|

市場調查報告書

商品編碼

2061774

泰國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Thailand Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

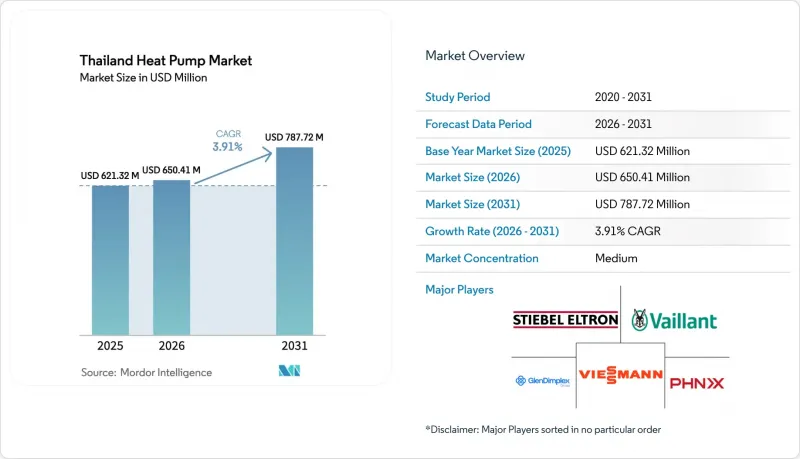

據 Mordor Intelligence 稱,2025 年泰國熱泵市值為 6.2132 億美元,預計到 2031 年將達到 7.8772 億美元,而 2026 年為 6.5041 億美元,預測期(2026-2031 年)的複合成長率為 3.91%。

本報告按供應來源(空氣源、水源等)、技術(空氣對空氣、空氣對水等)、容量(小於10kW、10-50kW等)、應用(空間供暖、空間製冷等)、最終用戶(住宅、商業、工業)、安裝類型(新建、維修)和地區進行細分。市場預測以美元計價。

泰國熱泵市場趨勢與洞察

加速泰國電力發展計畫中的電氣化目標

泰國《2026-2050年電力發展規劃》將可再生能源發電目標提高到2037年達到51%,增加了推動空調和製程加熱負載電氣化的政策壓力。東部經濟走廊不斷成長的工業用電需求已使發電尖峰時段負載捉襟見肘,電網營運商將熱泵視為一種可控負荷,能夠在夜間吸收多餘的太陽能。泰國國家電力局(EGAT)的「能源+」補貼計畫要求五星級認證和智慧電網控制系統的實施作為資格條件,這使得像泰國本田製造公司400kW熱泵機組這樣的計畫得以實施。該項目減少了天然氣的使用,並在2.4年內實現了投資回報。此外,遵守生物循環綠色經濟(BCG)資訊揭露規定進一步鼓勵製造商從燃氣鍋爐轉向熱泵,從而確保在碳排放受限市場中的出口競爭力。

擴大 EGAT 的分時電價系統,以提高熱泵的經濟效益。

泰國國家電力局 (EGAT) 計劃在 2026 年離峰時段尖峰時段電價差擴大至每千瓦時 1.8泰銖(約 0.055 美元),這將使熱泵用戶透過調整用電負載來降低高達 40% 的能源成本。住宿設施迅速利用了這項優惠政策。例如,Rayavadee Krabi 酒店安裝了 100 多台幾乎全部在電價低谷時段運作的變頻熱水器,熱水用電成本降低了 70%。雖然這一價格差異已將完全避開高價時段的混合能源配置的年複合成長率 (CAGR) 提升至 4.61%,但未來三年多電價調整的不確定性意味著這種資金籌措模式仍然面臨挑戰。

與分離式空調系統相比,初始安裝成本較高。

一套典型的10kW住宅機組的安裝成本為18萬至25萬泰銖(約5140至7140美元),是同等功率分離式空調價格的三倍。這使得消費者難以考慮未來節能帶來的兩位數折扣。由於需要專用熱水管道和與多個工種協調,人事費用增加了高達50%。到2025年,僅有12%的商業項目採用基於績效的能源服務公司(ESCO)合約。這是因為租賃方要求採用標準化的計量協議,才能確保共用收益。雖然壓縮機5%至10%的關稅波動增加了預算風險,但當地供應商正在考慮引入國產零件以縮小成本差距。

細分市場分析

至2025年,空氣源熱泵機組將佔泰國熱泵市場62.78%的佔有率。這主要得益於其即插即用的安裝方式,無需鑽孔或連接冷卻塔。曼谷一家中層飯店的商業維修案例凸顯了這種方法的優勢,它能最大限度地減少對飯店營運的干擾,並實現快速運作。水源及地源熱泵系統合計佔28%的佔有率,主要應用於公寓及工業廠房。在這些場所,較高的初始投資可以透過在泰國炎熱季節提高的能源效率來彌補。雖然地源熱泵系統目前仍屬於小眾市場,但它在將地源熱泵作為高階配套設施進行推廣的豪華公寓中正逐漸興起。

