|

市場調查報告書

商品編碼

2035141

中國摩托車市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Two Wheeler - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

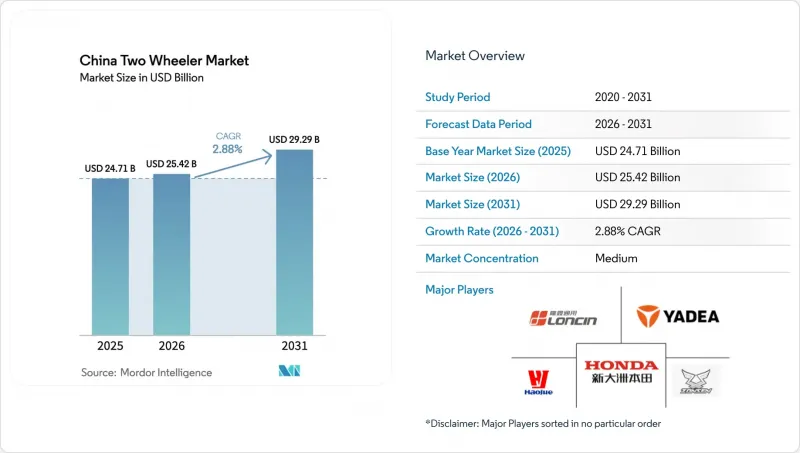

預計到 2026 年,中國摩托車市場規模將達到 254.2 億美元,高於 2025 年的 247.1 億美元,預計到 2031 年將達到 292.9 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 2.88%。

此次市場擴張主要由車主更換到更安全、性能更高的車輛所驅動,但電氣化和更嚴格的安全法規正在重塑競爭格局。華東地區擁有最廣泛的基本客群,這得益於其人口稠密的城市和成熟的供應鏈。然而,西南地區的銷售成長速度最快,基礎設施投資使得即使在山區也能使用電動出行。摩托車仍然是主要的交通工具,但踏板車和電動車的成長速度正在超過摩托車,因為通勤者更喜歡它們的緊湊型車身和補貼電池。價格敏感度依然很強,四分之三的出貨量仍低於1,000美元,但在1,501美元至2,000美元的價格區間,一種微妙的優質化趨勢正在顯現,消費者願意為鋰離子電池、智慧型儀表板和品牌可靠性買單。

中國摩托車市場的趨勢與洞察

政府對電動摩托車提供補助並免徵購置稅

獎勵計畫已顯著降低了電動機車的零售價格,使其成為內燃機汽車的有力競爭者。僅靠燃油成本的降低是無法實現這一目標的。許多城市於2024年春季推出的以舊換新計劃,鼓勵消費者更換到更新、更安全的摩托車型號。同時,監管政策的調整,特別是更新的國家電池安全標準,改變了補貼的資格要求。這些修訂優先考慮安全性和合規性,將財政支援從一般性獎勵轉向更有針對性的措施,重點在於更換老舊或不合規的車輛。

隨著政府扶持政策期限的縮短,製造商意識到情況緊迫,正在加強生產體系建設。然而,由於各地政策執行力度不一,企業正在策略性地調整產品上市時間,以配合當地的資金支持期限。因此,技術創新在經濟繁榮的沿海地區加速傳播,這些地區也成為全國推廣應用的標竿。

都市區擁塞正在推動最後一公里出行需求。

在上海、深圳等充滿活力的城市,尖峰時段的交通堵塞幾乎使車輛平均速度停滯不前。在此背景下,二輪車,尤其是電動機車和電動滑板車,已成為短程出行的最佳選擇,其效率往往遠超貨車。免徵壅塞費的政策使二輪車更加快速經濟,進一步提升了它們的優勢。快速發展的即時配送產業是城市物流的基石,由於二輪車的速度和靈活性,該行業對其依賴程度很高。此外,電池更換服務的日益普及使騎乘者能夠享受全天候的無縫服務,免去了在家充電的麻煩,提高了工作效率。

城市基礎設施正在發生變化,以適應二輪車輛的優勢。例如,試行興建路邊專用停車位和車道等舉措,凸顯了二輪車輛在最後一公里配送中的關鍵作用。然而,儘管共享出行解決方案(例如無樁共享單車)日益受到關注,但它們對於專業的宅配業者而言仍遠遠不夠。對於這些需要更大載貨量和更高可靠性的宅配業者來說,無樁共享單車無法滿足需求。

