|

市場調查報告書

商品編碼

2061771

印度熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

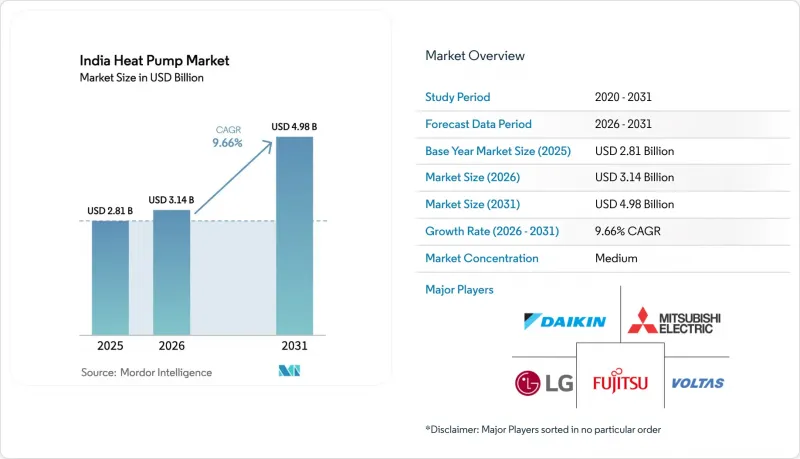

根據 Mordor Intelligence 預測,印度熱泵市場規模將從 2025 年的 28.1 億美元成長到 2026 年的 31.4 億美元,到 2031 年將達到 49.8 億美元,2026 年至 2031 年的複合年成長率預計為 9.66%。

本報告按熱源類型(空氣源、水源等)、技術(空氣-空氣、空氣-水等)、容量(小於10kW、10-50kW等)、應用(空間供暖、空間冷卻等)、最終用戶(住宅、商業、工業)、安裝類型(新建、維修)和地區進行細分。市場預測以美元計價。

印度熱泵市場趨勢與洞察

實施政府獎勵,例如生產關聯激勵計劃和消費稅減免,以促進節能型暖通空調技術的發展。

生產連結獎勵計畫(PLI)框架下的財政支持降低了對零件進口的依賴,使本地壓縮機和熱交換器製造商獲得了成本優勢。 2025年9月商品及服務稅(GST)的下調將使零售價格降低高達12%,縮短首次購買住宅熱泵的消費者的投資回收期。印度能源效率局(BEE)於2026年1月實施的更嚴格的星級評定標準提高了能源效率閾值。這有利於研發能力強的公司,但使小規模的組裝製造商處於不利地位。各邦的政策也提供了進一步的獎勵。古吉拉突邦提供高達200萬印度盧比(約2萬美元)的資本補貼,而泰米爾納德邦則強制要求在新城區進行區域供冷調查,導致各地在熱泵普及率方面存在差異。這些措施共同推動印度熱泵市場朝向符合新標籤規定的優質高效機型發展。

快速的都市化、不斷成長的可支配收入以及住宅建設熱潮。

印度每年新增約1,000萬名城市居民,2024年住宅量成長21%。這推動了對緊湊、易於安裝的空氣源熱泵的需求。 2024年人均收入達到18.5萬盧比(約1985美元),擴大了中產階級的規模,使他們能夠負擔得起高效的供暖、製冷和熱水解決方案。雖然空氣源系統更受人口密集的都市區地區的青睞,但列城機場的大規模熱項目和印度陸軍的淨零排放設施表明,高階項目的開發商正在試點地熱系統的設計。都市區消費者重視靜音運作和智慧控制功能,促使品牌商即使在10度以下的產品中也融入物聯網功能。因此,印度熱泵市場正持續從提升基本舒適度的設備轉向連網的高效解決方案。

前期投入成本高,資金籌措管道有限。

工業級系統的價格依容量不同,介於150萬至1,200萬印度盧比(約0.016至13萬美元)之間,系統整合費用最高可達30%。地熱能源專案(例如列城機場的457口鑽孔)需要鑽探110至120公尺深的鑽孔,這可能會超出大多數開發商的預算。由於銀行將熱泵歸類為專用設備,因此它們不屬於常規營運資金貸款的範疇,儘管能源效率服務有限公司(Energy Efficiency Services Limited)試驗計畫,但補貼貸款仍然有限。 18至48個月的投資回收期,遠長於中小製造商偏好的12個月,阻礙了熱泵在印度市場的廣泛普及。

