|

市場調查報告書

商品編碼

2061773

越南熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Vietnam Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

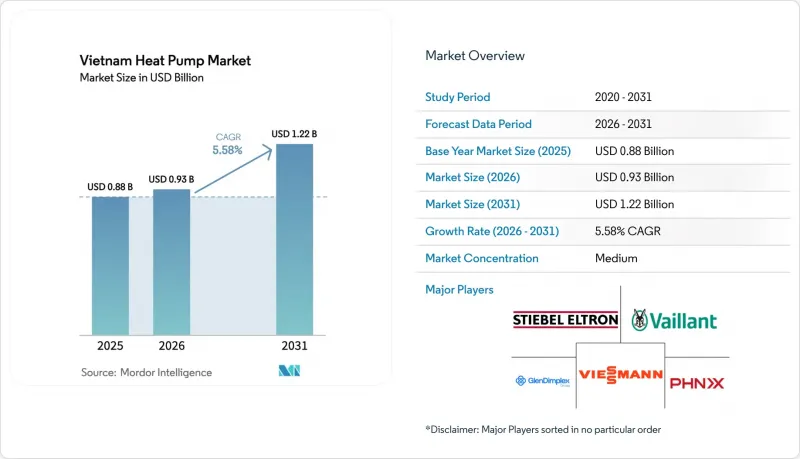

據 Mordor Intelligence 稱,2025 年越南熱泵市場價值 8.8 億美元,預計到 2031 年將從 2026 年的 9.3 億美元成長至 12.2 億美元,預測期(2026-2031 年)複合年成長率為 5.58%。

本報告按熱源類型(空氣源、水源等)、技術(空氣-空氣、空氣-水等)、容量(小於10kW、10-50kW等)、應用(空間供暖、空間冷卻等)、最終用戶(住宅、商業、工業)、安裝類型(新建、維修)和地區進行細分。市場預測以美元計價。

越南熱泵市場趨勢與洞察

加速推出政府補貼和無息綠色貸款。

資金籌措成本的降低正開始改變消費者的購買行為,尤其是一些小規模連鎖飯店和公寓管理協會,他們先前往往推遲升級到更有效率的系統。商業金融機構正在綠色貸款產品中納入2%的利息補貼,使得中層建築熱水系統的月供低於節能帶來的收益,從而為借款人創造即時的正現金流。據安裝商稱,2026年1月至3月期間,胡志明市R32冷熱水熱泵的訂單積壓量加倍。這一激增是由於買家爭相在配額用完前鎖定優惠條件。製造商也積極回應,提供包含設備、監控軟體和預填申請表格的「貸款就緒」套餐,降低了不熟悉綠色金融文件的終端用戶的交易門檻。預計在未來兩年內,這項政策主導的資金支持將使許多商業設施中熱泵和燃氣熱水器的投資回收期差距縮小到三年以內,從而帶來強勁的短期需求。

都市區強制淘汰低效電熱水器

QCVN 25:2025 規定的合規期限迫使物業管理人員檢查其設備並製定多年更換計畫。如今,城市檢查員在例行安全檢查中會核查能源證書記錄,老舊電阻式熱水器的用戶除了面臨電費上漲的風險外,還可能面臨罰款,這加速了他們更換技術的進程。河內的零售連鎖店已經將低效儲水式熱水器下商店,取而代之的是符合 2025 年最低性能標準的變頻熱泵熱水器。保險公司也表示,不符合標準的設備可能會導致火災風險保險失效,這無疑是在監管「胡蘿蔔」之外又增加了一項經濟「大棒」。隨著法規的實施範圍從一線城市擴展到二線城市,預計需求浪潮將蔓延至整個分銷管道,兩位數的出貨量成長預計將持續到 2029 年。

水產養殖業對低碳加熱系統的需求日益成長

以出口為導向的蝦類和巴沙魚養殖場面臨著巨大的壓力,需要證明其在第一階段(Scope 1)的排放目標上實現了減排,才能維持與歐洲和北美買家的契約,因為這些地區即將實施碳排放調整費。早期試點計畫表明,水源熱泵可以降低柴油消耗,同時將幼蝦存活率提高6-8個百分點,這項營運效益受到了養殖場管理者的廣泛好評。氣候變遷保險政策目前為採用電氣化技術的孵化場提供保費折扣,使這項提案更具吸引力。為了保護其價值100億美元的水產品出口產業,各州政府正在共同資助試點項目,向小規模企業展示其成本節約效益。隨著碳權現貨價格在2028年市場啟動前上漲,透過熱泵專案累積檢驗減排量的養殖場將獲得可交易的收入來源,從而增強專案的經濟可行性。

