|

市場調查報告書

商品編碼

2062362

法國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)France E-Commerce Warehouse - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

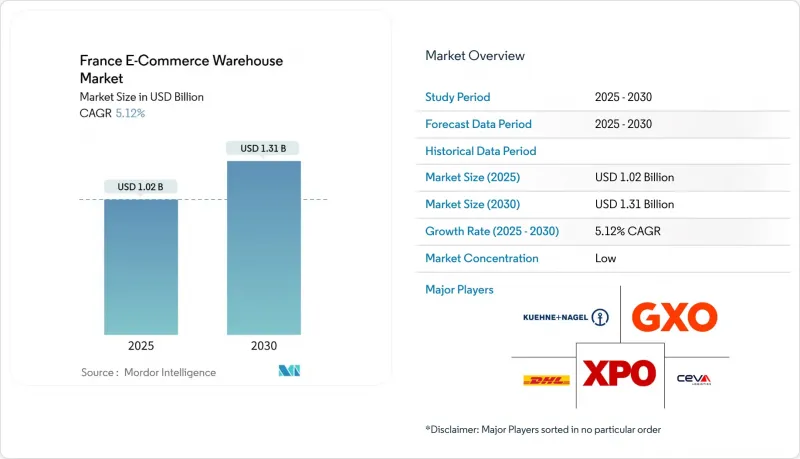

根據 Mordor Intelligence 預測,法國電子商務倉儲市場規模預計將在 2025 年達到 12.9 億美元,2026 年達到 13.6 億美元,到 2031 年達到 17.4 億美元,2026 年至 2031 年的複合年成長率為 5.06%。

本報告按倉庫類型(履約中心、物流中心、低溫運輸倉庫、暗店/微型倉配中心及其他)、服務類型(倉儲、揀貨包裝、附加價值服務)、自動化程度(人工、半自動、全自動)和終端用戶行業(服裝鞋類及其他)進行細分。市場預測以美元計價。

法國電子商務倉儲市場的趨勢與洞察

歐盟內部對跨境聚合中心的需求日益成長

法國位於歐盟中心地帶,使得企業能夠在一日送達範圍內向1.15億消費者寄送小包裹。像德迅(Kuehne+Nagel)這樣的領先第三方物流公司正將其海關專業知識融入直接面對消費者的服務中,預計跨境物流的成長速度將超過純粹的國內物流。沃克呂茲等周邊地區正吸引著集散中心的入駐,這些中心利用較低的地價和通往西班牙和義大利的高速公路網路,減輕了法國法蘭西島大區的負擔。 DHL旗下的Chronopost網路擁有19,555個收件點,充分展現了實現無縫國際電子商務所需的密集網點。歐盟數位單一市場內的監管協調進一步減少了摩擦,並吸引泛歐品牌進駐法國倉庫,這些倉庫在速度、成本和簡化的清關流程方面實現了平衡。

政府對改建為棕地倉庫的補貼

由於主要城市土地資源稀缺,政策制定者正在津貼廢棄工業用地的再開發。法蘭西島大區規劃(Schema Directeur de la Region Ile- 法國法蘭西島)引導物流中心向已都市化的地區集中,並為致力於環境修復的開發商提供稅收優惠和快速核准流程。政府支持的巴黎聖殿科學中心包含一個物流區,使投資者能夠享受簡化的核准程序。這使得像普洛斯(Prologis)這樣的公司能夠在擴大營運規模的同時滿足永續性要求。棕地再開發可以緩解人們對待開發區開發的抵觸情緒,符合法國的淨零排放目標,並透過將倉庫更靠近終端消費者來確保交貨前置作業時間。

遵守嚴格的城市噪音和交通排放氣體法規的成本。

如今,各市政府正將「暗店」(dark store)歸類為倉庫,從而允許當局限制其營業時間和實施夜間送貨禁令。尤其是在巴黎,由於違反分區規定,60家快速零售點面臨關閉風險。企業被迫投資隔音裝卸平台、電動貨車和即時交通管理系統以維持其都市區基地,這進一步加重了本已捉襟見肘的電子商務成本。法院的裁決強化了市政府的權力,並表明在車輛電氣化和微型配送中心模式成熟之前,監管合規支出在可預見的未來仍將是一項沉重的負擔。

