|

市場調查報告書

商品編碼

2061767

日本熱泵市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)Japan Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

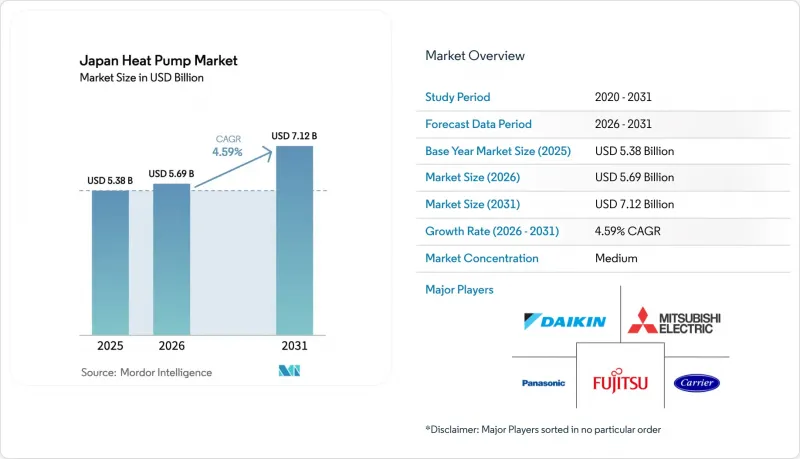

根據 Mordor Intelligence 預測,日本熱泵市場預計將從 2025 年的 53.8 億美元成長到 2026 年的 56.9 億美元,到 2031 年達到 71.2 億美元,2026 年至 2031 年的複合年成長率為 4.59%。

本報告按熱源類型(空氣源、水源等)、技術(空氣-空氣、空氣-水等)、容量(小於10kW、10-50kW等)、應用(空間供暖、工業/工藝供暖等)、最終用戶(住宅、商業設施等)、安裝類型(新建、維修)和地區進行分類。市場預測以美元計價。

日本熱泵市場趨勢與洞察

政府政策和獎勵的實施,以促進節能型暖通空調系統的推廣。

2026年推出的慷慨補貼計畫將為從傳統燃油燃氣鍋爐更換為節能鍋爐的住宅提供高達40%的設備和安裝費用補貼,立即提振了累積訂單。北海道和青森縣的地方補貼計畫進一步減輕了屋主1000至2000美元的實際負擔,緩解了他們對嚴寒冬季供暖性能的擔憂。 2025年4月實施的強制性能源標準有效地淘汰了新建住宅中的低效率供暖設備,推動了對變頻空氣源熱泵的需求,這類設備的價格比傳統旗艦機型高出約18%。 2026年GX排放交易體系下的碳定價將對工業二氧化碳排放徵收17至21美元的影子成本,鼓勵工廠轉型使用高溫熱泵。 《能源合理化法》允許的加速折舊正在縮短商業設施維修的投資回收期。

日本GX藍圖中的電氣化目標

該藍圖將熱泵定位為到2030年替代800萬千升油當量能源的主導技術,並將設備部署與日本的淨零排放目標掛鉤。一項於2026年1月啟動的電網級需量反應示範項目,將向減少用電量的家庭支付每千瓦時最高0.10美元的補貼,從而緩解此前令東京電力公司電網不堪重負的晚間用電高峰需求。鑑於電力公司被要求在2030年確保20吉瓦的靈活供給能力,大型熱泵電站與儲熱系統結合,現在有資格獲得容量補償,從而改善了專案的收入結構。大金和日立共同開發的即時定價分析技術,使商業營運成本降低了約13%,展現了智慧控制和電網服務的良性循環。這些措施共同加強了政策和技術協調,以支持長期需求。

安裝難度高且安裝成本高

地熱能源專案需要鑽探50至100公尺深的鑽孔並維修熱水管道,這將使預算增加2萬至3.3萬美元,工期延長至多六週。在人口稠密、地塊邊界狹窄的都市區地區,必須進行成本高昂的垂直鑽探,這將額外增加5,300至8,000美元的成本。設計用於80攝氏度熱水的傳統散熱器通常需要擴大尺寸,這將使成本翻倍並延長運作。由於擔心地震多發地區鑽孔的完整性,42%的承包商完全避免承接此類工作。 《建築標準法》中的退讓規定進一步限制了小規模地塊的可行性,並增加了軟成本的風險。

