|

市場調查報告書

商品編碼

2061763

中國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

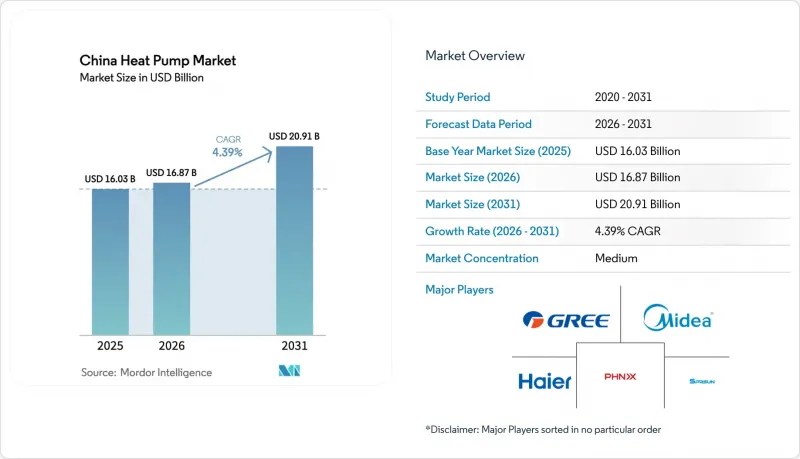

根據 Mordor Intelligence 預測,中國熱泵市場規模預計到 2025 年將達到 160.3 億美元,到 2026 年將達到 168.7 億美元,到 2031 年將達到 209.1 億美元,2026 年至 2031 年的複合成長率為 4.39%。

本報告按供熱源類型(空氣源、水源等)、技術(空氣-空氣、空氣-水等)、容量(小於10kW、10-50kW等)、應用(空間供暖、工業/工藝供暖等)、最終用戶(住宅、商業設施等)、安裝類型(新建、維修)和地區進行細分。市場預測以美元計價。

中國熱泵市場趨勢與洞察

將熱泵的應用範圍擴展到傳統暖氣和冷氣應用之外。

低於200 度C的工業製程熱在中國熱泵市場蘊藏著巨大的未開發潛力。紡織、食品和石化行業的先驅已在許多蒸氣工藝中實現了超過3的性能係數(COP)。燃煤發電廠和機場的餘熱回收系統採用兆瓦級技術,與傳統鍋爐相比,燃料消耗量降低了三分之二。成都的一個資料中心餘熱利用項目,透過即時調節伺服器產生的餘熱與附近商業設施的負荷,每年可減少約8千噸標準煤的消耗。這些試點計畫的成功提高了工業終端用戶投資的可行性,他們先前對電力和天然氣價格波動持懷疑態度。隨著高溫壓縮機逐漸成熟並走向市場,未來十年,165度C應用領域的技術空間將創造數十億美元的額外市場機會。

實施政府政策和獎勵,以推廣節能型暖氣和冷氣系統。

2025年5月推出的家用電器行動計畫的核心是津貼計劃,可涵蓋高達30%的初始成本,從而將北京、河北和河南的投資回收期縮短至五年以內。以舊換新計畫正在引導消費者減少對電暖器的關注,而《建築標準法》(GB 55015)則規定大規模新建建築的暖氣必須使用至少10%的可再生能源。能源服務公司正利用這些獎勵開發「供熱即服務」契約,從而減輕建築業主的資本投資負擔。此外,各省也根據季節性能係數閾值設定不同的補貼水平,鼓勵製造商超越標準能源效率。這些「胡蘿蔔加大棒」的措施相結合,正在創造持續的需求,並支撐中國熱泵市場的預期擴張。

前期安裝成本高,建築維修複雜。

住宅空氣源熱泵系統的初始成本是燃氣鍋爐的三到六倍,外牆和電氣維修費用還會額外增加20%到40%。維修工程通常需要更換散熱器以適應較低的供水溫度,這導致工期延長,造成居住者不便。除了省級補貼外,資金籌措仍難以籌集,導致許多農村住宅的投資回收期超過八年。在老舊的辦公大樓中,需要客製化設計才能將新的熱泵迴路整合到過時的冷凍水系統中,這會帶來顯著的風險溢價。這些經濟和技術上的摩擦正在阻礙中國原本蓬勃發展的熱泵市場。