細分市場分析

2025年,空氣源熱泵系統將佔據印度熱泵市場70.31%的佔有率。這主要歸功於其較低的初始成本以及安裝人員的熟悉程度。水源熱泵機組主要面向特定區域供冷和工業循環應用,而混合系統雖然提供故障容錯功能作為備用方案,但卻削弱了脫碳效益。另一方面,地熱系統預計將以11.31%的複合年成長率成長,這得益於財政獎勵以及一些引人注目的項目,例如列城機場2500千瓦的地熱系統項目。該計畫鑽探了457口井,以確保即使在零度以下的冬季也能保持穩定的效率。對於高海拔和高溫地區的機構投資者而言,這項技術是一個極具吸引力的選擇,因為它即使在極端戶外條件下也能高效運作。

儘管空氣源產品在住宅維修項目中佔據主導地位,但其性能係數會隨著溫度每升高1攝氏度(超過設計閾值),下降2-3%,這給北部平原等夏季高溫超過47攝氏度的地區帶來了運行挑戰。乾旱地區的用水限制也限制了水源設計的應用。混合系統在停電期間會切換到石化燃料燃燒器,這使得排碳權框架下的排放計算變得複雜。雖然鑽探成本高昂,但地熱政策下的加速折舊正鼓勵機場、國防設施和豪華地產開發商採用地熱解決方案,從而推動印度熱泵市場的戰略發展。

到2025年,採用小型機組供應熱水和熱水加熱的空氣源熱泵系統將佔62.29%的市場佔有率。雖然空氣源熱泵系統仍廣泛應用於零售商店和辦公室的製冷,但水源熱泵系統正被應用於封閉回路型工業流程。由於地溫穩定,地源熱泵系統無需備用熱源即可在高達65 度C的溫度下提供熱水,並保持4或更高的能源效率比(COP),預計其市場將以11.52%的複合年成長率成長。印度熱泵市場也正向高溫二氧化碳系統轉型。 Triveni Turbines公司額定溫度為122°C的機組已在製藥和食品加工生產線中實現了6的能源效率比。

住宅用戶更傾向於容量200-500公升的即插即用型空氣源熱水器,例如Racod公司提供的產品,價格在199,999印度盧比(約2,147美元)至299,000印度盧比(約3,220美元)之間,能源效率比(COP)可達4.4或更高。相較之下,地源熱泵系統,例如那格浦爾地鐵大樓(Nagpur Metro Bhavan)的175噸系統,可將傳統冷卻器的能耗從每噸1.6千瓦降至每噸0.6千瓦,並在4.3年內實現投資回報。古吉拉突邦化工行業的水源熱泵維修降低了38%的能耗,並在18個月內實現了投資回報,這表明,當資金籌措降低時,工業用戶樂於接受新技術。這些趨勢支撐了印度熱泵市場在各種技術領域的持續成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府獎勵,例如生產關聯激勵計劃和消費稅減免,旨在鼓勵使用節能型暖通空調系統。

- 快速的都市化、不斷成長的可支配收入和住宅建設熱潮

- 電費上漲推動了對高能源效率比暖氣和冷氣解決方案的需求。

- 各國為促進供暖電氣化而製定的可再生能源和脫碳目標。

- 智慧城市中微型公用事業熱泵計畫的示範效果

- 資料中心擴建需要採用製程熱泵進行低 PUE溫度控管。

- 市場限制因素

- 前期實施成本高,且資金籌措管道有限。

- 合格的熱泵安裝人員和服務技術人員短缺

- 電網堵塞罰款限制了工業叢集中大規模熱泵的部署。

- 在多塵環境下效能下降,導致維護成本增加

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按供應來源

- 空氣源

- 水源

- 地熱

- 混合

- 透過技術

- 空對空

- 空氣中的水

- 水-水

- 來自地下的水(土壤)

- 按產能

- 小於10千瓦

- 10~50 kW

- 50~200 kW

- 超過200千瓦

- 透過使用

- 空間暖氣

- 空間冷卻

- 家用和衛生熱水

- 工業和製程加熱

- 其他用途

- 最終用戶

- 住宅

- 商業

- 產業

- 按安裝類型

- 新安裝

- 改裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Daikin Industries, Ltd.

