|

市場調查報告書

商品編碼

2062051

亞太地區化學品倉儲市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)Asia-Pacific Chemical Warehousing And Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

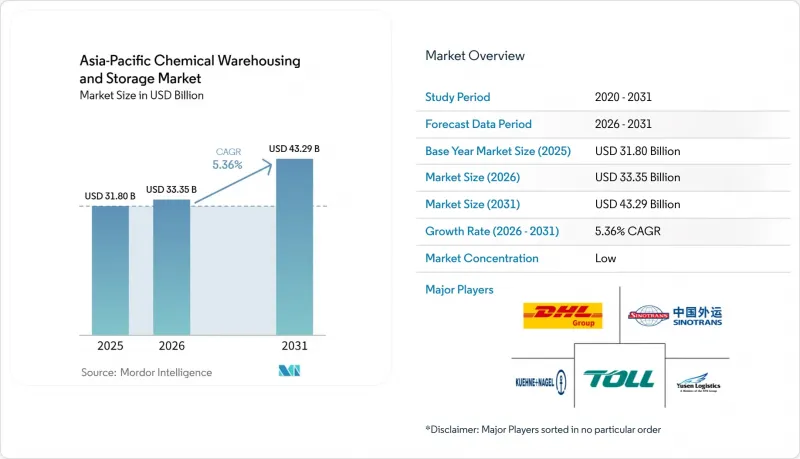

根據 Mordor Intelligence 預測,亞太地區的化學品倉儲市場規模預計在 2025 年將達到 318 億美元,在 2026 年將達到 333.5 億美元,在 2031 年將達到 432.9 億美元。

預計從 2026 年到 2031 年,年複合成長率將達到 5.36%。

本報告按倉庫類型(普通倉庫、特殊化學品倉庫等)、化學品類型(易燃液體、腐蝕性物質等)、終端用戶行業(基礎化學品製造、特種化學品製造等)和國家(中國、印度、日本等)進行細分。市場預測以以金額為準(十億美元)表示。

亞太地區化學品倉儲市場的趨勢與洞察

醫藥低溫運輸和生命科學製造領域的成長

隨著生物製藥和疫苗的配送需要能夠維持不同溫度區域並具備嚴格監控和預警能力的設施,低溫運輸物流正在重新思考儲存規範。區域營運商正在整合租賃資產以提高周轉率並減少資本投入,例如,亞太地區多個樞紐的單程托盤運輸網路就用於臨床用品的運輸。具備預測預警功能的即時冷藏貨櫃遙測系統正成為許多競標的標配,而每小時監控也已被納入亞太地區整個化學品倉儲市場的採購清單。具有快速警報功能的環境監測系統(例如台灣生物製藥儲存設施中使用的系統)擴大被列入提案(RFP)中,以幫助營運商滿足良好分銷規範(GDP)的要求。印度和東南亞不斷擴展的網路正在將港口儲存能力與內陸冷藏倉庫連接起來,以方便處理對時間和溫度敏感的貨物並縮短週期時間。在全部區域,受食品和醫藥產業強勁需求的推動,低溫運輸倉儲面積持續擴張。這反過來又支撐了亞太地區化學品倉儲市場中溫控設施的價格穩定和運轉率。

加速外包給第三方物流(3PL) 供應商

化工企業正透過與關鍵物流合作夥伴合作,整合倉儲和運輸業務,以確保營運透明度、建立合規體系並實現規模化成本控制。一個顯著的例子是,企業選擇一位區域負責人,負責統籌每年數萬件透過空運、海運和陸運路線運輸的貨物,並利用整合平台進行路線風險評估和承運商篩選。這表明,外包如何能夠降低亞太地區化工倉儲市場小規模網路帶來的風險。在中國,關於危險物品生命週期資訊科技追蹤並與主管機關進行電子通訊的法規草案,正促使小型托運人與已運作合規系統的第三方物流合作夥伴開展合作。此外,外包商正在利用化學品專用工作流程,提供諸如重新包裝和文件管理等附加價值服務,從而縮短亞太地區化工倉儲市場的前置作業時間並降低異常處理成本。隨著本地企業將業務拓展至印度和東南亞,港口樞紐與內陸物流中心之間的合作日益加強,即使在大規模企業發展中,也能提高服務可靠性。