細分市場分析

預計到2025年,空氣源熱泵將佔據中國熱泵市場68.78%的佔有率。這主要歸功於開發商看重其較低的初始成本、適合屋頂安裝以及較低的授權門檻。雖然水源熱泵目前仍佔少數,但預計到2031年將以5.26%的複合年成長率成長,因為區域供熱運營商和工業園區可以利用河流、含水層或排水溝渠等全年水溫穩定的水源。在北方省份,空氣源和地下循環相結合的混合系統正日益普及,因為極寒天氣會降低空氣源熱泵的效率,並增加電網負荷。邢台仁澤計畫就是一個例證,該計畫佔地93萬平方公尺,在-19度C的環境溫度下實現了3.64的能源效率比(COP)。政策制定者開始關注這些混合系統,將其作為示範案例,以推動監管政策的訂定,加速擺脫單一熱源設計。

區域供熱運營商也在進行深井水源循環系統的試點運行,該系統可同時提供供暖和熱水,從而延長滿載運行時間,並緩解季節性收入波動。在天津和河北,中石化的地熱工程規模已超過1.2億平方米,整合水源熱泵後的季節能源效率比超過4.0。地方政府正著重強調這些指標,以證明擴大補貼的合理性,進而提升水源技術的商業性吸引力。儘管地下水開採許可的取得仍然面臨挑戰,但井基設施的長期運作壽命與營運商的投資週期相吻合,這有利於水源熱泵在中國市場的穩步發展。

預計到2025年,空氣源熱泵平台將佔中國熱泵市場46.59%的佔有率。這主要得益於第四代區域供熱管網的日益普及,這些管網的供熱溫度範圍為35-45度C,正好符合空氣源熱泵運作的最佳供熱溫度範圍。河北省昭縣一個430萬平方公尺的計畫表明,一體化的空氣源熱泵系統可以取代燃煤鍋爐,同時滿足城市舒適度標準。水源熱泵利用穩定的地熱和工業餘熱,可達到5以上的能源效率比(COP)。尤其是在紡織和食品產業園區,同時進行暖氣和冷氣可以提高生產過程的經濟效益。地下水源熱泵由於鑽井成本和地下水法規等因素導致專案複雜性增加,目前仍屬於小眾市場,但其長達50年的熱交換器使用壽命以及不受環境溫度波動的影響,正促使高校和醫院擴大採用該系統。

在南方省份,由於空調普及率高且水循環管道不完善,空氣源熱泵仍是首選。然而,政策獎勵正鼓勵開發商採用雙盤管系統,以便在未來維修加裝地板時,可升級為空氣源熱泵系統。國家補貼鼓勵同時生產冷熱水,進而提高資產的年利用率,進而推動水源熱泵的普及。隨著中國熱泵市場的擴張,製造商正在增加智慧控制功能,使建築物能夠根據一天中的時間和室外條件,在空氣、水和地熱熱源之間動態切換。控制技術的進步提高了季節性能係數,並增強了多源技術組合的價值提案。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 將熱泵的應用範圍擴展到傳統暖氣和冷氣應用之外。

- 實施政府政策和獎勵,以促進節能型暖氣和冷氣系統的廣泛應用。

- 快速的都市化和新建築的建設

- 額定工作溫度低至 -35 度C 的壓縮機的出現,導致寒冷氣候地區空氣源熱泵的採用量激增。

- 擴大對農村地區以熱泵爐灶取代燃煤爐灶的補貼

- 熱泵和屋頂太陽能發電的結合,以及分時電價制度,促進了能源自給自足。

- 市場限制因素

- 建築維修的初期實施成本高且複雜。

- 公眾意識薄弱,且合格承包商短缺

- 農村配電網路冬季尖峰負載限制

- 電力與天然氣價格比率長期不確定性對工業採用的影響。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按供應來源

- 空氣源

- 水源

- 地熱

- 混合

- 透過技術

- 從空中到空中

- 從空氣到水

- 水到水

- 從地面到水

- 按產能

- 小於10千瓦

- 10~50 kW

- 50~200 kW

- 超過200千瓦

- 透過使用

- 空間暖氣

- 空間冷卻

- 家用和衛生熱水

- 工業和製程加熱

- 其他用途

- 最終用戶

- 住宅

- 商業

- 產業

- 按安裝類型

- 新安裝

- 改裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Ariston Holding NV

- Carrier Global Corporation

- Daikin Industries, Ltd.