摩托車駕駛員事故率和死亡率高

2023年,與室內電池充電相關的火災超過21,000起,促使政府從2024年11月起對所有新型電動自行車系統實施更嚴格的強制檢查和CCC認證。與汽車乘員相比,電動自行車的受傷率仍高出每公里15到20倍。地方政府正在試驗強制佩戴頭盔和設立電動二輪車專用車道,這表明政府正在加強安全監管。保險公司正在推出第三方責任責任險選項,導致高速車型的保費略有上漲。製造商為了符合新的國家車架和電池安全標準,承擔了更高的生產成本。雖然這些調整導致了更高的成本,但也提振了消費者的信心,並凸顯了市場正在轉向更注重安全性和可靠性的方向。

細分市場分析

在中國二輪車市場,摩托車預計到2025年將佔市場佔有率的69.12%,但踏板車預計將以4.12%的複合年成長率快速成長至2031年,這主要得益於其便捷的跨騎式人體工學設計,使其在擁擠的道路上更具優勢。隨著收入的成長,週末日益普及,大排氣量休閒摩托車預計在2024年初迎來顯著成長。配備人工智慧語音助理和OTA升級功能的數位化叢集已成為中階車型的標配,類似於汽車的儀表板。雖然摩托車憑藉更長的燃料箱里程和堅固的車架在農村騎行者中仍然佔據主導地位,但踏板車憑藉其停車便利性和自動變速箱等優勢,正在城市通勤者中越來越受歡迎。

都市區踏板車的流行得益於地方政府禁止大型摩托車進入市中心的法規,這使得人們對輕型踏板車的需求轉向了更輕的車型。各品牌紛紛為踏板車配備標準配置,例如座椅下方的鋰離子電池和NFC啟動鑰匙,從而將平均售價推高至1501至頻寬美元。從智慧頭盔到應用程式訂閱等配件收入進一步提升了利潤率,即便成熟的二輪車市場銷售成長放緩。

即使到了2025年,內燃機摩托車仍將佔據中國摩托車市場71.84%的佔有率,但預計到2031年,電動車將以7.05%的複合年成長率成長,這主要得益於補貼、充電網路建設和排放控制區的擴大。雅迪和泰爾格聯合研發的鈉離子電池原型於2024年問世,實現了3000次循環壽命,同時將電池組成本降低了10-15%。沿海城市電動送貨車正迅速普及,這得益於營運成本的降低和都市區交通的便利。同時,由於基礎設施不足以及電池價格亟待進一步降低,農村地區仍高度依賴汽油車。這種都市區差距凸顯了電氣化進程的進展以及全國範圍內實現電氣化轉型仍需克服的挑戰。

電動車製造商正透過建造換電站和將即時定位追蹤功能整合到應用程式中來解決續航里程問題。傳統內燃機(ICE)製造商正在提高燃油效率並改善引擎以滿足更嚴格的排放氣體法規,但由於碳排放法規日益嚴格,市場正在萎縮。混合動力汽車由於其複雜的結構和缺乏補貼,仍然是一個小眾市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章:主要產業趨勢

- 人口和都市化

- 人均GDP(購買力平價)和可支配所得中位數

- 汽車購買和交通運輸的消費者支出(CVP)

- 燃油價格

- 取得摩托車和汽車貸款利率及信用使用資訊。

- 摩托車擁有率(每千人擁有的車輛數)和車輛擁有量

- 經銷商/服務網路密度

- 摩托車貿易及收入(進口/出口)

- 電氣化準備(基礎設施和電力)

- 電池組價格和化學成分

- 電池更換站(安裝密度和利用率)

