|

市場調查報告書

商品編碼

2044240

中東和非洲設施管理:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East And Africa Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

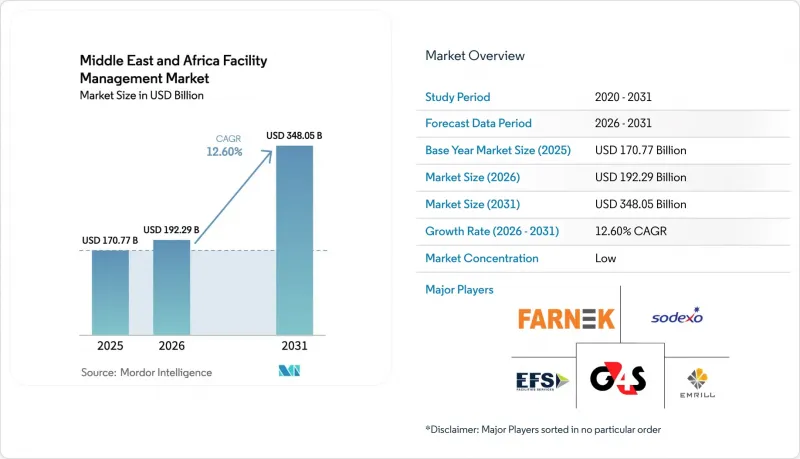

2025 年中東和非洲的設施管理市場價值為 1,707.7 億美元,預計到 2031 年將達到 3,480.5 億美元,而 2026 年為 1922.9 億美元,預測期(2026-2031 年)的複合年成長率為 12.60%。

沙烏地阿拉伯、阿拉伯聯合大公國、埃及和南非不斷擴大的基礎設施投資催生了大規模的資產儲備,從而帶動了對捆綁式和一體化設施服務需求的成長。隨著企業和公共部門業主擴大轉向基於績效的契約,將服務費用與運轉率、能源消耗和用戶體驗等指標掛鉤,外包合約在新支出中佔據了相當大的比例。中東和非洲的設施管理市場加速了數位化進程,預測性維護、物聯網賦能的建築管理系統數位雙胞胎平台被廣泛採用,以最佳化能源消耗並減少關鍵設備的意外停機時間。因此,競爭優勢取決於數據分析能力以及將ESG報告融入日常營運的能力,這一點在NEOM和阿卜杜拉國王金融區(KAFD)等大型企劃中尤其明顯。同時,隨著全球領導企業與區域專家合作,擴大其地域覆蓋範圍並深化行業專業知識,行業重組也在加速進行。

中東和非洲設施管理市場趨勢與洞察

基礎建設的擴展

僅在沙烏地阿拉伯,2024年就根據「2030願景」授予了大規模建築契約,而NEOM耗資5000億美元的總體規劃也顯著提高了整個行業的工資水平。這清楚地表明,大型專案如何推動了整個中東和非洲物業管理市場的服務需求。在非洲,非洲金融公司於2024年3月安排的企業聯合組織團貸款表明,新的資本流入旨在填補資金缺口,從而擴大需要全生命週期支持的資產基礎。同樣,阿拉伯聯合大公國的房地產熱潮也提振了高階辦公室、住宅和零售物業對技術性物業管理的需求。由於這些累積效應,物業經理們正在尋找能夠幫助他們快速擴展業務、規範流程並管理多階段開發專案中複雜相關人員群體的服務提供者。

建築管理外包的擴展

外包發展勢頭強勁,這主要得益於阿卜杜拉國王金融區 (KAFD) 等開創性計畫的推動。在該金融區,基於 IBM Maximo 的整合合約為業主創造了可量化的價值,客戶滿意度提升了 95%,同時降低了維修成本。監管機構也紛紛效法。例如,中東設施管理協會 (MEFA) 和阿治曼房地產監管局 (RERA Ajman) 於 2024 年 6 月簽署協議,正式製定最佳實踐和培訓路徑,將住宅和綜合用途區域的外包模式製度化。醫療保健機構也早早接受了這個趨勢,將關鍵環境中的合規工作委託給精通感染控制規程的外部團隊。基於績效的合約透過將付款與運轉率和能源相關關鍵績效指標 (KPI) 掛鉤,延長了平均合約期限,從而最佳化了獎勵。

