|

市場調查報告書

商品編碼

1934835

越南資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Vietnam ICT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

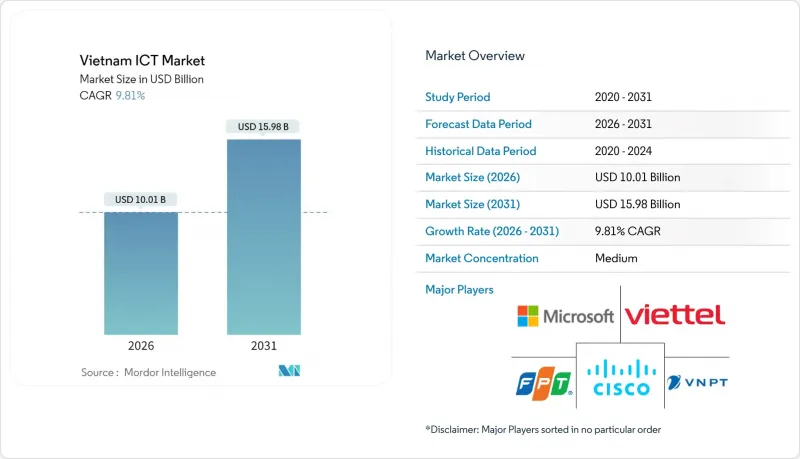

越南資訊通訊技術市場規模在 2025 年達到 91.2 億美元,預計到 2031 年將達到 159.8 億美元,高於 2026 年的 100.1 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 9.81%。

政府主導的數位化專案、大規模外商直接投資以及半導體生產在地化的推進,持續加速硬體、軟體和服務領域的數位轉型。大規模的5G部署,以及不斷擴大的雲端和資料中心容量,正在為通訊業者和全球超大規模資料中心業者創造新的收入來源。同時,越南48個市級政府的智慧城市建設項目,推動了對整合連接、分析和網路安全解決方案的需求。國營通訊業者與跨國技術供應商之間的競爭格局較為平衡,後者正不斷深化與本地企業的夥伴關係,以滿足特定產業的數位轉型需求。儘管面臨資金限制和省會城市高技能工程人才短缺等不利因素,但隨著企業實現營運現代化並拓展新的數位化服務模式,越南資訊通訊技術市場預計到2030年仍將保持兩位數的成長。

越南資訊通訊技術市場趨勢與洞察

智慧城市基礎建設發展計劃

政府核准了48個市政數位化藍圖,由此催生了價值20億美元的互聯互通、感測器網路和網路安全平台專案儲備。胡志明市防洪系統的升級和峴港市的永續城市規劃都需要即時數據分析,推動了對邊緣運算和物聯網閘道的需求。公共部門至少10%的IT預算必須用於網路安全,這進一步擴大了威脅偵測供應商的潛在市場。國家數位身分識別系統「VNeID」的推出已惠及數百萬公民,並正在擴展電子政府入口網站的身份驗證服務。這些計劃為通訊業者、雲端服務供應商和系統整合商創造了協同效應,同時也將越南打造成為區域智慧城市解決方案的試驗場。

工業4.0價值鏈中的數位轉型

實施人工智慧驅動的預測維修系統的製造工廠報告稱,生產效率提高了30%至50%。紡織品出口商Vinatex在實施物聯網賦能的供應鏈分析後,連合收益成長了6.1%。三星9.2億美元的擴張計畫證實了越來越多的資金流入基於機器學習的品管和自動化物流領域。第109號法令降低了本地生產車輛的註冊稅,透過機器人技術和連網工廠平台加速了汽車產業的數位化。基於區塊鏈的溯源追蹤和人工智慧增強的需求預測正在幫助越南製造商贏得高利潤的全球訂單,同時縮短產品上市時間。

建設網路和資料中心的初始投資成本很高

5G頻譜、光纖回程傳輸和三級資料中心建設的高資本密集度給營運商的財務狀況帶來了壓力,尤其是在兩個大都會圈以外的地區。農村地區的需求密度往往低於利用標準,導致投資者的投資回收期延長。匯率波動風險和利率上升推高了資金籌措成本,而土地使用核准也面臨行政延誤。儘管公私合營模式興起,但小規模本地通訊業者和中立鐵塔公司仍面臨資金籌措缺口。這些限制因素可能會延緩農村寬頻部署進程,並限制邊緣運算的覆蓋範圍,而邊緣運算是許多工業4.0應用場景所必需的。