- Fujitsu General Limited

- Glen Dimplex Group

- Haier Group Corporation

- Johnson Controls-Hitachi Air Conditioning

- LG Electronics Inc.

- Mitsubishi Electric Corporation

- NIBE Industrier AB

- Panasonic Corporation

- PHNIX Eco-Energy Solution Ltd.

- Robert Bosch GmbH(Bosch Thermotechnology)

- Sanden Corporation

- Stiebel Eltron GmbH and Co. KG

- Thermia Heat Pumps

- Trane Technologies plc

- Vaillant Group

- Viessmann Group

- WaterFurnace International Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the china heat pump market size is projected to be USD 16.03 billion in 2025, USD 16.87 billion in 2026, and reach USD 20.91 billion by 2031, growing at a CAGR of 4.39% from 2026 to 2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Industrial and Process Heating, and More), End User (Residential, Commercial, and More), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

China Heat Pump Market Trends and Insights

Growing Use of Heat Pumps Beyond Traditional Heating and Cooling Applications

Industrial process heat below 200 °C represents a sizeable but under-served opportunity for the China heat pump market, and first movers in textiles, food, and petrochemicals now validate coefficients of performance that exceed 3 for many steam processes. Waste-heat-recovery installations at coal-fired units and airports showcase megawatt-scale systems that trim fuel use by two-thirds versus legacy boilers. Data-center coupling projects in Chengdu demonstrate real-time balancing of server waste heat with nearby commercial loads, cutting standard-coal consumption by almost 8 kilotonnes annually. Successful pilots accelerate bankability for industrial end users that were historically skeptical of electricity-to-gas price volatility. As high-temperature compressors reach market readiness, technical headroom for 165 °C applications offers an incremental addressable market worth billions over the next decade.

Implementation of Government Policies and Incentives to Promote Energy-Efficient Heating and Cooling Systems

The May 2025 household-appliance action plan anchors subsidy streams that reimburse up to 30% of upfront costs, slashing payback periods below five years in Beijing, Hebei, and Henan. Trade-in programs direct consumer attention away from electric resistance heaters, while GB 55015 building codes mandate renewable thermal inputs above 10% for large new construction. Energy service companies harness these incentives to roll out heat-as-a-service contracts, freeing building owners from capital budgeting. Provinces also differentiate rebate levels by seasonal performance factor thresholds, nudging manufacturers to surpass baseline efficiency. Together, these carrots and sticks channel sustained demand that underpins the projected expansion of the China heat pump market.

High Upfront Installation Cost and Building Retrofit Complexity

Residential air-to-water systems cost three to six times more than gas boilers on a first-cost basis, and extra envelope or electrical upgrades can add another 20-40%. Retrofit projects must often replace radiators to accommodate lower supply temperatures, stretching construction timetables and disrupting occupants. Financing remains scarce outside provincial subsidies, pushing payback periods above eight years for many rural homes. Older office towers face bespoke engineering to merge new heat-pump loops with vintage chilled-water infrastructure, inflating risk premiums. These economic and technical frictions drag on the otherwise favorable growth trajectory of the China heat pump market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Urbanization and Construction of New Buildings

- Surge in Cold-Climate Air-Source Heat Pump Deployments Enabled by -35 °C Rated Compressors

- Limited Public Awareness and Certified Installer Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air source heat pumps controlled 68.78% of the China heat pump market share in 2025 as developers favored their lower upfront cost, rooftop compatibility, and limited permitting hurdles. Water source units, though still a minority, are projected to grow at a 5.26% CAGR through 2031 because district-heating companies and industrial parks can tap rivers, aquifers, or wastewater streams that deliver seasonally stable temperatures. Hybrid systems that couple air and ground loops are gaining favor in northern provinces where extreme cold can curb air source efficiency and raise grid stress, as evidenced by the 930,000 m2 Xingtai Renze scheme that achieved a 3.64 COP under -19 °C ambient conditions. Policymakers have begun spotlighting these hybrid architectures as model cases, signaling regulatory tailwinds that could accelerate diversification away from single-source designs.