細分市場分析

預計到2025年,空氣源熱泵系統將佔越南熱泵市場佔有率的68.78%。這主要歸功於適宜的環境溫度、廣泛的分銷網路以及便捷的安裝方式。隨著商業和工業用戶對沖電價尖峰時段和電網不穩定風險,將熱泵與燃氣或生質能鍋爐相結合的混合式設計預計將以7.13%的複合年成長率成長。儘管越南水源熱泵市場規模仍然小規模,但沿海度假勝地和水產養殖業的試點計畫表明,該細分市場具有長期成長潛力。地熱能的廣泛應用受到都市區土地稀缺和鑽井成本的限制,目前僅限於資料中心園區和新建工業園區等可以從一開始就規劃垂直鑽孔的場所。

河內和胡志明市的開發商正擴大預裝符合2029年冷媒法規的R32冷媒空氣源熱泵機組,減輕居民的維修負擔。同時,製造商正在對室外機盤管和變頻驅動裝置進行微調,以適應夏季高濕度和35-40°C高溫的氣候條件,即使在部分負載下也能保持4.5或更高的季節能源效率比(SEER)。這些進步進一步增強了空氣源熱泵的優勢,而工業電氣化的推進和冷媒的逐步淘汰也為地源熱泵和水源熱泵在特定應用領域的推廣提供了契機。

到2025年,空氣-水系統將佔越南熱泵市場60.31%的佔有率,因為飯店、醫院和公寓優先考慮熱水和地暖循環系統。隨著資料中心尋求廢熱回收,以及湄公河三角洲孵化場採用地熱循環系統在極端天氣下穩定水溫,預計越南地下水機組的市場佔有率將上升。空氣-空氣分離式空調機組在南部省份的冷凍應用中佔據主導地位,但運作較少,限制了其對市場擴張的貢獻。水-水系統則應用於城市改造區域的區域冷卻系統中,其中中央冷水機組整合了熱回收冷卻器,無需額外電力輸入即可提供製程或生活熱水。

平陽省的資料中心和園區開發商正在試驗雙溫水熱循環系統,該系統利用地下水熱泵回收30°C的伺服器廢熱,並將其加熱至60°C的製程用水,無需輔助增壓裝置。同時,水產養殖戶更傾向於使用與模組化水-水單元連接的閉式循環池塘盤管,因為這種盤管具有耐腐蝕性,並且在雨季期間性能係數(COP)穩定。設備製造商提供工廠預製撬裝模組,將設計時間從數月縮短至數週。這對於需要趕工以滿足出口認證審核的專案來說是一項顯著優勢。監測平台彙整現場數據,使投資者對系統的長期性能更有信心,從而降低融資成本,並縮小與主流空氣-水系統的成本差距。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 產業價值鏈分析

- 市場促進因素

- 加速推出政府補貼和無息綠色貸款。

- 都市區強制淘汰低效電熱水器

- 一線城市高層建築住宅的快速建設熱潮

- 水產養殖業對低碳加熱系統的需求日益成長

- 將熱泵整合到超大規模資料中心的廢熱回收系統中

- 即將禁止使用R22冷媒正在推動維修需求。

- 市場限制因素

- 高昂的初始設備和安裝成本

- 持證熱泵技術人員短缺

- 可用於興建地下環形場的土地有限。

- 工業天然氣價格相對於電力價格的優勢

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按供應來源

- 空氣源

- 水源

- 地熱

- 混合

- 透過技術

- 從空中到空中

- 從空氣到水

- 水到水

- 從地熱能到水

- 按產能

- 小於10千瓦

- 10~50 kW

- 50~200 kW

- 超過200千瓦

- 透過使用

- 空間暖氣

- 空間冷卻

- 家用和衛生熱水

- 工業和製程加熱

- 其他用途

- 最終用戶

- 住宅

- 商業

- 產業

- 按安裝類型

- 新安裝

- 改裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Daikin Industries Ltd.

- Panasonic Holdings Corp.

- Mitsubishi Electric Corp.

- Midea Group Co. Ltd.

- Gree Electric Appliances Inc. of Zhuhai

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- Glen Dimplex Group

- WaterFurnace International Inc.

- PHNIX Eco-Energy Solution Ltd.

- Thermia Heat Pumps AB

- Sanden Holdings Corp.(Heat Pump Div.)

- Enertech Global LLC

- Ecoforest Geotermia SL

- MasterTherm CZ sro

- Mayekawa Mfg. Co. Ltd.(Heat Pump Div.)

- Clade Engineering Systems Ltd.