海岸工業區土地嚴重短缺

在亞洲沿海工業區,更嚴格的緩衝區和風險疊加區正在減少適合儲存危險物品的土地存量。一項針對中國沿海風險區的同行評審分析顯示,隨著安全距離規定的日益嚴格,獲準的工業用地面積明顯減少,推高了地價,並使亞太地區化學品倉儲市場的擴張計劃變得更加複雜。營運商正透過採用高層貨架、自動化和提高垂直密度來應對用地面積有限的問題,同時維持服務水準和安全標準。重建面臨分區和社區方面的限制,網路也擴大被重新分配到內陸地區。這增加了土地和多式聯運成本,但也釋放了可用於建設的土地。成熟大都會圈的低溫運輸設施產運轉率緊張,導致經認證的冷藏托盤儲存空間溢價上漲,並且其與常溫儲存之間的價值差距持續存在。從長遠來看,隨著亞太地區化學品倉儲市場稀缺的土地滿足更嚴格的監管標準,整合自動化、安全認證和智慧型能源管理的計畫將展現成本優勢。

細分市場分析

到2025年,通用倉儲將佔亞太地區化學品倉儲市場佔有率的30.12%,反映出其廣泛適用於可常溫儲存的通用溶劑、基礎油和中間體化學品。溫控設施預計將持續成長,到2031年將達到6.81%的複合年成長率,因為生物製藥、疫苗和溫度敏感製劑需要規劃冷藏區域、檢驗的感測器和事件日誌。營運商繼續在同一場地內建造冷藏室和常溫儲存區,以便在不影響產品品質的前提下管理多樣化的產品組合。配備低於度C的儲存室、自動發泡噴灌以及與倉庫管理系統(WMS)整合的揀選功能的專用物流中心,體現了高需求地區向高品質基礎設施的結構性轉變。在成熟的大都會圈,低溫運輸設施的利用率仍然不足,這導致其與常溫儲存設施之間存在租金差距,並支撐了新建設施的經濟可行性。在預測期內,亞太地區的化學品倉儲市場預計將更多地採用港口和機場附近的綜合常溫和冷藏設施,從而縮短收貨和交付流程,並降低與溫度敏感貨物相關的風險。

在亞太地區的化學品倉儲市場,隨著GDP、ISO 9001和ISO 45001等認證架構日益嚴格,溫控設施的市場規模預計將會擴大。與物流相關的即時遙測和預測性警報正逐漸成為新競標的標配,這進一步強化了物聯網賦能的冷庫和儲存過程中持續監控的商業價值。同時,危險物品儲存的標準化進程提高了對防火、通風和抗震穩定性的基本結構要求,增加了資本支出(CAPEX)的需求,並擴大了傳統設施和A級設施之間的性能差距。隨著客戶考慮簽訂包含儲存、監控和合規報告的多年期契約,這些趨勢正在改變亞太地區化學品倉儲產業的格局。對溫度分佈圖、區域分類和氣流控制等方面的設施投資,使營運商能夠在滿足審核要求的同時,提高單位面積的有效儲存容量。因此,亞太地區化學品倉庫和儲存市場中,經過認證的冷藏和專用環境的構成比正在穩步轉變。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 醫藥低溫運輸和生命科學製造領域的成長

- 加速外包給第三方物流(3PL) 供應商

- 從液化天然氣到化工產業的策略性樞紐投資

- 建造-擁有-營運 (BOO) 和建造-營運-移交 (BOT) 專案模式

- 特種化學品和先進材料製造的成長

- 小規模企業的電子商務和化學品分銷

- 市場限制因素

- 海岸工業走廊土地嚴重短缺

- 訓練有素的危險物品處理人員長期短缺

- 嚴重事故後保險費飆升。

- 高資本密集度及長投資回收期

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 按類型對化學物質進行分類,會影響設施設計

- 溫度控制細分市場推動高階市場成長

第5章 市場規模與成長預測

- 倉庫類型

- 普通倉庫

- 特用化學品倉庫

- 危險品(HAZMAT)倉庫

- 溫控化學品倉庫

- 依化學物質類型

- 易燃液體

- 腐蝕性物質

- 危險物質

- 氧化劑

- 其他

- 按最終用戶行業分類

- 基礎化學製造

- 特種化學品製造

- 製藥和生命科學

- 農業化學品

- 油漆、塗料、黏合劑

- 食品/飼料添加劑

- 石油天然氣/石油化工

- 其他

- 國家

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 馬來西亞

- 泰國

- 越南

- 菲律賓

- 新加坡

- 澳洲

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- Sinotrans

- Toll Group

- Kuehne+Nagel International AG

- Yusen Logistics Co., Ltd.(Part of NYK Line)

- HOYER Group

- CH Robinson

- DSV

- Suttons Group

- Nippon Express

- Broekman Logistics

- CEVA Logistics

- Rhenus Logistics

- BDP International

- Den Hartogh Logistics

- Talke Logistics

- Kerry Logistics Network Ltd.