- 新車型陣容和OEM覆蓋範圍

- 價值鏈本地化和組裝能力

- 法律規範

- 車輛標準、安全性與駕駛性能

- CBU/CKD/SKD 關稅、增值稅(VAT) 和在地採購稅率的規定

- 電氣化、能源與環境政策

- 關於摩托車計程車、送貨車輛和資金籌措。

第5章 市場狀況

- 市場概覽

- 市場促進因素

- 政府對電動摩托車提供補助和免徵購置稅

- 都市區擁塞正在推動最後一公里出行需求。

- 與汽車和公共交通相比,總擁有成本更低

- 電子商務配送量激增

- 在三、四線城市擴展電池更換生態系統

- 利用人工智慧驅動的遠端資訊處理技術最佳化車輛運轉率。

- 市場限制因素

- 摩托車事故和死亡率高

- 鋰和石墨供應鏈的波動性

- 對低速電動自行車制定更嚴格的分類規則

- 與共享微出行平台的競爭

- 價值/供應鏈分析

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第6章 市場規模及成長預測(價值(美元)及數量(單位))

- 車輛類型

- 摩托車

- 小型摩托車

- 透過推進力

- 內燃機

- 電

- 按引擎排氣量/馬達輸出功率

- 內燃機

- 110cc或以下

- 111~125cc

- 126~150cc

- 151~200cc

- 201~250cc

- 250~350cc

- 350~500cc

- 500cc或以上

- 電

- 1.0 千瓦或以下

- 1.1~3.0 kW

- 3.1~5.0 kW

- 5.0度或以上

- 內燃機

- 按價格範圍

- 低於1000美元

- 1000美元至1500美元

- 1,501美元至2,000美元

- 2001-3000美元

- 3001-5000美元

- 超過5000美元

- 最終用戶

- B2C

- B2B

- 共乘/自行車計程車/租賃/觀光

- 配送/物流

- 為企業和中小企業提供車隊

- 其他(政府、非政府組織、其他機構)

- 銷售管道

- 線上

- 離線

- 按地區

- 華東

- 中國中南部

- 華北

- 中國東北

- 中國西南地區

- 中國西北地區

第7章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Yadea Group Holdings Ltd.

- Jiangsu Xinri E-Vehicle Co., Ltd.(SUNRA)

- Zhejiang Luyuan Electric Vehicle Co., Ltd.

- NIU Technologies

- Tailing Electric Vehicle Co., Ltd.

- Wuyang-Honda Motors(Guangzhou)Co., Ltd.

- Sundiro Honda Motorcycle Co., Ltd.

- Guangzhou Dayun Motorcycle Co., Ltd.

- Jiangmen Dachangjiang Group Co., Ltd.(Haojue)

- Loncin Motor Co., Ltd.

- Lifan Technology(Group)Co., Ltd.

- Chongqing Zongshen Industrial Group Co., Ltd.

- Qingqi Group Co., Ltd.

- Chongqing Huansong Industries(HSUN)

- Tayo Motorcycle Technology(Qingdao)Co., Ltd.

- Zhe Jiang Qianjiang Motorcycle Co., Ltd.(QJMotor)

第8章 市場機會與未來展望

- 評估未開發的領域和未滿足的需求

第9章:執行長面臨的主要策略挑戰:

China two-wheeler market size in 2026 is estimated at USD 25.42 billion, growing from 2025 value of USD 24.71 billion with 2031 projections showing USD 29.29 billion, growing at 2.88% CAGR over 2026-2031.

Expansion is driven mainly by owners upgrading to safer, more capable machines, while electrification and tighter safety rules reshape competitive strategy. East China retains the most extensive customer base because of dense cities and mature supply chains. Yet, Southwest China posts the fastest volume gains as infrastructure investments open hilly terrain to electric mobility. Motorcycles stay dominant for mixed-use transport, but scooters and electric variants outpace them in growth as commuters favor compact frames and subsidy-eligible batteries. Price sensitivity remains acute-three-quarters of deliveries are still below USD 1,000-but gradual premiumization is visible in the USD 1,501-2,000 bracket where riders pay for lithium packs, connected dashboards, and brand reliability.

China Two Wheeler Market Trends and Insights

Government e-2W Subsidies and Purchase-Tax Exemption

Incentive programs have slashed the retail prices of electric bikes, positioning them as a competitive alternative to internal combustion engine (ICE) vehicles, and doing so much sooner than fuel savings would allow. A spring 2024 trade-in initiative, embraced by numerous cities, is nudging consumers towards upgrading to newer, safer bike models. Meanwhile, regulatory shifts, especially the updated national battery safety standards, alter subsidy eligibility criteria. These revisions prioritize safety and compliance, redirecting financial support from generalized incentives to a more targeted approach, focusing on replacing outdated or non-compliant units.