- Calorex Heat Pumps Ltd.

- Aermec SpA

- Alpha Innotec GmbH

- Heliotherm Warmepumpentechnik GmbH

- Ochsner Warmepumpen GmbH

- Clivet SpA

- Hitachi Air Conditioning

第7章 市場機會與未來展望

According to Mordor Intelligence, the vietnam heat pump market size was valued at USD 0.88 billion in 2025 and estimated to grow from USD 0.93 billion in 2026 to reach USD 1.22 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031).

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Space Cooling, and More), End User (Residential, Commercial, and Industrial), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Heat Pump Market Trends and Insights

Accelerated Roll-out of Government Subsidies and Zero-Interest Green Loans

Cheaper capital is beginning to reshape buying behavior, especially among small hotel chains and condominium associations that historically delayed high-efficiency upgrades. As commercial lenders embed the 2% interest subsidy in their green-loan products, monthly installments for a mid-rise hot-water plant fall below the cash savings from lower electricity use, creating immediate positive cash flow for borrowers. Installation contractors report that order backlogs for R32 air-to-water units in Ho Chi Minh City doubled between January and March 2026, a shift they attribute to buyers racing to lock in concessional terms before any quota caps are reached. Manufacturers are responding by offering "loan-ready" packages that bundle equipment, monitoring software, and pre-filled application documents, reducing transaction friction for end users who lack experience with green-finance paperwork. Over the next two years, this policy-driven liquidity is expected to narrow the payback gap between heat pumps and gas heaters to less than three years for many commercial sites, firmly anchoring demand in the short term.

Mandatory Phase-Out of Inefficient Electric Water Heaters in Urban Areas

Compliance deadlines embedded in QCVN 25:2025 are forcing property managers to audit appliance fleets and draft multi-year replacement schedules. Because municipal inspectors now review energy-certificate logs during routine safety checks, owners of older resistance heaters are exposed to fines as well as higher electricity bills, accelerating their decision to switch technologies. Retail chains in Hanoi have already removed low-efficiency storage heaters from shelves, replacing them with inverter-driven heat-pump models that meet the 2025 minimum-performance threshold. Insurance firms are also signaling that non-compliant equipment could void fire-risk coverage, adding a financial stick to the regulatory carrot. As enforcement radiates from tier-1 to tier-2 cities, a rolling wave of demand is expected to cascade through the distribution channel, sustaining double-digit shipment growth through 2029.

Rising Demand for Low-Carbon Aquaculture Heating Systems

Export-oriented shrimp and pangasius farms are under pressure to document Scope 1 reductions to retain buyer contracts in Europe and North America, where carbon-adjustment fees loom. Early pilots show that water-source heat pumps can lift larval survival rates by 6-8 percentage points while trimming diesel usage, an operational win that resonates with farm managers. Climate-linked insurance policies now offer premium discounts for electrified hatcheries, further sweetening the value proposition. Provincial authorities, keen to safeguard a USD 10 billion seafood export sector, are co-financing demonstration plants to showcase cost savings to smaller operators. As carbon-credit spot prices rise ahead of the 2028 market launch, farms that bank verified reductions via heat-pump projects will gain a tradable revenue stream that enhances project economics.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Residential High-Rise Construction Boom in Tier-1 Cities

- High Upfront Equipment and Installation Cost

- Shortage of Certified Heat-Pump Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-source systems accounted for 68.78% of the Vietnam heat pump market share in 2025, underpinned by favorable ambient temperatures, widespread dealer networks, and lower installation complexity. Hybrid designs pairing heat pumps with gas or biomass boilers are set for a 7.13% CAGR as commercial and industrial users hedge against peak-hour electricity prices and grid instability. The Vietnam heat pump market size for water-source solutions remains modest, yet pilots in coastal resorts and aquaculture hint at long-term niche expansion. Ground-source uptake is inhibited by urban land scarcity and drilling costs, restricting deployments to data-center campuses and greenfield industrial parks where vertical boreholes can be planned from the outset.

Developers in Hanoi and Ho Chi Minh City increasingly pre-install R32-charged air-source units that meet 2029 refrigerant rules, cutting retrofit headaches for residents. Meanwhile, manufacturers fine-tune outdoor coils and inverter drives for humid, 35-40 °C summer conditions, sustaining seasonal performance factors above 4.5 even at partial load. These advances reinforce air-source hegemony, yet rising industrial electrification and refrigerant phase-outs are opening beachheads for ground- and water-source configurations in specialized applications.