細分市場分析

2025年,空氣源熱泵在日本熱泵市場佔有53.81%的銷售佔有率。其主導地位源於空氣源熱泵相對較低的初始成本以及在溫暖的沿海地區易於安裝。同時,水源和地源熱泵的總合佔有率維持在12%左右。這是由於鑽井和水源獲取的複雜性日益增加,使得它們難以在許多都市區計畫中實施。混合型熱泵雖然仍佔少數,但正以每年5.31%的速度成長。這是因為住宅和建築管理人員重視在電價高企或極端寒冷天氣導致效率下降時,能夠靈活切換使用電力和燃氣。這一趨勢在北海道嚴寒的冬季尤為明顯。東京瓦斯公司決定從2026年4月起停止銷售獨立式瓦斯熱水器,凸顯並推動了向雙燃料系統轉型的趨勢。

在政府補貼的資助下,能夠處理高達90°C水溫的二氧化碳混合式熱水器預計到2027年年產量將達到5萬台,直接滿足了人們對特定洗澡水溫度的需求,而這一初級能源35%至40%。住友林業計劃在小樽市開展一項針對200戶家庭的試點項目,該項目展示瞭如何透過地方政府、開發人員和原始設備製造商(OEM)之間的合作,即使在地震多發地區,也能實現地熱能利用的經濟可行性。這些趨勢,加上純電動產品性能的提升,正促使混合系統成為切實可行的過渡方案。

由於空氣-水式熱水器與日本現有的熱水散熱器系統無縫相容,且可透過變頻驅動實現寬廣的輸出調節範圍,預計到2025年,空氣-水式熱水器的銷售額將佔總銷售額的48.62%。然而,地下水式熱水器系統正以5.02%的複合年成長率(CAGR)保持著最快的成長速度,這主要得益於市政試點項目,這些項目展示了季節性能係數(COP)超過4.5,初級能源消耗降低率超過40%。位於尾形村的1.2兆瓦循環系統已在實際運作中展現節能效果,目前正在影響補貼評估。同時,小樽市正在興建的大型季節性蓄熱設施可望進一步驗證其節能效果。空氣-空氣式熱水器在銷售方面仍然佔據主導地位,但由於其組件結構更簡單、更換週期更短,因此其單位銷售額佔比較低。

儘管水-水系統仍處於小眾領域,但其戰略地位舉足輕重。沿海資料中心安裝的海水熱源設備可回收鍋爐給水中的廢熱,每年可減少數萬噸二氧化碳排放。 JERA位於橫濱的3兆瓦電站吸引了整個公共產業行業經營團隊對可再生熱能津貼的興趣。同時,三菱電機專為級聯運轉而設計的模組化熱水系統,可望降低多棟建築園區的設計門檻,並使產品策略與區域高需求營運商的需求保持一致。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府政策和獎勵的實施,以促進節能型暖通空調系統的推廣。

- 日本GX藍圖中的電氣化目標

- 家庭熱水供應需求的無碳

- 將熱泵的應用範圍擴展到傳統暖氣和冷氣應用之外。

- 第四代區域供熱技術,整合大型熱泵的出現。

- 擴大與OEM公司在資料中心廢熱回收的合作。

- 市場限制因素

- 安裝難度高且安裝成本高

- 安裝技術人員短缺

- 由於可再生能源證書價值下降,投資回報率降低。

- 與固體熱電HVAC模組的競爭

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按供應來源

- 空氣源

- 水源

- 地熱

- 混合

- 透過技術

- 空對空

- 空氣中的水

- 水-水

- 來自地下的水(土壤)

- 按產能

- 小於10千瓦

- 10~50 kW

- 50~200 kW

- 超過200千瓦

- 透過使用

- 空間暖氣

- 空間冷卻

- 家用和衛生熱水

- 工業和製程加熱

- 其他用途

- 最終用戶

- 住宅

- 商業

- 產業

- 按安裝類型

- 新安裝

- 改裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Daikin Industries, Ltd.