Sensing the urgency as the window for government aid tightens, manufacturers are ramping up operations. However, regional policy rollout disparities mean companies strategically timing product launches to coincide with local funding windows. This has led to a quicker dissemination of technological advancements in the economically vibrant coastal regions, setting a benchmark for national adoption.

Urban Congestion Driving Last-mile Demand

In bustling cities such as Shanghai and Shenzhen, peak-hour traffic congestion has brought average vehicle speeds to a standstill. Amidst this backdrop, two-wheelers-particularly electric motorcycles and scooters-have emerged as the preferred choice for short-distance travel, often leaving vans in the dust. Their edge is heightened by policies exempting motorcycles from congestion charges, making them swifter and more economical. The surging instant-delivery sector, a linchpin of urban logistics, heavily leans on two-wheelers for their speed and adaptability. Moreover, the rising popularity of battery-swap services ensures riders enjoy seamless service throughout the day, sidestepping the hassle of home charging and boosting productivity.

Urban infrastructure is adapting to this two-wheeler dominance. Initiatives like dedicated curbside parking and exclusive lane pilot programs underscore the pivotal role of two-wheelers in last-mile delivery. Yet, while shared mobility solutions, such as dockless bikes, have made waves, they've fallen short for professional couriers. These couriers, needing greater payload capacity and reliability, find dockless bikes lacking.

High Accident and Fatality Rates among Riders

Fire incidents linked to indoor battery charging topped 21,000 cases in 2023, prompting tougher inspections and CCC certification for every new e-bike system from November 2024. Injury rates remain 15-20 times higher than car occupants per kilometer. Municipal governments are piloting helmet mandates and dedicated lanes for electric two-wheelers, marking a move towards heightened safety oversight. Insurance firms are rolling out third-party coverage options, marginally bumping costs for swifter models. Manufacturers are shouldering increased production costs to align with new national standards on vehicle frames and battery safety. Although these adjustments increase expenses, they enhance consumer trust and underscore a market shift prioritizing safety and reliability.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Delivery Boom

- Low Total Cost of Ownership

- Lithium and Graphite Supply-chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Motorcycles account for 69.12% of the China two-wheeler market size in 2025, yet scooters are surging ahead at a 4.12% CAGR through 2031, thanks to step-through ergonomics that are favored in crowded streets. Large-displacement leisure bikes are expected to experience significant growth in early 2024, as rising incomes add weekend touring to the use-case mix. Digital clusters with AI voice assistants and OTA updates are now standard on mid-tier models, mirroring car dashboards. Rural riders keep motorcycles in front through fuel-tank range and robust frames, but in downtown cores, scooter parking privileges and automatic gearboxes are winning commuters.

Urban scooter uptake also benefits from local rules barring full-size motorcycles from central districts, tilting replacement cycles toward lighter frames. Brands package under-seat lithium packs and NFC start keys, pushing ASPs into the USD 1,501-2,000 band. Accessory revenue-from smart helmets to app subscriptions-deepens margins even as unit growth moderates in the mature motorcycle segment.

Internal combustion engines still account for 71.84% of the China two-wheeler market size in 2025, but electric vehicles are growing at a compound annual rate of 7.05% to 2031, as subsidies, charging networks, and emission zones expand. Sodium-ion prototypes from Yadea and Tailg debuted in 2024, offering 3,000-cycle life while trimming 10-15% off pack cost. Coastal cities are witnessing a rapid expansion of electric delivery fleets, driven by low operating costs and improved urban access. Meanwhile, rural regions rely heavily on gasoline vehicles, hindered by limited infrastructure and the need for further reductions in battery prices. This urban-rural disparity underscores the progress in electrification and the hurdles that still need to be addressed for a nationwide shift.

Electric vehicle manufacturers are addressing range anxiety by deploying battery swap stations and integrating real-time location tracking into their apps. Traditional internal combustion engine (ICE) makers are improving fuel efficiency and updating engines to meet stricter emissions standards, though tightening carbon regulations are shrinking their market. Hybrid vehicles remain a niche market due to their added complexity and the lack of subsidies.