細分市場分析

到2025年,IT硬體將維持越南ICT市場22.88%的佔有率,這主要得益於通訊業者升級基地台和資料中心設施以支援全國5G骨幹網路建設。然而,隨著基礎建設的日益成熟,越南ICT市場硬體部分的成長速度預計將低於服務部分。同時,在諮詢、系統整合和託管安全計劃等需要專業知識的推動下,IT服務預計到2031年將以12.07%的複合年成長率成長。混合雲端、ERP現代化和人工智慧實施需要持續的專業服務支持,這將為供應商和整合商創造穩定的收入來源。

企業對計量收費可擴展性的追求正在加速雲端服務的普及,從而推動對營運商提供的連接服務和網路安全解決方案的需求。隨著企業從永久授權轉向基於訂閱的SaaS模式,軟體收入也在成長,降低了前期成本。電信服務受惠於行動數據消費的成長和企業5G應用場景的擴展。託管服務協議,尤其是網路安全監控服務,使中小企業能夠外包複雜功能,並以最少的人力滿足監管要求。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 智慧城市基礎建設發展計劃

- 工業4.0價值鏈中的數位轉型

- 雲端運算和人工智慧領域的資本支出激增

- 政府的「越南製造」數位經濟藍圖

- 提高半導體自給自足能力的獎勵

- 建構超大規模和區域性IDC中心

- 市場限制

- 網路和資料中心建設初期成本高昂

- 專業資訊通訊技術人員短缺

- 對進口核心零件的高度依賴

- 分散網路安全合規的負擔

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 重大技術投資

- 雲端運算

- 人工智慧

- 網路安全

- 數位服務

- 邊緣運算和物聯網

- 重大技術投資

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 生態系分析

- 產業相關人員分析

- 新冠疫情及宏觀環境變化的影響及復甦

第5章 市場規模與成長預測

- 按類型

- IT硬體

- 電腦硬體

- 網路裝置

- 周邊設備

- IT軟體

- IT服務

- 託管服務

- 業務流程服務

- 商業諮詢服務

- 雲端服務

- IT基礎設施

- 通訊服務

- IT硬體

- 按最終用戶公司規模分類

- 小型企業

- 主要企業

- 按最終用戶行業分類

- 政府和公共機構

- BFSI

- 能源與公共產業

- 零售、電子商務與物流

- 製造業和工業4.0

- 醫療保健和生命科學

- 石油和天然氣(上游、中游、下游)

- 遊戲和電子競技

- 其他行業

- 按行業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- Cisco Systems Inc.

- Viettel Group

- VNPT Group

- FPT Corporation

- CMC Corporation

- Qualcomm Technologies Inc.

- Google LLC(Alphabet Inc.)

- Fujitsu Ltd.

- Fortinet Inc.

- Vietnamobile

- D-Link Systems Inc.

- Hewlett Packard Enterprise

- Telehouse Vietnam

- Oracle Corporation

- IBM Corporation

- Samsung Electronics Vietnam

- VNG Corporation

- MobiFone

- TMA Solutions

- KMS Technology

- NashTech

- Axon Active Vietnam

- Ciena Corporation

- Ericsson Vietnam

第7章 市場機會與未來展望

The Vietnam ICT market was valued at USD 9.12 billion in 2025 and estimated to grow from USD 10.01 billion in 2026 to reach USD 15.98 billion by 2031, at a CAGR of 9.81% during the forecast period (2026-2031).

Government-led digitalization programs, sizable foreign direct investment, and the push to localize semiconductor production continue to accelerate adoption across hardware, software, and services. Large-scale 5G rollouts, paired with expanding cloud and data-center capacity, are fueling new revenue streams for telecommunications operators and global hyperscalers. At the same time, smart-city initiatives in 48 municipalities are driving demand for integrated connectivity, analytics, and cybersecurity solutions. The competitive dynamic remains balanced between state-owned carriers and multinational technology vendors that are deepening local partnerships to address industry-specific digital-transformation mandates. Although funding constraints in secondary cities and a shortage of advanced engineering talent pose headwinds, the Vietnam ICT market is expected to maintain double-digit momentum through 2030 as enterprises modernize operations and new digital-services models scale.