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Carrier Global Corporation

- Robert Bosch GmbH(Bosch Thermotechnology)

- NIBE Industrier AB

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Group

- LG Electronics Inc.

- Fujitsu General Limited

- Johnson Controls-Hitachi Air Conditioning

- Trane Technologies plc

- Ariston Holding NV

- PHNIX Eco-Energy Solution Ltd.

- Sanden Corporation

- Toshiba Carrier Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan heat pump market size is expected to increase from USD 5.38 billion in 2025 to USD 5.69 billion in 2026 and reach USD 7.12 billion by 2031, growing at a CAGR of 4.59% over 2026-2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Industrial and Process Heating, and More), End User (Residential, Commercial, and More), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Japan Heat Pump Market Trends and Insights

Implementation of Government Policies and Incentives Promoting Energy-Efficient HVAC

Generous 2026 subsidies cover up to 40% of equipment and labor for households swapping legacy oil or gas boilers, creating an immediate pull on the order backlog. Local add-ons in Hokkaido and Aomori shrink net homeowner outlays by another USD 1,000-2,000, overcoming performance anxiety during sub-zero winters. Mandatory energy codes that took force in April 2025 effectively eliminate low-efficiency furnaces from new builds, channeling procurement toward inverter-driven air-to-water units that price roughly 18% higher than past workhorse models. Carbon pricing under the 2026 GX Emissions Trading Scheme puts a USD 17-21 shadow cost on industrial CO2, nudging factories toward high-temperature heat pumps. Accelerated depreciation granted under the Act on Rationalizing Energy Use sweetens payback for commercial retrofits.

Electrification Targets Under Japan's GX Roadmap

The roadmap assigns heat pumps a leading role in displacing 8 million kL of oil-equivalent by 2030, tying appliance uptake to national net-zero ambitions. A grid-wide demand-response pilot begun in January 2026 pays households up to USD 0.10 per kilowatt-hour for curtailment, cushioning evening peaks that once strained the TEPCO network. Utilities must line up 20 GW of flexible capacity by 2030, and large heat-pump plants paired with thermal storage now qualify for capacity payments, improving project revenue stacks. Real-time pricing analytics co-developed by Daikin and Hitachi trim commercial operating costs by roughly 13% and illustrate the virtuous cycle between smart controls and grid services. Together, these measures tighten the policy-technology loop that underpins long-run demand.

Difficulties in Installation and High Installation Cost

Ground-source projects demand 50-100 m boreholes and hydronic retrofits, inflating budgets to USD 20,000-33,000 and stretching schedules by up to six weeks. Tight property lines in metropolitan wards force costly vertical drilling that adds another USD 5,300-8,000. Legacy radiators designed for 80 °C supply water often require upsizing, doubling expenses and lengthening downtime. Concerns over borehole integrity in seismic terrain lead 42% of contractors to avoid these jobs outright. Setback rules under the Building Standards Act further squeeze feasibility for small lots and heighten soft-cost risk.

Other drivers and restraints analyzed in the detailed report include:

- Decarbonization of Domestic Water-Heating Demand

- Growing Use of Heat Pumps Beyond Traditional Heating and Cooling

- Installer Skill Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air Source units generated 53.81% of 2025 revenue in the Japan heat pump market, a dominance rooted in modest upfront costs and ease of installation across temperate coastal regions. Water and Ground Source variants together remained near 12% because borehole drilling and water-body access add complexity that many urban projects cannot absorb. Hybrid configurations, though still a minority, are scaling at 5.31% annually as homeowners and building managers prize the ability to toggle between electricity and gas when tariffs spike or deep freezes sap efficiency, a pattern most visible in Hokkaido's harsher winters. Tokyo Gas' decision to end stand-alone gas water-heater sales from April 2026 both validates and propels this pivot toward dual-fuel resilience.