技術純熟勞工短缺

到2030年,非洲每年都需要大量新增專案管理專業人員。然而,人才培養體系難以滿足這一需求,導致關鍵的管理職缺,阻礙了中東和非洲設施管理市場的成長。在海灣國家,機電管道(MEP)公司反映中階管理人員缺乏相關知識,減緩了數位化系統的應用,並降低了生產力。到2024年,建築業對技能發展的需求日益成長,但高員工離職率使得雇主不願投資培訓。綠建築領域專業人才的短缺進一步加劇了智慧資產最佳化專案面臨的挑戰。

細分市場分析

2025年,硬性服務在中東和非洲的設施管理市場中佔比達56.25%。這主要得益於必要的暖通空調(HVAC,包括暖氣、通風、供水和排水)、消防安全以及針對氣候惡劣、運轉率率高的物業設計的物業健康管理項目。其中,機電工程(MEP)服務佔了大部分支出,因為節能維修已成為A級物業的強制性要求。軟性服務也呈現強勁成長,複合年成長率(CAGR)達到12.78%,並擴大被納入綜合合約中,以提升租戶福祉指標和環境、社會及治理(ESG)報告的品質。

軟性服務的成長反映了其範圍的擴大,涵蓋了永續清潔化學品、健康認證和租戶互動分析等領域。儘管軟性服務在絕對規模上仍然較小,但它已成為服務提供者與客戶組織深度互動並交叉銷售高利潤諮詢服務的策略途徑。這一趨勢表明,在預測期內,軟性服務在中東和非洲設施管理市場的佔有率將繼續穩步成長。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基礎建設的擴展

- 建築管理外包的增加

- 安全保障的需求日益成長

- 設施管理的技術進步

- ESG主導的設施管理需求

- 來自 Gigamix 青年計畫的 FM 需求

- 市場限制因素

- 熟練勞動力短缺

- 監管挑戰

- 經濟情勢不穩定與原油價格波動

- 中東和非洲各國FM標準的差異

- 產業價值鏈分析

- PESTEL 分析

- 市場進入者的法規與法律體系

- 宏觀經濟指標對FM需求的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 投資與資金籌措分析

第5章 市場規模與成長預測

- 按服務類型

- 硬服務

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全

- 其他硬體服務

- 軟服務

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟體服務

- 硬服務

- 以規定形式

- 內部

- 外包

- 單頻調頻

- 捆綁式調頻廣播

- 整合調頻

- 按最終用戶行業分類

- 商業(IT/電信、零售/倉儲)

- 飯店餐飲業(飯店、餐廳、大型餐廳)

- 設施和公共基礎設施(政府、教育、交通)

- 醫療保健(公立和私立機構)

- 工業流程(製造業、能源業、採礦業)

- 其他

- 國家

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 南非

- 埃及

- 奈及利亞

- 其他中東和非洲國家

第6章 競爭情勢

- 市場集中度

- 策略舉措和夥伴關係

- 市佔率分析

- 公司簡介

- Engie Cofely Energy Services LLC(Engie SA)

- EFS Facilities Services Group

- Ejadah Asset Management Group

- Emrill Services LLC

- Farnek Services LLC

- Bidvest Facilities Management

- Kharafi National for Infrastructure Projects Developments Construction & Services SAE

- Initial Saudi Group

- Sodexo

- Ecolab

- Imdaad

- G4S

- CBRE Group Inc.

