|

市場調查報告書

商品編碼

2061761

法國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)France Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

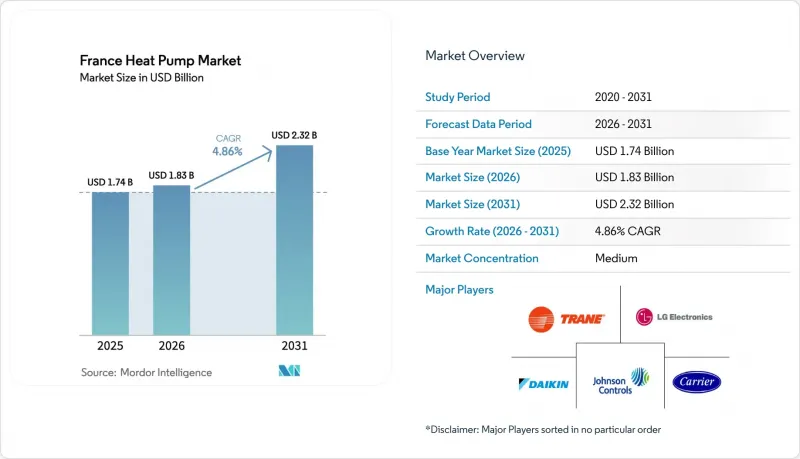

根據 Mordor Intelligence 預測,法國熱泵市場規模將從 2025 年的 17.4 億美元成長到 2026 年的 18.3 億美元,然後在 2031 年達到 23.2 億美元,2026 年至 2031 年的複合年成長率為 4.86%。

本報告按熱源類型(空氣源、水源等)、技術(空氣-空氣、空氣-水等)、容量(小於10kW、10-50kW等)、應用(空間供暖、工業/工藝供暖等)、最終用戶(住宅、商業設施等)、安裝類型(新建、維修)和地區進行分類。市場預測以美元計價。

法國熱泵市場趨勢與洞察

「MaPrimeRenov」補貼計劃擴大了其目標市場。

高階補貼現要求產品必須為歐洲製造,每年約有20億歐元(22.4億美元)的資金流向本土品牌。遍遠地區低收入家庭維修空氣-水循環系統的投資回收期將從8年縮短至5年。地熱系統的補貼上限已提高至5,000歐元(5,600美元),縮小了與空氣源設備的成本差距,預計到2026年銷售量將成長18%。在10千瓦以下的細分市場,先前佔25%佔有率的亞洲進口商的退出,將立即為Atlantic和Bosch等品牌創造市場擴張空間。透過EHPA資料庫進行檢驗將使前置作業時間延長3週,但將提高供應鏈的透明度。

RE2020建築能源標準強制要求低碳供暖

由於二氧化碳當量/平方公尺/年的排放限值為4公斤二氧化碳當量/年,燃氣鍋爐將不再符合標準,預計2023年完工的獨棟住宅中將有86%選擇熱泵。開發商願意承擔8,000歐元至12,000歐元、8,960歐元至13,440歐元的額外外部成本,以避免可能超過4萬歐元的碳排放罰款(在其使用壽命內)。將屋頂太陽能發電與熱泵結合使用,可將初級能源係數降低高達40%,從而釋放碳排放預算,用於其他系統。目前,南部地區正在推廣使用可逆式熱泵機組。

冷媒法規將加速技術變革。

歐盟法規 2024/573 要求到 2030 年將氫氟碳化合物 (HFC) 配額減少 79%,這需要轉向易燃的 R290 或 R454B 混合冷媒。 R290 的高壓要求使用更厚的管道和新的壓縮機殼體,導致每台設備的成本增加 300 至 500 歐元(336 至 60 美元)。三菱電機的「Ecodan 2026」系列空調清楚地體現了這種權衡:雖然在 -7°C 下的效率提高了 15%,但可用室內面積卻被限制在 20平方公尺或以上。