The China Two Wheeler Market Report is Segmented by Vehicle Type (Motorcycles and Scooters), Propulsion (ICE and Electric), Engine Capacity/Motor Power (Up To 110cc, and More), Price Band (Up To USD 1, 000, and More), End User (B2C and B2B), Sales Channel (Online and Offline), and by Region. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Yadea Group Holdings Ltd.

- Jiangsu Xinri E-Vehicle Co., Ltd. (SUNRA)

- Zhejiang Luyuan Electric Vehicle Co., Ltd.

- NIU Technologies

- Tailing Electric Vehicle Co., Ltd.

- Wuyang-Honda Motors (Guangzhou) Co., Ltd.

- Sundiro Honda Motorcycle Co., Ltd.

- Guangzhou Dayun Motorcycle Co., Ltd.

- Jiangmen Dachangjiang Group Co., Ltd. (Haojue)

- Loncin Motor Co., Ltd.

- Lifan Technology (Group) Co., Ltd.

- Chongqing Zongshen Industrial Group Co., Ltd.

- Qingqi Group Co., Ltd.

- Chongqing Huansong Industries (HSUN)

- Tayo Motorcycle Technology (Qingdao) Co., Ltd.

- Zhe Jiang Qianjiang Motorcycle Co., Ltd. (QJMotor)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Key Industry Trends

- 4.1 Population and Urbanization Rate

- 4.2 GDP per Capita (PPP) and Median Disposable Income

- 4.3 Consumer Spend on Vehicle Purchase/Transport (CVP)

- 4.4 Fuel Prices

- 4.5 Interest Rate for 2W/Auto Loans and Credit Access

- 4.6 2W Penetration (units/1,000) and Parc

- 4.7 Dealer/Service Network Density

- 4.8 Two-Wheeler Trade and Revenue (Imports/Exports)

- 4.9 Electrification Readiness (Infrastructure and Power)

- 4.10 Battery Pack Price and Chemistry Mix

- 4.11 Battery Swapping Stations (Density and Utilization)

- 4.12 New Model Pipeline and OEM Coverage

- 4.13 Value-Chain Localization and Assembly Capacity

- 4.14 Regulatory Framework

- 4.14.1 Vehicle Standards, Safety and Roadworthiness

- 4.14.2 CBU/CKD/SKD Duties, VAT and Local-content Rules

- 4.14.3 Electrification, Energy and Environmental Policy

- 4.14.4 Rules for Bike-taxis, Delivery Fleets and Financing

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Government e-2W Subsidies and Purchase Tax Exemption