細分市場分析

履約中心憑藉其深層儲存和多品揀選能力,能夠應對全國範圍內的訂單高峰,預計到2025年將佔法國電商倉儲市場規模的51.43%。亞馬遜位於奧尼(Augny)的18萬平方公尺物流中心,擁有4000名員工和25公里長的輸送機,清晰地展現了其在阿爾薩斯、洛林及周邊地區穩定前置作業時間的規模。這些大型物流中心優先考慮自動化,以抵消不斷上漲的工資成本,並透過引入貨到人穿梭車和自動化分類機,將貨到貨的周轉時間縮短至30分鐘以內。此外,營運商也致力於透過在現有設施中增建夾層來最佳化空間利用率,從而規避在巴黎附近購買新土地的障礙。

暗店和微型倉配中心目前僅佔占地面積的4%,卻是成長最快的細分領域,預計到2031年複合年成長率將達到10.26%。快時尚業者正在利用環城公路內1000至3000平方公尺的設施,承諾15分鐘內送達雜貨。隨著土地使用法規的日益嚴格,下一波浪潮正轉向停車場和鐵路車輛的改造。普洛斯(Prologis)正在奧爾良試行「城市樞紐」概念,將宅配櫃、電動車充電站和自行車停車位整合在一起。隨著按需食品解決方案的擴展,低溫運輸的各種變體也應運而生,為需要溫控的微型配送中心在法國電商倉儲市場開闢了一個高階細分市場。

到2025年,倉儲服務將佔法國電商倉儲市場佔有率的45.16%,反映出在價值鏈波動的情況下,企業對安全庫存的需求依然強勁。大型零售商正在與多家客戶簽訂長期租賃協議,租用多客戶園區,並預留貨架空間,以應對假期季節的需求高峰。像STEF的三溫區倉儲設施這樣的加值倉儲服務,透過遵守食品安全規程和能源效率目標,提供更高的租金。

揀貨包裝業務正以9.54%的複合年成長率快速成長,機器人技術將訂單處理時間縮短至不到一小時,推動了這項業務的蓬勃發展。在DISPEO位於埃夫勒的倉庫,引進貨物搬運機器人(GTP)後,每人每小時可揀選180件商品,節省的人事費用遠超投資成本。訂閱盒和網紅行銷的「限時搶購」需要進行套裝組裝、貼標和禮品包裝等流程,所有這些流程都整合到統一的服務合約中,從而提高了倉庫的運轉率。隨著當日達服務的普及,托運人越來越傾向於選擇能夠將倉儲、揀貨、個人化客製化和退貨處理整合於一體的營運商,這進一步加速了法國電商倉儲市場的一體化趨勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟內部對跨境聚合中心的需求日益成長

- 政府對棕地倉庫改造的補貼

- 全通路線上訂購線下取貨模式的激增,正在推動對本地配送中心的需求。

- 利用人工智慧驅動的庫存分析提高設施投資報酬率

- 需要溫控空間的常規配送模式的迅速興起

- 電動車最後一公里配送車隊的擴張需要配備充電設施的倉庫。

- 市場限制因素

- 遵守嚴格的城市噪音和交通排放氣體分區法規的成本。

- 缺乏具備機器人技術技能的人員正在減緩自動化技術的普及。

- 電費波動推高了營運成本。

- 歐盟網路安全法規增加了倉庫管理系統 (WMS) 的升級成本。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 倉庫類型

- 履約中心

- 物流中心(DC)

- 低溫運輸倉庫

- 暗店/微型倉配中心

- 其他(逆向物流中心、保稅倉庫、多功能空間等)

- 按服務類型

- 貯存

- 揀貨和包裝

- 附加價值服務及其他服務(套件組裝、貼標籤)

- 按自動化級別

- 手動的

- 半自動

- 自動化

- 按最終用戶行業分類

- 服裝和鞋類

- 家用電子產品

- 食品和快速消費品

- 醫藥、美容和健康

- 家居用品和家具

- 其他

- 法國各地區

- 法國法蘭西島

- 奧弗涅-羅納-阿爾卑斯大區

- 上法蘭西區

- 普羅旺斯-阿爾卑斯-藍色海岸

- 格蘭德埃斯特

- 新阿基坦

- 奧克西塔尼

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- ID Logistics

- GEODIS

- GXO Logistics

- La Poste Group(including Colissimo/Chronopost)

- STEF

- FM Logistic

- Kuehne+Nagel

- Centrimex

- XPO Logistics

- DSV

- DACHSER

- CMA CGM Group(including CEVA Logistics)

- Bansard International

- Seko Logistics

- Schneider Logistics

- SupplyWeb

- Amazon Logistics

- Rhenus Logistics

- Loxxess

第7章 市場機會與未來展望

According to Mordor Intelligence, the france e-Commerce warehouse market size is projected to be USD 1.29 billion in 2025, USD 1.36 billion in 2026, and reach USD 1.74 billion by 2031, growing at a CAGR of 5.06% from 2026 to 2031.