Grant-backed production of CO2 hybrid water heaters rated at 90 °C should lift annual output to 50,000 units by 2027, directly addressing bathwater temperature preferences that once discouraged full electrification. Ground Source systems, while small, benefit from year-round COP values above 4.0 and headline research showing potential 35-40% primary-energy savings in fifth-generation district schemes. Sumitomo Forestry's forthcoming 200-home pilot in Otaru illustrates how municipal, developer and OEM collaboration can unlock ground-coupled economics even in seismic regions. Collectively these trends entrench hybrids as a pragmatic bridge while pure-electric performance edges upward.

Air-to-Water designs held 48.62% of 2025 revenue owing to their seamless match with Japan's hydronic radiator base and the wide modulation range offered by inverter drives. Yet Ground-to-Water systems log the swiftest expansion at 5.02% CAGR, fueled by municipal pilots that show seasonal COPs topping 4.5 and primary-energy cuts exceeding 40%. Ogata Village's 1.2 MW loop demonstrated real-world savings that now influence subsidy scoring, while Otaru's large-scale seasonal-storage build promises additional proof. Air-to-Air models still dominate unit volumes but contribute less revenue per install because of their simpler bill of materials and quicker replacement cycle.

Water-to-Water remains niche but strategic, with seawater-source machines at coastal data centers capturing waste heat for boiler feedwater, cutting CO2 by tens of thousands of tons annually. JERA's 3 MW plant in Yokohama opened boardroom eyes in the broader utilities segment and has raised policy interest in renewable-thermal grants. Meanwhile, Mitsubishi Electric's modular hydronic line designed for cascading could lower engineering hurdles for multi-building campuses, aligning product strategy with district-scale demand aggregators.

List of Companies Covered in this Report:

- Daikin Industries, Ltd.

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Carrier Global Corporation

- Robert Bosch GmbH (Bosch Thermotechnology)

- NIBE Industrier AB

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Group

- LG Electronics Inc.

- Fujitsu General Limited

- Johnson Controls-Hitachi Air Conditioning

- Trane Technologies plc

- Ariston Holding N.V.

- PHNIX Eco-Energy Solution Ltd.

- Sanden Corporation

- Toshiba Carrier Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Implementation of Government Policies and Incentives Promoting Energy-Efficient HVAC

- 4.2.2 Electrification Targets Under Japan's GX Roadmap

- 4.2.3 Decarbonization of Domestic Water-Heating Demand

- 4.2.4 Growing Use of Heat Pumps Beyond Traditional Heating and Cooling Applications

- 4.2.5 Emergence of Fourth-Generation District Heating Integrating Large-Scale Heat Pumps

- 4.2.6 Expansion of Data Center Waste-Heat Recovery Partnerships With OEMs

- 4.3 Market Restraints

- 4.3.1 Difficulties in Installation and High Installation Cost

- 4.3.2 Installer Skill Shortages

- 4.3.3 Diminishing Renewable Energy Certificate Value Reducing ROI

- 4.3.4 Competition From Solid-State Thermoelectric HVAC Modules

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries, Ltd.

- 6.4.2 Mitsubishi Electric Corporation

- 6.4.3 Panasonic Corporation

- 6.4.4 Carrier Global Corporation

- 6.4.5 Robert Bosch GmbH (Bosch Thermotechnology)

- 6.4.6 NIBE Industrier AB

- 6.4.7 Stiebel Eltron GmbH & Co. KG

- 6.4.8 Vaillant Group

- 6.4.9 Viessmann Group

- 6.4.10 LG Electronics Inc.

- 6.4.11 Fujitsu General Limited

- 6.4.12 Johnson Controls-Hitachi Air Conditioning

- 6.4.13 Trane Technologies plc

- 6.4.14 Ariston Holding N.V.

- 6.4.15 PHNIX Eco-Energy Solution Ltd.

- 6.4.16 Sanden Corporation

- 6.4.17 Toshiba Carrier Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)