- ISS A/S

- Jones Lang LaSalle Incorporated

- Khidmah LLC

- Transguard Group

- Al Shirawi Facilities Management LLC

- Serco Group Middle East

- Aramark Corporation

第7章 市場機會與未來展望

The Middle East and Africa facility management market size was valued at USD 170.77 billion in 2025 and estimated to grow from USD 192.29 billion in 2026 to reach USD 348.05 billion by 2031, at a CAGR of 12.60% during the forecast period (2026-2031).

Mounting infrastructure outlays across Saudi Arabia, the United Arab Emirates, Egypt and South Africa shaped a sizeable pipeline of assets that, in turn, lifted demand for bundled and integrated facility services. Outsourced contracts attracted the bulk of new spending as corporate and public-sector owners increasingly shifted to outcome-based agreements that tied service fees to uptime, energy use and occupant-experience metrics. Digitalisation accelerated across the Middle East and Africa facility management market, with predictive maintenance, IoT-enabled building management systems, and digital-twin platforms optimizing energy consumption and reducing unplanned downtime in critical equipment fleets. Competitive differentiation therefore hinged on data analytics skills and the ability to embed ESG reporting into day-to-day operations, especially on mega projects such as NEOM and the King Abdullah Financial District. At the same time, consolidation quickened as global majors partnered with regional specialists to expand geographic reach and deepen sector know-how.

Middle East And Africa Facility Management Market Trends and Insights

Increasing Infrastructure Development

Saudi Arabia alone had awarded significant construction contracts in 2024 under Vision 2030, and NEOM's USD 500 billion masterplan stimulated significant spike in sector-wide wages, underscoring how large-scale projects fuelled service volumes across the Middle East and Africa facility management market. In Africa, the syndicated facility raised by Africa Finance Corporation in March 2024 signaled renewed capital inflows aimed at closing the funding gap and thereby broadening the asset base requiring lifecycle support. The UAE real estate boom similarly lifted demand for technical asset care in premium office, residential, and retail stock. As a cumulative result, facility executives sought providers able to scale quickly, standardize processes, and manage complex stakeholder groups across multi-phase developments.

Rising Outsourcing in Building Management

Outsourcing gained momentum after landmark deployments such as the King Abdullah Financial District, where an integrated contract underpinned by IBM Maximo boosted customer-satisfaction scores by 95% while lowering corrective maintenance outlays, demonstrating quantifiable value creation for owners. Regulatory bodies followed suit; for example, the Middle East Facility Management Association and Rera Ajman signed a June 2024 accord to formalise best practice and training pathways, institutionalising outsourced models in residential towers and mixed-use precincts. Healthcare operators were early adopters, entrusting critical-environment compliance to external teams steeped in infection-control protocols. Outcome-based contracts tied payments to uptime and energy KPIs, aligning incentives and lengthening average contract tenures.

Skilled Labour Shortages

Africa faced a significant demand for additional project-management professionals annually through 2030. However, training pipelines struggled to meet this demand, leaving critical supervisory positions unfilled and hindering the growth of the Middle East and Africa facility management market. In the Gulf, mechanical-electrical-plumbing firms reported mid-management knowledge gaps that delayed the implementation of digital systems and reduced productivity. In 2024, there is a significant need for upskilling in the construction sector, leading employers to hesitate in investing in training due to high personnel turnover. The scarcity of green-building specialisms further compounded the challenges faced in smart-asset optimisation projects.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Facility Management

- ESG-Driven Facility Operations Demand

- Volatile Economic Conditions and Oil Price Swings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard services controlled 56.25% of the Middle East and Africa facility management market in 2025, underpinned by mandatory HVAC, fire-safety and asset-integrity programs designed for harsh climates and high-occupancy assets. Within that basket, MEP services captured most spend, as energy-optimisation retrofits became obligatory for Grade-A stock. Soft services displayed brisk 12.78% CAGR and were increasingly bundled into integrated contracts that elevated occupant-wellbeing metrics and ESG reporting quality.