- 5.2.2 Urban Congestion Driving Last-mile Demand

- 5.2.3 Low Total Cost of Ownership vs. Cars and Public Transit

- 5.2.4 E-commerce Delivery Boom

- 5.2.5 Tier-3/4 City Battery-Swapping Ecosystem Expansion

- 5.2.6 AI-enabled Telematics Optimising Fleet Utilisation

- 5.3 Market Restraints

- 5.3.1 High Accident and Fatality Rates among Riders

- 5.3.2 Lithium and Graphite Supply-chain Volatility

- 5.3.3 Stricter Classification Rules for Low-speed E-bikes

- 5.3.4 Competition from Shared Micromobility Platforms

- 5.4 Value / Supply-Chain Analysis

- 5.5 Technological Outlook

- 5.6 Porter's Five Forces

- 5.6.1 Threat of New Entrants

- 5.6.2 Bargaining Power of Suppliers

- 5.6.3 Bargaining Power of Buyers

- 5.6.4 Threat of Substitutes

- 5.6.5 Competitive Rivalry

6 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 6.1 By Vehicle Type

- 6.1.1 Motorcycles

- 6.1.2 Scooters

- 6.2 By Propulsion

- 6.2.1 Internal Combustion Engine

- 6.2.2 Electric

- 6.3 By Engine Capacity / Motor Power

- 6.3.1 Internal Combustion Engine

- 6.3.1.1 Up to 110 cc

- 6.3.1.2 111-125 cc

- 6.3.1.3 126-150 cc

- 6.3.1.4 151-200 cc

- 6.3.1.5 201-250 cc

- 6.3.1.6 250-350 cc

- 6.3.1.7 350-500 cc

- 6.3.1.8 Above 500 cc

- 6.3.2 Electric

- 6.3.2.1 Up to 1.0 kW

- 6.3.2.2 1.1-3.0 kW

- 6.3.2.3 3.1-5.0 kW

- 6.3.2.4 Above 5.0 kW

- 6.3.1 Internal Combustion Engine

- 6.4 By Price Band

- 6.4.1 Up to USD 1,000

- 6.4.2 USD 1,000-1,500

- 6.4.3 USD 1,501-2,000

- 6.4.4 USD 2,001-3,000

- 6.4.5 USD 3,001-5,000

- 6.4.6 Above USD 5,000

- 6.5 By End User

- 6.5.1 B2C

- 6.5.2 B2B

- 6.5.2.1 Ride-hail / Bike-Taxi / Rental / Tourism

- 6.5.2.2 Delivery and Logistics

- 6.5.2.3 Corporate and SME Fleets

- 6.5.2.4 Others (Govt., NGO, Institutional)

- 6.6 Sales Channel

- 6.6.1 Online

- 6.6.2 Offline

- 6.7 By Region

- 6.7.1 East China

- 6.7.2 South-Central China

- 6.7.3 North China

- 6.7.4 Northeast China

- 6.7.5 Southwest China

- 6.7.6 Northwest China

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 Yadea Group Holdings Ltd.

- 7.4.2 Jiangsu Xinri E-Vehicle Co., Ltd. (SUNRA)

- 7.4.3 Zhejiang Luyuan Electric Vehicle Co., Ltd.

- 7.4.4 NIU Technologies

- 7.4.5 Tailing Electric Vehicle Co., Ltd.

- 7.4.6 Wuyang-Honda Motors (Guangzhou) Co., Ltd.

- 7.4.7 Sundiro Honda Motorcycle Co., Ltd.

- 7.4.8 Guangzhou Dayun Motorcycle Co., Ltd.

- 7.4.9 Jiangmen Dachangjiang Group Co., Ltd. (Haojue)

- 7.4.10 Loncin Motor Co., Ltd.

- 7.4.11 Lifan Technology (Group) Co., Ltd.

- 7.4.12 Chongqing Zongshen Industrial Group Co., Ltd.

- 7.4.13 Qingqi Group Co., Ltd.

- 7.4.14 Chongqing Huansong Industries (HSUN)

- 7.4.15 Tayo Motorcycle Technology (Qingdao) Co., Ltd.

- 7.4.16 Zhe Jiang Qianjiang Motorcycle Co., Ltd. (QJMotor)

8 Market Opportunities and Future Outlook

- 8.1 White-space and Unmet-need Assessment

9 Key Strategic Questions for CEOs

摩托車市場-全球產業規模、佔有率、趨勢、機會和預測:按車型、動力系統、地區和競爭格局分類,2021-2031年

摩托車市場-全球產業規模、佔有率、趨勢、機會和預測:按車型、動力系統、地區和競爭格局分類,2021-2031年 摩托車市場:2026年至2032年全球預測(按車型、動力系統、性能類型、類別、變速箱類型、價格範圍、應用和最終用戶分類)

摩托車市場:2026年至2032年全球預測(按車型、動力系統、性能類型、類別、變速箱類型、價格範圍、應用和最終用戶分類) 摩托車照明市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年摩托車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

摩托車照明市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年摩托車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 日本摩托車市場:規模、佔有率、趨勢和預測:按類型、技術、變速箱、引擎排氣量、燃料類型、分銷管道、最終用戶和地區分類(2026-2034 年)

日本摩托車市場:規模、佔有率、趨勢和預測:按類型、技術、變速箱、引擎排氣量、燃料類型、分銷管道、最終用戶和地區分類(2026-2034 年) 印度摩托車市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

印度摩托車市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 摩托車市場機會、成長要素、產業趨勢分析及2026年至2035年預測歐洲摩托車市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031)

摩托車市場機會、成長要素、產業趨勢分析及2026年至2035年預測歐洲摩托車市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031) 摩托車智能化與產業鏈(2025-2026)

摩托車智能化與產業鏈(2025-2026) 全球摩托車市場

全球摩托車市場