細分市場分析

到2025年,空氣源熱泵將成為法國市場的主導力量,佔74.78%的銷售量。空氣源熱泵安裝成本適中,介於8,000歐元至12,000歐元(約8,960美元至13,440美元)之間,因此在現有散熱器能夠處理40-55°C給水溫度的維修專案中,空氣源熱泵仍然是一個極具吸引力的選擇。雖然地熱能源專案的市場規模較小,但由於工業廢熱的利用和鑽井成本的降低,預計其年成長率將達到5.31%。由於歐盟水框架指令下核准程序的複雜性,水熱能源裝置仍然是一個小眾市場,但混合式(燃氣+熱泵)系統正受到那些儘管面臨碳排放罰款卻仍不願拆除鍋爐的家庭的青睞。

由於花崗岩地質、淺層含水層以及慷慨的補貼政策,布列塔尼已成為法國地熱能利用中心,與北部沉積岩地區相比,鑽井成本降低了20%至30%。奧弗涅-羅納-阿爾卑斯大區的相關人員已採用海水-水循環系統,實現了4.5或更高的季節性能係數,而周邊空氣源地熱系統的平均水平僅為3.2,這為採用更深層的地熱能提供了經濟上的合理性。

預計到2025年,空氣-水系統將佔總銷售額的65.86%,反映出它們與現有水循環系統相容,且供水溫度符合RE2020標準。地熱地下水系統雖然規模較小,但由於鑽井成本降至每公尺48歐元(54美元),以及RE2020初級能源係數有利於超低碳供熱,其成長速度最快,年複合成長率達5.14%。空氣-空氣空調機組佔總銷售額的28%,用於滿足南部地區日益成長的製冷負荷,但由於不符合MaPrimeRenov補貼資格,其維修速度較慢。水-水系統目前仍僅限於特定湖濱地區的試點計畫和區域供熱。

威斯曼公司於2026年1月發布的「Vitocal 350-G」地熱能利用系統採用R290變頻壓縮機,在0°C鹽水入口溫度下,其能源效率比(COP)達到5.2,比同類空氣源機組性能提升35%。博世公司則以「Compress 7800i LW」地熱能利用系統與之競爭。該系統採用空氣-水循環平台,配備300升儲槽和內建的需量反應介面,顯示雙方將在能源效率和電網服務方面展開競爭。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- MaPrimeRenov的補貼擴大了目標市場。

- RE2020建築能源標準強制要求採用低碳暖氣。

- 供熱即服務模式降低了前期成本。

- 智慧電網需量反應帶來的收入提高了投資報酬率。

- 適用於寒冷氣候的 R290 機組在各個季節都能提供更佳的性能。

- 利用高溫熱泵進行工業廢熱回收

- 市場限制因素

- 冷媒的逐步減少導致了代價高昂的重新設計。

- 合格安裝人員短缺限制了產品的普及。

- 農村地區的擁擠費推高了營運成本。

- 二手設備灰色市場正在給原始設備製造商的利潤率帶來壓力。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按供應來源

- 空氣源

- 水源

- 地熱

- 混合

- 透過技術

- 空對空

- 空氣中的水

- 水-水

- 來自地下的水(土壤)

- 按產能

- 小於10千瓦

- 10~50 kW

- 50~200 kW

- 超過200千瓦

- 透過使用

- 空間暖氣

- 空間冷卻

- 家用和衛生熱水

- 工業和製程加熱

- 其他用途

- 最終用戶

- 住宅

- 商業

- 產業

- 按安裝類型

- 新安裝

- 改裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Trane Inc., Trane Technologies Plc

- LG Electronics Inc.

- Daikin Industries Ltd.

- Johnson Controls International Plc

- Carrier Corporation

- Atlantic Group

- Vaillant Group

- Intuis Inc.