混合系統是成長最快的領域,複合年成長率達 4.61%。面臨尖峰時段高成本風險的工業用戶優先考慮採用輔助氣體和電力備用系統實現冗餘,而資料中心則將混合系統視為應對電網不穩定的保障。製造商正在推出改良型蒸汽噴射壓縮機和變速風扇,以將空氣源系統的性能係數 (COP) 下降幅度控制在 15% 以下,即使環境蒸氣超過 38°C 也是如此。

到2025年,空氣-水平台將佔銷售額的48.31%,透過共用熱水循環系統滿足空間冷卻和熱水需求。飯店和醫院尤其青睞其面積小的優勢,因為只需一個機房即可運行,且維護合約集中化。空氣-空氣變冷媒流量(VRF)系統約佔市場佔有率的三分之一,在缺乏冷凍水管道網路的場所廣受歡迎。地下水系統正以5.02%的複合年成長率快速成長,製造商希望全年都能獲得40-80°C的穩定製程溫度,同時根據範圍1揭露要求限制液化石油氣(LPG)的使用。

水-水聯產設計雖然仍屬小眾領域,但代表著技術的尖端水平。 GR TECH 的 HEATAQUA 系統展示了汽電共生的潛力,可同時為食品加工廠提供 5°C 的冷水和 80°C 的熱水。曼谷政府大樓等公共工程正在推廣適用於水基熱泵的熱水循環系統。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速泰國電力發展計畫中的電氣化目標

- 擴大 EGAT 的分時電價制度將提高熱泵的經濟可行性。

- 商業建築節能基金的退款

- 綠色房地產投資信託基金的進入

- 《臭氧層保護法》修正案強制要求過渡到低全球暖化潛勢冷媒。

- 資料中心的發展需要高效冷卻系統

- 市場限制因素

- 初始安裝成本高:與分離式空調系統相比

- 大眾對熱泵的優勢了解有限。

- 售後服務網路分散到大曼谷地區以外。

- 對壓縮機等主要零件徵收的進口關稅波動極大。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按供應來源

- 空氣源

- 水源

- 地熱

- 混合

- 透過技術

- 從空中到空中

- 從空氣到水

- 從水到水

- 從地熱能到水

- 按產能

- 小於10千瓦

- 10~50 kW

- 50~200 kW

- 超過200千瓦

- 透過使用

- 空間暖氣

- 空調

- 家用和衛生熱水

- 工業和製程加熱

- 其他用途

- 最終用戶

- 住宅

- 商業

- 產業

- 按安裝類型

- 新安裝

- 改裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- Glen Dimplex Group

- PHNIX Eco-Energy Solution Ltd.

- Sanden Holdings Corp.(Heat Pump Div.)

- MasterTherm CZ sro

- Mayekawa Mfg. Co., Ltd.(Heat Pump Div.)

- Mitsubishi Electric Corp.

- Johnson Controls International plc

- Aermec SpA

- Alpha Innotec GmbH

- Daikin Applied

- Ochsner Warmepumpen GmbH

- Clivet SpA

- NIBE Industrier AB(NIBE Climate Solutions)

第7章 市場機會與未來展望

According to Mordor Intelligence, the thailand heat pump market size was valued at USD 621.32 million in 2025 and estimated to grow from USD 650.41 million in 2026 to reach USD 787.72 million by 2031, at a CAGR of 3.91% during the forecast period (2026-2031).

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Space Cooling, and More), End User (Residential, Commercial, and Industrial), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Thailand Heat Pump Market Trends and Insights

Accelerating Electrification Targets in Thailand's Power Development Plan

Thailand's 2026-2050 Power Development Plan lifts the renewable-generation target to 51% by 2037, reinforcing policy pressure to electrify space-conditioning and process-heating loads. Rising industrial electricity demand in the Eastern Economic Corridor is already stressing peak generation windows, and grid operators view heat pumps as controllable loads that can absorb overnight solar surplus. EGAT's Energy Plus rebates link eligibility to five-star labels and smart-grid-ready controls, enabling projects such as Thai Honda Manufacturing's 400 kW unit that trimmed natural-gas use and achieved a 2.4-year payback. Compliance with Bio-Circular-Green Economy disclosure rules further incentivizes manufacturers to switch from gas boilers to heat pumps, ensuring export competitiveness in carbon-constrained market.

Extension of EGAT Time-of-Use Tariffs Favoring Heat Pump Economics

EGAT widened the peak-to-off-peak differential to 1.8 THB (USD 0.055) kWh in 2026, cutting levelized energy costs for load-shifting heat-pump users by up to 40%. Hospitality properties have quickly capitalized; Rayavadee Krabi reported 70% hot-water electricity savings after installing more than 100 inverter units that operate almost exclusively during discounted hours. The pricing spread is also spurring a 4.61% CAGR for hybrid configurations that bypass high-tariff windows entirely, although financing models still grapple with tariff-review uncertainty beyond three-year horizons.