- United Parcel Service(UPS)

- Stolt-Nielsen Ltd.

- Aegis Logistics Ltd

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific chemical warehousing and storage market size is projected to be USD 31.80 billion in 2025, USD 33.35 billion in 2026, and reach USD 43.29 billion by 2031, growing at a CAGR of 5.36% from 2026 to 2031.

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More), and by Country (China, India, Japan, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

Asia-Pacific Chemical Warehousing And Storage Market Trends and Insights

Pharmaceutical Cold Chain and Life Sciences Manufacturing Growth

Cold-chain logistics is reshaping storage specifications as biologics and vaccine flows demand facilities that can maintain distinct temperature zones with tight monitoring and alerting. Regional operations are deploying rental-asset pooling to accelerate turns and limit capital lock-up, illustrated by one-way pallet shipper networks now spanning multiple Asia-Pacific hubs for clinical materials. Real-time reefer telemetry with predictive alerts has become standard in many tenders, and hour-by-hour monitoring is now embedded into procurement checklists across the Asia-Pacific chemical warehousing and storage market. Environmental Monitoring Systems with rapid alarms, as seen in Taiwan biologics storage, are increasingly specified in requests for proposals and help operators meet Good Distribution Practice expectations. Network buildouts in India and Southeast Asia are aligning port-proximate capacity with inland cold rooms to reduce handovers and cycle time for time- and temperature-sensitive shipments. Cold-chain square meters across APAC continue to expand under strong food and pharma pull, which supports rate resilience and utilization for temperature-controlled nodes serving the Asia-Pacific chemical warehousing and storage market.

Accelerating Outsourcing to Third-Party Logistics (3PL) Providers

Chemical producers are consolidating warehousing and transportation with lead logistics partners to gain visibility, compliance readiness, and scale-based cost control. A prominent example is the selection of a single regional leader to orchestrate tens of thousands of annual shipments across air, ocean, and road while using integrated platforms for lane risk and carrier vetting, which demonstrates how outsourcing de-risks complex networks in the Asia-Pacific chemical warehousing and storage market. Draft regulations in China are formalizing lifecycle IT tracking and electronic connectivity with authorities for dangerous goods, which is pushing smaller shippers toward 3PL partnerships that already operate compliant systems. Outsourcers are also bundling value-added services like repackaging and documentation management using specialized chemical workflows, which shortens lead times and reduces exception costs in the Asia-Pacific chemical warehousing and storage market. Network expansion by regional operators into India and Southeast Asia is strengthening the interplay between port-based nodes and inland distribution centers that support higher service reliability at scale.

Severe Land Scarcity in Coastal Industrial Corridors

Coastal industrial belts in Asia are tightening buffer zones and risk overlays, which reduces the inventory of land parcels eligible for hazardous-materials storage. Peer-reviewed analysis of China's coastal risk zones shows a clear contraction of permitted industrial spaces as safety-distance rules take hold, which elevates land prices and complicates expansion plans for the Asia-Pacific chemical warehousing and storage market. Operators are responding with high-bay racking, automation, and vertical density to offset constrained footprints while maintaining service levels and safety envelopes. Redevelopments are facing zoning and community constraints, and networks are rebalancing inland, which adds drayage and intermodal costs but secures buildable land. Cold-chain locations in mature metros are running tight utilization, which amplifies the premium on certified refrigerated pallet positions and creates a durable value gap with ambient storage. Over the long term, projects that blend automation, safety certification, and smart energy management will carry a cost advantage when scarce land meets higher regulatory thresholds in the Asia-Pacific chemical warehousing and storage market.