District heating utilities are also trialing deep-well water source loops that allow simultaneous space heating and hot-water production, boosting full-load hours and flattening seasonal revenue volatility. In Tianjin and Hebei, Sinopec's geothermal portfolio already covers more than 120 million m2, with seasonal performance factors above 4.0 after water source heat pump integration. Local officials tout these metrics to justify subsidy extensions, thereby enhancing the commercial appeal of water source technology. Although permitting for groundwater extraction remains stringent, the long operational life of well infrastructure aligns with utility investment horizons and supports steady uptake within the China heat pump market.

Air-to-water platforms held 46.59% of the China heat pump market share in 2025 because fourth-generation district networks increasingly run at 35-45 °C supply temperatures that match these units' optimal operating range. Hebei Zhaoxian's 4.3 million m2 project validated that clustered air-to-water arrays can displace coal boilers while meeting municipal comfort standards. Water-to-water machines leverage stable geothermal or industrial waste-heat sources to deliver COPs above 5, especially in textile and food parks where simultaneous chilling and heating improve process economics. Ground-to-water units remain niche because drilling costs and groundwater regulations elevate project complexity, but universities and hospitals adopt them for their 50-year exchanger lifespan and immunity to outdoor temperature swings.

Southern provinces still prefer air-to-air heat pumps for cooling-led climates that lack hydronic distribution, yet policy incentives are nudging developers to specify dual coils so systems can upgrade to air-to-water when future retrofits add radiant flooring. Water-to-water penetration is aided by national subsidies that reward simultaneous production of chilled and hot water, improving annualized asset utilization. As the China heat pump market size grows, manufacturers are adding smart controls that let buildings switch dynamically among air, water, and ground sources based on tariff windows and outdoor conditions. This control sophistication boosts seasonal performance factors and reinforces the value proposition of multi-source technology stacks.

List of Companies Covered in this Report:

- Ariston Holding N.V.

- Carrier Global Corporation

- Daikin Industries, Ltd.

- Fujitsu General Limited

- Glen Dimplex Group

- Haier Group Corporation

- Johnson Controls-Hitachi Air Conditioning

- LG Electronics Inc.

- Mitsubishi Electric Corporation

- NIBE Industrier AB

- Panasonic Corporation

- PHNIX Eco-Energy Solution Ltd.

- Robert Bosch GmbH (Bosch Thermotechnology)

- Sanden Corporation

- Stiebel Eltron GmbH and Co. KG

- Thermia Heat Pumps

- Trane Technologies plc

- Vaillant Group

- Viessmann Group

- WaterFurnace International Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Use of Heat Pumps Beyond Traditional Heating and Cooling Applications

- 4.2.2 Implementation of Government Policies and Incentives to Promote Energy-Efficient Heating and Cooling Systems

- 4.2.3 Rapid Urbanization and Construction of New Buildings

- 4.2.4 Surge in Cold-Climate Air-Source Heat Pump Deployments Enabled by -35 °C Rated Compressors

- 4.2.5 Expansion of Rural Subsidies Replacing Coal Stoves with Heat Pumps

- 4.2.6 Integration of Heat Pumps with Rooftop PV and Time-of-Use Tariffs Driving Self-Consumption

- 4.3 Market Restraints

- 4.3.1 High Upfront Installation Cost and Building Retrofit Complexity

- 4.3.2 Limited Public Awareness and Certified Installer Shortage

- 4.3.3 Winter Peak-Load Constraints on Rural Distribution Grids

- 4.3.4 Uncertainty in Long-Term Electricity-to-Gas Price Ratios Affecting Industrial Adoption

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ariston Holding N.V.

- 6.4.2 Carrier Global Corporation

- 6.4.3 Daikin Industries, Ltd.

- 6.4.4 Fujitsu General Limited

- 6.4.5 Glen Dimplex Group

- 6.4.6 Haier Group Corporation

- 6.4.7 Johnson Controls-Hitachi Air Conditioning

- 6.4.8 LG Electronics Inc.

- 6.4.9 Mitsubishi Electric Corporation

- 6.4.10 NIBE Industrier AB

- 6.4.11 Panasonic Corporation

- 6.4.12 PHNIX Eco-Energy Solution Ltd.

- 6.4.13 Robert Bosch GmbH (Bosch Thermotechnology)

- 6.4.14 Sanden Corporation

- 6.4.15 Stiebel Eltron GmbH and Co. KG

- 6.4.16 Thermia Heat Pumps

- 6.4.17 Trane Technologies plc

- 6.4.18 Vaillant Group

- 6.4.19 Viessmann Group

- 6.4.20 WaterFurnace International Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)