- Mitsubishi Electric Corp.

- NIBE Industrier AB

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- Glen Dimplex Group

- Blue Star Limited

- Voltas Limited

- LG Electronics India Pvt. Ltd.

- Thermia Heat Pumps AB

- Bosch Thermotechnology GmbH

- Panasonic Heating and Cooling Solutions

- Fujitsu General Ltd.

- Carrier Global Corp.

- Trane Technologies plc

- Johnson Controls-Hitachi Air Conditioning

- Danfoss A/S(Heating Segment)

第7章 市場機會與未來展望

According to Mordor Intelligence, the india heat pump market size is expected to increase from USD 2.81 billion in 2025 to USD 3.14 billion in 2026 and reach USD 4.98 billion by 2031, growing at a CAGR of 9.66% over 2026-2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Space Cooling, and More), End User (Residential, Commercial, and Industrial), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

India Heat Pump Market Trends and Insights

Implementation of Government Incentives such as PLI Scheme and GST Reductions for Energy-Efficient HVAC

Financial support under the Production Linked Incentive framework lowers component import dependence, giving local compressor and heat-exchanger production a cost edge. The September 2025 Goods and Services Tax cut reduced retail prices by up to 12%, shortening payback periods for first-time residential buyers. Stricter Bureau of Energy Efficiency star-rating norms that took effect in January 2026 raised efficiency thresholds, benefitting firms with strong R&D capability but squeezing smaller assemblers. State policies layer additional incentives: Gujarat offers capital subsidies of up to INR 2 million (USD 0.02 million), while Tamil Nadu mandates district-cooling studies in new urban zones, creating uneven regional uptake. Combined, these measures tilt the India heat pump market toward premium, high-efficiency models that comply with new labeling rules.

Rapid Urbanization, Rising Disposable Income and Residential Construction Boom

India adds roughly 10 million urban residents each year, and housing launches grew 21% in 2024, reinforcing demand for compact, plug-and-play air-to-water units. Per-capita income climbed to INR 185,000 (USD 1,985) in FY 2024, enlarging the middle-class cohort that can finance efficient cooling and hot-water solutions. While dense city plots favor air source systems, marquee geothermal projects at Leh Airport and an Indian Army net-zero facility signal that developers of premium projects are testing ground source designs. Urban consumers value quiet operation and smart-controls integration, nudging brands to bundle Internet of Things features even in sub-10 kW offerings. As a result, the India heat pump market continues to shift from basic comfort appliances toward connected, high-efficiency solutions.

High Upfront Installation Costs and Limited Financing Options

Industrial-grade systems cost INR 1.5-12 million (USD 0.016-0.13 million) depending on capacity, with integration adding up to 30% extra outlay. Drilling 110-120 m boreholes for ground source projects, such as the 457 holes at Leh Airport, can push project budgets beyond the comfort zone of most developers. Banks classify heat pumps as specialized equipment, sidelining them from standard working-capital credit lines, and subsidized loans remain scarce despite pilot programs by Energy Efficiency Services Limited. Payback periods of 18-48 months exceed the 12-month horizon preferred by small manufacturers, delaying broader penetration of the India heat pump market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Electricity Costs Driving Demand for High-COP Heating and Cooling Solutions

- National Renewable-Energy and Decarbonization Targets Promoting Electrification of Heating

- Shortage of Certified Heat-Pump Installers and Service Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air source systems held 70.31% of the India heat pump market share in 2025 thanks to lower upfront costs and installer familiarity. Water source units cater to niche district-cooling and industrial loops, whereas hybrids provide backup resiliency but dilute decarbonization gains. Ground source units, however, are projected to grow at an 11.31% CAGR, buoyed by fiscal incentives and headline projects like the 2,500 kW Leh Airport installation that drilled 457 boreholes to maintain stable efficiency in sub-zero winters. The technology's ability to operate efficiently at ambient extremes positions it well for institutional buyers across high-altitude and high-heat regions.