Soft-service growth reflected expanded scope spanning sustainable cleaning chemicals, wellness certifications and tenant-engagement analytics. Although smaller in absolute value, soft services represented a strategic pathway for providers to embed themselves in client organisations and cross-sell higher-margin advisory work. The dynamic signalled further incremental share gain for soft services within the Middle East and Africa facility management market size during the forecast horizon.

The Middle East and Africa Facility Management Market Report is Segmented by Service Type (Hard Services, and Soft Services), Offering Type (In-House, and Outsourced), End-User Industry (Commercial, Hospitality, and More), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, South Africa, Egypt, Nigeria, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Engie Cofely Energy Services LLC (Engie SA)

- EFS Facilities Services Group

- Ejadah Asset Management Group

- Emrill Services LLC

- Farnek Services LLC

- Bidvest Facilities Management

- Kharafi National for Infrastructure Projects Developments Construction & Services SAE

- Initial Saudi Group

- Sodexo

- Ecolab

- Imdaad

- G4S

- CBRE Group Inc.

- ISS A/S

- Jones Lang LaSalle Incorporated

- Khidmah LLC

- Transguard Group

- Al Shirawi Facilities Management LLC

- Serco Group Middle East

- Aramark Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Infrastructure Development

- 4.2.2 Rising Outsourcing in Building Management

- 4.2.3 Heightened Safety and Security Needs

- 4.2.4 Technological Advancements in Facility Management

- 4.2.5 ESG-Driven Facility Operations Demand

- 4.2.6 FM Demand from Giga Mixed-Use Projects

- 4.3 Market Restraint

- 4.3.1 Skilled Labour Shortages

- 4.3.2 Regulatory Challenges

- 4.3.3 Volatile Economic Conditions and Oil Price Swings

- 4.3.4 Fragmented FM Standards Across MEA Countries

- 4.4 Industry Value Chain Analysis

- 4.5 PESTEL Analysis

- 4.6 Regulatory and Legislative Framework for Market Entrants

- 4.7 Impact of Macroeconomic Indicators on FM Demand

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Services

- 5.1.2 Soft Services

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM

- 5.3 By End-user Industry

- 5.3.1 Commercial (IT and Telecom, Retail and Warehouses)

- 5.3.2 Hospitality (Hotels, Eateries, Large-scale Restaurants)

- 5.3.3 Institutional and Public Infrastructure (Govt, Education, Transportation)

- 5.3.4 Healthcare (Public and Private Facilities)

- 5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

- 5.3.6 Other End-user Industry

- 5.4 By Country

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Kuwait

- 5.4.5 South Africa

- 5.4.6 Egypt

- 5.4.7 Nigeria

- 5.4.8 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Engie Cofely Energy Services LLC (Engie SA)

- 6.4.2 EFS Facilities Services Group

- 6.4.3 Ejadah Asset Management Group

- 6.4.4 Emrill Services LLC

- 6.4.5 Farnek Services LLC

- 6.4.6 Bidvest Facilities Management

- 6.4.7 Kharafi National for Infrastructure Projects Developments Construction & Services SAE

- 6.4.8 Initial Saudi Group

- 6.4.9 Sodexo

- 6.4.10 Ecolab

- 6.4.11 Imdaad

- 6.4.12 G4S

- 6.4.13 CBRE Group Inc.

- 6.4.14 ISS A/S

- 6.4.15 Jones Lang LaSalle Incorporated

- 6.4.16 Khidmah LLC

- 6.4.17 Transguard Group

- 6.4.18 Al Shirawi Facilities Management LLC

- 6.4.19 Serco Group Middle East

- 6.4.20 Aramark Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technology-led Integrated FM (IoT, BMS, AI-based Predictive Maintenance)

- 7.3 ESG-Compliant FM Solutions Demand

- 7.4 Future Service-Model Shifts (Outcome-Based Contracts)

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)