- Bosch Thermotechnology GmbH

- NIBE Energy Systems

- Thermor

- De Dietrich Thermique

- Saunier Duval

- Aldes Corporation

- CIAT Corporation

- Frisquet SA

- Viessmann Climate Solutions SE

- Stiebel Eltron GmbH and Co. KG

- Glen Dimplex Thermal Solutions

- Aermec SpA

- Hoval Group

- Baxi Heating, BDR Thermea

- Wolf GmbH

- Ariston Thermo Group

- Panasonic Corporation

- Mitsubishi Electric Corporation

- Hitachi Air Conditioning

- ETT, Energie Transfert Thermique

第7章 市場機會與未來展望

According to Mordor Intelligence, the france heat pump market size is valued at USD 1.83 billion in 2026, up from USD 1.74 billion in 2025, and is projected to reach USD 2.32 billion by 2031, growing at a 4.86% CAGR over 2026-2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Industrial and Process Heating, and More), End User (Residential, Commercial, and More), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

France Heat Pump Market Trends and Insights

MaPrimeRenov' Subsidies Expand Addressable Market

Premium-tier rebates now require European factory origin, steering roughly EUR 2 billion (USD 2.24 billion) of annual funding toward local brands. Payback periods for rural air-to-water retrofits fall from eight to five years for low-income households. The raised EUR 5,000 (USD 5,600) cap on geothermal systems narrows the cost gap with air-source equipment, supporting an 18% unit-sales bump in 2026. Market share vacated by Asian importers, previously 25% in the sub-10 kW tier, creates immediate runway for Atlantic and Bosch. Verification through the EHPA database adds three-week approval lags but improves supply-chain transparency.

RE2020 Building Energy Code Mandates Low-Carbon Heating

The 4 kg CO2e m-2-year ceiling makes gas boilers non-compliant, prompting 86% of single-family completions in 2023 to choose heat pumps. Developers accept EUR 8,000-12,000 (USD 8,960-13,440) extra envelope cost to avoid lifetime carbon penalties that can exceed EUR 40,000 (USD 44,800). Pairing rooftop photovoltaics with heat pumps cuts primary-energy factors by up to 40%, freeing carbon budget for other systems and tilting specification toward reversible units in the south.

Refrigerant Regulations Accelerate Technology Transition

EU Regulation 2024/573 reduces HFC quotas 79% by 2030, forcing a pivot to flammable R290 or R454B blends. R290's higher pressure demands thicker tubing and new compressor housings, adding EUR 300-500 (USD 336-560) per unit. Mitsubishi Electric's Ecodan 2026 range illustrates the trade-off: 15% higher efficiency at -7 °C but indoor placement limited to rooms above 20 m2.

Other drivers and restraints analyzed in the detailed report include:

- Heat-as-a-Service Models Lower Up-Front Costs

- Smart-Grid Demand Response Revenues Improve ROI

- Shortage of Certified Installers Limits Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-source configurations led the France heat pump market with 74.78% revenue share in 2025. Favorable capex of EUR 8,000-12,000 (USD 8,960-13,440) installed keeps air units attractive for retrofit scenarios where existing radiators match 40 °C-55 °C water supply. Ground-source projects commanded a smaller base but show 5.31% annual growth potential thanks to industrial waste-heat integration and drilling-cost declines. Water-source units remain niche, bound by Water Framework permitting complexity, while hybrid gas-plus-heat-pump systems appeal to households reluctant to decommission boilers despite carbon penalties.

Granite geology, shallow aquifers, and supportive subsidies make Brittany the national stronghold for ground-source, lowering borehole expenditures 20-30% relative to northern sedimentary zones. Industrial actors in Auvergne-Rhone-Alpes deploy brine-to-water loops achieving seasonal performance factors above 4.5 when ambient air-source rivals stall at 3.2, validating the economic thesis for deeper geothermal adoption.