While air source products dominate residential retrofits, their coefficient of performance drops 2-3% for every 1 °C rise beyond design conditions, challenging operations when summer peaks top 47 °C in the northern plains. Regulatory water-extraction limits in drought-prone states curb wider use of water source designs. Hybrid setups switch to fossil burners during outages, complicating emissions accounting under the carbon-credit framework. Despite higher drilling expenses, accelerated depreciation under the geothermal policy is persuading airports, defense campuses, and premium real-estate developers to opt for ground source solutions, expanding the strategic canvas of the India heat pump market.

Air-to-water designs captured 62.29% share in 2025 by supplying domestic hot water and hydronic heating from compact packages. Air-to-air variants remain common in retail and office cooling, whereas water-to-water units serve closed-loop industrial processes. Ground-to-water solutions are forecast to expand at an 11.52% CAGR, aided by stable ground temperatures that keep coefficients of performance above 4 while delivering up to 65 °C without backup heat. The India heat pump market is also witnessing a pivot to high-temperature carbon-dioxide systems: Triveni Turbines' 122 °C unit shows a coefficient of performance of 6 for pharmaceutical and food-processing lines.

Residential buyers favor plug-and-play 200-500 L air-to-water cylinders such as Racold's range, priced between INR 199,999 (USD 2,147) and INR 299,000 (USD 3,220), delivering coefficients of performance above 4.4. In contrast, ground-to-water installations like Nagpur Metro Bhavan's 175-ton system cut power demand from 1.6 kW/ton for conventional chillers to 0.6 kW/ton, achieving payback in 4.3 years. Water-to-water retrofits in Gujarat's chemical sector have slashed energy by 38% with 18-month returns, proving that industrial users are ready to adopt once financing hurdles ease. Together, these developments reinforce the upward trajectory of the India heat pump market across diversified technologies.

List of Companies Covered in this Report:

- Daikin Industries, Ltd.

- Mitsubishi Electric Corp.

- NIBE Industrier AB

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- Glen Dimplex Group

- Blue Star Limited

- Voltas Limited

- LG Electronics India Pvt. Ltd.

- Thermia Heat Pumps AB

- Bosch Thermotechnology GmbH

- Panasonic Heating and Cooling Solutions

- Fujitsu General Ltd.

- Carrier Global Corp.

- Trane Technologies plc

- Johnson Controls-Hitachi Air Conditioning

- Danfoss A/S (Heating Segment)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Implementation of Government Incentives Such as PLI Scheme and GST Reductions for Energy-Efficient HVAC

- 4.2.2 Rapid Urbanization, Rising Disposable Income and Residential Construction Boom

- 4.2.3 Increasing Electricity Costs Driving Demand for High-COP Heating and Cooling Solutions

- 4.2.4 National Renewable Energy and Decarbonization Targets Promoting Electrification of Heating

- 4.2.5 Micro-Utility Heat Pump Projects in Smart Cities Creating Demonstration Effect

- 4.2.6 Expansion of Data Centers Requiring Low-PUE Thermal Management Using Process Heat Pumps

- 4.3 Market Restraints

- 4.3.1 High Upfront Installation Costs and Limited Financing Options

- 4.3.2 Shortage of Certified Heat Pump Installers and Service Technicians

- 4.3.3 Grid Congestion Penalties Limiting Large-Scale Heat Pump Adoption in Industrial Clusters

- 4.3.4 Performance Degradation in High-Ambient Dusty Conditions Increasing Maintenance Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries, Ltd.

- 6.4.2 Mitsubishi Electric Corp.

- 6.4.3 NIBE Industrier AB

- 6.4.4 Stiebel Eltron GmbH & Co. KG

- 6.4.5 Vaillant Group

- 6.4.6 Viessmann Climate Solutions SE

- 6.4.7 Glen Dimplex Group

- 6.4.8 Blue Star Limited

- 6.4.9 Voltas Limited

- 6.4.10 LG Electronics India Pvt. Ltd.

- 6.4.11 Thermia Heat Pumps AB

- 6.4.12 Bosch Thermotechnology GmbH

- 6.4.13 Panasonic Heating and Cooling Solutions

- 6.4.14 Fujitsu General Ltd.

- 6.4.15 Carrier Global Corp.

- 6.4.16 Trane Technologies plc

- 6.4.17 Johnson Controls-Hitachi Air Conditioning

- 6.4.18 Danfoss A/S (Heating Segment)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)