resorts

- 4.2.6 Push From Cold-Chain Fishery Exports Requiring High-Efficiency Process Cooling

- 4.3 Market Restraints

- 4.3.1 High Initial Installation Cost and Limited Financing Options

- 4.3.2 Shortage of Skilled Heat Pump Technicians

- 4.3.3 Fragmented After-Sales Service Network in Outer Islands

- 4.3.4 Customer Preference for Cheap Split AC and Water Heater Combos

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries, Ltd.

- 6.4.2 Mitsubishi Electric Corp.

- 6.4.3 Panasonic Heating and Cooling Solutions

- 6.4.4 Fujitsu General Ltd.

- 6.4.5 Carrier Global Corp.

- 6.4.6 Trane Technologies plc

- 6.4.7 Johnson Controls-Hitachi Air Conditioning

- 6.4.8 NIBE Industrier AB

- 6.4.9 Stiebel Eltron GmbH and Co. KG

- 6.4.10 Viessmann Climate Solutions SE

- 6.4.11 Vaillant Group

- 6.4.12 Glen Dimplex Group (Dimplex)

- 6.4.13 PHNIX Eco-Energy Solution Ltd.

- 6.4.14 Thermia Heat Pumps AB

- 6.4.15 Sanden Holdings Corp.

- 6.4.16 Mayekawa Mfg. Co., Ltd.

- 6.4.17 Aermec S.p.A

- 6.4.18 Clivet SpA

- 6.4.19 Alpha Innotec GmbH

- 6.4.20 Ochsner Warmepumpen GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)