This report is Segmented by Warehouse Type (Fulfilment Centres, Distribution Centres, Cold-Chain Warehouses, Dark Stores/Micro-Fulfillment Centers, Others), by Service Type (Storage, Picking and Packing, Value-Added Services), by Automation Level (Manual, Semi-Automated, Automated), by End-User Industry (Apparel and Footwear, and More). The Market Forecasts are Provided in Terms of Value (USD).

France E-Commerce Warehouse Market Trends and Insights

Growing Demand for EU Cross-Border Consolidation Hubs

France sits at the heart of the European Union, letting operators dispatch parcels to 115 million consumers within a single-day delivery radius. Large 3PLs such as Kuehne+Nagel fold customs-clearance expertise into direct-to-consumer offerings, betting on faster growth in cross-border flows than in purely domestic traffic. Peripheral sites like Vaucluse leverage lower land prices and motorway links to Spain and Italy to attract consolidation hubs that relieve pressure on Ile-de-France. DHL's Chronopost network of 19,555 drop-off points underscores the node density required to make international e-commerce seamless. Regulatory harmonization under the EU Digital Single Market further reduces friction, steering pan-European brands toward French warehouses that balance speed, cost, and customs simplicity.

Government Subsidies for Brownfield Warehouse Conversions

Limited land in big cities drives policymakers to subsidize the reclamation of disused industrial parcels. The Schema Directeur de la Region Ile-de-France steers logistics toward already-urbanized plots, offering fiscal incentives and faster permits to developers that commit to environmental remediation. Paris-Saclay's government-backed science hub includes logistics zones where investors benefit from streamlined approvals, helping operators like Prologis meet sustainability mandates while enlarging their footprint. Upgrading brownfields cuts greenfield resistance, aligns with national net-zero goals, and keeps warehouses near end consumers to preserve delivery lead times.

Stringent Urban Noise and Traffic-Emission Zoning Compliance Costs

Municipalities now classify dark stores as warehouses, letting officials curb operating hours and impose delivery curfews, especially in Paris, where 60 quick-commerce sites risk closure for zoning breaches. Operators must invest in soundproof docks, electric vans, and real-time traffic management to retain urban footprints, inflating cost bases that already face thin e-commerce margins. Court rulings reinforce city authority, signaling that compliance spending will remain a near-term burden until vehicle electrification and micro-hub models mature.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel Click-and-Collect Surge Boosting Regional Hub Needs

- AI-Driven Inventory Analytics Improving Facility ROI

- Shortage of Robotics-Skilled Labor Delaying Automation Roll-Outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fulfillment centers captured 51.43% of the France e-commerce warehouse market size in 2025, thanks to deep-lane storage and multi-SKU picking that serve national order peaks. Amazon's 180,000 m2 Augny site illustrates the scale of 4,000 staff and 25 km of conveyors keep lead times stable across Alsace, Lorraine, and neighboring countries. These megasites prioritize automation to offset wage inflation, embedding goods-to-person shuttles and automated sorters that push dock-to-dock cycles below 30 minutes. Operators also retrofit mezzanines into legacy shells, focusing on cubic optimization to avoid greenfield barriers near Paris.

Dark stores and micro-fulfillment centers, though only 4% of floor space today, are the fastest-growing sub-category at 10.26% CAGR through 2031. Quick-commerce players exploit 1,000-3,000 m2 facilities inside ring roads to promise 15-minute grocery drops. Land-use pushback is steering the next wave toward converted parking garages and rail depots, with Prologis piloting urban-hub concepts in Orleans that mix parcel lockers, EV charging, and bicycle docks. Cold-chain variants emerge as on-demand meal solutions expand, opening a premium pocket inside the France e-commerce warehouse market for temperature-specific micro sites.