Vietnam ICT Market Trends and Insights

Smart-City Infrastructure Programs

Government approval of 48 municipal digitalization roadmaps has created a USD 2 billion pipeline for connectivity, sensor networks, and cybersecurity platforms. Ho Chi Minh City's flood-management upgrade and Da Nang's sustainable-city plan both require real-time data analytics, strengthening demand for edge computing and IoT gateways. Mandatory allocation of at least 10% of public-sector IT budgets to cybersecurity further expands the addressable market for threat-detection vendors. The national VNeID digital-identity roll-out already serves millions of citizens and is scaling authentication services for e-government portals. These projects generate multiplier effects for telecom carriers, cloud providers, and systems integrators while positioning Vietnam as a testbed for regional smart-city solutions.

Digital Transformation Across Industry 4.0 Value Chains

Manufacturing plants adopting AI-driven predictive-maintenance systems report production-efficiency gains of 30-50%. Textile exporters such as Vinatex have boosted consolidated revenue by 6.1% after deploying IoT-enabled supply-chain analytics. Samsung's USD 920 million expansion underscores rising capital inflows devoted to machine-learning-based quality control and automated logistics. Decree 109, which lowered registration taxes for locally produced vehicles, has accelerated automotive digitalization through robotics and connected-factory platforms. Blockchain-powered provenance tracking and AI-enhanced demand forecasting are helping Vietnamese manufacturers capture higher-margin global orders while shortening time-to-market.

High Up-Front Network and Data-Center Build Costs

The capital intensity of 5G spectrum, fiber backhaul, and Tier III data-center construction strains operator balance sheets, especially outside the two largest metros. Secondary cities often lack the demand density to hit utilization thresholds, extending payback periods for investors. Currency fluctuation risk and rising interest rates elevate funding costs, while land-use approvals add administrative delays. Although public-private-partnership models are emerging, financing gaps persist for small regional carriers and neutral-host tower companies. These constraints could defer rural broadband timelines and limit edge-computing coverage that many Industry 4.0 use cases require.

Other drivers and restraints analyzed in the detailed report include:

- Surging Cloud- and AI-Linked Capex

- "Make-in-Vietnam" Digital-Economy Roadmap

- Shortage of Specialized ICT Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IT Hardware maintained a 22.88% share of the Vietnam ICT market in 2025 as operators upgraded base-station and data-center equipment to support nationwide 5G backbones. However, the Vietnam ICT market size for hardware is expected to expand more slowly than that for services as infrastructure build-outs mature. In contrast, IT Services is on track for a 12.07% CAGR through 2031, propelled by consulting, systems integration, and managed-security projects that require specialized know-how. Hybrid cloud, ERP modernization, and AI implementation demand continuous professional-services support, creating sticky revenue streams for vendors and integrators.

Cloud-services adoption is escalating as enterprises pursue pay-as-you-go scalability; this, in turn, lifts demand for connectivity and cybersecurity offerings bundled by telecom carriers. Software revenue is also climbing as firms migrate from perpetual licenses to subscription-based SaaS, lowering up-front costs. Communication services benefit from growing mobile-data consumption and enterprise 5G use cases. Managed-services contracts, especially for cybersecurity monitoring, allow SMEs to outsource complex functions and keep headcount lean while meeting regulatory mandates.

The Vietnam ICT Market Report is Segmented by Type (IT Hardware, IT Software, IT Services, IT Infrastructure, Communication Services), End-User Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-User Industry Vertical (Government and Public Administration, BFSI, Energy and Utilities, Retail, E-Commerce and Logistics, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Microsoft Corporation

- Cisco Systems Inc.

- Viettel Group

- VNPT Group

- FPT Corporation

- CMC Corporation

- Qualcomm Technologies Inc.

- Google LLC (Alphabet Inc.)

- Fujitsu Ltd.

- Fortinet Inc.

- Vietnamobile

- D-Link Systems Inc.