Air-to-water equipment captured 60.31% of the Vietnam heat pump market size in 2025 as hotels, hospitals, and condominiums prioritized domestic hot water and radiant floor loops. The Vietnam heat pump market share for ground-to-water units will rise as data centers pursue waste-heat recovery and Mekong Delta hatcheries deploy geothermal loops to stabilize water temperatures during extreme weather events. Air-to-air split units dominate southern provinces for cooling but seldom run in heating mode, curbing their incremental contribution. Water-to-water machines serve district cooling schemes in urban redevelopment zones, where central chilled-water plants integrate heat-recovery chillers to deliver process or sanitary hot water without extra electrical input.

Developers of data-center campuses in Binh Duong are piloting dual-temperature hydronic loops that let ground-to-water heat pumps scavenge 30 °C server exhaust and elevate it to 60 °C process water without auxiliary boosters. Aquaculture operators, meanwhile, favor sealed-loop pond coils linked to modular water-to-water units, citing corrosion resistance and stable COPs during monsoon season. Equipment makers are responding with factory-prefabricated skid modules that compress design timelines from months to weeks, an advantage for fast-track projects racing to meet export certification audits. As monitoring platforms aggregate field data, financiers gain confidence in long-term performance, unlocking cheaper debt that narrows the cost differential with mainstream air-to-water systems.

List of Companies Covered in this Report:

- Daikin Industries Ltd.

- Panasonic Holdings Corp.

- Mitsubishi Electric Corp.

- Midea Group Co. Ltd.

- Gree Electric Appliances Inc. of Zhuhai

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- Glen Dimplex Group

- WaterFurnace International Inc.

- PHNIX Eco-Energy Solution Ltd.

- Thermia Heat Pumps AB

- Sanden Holdings Corp. (Heat Pump Div.)

- Enertech Global LLC

- Ecoforest Geotermia S.L.

- MasterTherm CZ s.r.o.

- Mayekawa Mfg. Co. Ltd. (Heat Pump Div.)

- Clade Engineering Systems Ltd.

- Calorex Heat Pumps Ltd.

- Aermec S.p.A

- Alpha Innotec GmbH

- Heliotherm Warmepumpentechnik GmbH

- Ochsner Warmepumpen GmbH

- Clivet SpA

- Hitachi Air Conditioning

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Market Drivers

- 4.3.1 Accelerated Roll-out of Government Subsidies and Zero-Interest Green Loans

- 4.3.2 Mandatory Phase-Out of Inefficient Electric Water Heaters in Urban Areas

- 4.3.3 Rapid Residential High-Rise Construction Boom in Tier-1 Cities

- 4.3.4 Rising Demand for Low-Carbon Aquaculture Heating Systems

- 4.3.5 Heat-Pump Integration in Hyperscale Data-Center Waste-Heat Recovery

- 4.3.6 Impending Ban on R22 Refrigerant Driving Retrofit Demand

- 4.4 Market Restraints

- 4.4.1 High Upfront Equipment and Installation Cost

- 4.4.2 Shortage of Certified Heat-Pump Technicians

- 4.4.3 Limited Available Land for Ground-Source Loop Fields

- 4.4.4 Industrial Natural-Gas Tariff Advantage Over Electricity Prices

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries Ltd.

- 6.4.2 Panasonic Holdings Corp.

- 6.4.3 Mitsubishi Electric Corp.

- 6.4.4 Midea Group Co. Ltd.

- 6.4.5 Gree Electric Appliances Inc. of Zhuhai

- 6.4.6 Stiebel Eltron GmbH & Co. KG

- 6.4.7 Vaillant Group

- 6.4.8 Viessmann Climate Solutions SE

- 6.4.9 Glen Dimplex Group

- 6.4.10 WaterFurnace International Inc.

- 6.4.11 PHNIX Eco-Energy Solution Ltd.

- 6.4.12 Thermia Heat Pumps AB

- 6.4.13 Sanden Holdings Corp. (Heat Pump Div.)

- 6.4.14 Enertech Global LLC

- 6.4.15 Ecoforest Geotermia S.L.

- 6.4.16 MasterTherm CZ s.r.o.

- 6.4.17 Mayekawa Mfg. Co. Ltd. (Heat Pump Div.)

- 6.4.18 Clade Engineering Systems Ltd.

- 6.4.19 Calorex Heat Pumps Ltd.

- 6.4.20 Aermec S.p.A

- 6.4.21 Alpha Innotec GmbH

- 6.4.22 Heliotherm Warmepumpentechnik GmbH

- 6.4.23 Ochsner Warmepumpen GmbH

- 6.4.24 Clivet SpA

- 6.4.25 Hitachi Air Conditioning

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)