Other drivers and restraints analyzed in the detailed report include:

- Strategic LNG-to-Chemicals Hub Investments

- Build-Own-Operate (BOO) and Build-Operate-Transfer (BOT) Project Models

- Chronic Shortage of Trained Hazmat Handling Personnel

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General warehousing captured 30.12% of the Asia-Pacific chemical warehousing and storage market share in 2025, reflecting broad suitability for commodity solvents, base oils, and intermediate chemicals subject to ambient conditions. Temperature-controlled facilities are pacing growth at 6.81% CAGR through 2031 as biologics, vaccines, and sensitive formulations require mapped refrigeration zones, validated sensors, and event logging. Operators continue to deploy cold rooms alongside ambient bays in the same compound to manage mixed portfolios without compromising product integrity. Purpose-built distribution hubs with sub-25°C rooms, foam-based automated sprinklers, and WMS-integrated order picking reflect a structural pivot toward premium infrastructure in high-volume nodes. Cold-chain utilization remains tight across mature metros, which sustains rent differentials relative to dry storage and supports new-build economics. Over the forecast window, the Asia-Pacific chemical warehousing and storage market will likely see greater adoption of integrated ambient-and-cold sites near ports and airports to trim handovers and reduce exception risk for sensitive loads.

The Asia-Pacific chemical warehousing and storage market size for temperature-controlled facilities is projected to expand as certification frameworks tighten around GDP, ISO 9001, and ISO 45001. Real-time telemetry, in referring to logistics and predictive alerting are becoming a default feature in new tenders, which strengthens the business case for IoT-enabled cold rooms and continuous monitoring in storage. Parallel standard-setting for toxic-substance storage is raising baseline structural requirements for fire resistance, ventilation, and seismic anchoring, which is lifting capex needs and widening performance spreads between legacy and Grade A facilities. These preferences are reshaping the Asia-Pacific chemical warehousing and storage industry profile as customers weigh multi-year commitments that bundle storage, monitoring, and compliance reporting. Facility-level investments in temperature mapping, zone segregation, and controlled airflow are also enabling operators to stretch usable capacity per square foot while upholding audit requirements. The net effect is a steady mix shift toward certified cold and specialty-ready environments within the Asia-Pacific chemical warehousing and storage market.

List of Companies Covered in this Report:

- DHL Group

- Sinotrans

- Toll Group

- Kuehne + Nagel International AG

- Yusen Logistics Co., Ltd. (Part of NYK Line)

- HOYER Group

- C.H. Robinson

- DSV

- Suttons Group

- Nippon Express

- Broekman Logistics

- CEVA Logistics

- Rhenus Logistics

- BDP International

- Den Hartogh Logistics

- Talke Logistics

- Kerry Logistics Network Ltd.

- United Parcel Service (UPS)

- Stolt-Nielsen Ltd.

- Aegis Logistics Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pharmaceutical Cold Chain and Life Sciences Manufacturing Growth

- 4.2.2 Accelerating Outsourcing to Third-Party Logistics (3PL) Providers

- 4.2.3 Strategic LNG-to-Chemicals Hub Investments

- 4.2.4 Build-Own-Operate (BOO) and Build-Operate-Transfer (BOT) Project Models

- 4.2.5 Growth in Specialty Chemicals and Advanced Materials Manufacturing

- 4.2.6 E-commerce and Chemical Distribution to Small-Scale Industries

- 4.3 Market Restraints

- 4.3.1 Severe Land Scarcity in Coastal Industrial Corridors

- 4.3.2 Chronic Shortage of Trained Hazmat Handling Personnel

- 4.3.3 Escalating Insurance Premiums Following Major Incidents

- 4.3.4 High Capital Intensity and Long Payback Periods

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Chemical Type Segmentation Driving Facility Design

- 4.9 Temperature-Controlled Segment Leading Premium Growth

5 Market Size & Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Country

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Indonesia

- 5.4.6 Malaysia

- 5.4.7 Thailand

- 5.4.8 Vietnam

- 5.4.9 Philippines

- 5.4.10 Singapore

- 5.4.11 Australia

- 5.4.12 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Sinotrans

- 6.4.3 Toll Group

- 6.4.4 Kuehne + Nagel International AG

- 6.4.5 Yusen Logistics Co., Ltd. (Part of NYK Line)

- 6.4.6 HOYER Group

- 6.4.7 C.H. Robinson

- 6.4.8 DSV

- 6.4.9 Suttons Group

- 6.4.10 Nippon Express

- 6.4.11 Broekman Logistics

- 6.4.12 CEVA Logistics

- 6.4.13 Rhenus Logistics

- 6.4.14 BDP International

- 6.4.15 Den Hartogh Logistics

- 6.4.16 Talke Logistics

- 6.4.17 Kerry Logistics Network Ltd.

- 6.4.18 United Parcel Service (UPS)

- 6.4.19 Stolt-Nielsen Ltd.

- 6.4.20 Aegis Logistics Ltd

7 Market Opportunities & Future Outlook

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)