Storage services accounted for 45.16% of France e-commerce warehouse market share in 2025, reflecting the enduring need to hold safety stock amid supply-chain volatility. Large retailers secure long-term leases on multi-client campuses, tying up racked capacity ahead of holiday peaks. Value-added storage, such as tri-temperature chambers at STEF, commands premium rents by complying with food-safety protocols and energy-efficiency targets.

Picking and packing, expanding at 9.54% CAGR, gains traction as robotics slashes order-cycle times to under one hour. DISPEO's Evreux site reaches 180 picks per person per hour with goods-to-person robots, extracting labor savings that more than offset capital outlays. Subscription boxes and influencer "drops" require kitting, labeling, and gift-wrap steps all bundled into integrated service contracts that lift warehouse yields. As same-day delivery proliferates, shippers favor operators that fuse storage, picking, personalization, and return handling under one roof, reinforcing convergence in the France e-commerce warehouse market.

List of Companies Covered in this Report:

- DHL Group

- ID Logistics

- GEODIS

- GXO Logistics

- La Poste Group (including Colissimo/Chronopost)

- STEF

- FM Logistic

- Kuehne+Nagel

- Centrimex

- XPO Logistics

- DSV

- DACHSER

- CMA CGM Group (including CEVA Logistics)

- Bansard International

- Seko Logistics

- Schneider Logistics

- SupplyWeb

- Amazon Logistics

- Rhenus Logistics

- Loxxess

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for EU Cross-Border Consolidation Hubs

- 4.2.2 Government Subsidies for Brownfield Warehouse Conversions

- 4.2.3 Omnichannel Click-and-Collect Surge Boosting Regional Hub Needs

- 4.2.4 AI-Driven Inventory Analytics Improving Facility ROI

- 4.2.5 Rapid Rise of Subscription Delivery Models Requiring Temperature-Controlled Space

- 4.2.6 Expansion of EV Last-Mile Fleets Needing Charging-Ready Warehouses

- 4.3 Market Restraints

- 4.3.1 Stringent Urban Noise and Traffic-Emission Zoning Compliance Costs

- 4.3.2 Shortage of Robotics-Skilled Labor Delaying Automation Roll-Outs

- 4.3.3 Volatile Electricity Tariffs Inflating Operating Expenses

- 4.3.4 EU Cyber-Security Mandates Raising WMS Upgrade Outlays

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Warehouse Type

- 5.1.1 Fulfilment Centres

- 5.1.2 Distribution Centres (DCs)

- 5.1.3 Cold-Chain Warehouses

- 5.1.4 Dark Stores / Micro-Fulfillment Centers

- 5.1.5 Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, Etc.)

- 5.2 By Service Type

- 5.2.1 Storage

- 5.2.2 Picking and Packing

- 5.2.3 Value-Added Services and Others (Kitting, Labelling)

- 5.3 By Automation Level

- 5.3.1 Manual

- 5.3.2 Semi-Automated

- 5.3.3 Automated

- 5.4 By End-User Industry

- 5.4.1 Apparel and Footwear

- 5.4.2 Consumer Electronics

- 5.4.3 Grocery and FMCG

- 5.4.4 Pharmaceuticals, Beauty and Wellness

- 5.4.5 Home Essentials and Furnishings

- 5.4.6 Others

- 5.5 By French Region (Value)

- 5.5.1 Ile-de-France

- 5.5.2 Auvergne-Rhone-Alpes

- 5.5.3 Hauts-de-France

- 5.5.4 Provence-Alpes-Cote d'Azur

- 5.5.5 Grand Est

- 5.5.6 Nouvelle-Aquitaine

- 5.5.7 Occitanie

- 5.5.8 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)}

- 6.4.1 DHL Group

- 6.4.2 ID Logistics

- 6.4.3 GEODIS

- 6.4.4 GXO Logistics

- 6.4.5 La Poste Group (including Colissimo/Chronopost)

- 6.4.6 STEF

- 6.4.7 FM Logistic

- 6.4.8 Kuehne+Nagel

- 6.4.9 Centrimex

- 6.4.10 XPO Logistics

- 6.4.11 DSV

- 6.4.12 DACHSER

- 6.4.13 CMA CGM Group (including CEVA Logistics)

- 6.4.14 Bansard International

- 6.4.15 Seko Logistics

- 6.4.16 Schneider Logistics

- 6.4.17 SupplyWeb

- 6.4.18 Amazon Logistics

- 6.4.19 Rhenus Logistics

- 6.4.20 Loxxess

7 Market Opportunities and Future Outlook

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)