Air-to-water systems controlled 65.86% of 2025 sales, underscoring their fit with legacy hydronic circuits and RE2020 compliant supply temperatures. Geothermal ground-to-water solutions, although smaller, are the fastest expanding at 5.14% CAGR as drilling prices fall to EUR 48 (USD 54) per meter and RE2020's primary-energy factor of 0.6 rewards ultra-low-carbon heat. Air-to-air units, accounting for 28% of revenue, meet rising cooling loads in the south but lose out on premium MaPrimeRenov' subsidies, curbing retrofit momentum. Water-to-water remains confined to select lakeside or district-heating pilots.

Viessmann's Vitocal 350-G, unveiled January 2026, puts a R290 inverter compressor in geothermal service, posting a 5.2 COP at 0 °C brine inlet, 35% better than air-equivalent units. Bosch counters with the Compress 7800i LW, an air-to-water platform embedding a 300-liter tank and native demand-response interface, signaling competition on both efficiency and grid service.

List of Companies Covered in this Report:

- Trane Inc., Trane Technologies Plc

- LG Electronics Inc.

- Daikin Industries Ltd.

- Johnson Controls International Plc

- Carrier Corporation

- Atlantic Group

- Vaillant Group

- Intuis Inc.

- Bosch Thermotechnology GmbH

- NIBE Energy Systems

- Thermor

- De Dietrich Thermique

- Saunier Duval

- Aldes Corporation

- CIAT Corporation

- Frisquet S.A.

- Viessmann Climate Solutions SE

- Stiebel Eltron GmbH and Co. KG

- Glen Dimplex Thermal Solutions

- Aermec S.p.A.

- Hoval Group

- Baxi Heating, BDR Thermea

- Wolf GmbH

- Ariston Thermo Group

- Panasonic Corporation

- Mitsubishi Electric Corporation

- Hitachi Air Conditioning

- ETT, Energie Transfert Thermique

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 MaPrimeRenov' Subsidies Expand Addressable Market

- 4.2.2 RE2020 Building Energy Code Mandates Low-Carbon Heating

- 4.2.3 Heat-as-a-Service Models Lower Up-Front Costs

- 4.2.4 Smart-Grid Demand Response Revenues Improve ROI

- 4.2.5 Cold-Climate R290 Units Boost Seasonal Performance

- 4.2.6 Industrial Waste-Heat Recovery via High-Temp HPs

- 4.3 Market Restraints

- 4.3.1 Refrigerant Phase-Down Drives Costly Redesigns

- 4.3.2 Shortage of Certified Installers Limits Deployments

- 4.3.3 Grid Congestion Fees in Rural Areas Raise Opex

- 4.3.4 Used-Equipment Grey Market Undercuts OEM Margins

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Trane Inc., Trane Technologies Plc

- 6.4.2 LG Electronics Inc.

- 6.4.3 Daikin Industries Ltd.

- 6.4.4 Johnson Controls International Plc

- 6.4.5 Carrier Corporation

- 6.4.6 Atlantic Group

- 6.4.7 Vaillant Group

- 6.4.8 Intuis Inc.

- 6.4.9 Bosch Thermotechnology GmbH

- 6.4.10 NIBE Energy Systems

- 6.4.11 Thermor

- 6.4.12 De Dietrich Thermique

- 6.4.13 Saunier Duval

- 6.4.14 Aldes Corporation

- 6.4.15 CIAT Corporation

- 6.4.16 Frisquet S.A.

- 6.4.17 Viessmann Climate Solutions SE

- 6.4.18 Stiebel Eltron GmbH and Co. KG

- 6.4.19 Glen Dimplex Thermal Solutions

- 6.4.20 Aermec S.p.A.

- 6.4.21 Hoval Group

- 6.4.22 Baxi Heating, BDR Thermea

- 6.4.23 Wolf GmbH

- 6.4.24 Ariston Thermo Group

- 6.4.25 Panasonic Corporation

- 6.4.26 Mitsubishi Electric Corporation

- 6.4.27 Hitachi Air Conditioning

- 6.4.28 ETT, Energie Transfert Thermique

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)