High Up-Front Installation Cost Versus Split-Type HVAC Systems

Typical 10 kW residential units cost 180,000-250,000 THB (USD 5,140-7,140) installed, three times the price of comparable split air conditioners, deterring buyers who discount future savings at double-digit rates. Specialized hydronic piping and multi-trade coordination inflate labor outlays by up to 50%. Only 12% of commercial projects in 2025 leveraged performance-based Energy Service Company contracts, as lenders demand standardized measurement protocols before underwriting shared-savings streams. Import-duty swings of 5-10% on compressors compound budgeting risk, although local suppliers are exploring domestically sourced components to narrow the cost gap.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Fund Rebates for Commercial Buildings

- Shift Toward Low-GWP Refrigerants Mandated by Ozone Protection Act Amendments

- Limited Public Awareness of Heat Pump Benefits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air source units delivered 62.78% Thailand heat pump market share in 2025, propelled by plug-and-play installation that avoids drilling or cooling-tower tie-ins. Commercial retrofits in mid-rise Bangkok hotels underline the appeal of minimal disruption and rapid commissioning. Water- and ground-source systems together held 28%, clustered in condominiums and industrial plants where higher capital outlays are offset by efficiency gains during Thailand's hot season. Ground-source installations, though just a niche today, are gathering momentum among luxury condominiums marketing geothermal systems as premium amenities.

Hybrid architectures are the quickest-growing slice at a 4.61% CAGR. Industrial users facing peak-tariff exposure value the redundancy of auxiliary gas or electric backup, while data centers view hybridization as a hedge against grid instability. Manufacturers are rolling out enhanced-vapor-injection compressors and variable-speed fans to keep air-source coefficient-of-performance drops below 15% even when ambient temperatures top 38 °C.

Air-to-water platforms captured 48.31% of 2025 revenue, serving space cooling and hot-water loads from a shared hydronic loop. Hotels and hospitals appreciate the single-plantroom footprint and consolidated maintenance contracts. Air-to-air variable refrigerant flow systems held roughly one-third share, thriving where chilled-water distribution is absent. Ground-to-water solutions are expanding at 5.02% CAGR as manufacturers seek stable year-round 40-80 °C process heat while curbing liquefied-petroleum-gas use under Scope 1 disclosure mandates.

Water-to-water designs remain niche but showcase technical frontiers: GR TECH's HEATAQUA simultaneously produces 5 °C chilled water and 80 °C hot water for food plants, demonstrating co-generation potential. Public projects like the Government Complex Bangkok validate hydronic architectures that favor water-based heat-pump roll-outs.

List of Companies Covered in this Report:

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- Glen Dimplex Group

- PHNIX Eco-Energy Solution Ltd.

- Sanden Holdings Corp. (Heat Pump Div.)

- MasterTherm CZ s.r.o.

- Mayekawa Mfg. Co., Ltd. (Heat Pump Div.)

- Mitsubishi Electric Corp.

- Johnson Controls International plc

- Aermec S.p.A

- Alpha Innotec GmbH

- Daikin Applied

- Ochsner Warmepumpen GmbH

- Clivet SpA

- NIBE Industrier AB (NIBE Climate Solutions)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Electrification Targets in Thailand's Power Development Plan

- 4.2.2 Extension of EGAT Time-of-Use Tariffs Favoring Heat Pump Economics

- 4.2.3 Energy-Efficiency Fund Rebates for Commercial Buildings

- 4.2.4 Crowding-In of Green Real Estate Investment Trusts

- 4.2.5 Shift Toward Low-GWP Refrigerants Mandated by Ozone Protection Act Amendments

- 4.2.6 Growth of Data Centers Requiring High-Efficiency Cooling

- 4.3 Market Restraints

- 4.3.1 High Up-Front Installation Cost Versus Split-Type HVAC Systems

- 4.3.2 Limited Public Awareness of Heat Pump Benefits

- 4.3.3 Fragmented After-Sales Service Network Outside Greater Bangkok

- 4.3.4 Volatile Import Duties on Key Components Such as Compressors

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Stiebel Eltron GmbH & Co. KG

- 6.4.2 Vaillant Group

- 6.4.3 Viessmann Climate Solutions SE

- 6.4.4 Glen Dimplex Group

- 6.4.5 PHNIX Eco-Energy Solution Ltd.

- 6.4.6 Sanden Holdings Corp. (Heat Pump Div.)

- 6.4.7 MasterTherm CZ s.r.o.

- 6.4.8 Mayekawa Mfg. Co., Ltd. (Heat Pump Div.)

- 6.4.9 Mitsubishi Electric Corp.

- 6.4.10 Johnson Controls International plc

- 6.4.11 Aermec S.p.A

- 6.4.12 Alpha Innotec GmbH

- 6.4.13 Daikin Applied

- 6.4.14 Ochsner Warmepumpen GmbH

- 6.4.15 Clivet SpA

- 6.4.16 NIBE Industrier AB (NIBE Climate Solutions)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)