- Hewlett Packard Enterprise

- Telehouse Vietnam

- Oracle Corporation

- IBM Corporation

- Samsung Electronics Vietnam

- VNG Corporation

- MobiFone

- TMA Solutions

- KMS Technology

- NashTech

- Axon Active Vietnam

- Ciena Corporation

- Ericsson Vietnam

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smart-city infrastructure programmes

- 4.2.2 Digital transformation across Industry 4.0 value-chains

- 4.2.3 Surging cloud- and AI-linked capex

- 4.2.4 Government "Make-in-Vietnam" digital-economy roadmap

- 4.2.5 Semiconductor self-sufficiency incentives

- 4.2.6 Hyperscale and regional IDC hub build-out

- 4.3 Market Restraints

- 4.3.1 High up-front network and data-centre build costs

- 4.3.2 Shortage of specialised ICT talent

- 4.3.3 Heavy reliance on imported core components

- 4.3.4 Fragmented cyber-regulatory compliance burden

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Key Technology Investments

- 4.6.1.1 Cloud Technology

- 4.6.1.2 Artificial Intelligence

- 4.6.1.3 Cyber-security

- 4.6.1.4 Digital Services

- 4.6.1.5 Edge Computing and IoT

- 4.6.1 Key Technology Investments

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Ecosystem Analysis

- 4.9 Industry Stakeholder Analysis

- 4.10 Impact and Recovery from COVID-19 and Macro Shifts

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 IT Hardware

- 5.1.1.1 Computer Hardware

- 5.1.1.2 Networking Equipment

- 5.1.1.3 Peripherals

- 5.1.2 IT Software

- 5.1.3 IT Services

- 5.1.3.1 Managed Services

- 5.1.3.2 Business Process Services

- 5.1.3.3 Business Consulting Services

- 5.1.3.4 Cloud Services

- 5.1.4 IT Infrastructure

- 5.1.5 Communication Services

- 5.1.1 IT Hardware

- 5.2 By End-User Enterprise Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By End-user Industry Vertical

- 5.3.1 Government and Public Administration

- 5.3.2 BFSI

- 5.3.3 Energy and Utilities

- 5.3.4 Retail, E-commerce and Logistics

- 5.3.5 Manufacturing and Industry 4.0

- 5.3.6 Healthcare and Life Sciences

- 5.3.7 Oil and Gas (Up-, Mid-, Down-stream)

- 5.3.8 Gaming and Esports

- 5.3.9 Other Verticals

- 5.3.10 By Industry Vertical (Value)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Cisco Systems Inc.

- 6.4.3 Viettel Group

- 6.4.4 VNPT Group

- 6.4.5 FPT Corporation

- 6.4.6 CMC Corporation

- 6.4.7 Qualcomm Technologies Inc.

- 6.4.8 Google LLC (Alphabet Inc.)

- 6.4.9 Fujitsu Ltd.

- 6.4.10 Fortinet Inc.

- 6.4.11 Vietnamobile

- 6.4.12 D-Link Systems Inc.

- 6.4.13 Hewlett Packard Enterprise

- 6.4.14 Telehouse Vietnam

- 6.4.15 Oracle Corporation

- 6.4.16 IBM Corporation

- 6.4.17 Samsung Electronics Vietnam

- 6.4.18 VNG Corporation

- 6.4.19 MobiFone

- 6.4.20 TMA Solutions

- 6.4.21 KMS Technology

- 6.4.22 NashTech

- 6.4.23 Axon Active Vietnam

- 6.4.24 Ciena Corporation

- 6.4.25 Ericsson Vietnam

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

新加坡資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

新加坡資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球資訊與通訊技術(ICT)市場規模、佔有率、趨勢及成長分析報告(2026-2034)印度資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利資訊通訊技術市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)菲律賓資訊通訊技術市場:市場佔有率分析、行業趨勢與統計、成長預測(2026-2031年)零售業先進資訊與通訊解決方案的成長機遇資訊通訊科技(ICT)產業客戶經驗(CX)成長機會,2025-2026年醫療保健產業先進資訊與通訊解決方案的成長機會

全球資訊與通訊技術(ICT)市場規模、佔有率、趨勢及成長分析報告(2026-2034)印度資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利資訊通訊技術市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)菲律賓資訊通訊技術市場:市場佔有率分析、行業趨勢與統計、成長預測(2026-2031年)零售業先進資訊與通訊解決方案的成長機遇資訊通訊科技(ICT)產業客戶經驗(CX)成長機會,2025-2026年醫療保健產業先進資訊與通訊解決方案的成長機會 NTN和D2C商業模式的演變

NTN和D2C商業模式的演變