|

市場調查報告書

商品編碼

1911723

菲律賓資訊通訊技術市場:市場佔有率分析、行業趨勢與統計、成長預測(2026-2031年)Philippines ICT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

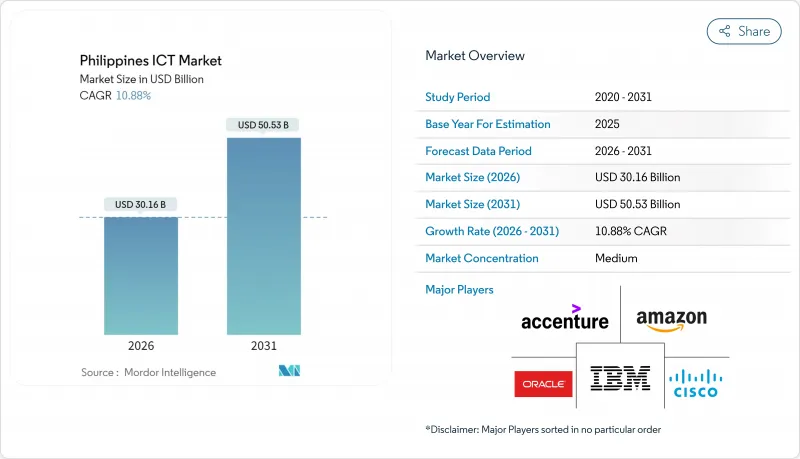

預計到 2025 年,菲律賓 ICT 市場價值將達到 272 億美元,從 2026 年的 301.6 億美元成長到 2031 年的 505.3 億美元,在預測期(2026-2031 年)內複合年成長率為 10.88%。

這一強勁的成長軌跡反映了該國自由化的外商投資環境、大規模的5G部署、超過100億美元的超大規模資料中心投資計劃,以及政府旨在將70%以上的公共服務數位化的計劃。對雲端運算、邊緣運算和網路安全解決方案日益成長的需求正在推動支出成長,而鐵塔共用政策和新成立的通用鐵塔公司正在擴大網路覆蓋範圍,惠及服務不足的農村地區。同時,菲律賓資訊通訊技術市場正受益於東協供應鏈的多元化,吸引半導體組裝、數據分析和人工智慧等工作負載進入該國不斷成長的技能人才庫。固網營運商和行動通訊業者之間日益激烈的競爭通訊業者了電信資費的下降趨勢,同時也促進了對光纖回程傳輸、專用5G和衛星通訊鏈路的投資,從而有助於提高服務品質和地理覆蓋範圍。

菲律賓資訊通訊技術市場趨勢與洞察

快速部署 5G 推動基礎架構現代化

在菲律賓商業資訊通訊技術(ICT)市場,網路現代化正在加速推進。 Globe和PLDT計劃到2025年在地理位置偏遠且服務不足的地區(GIDA)聯合增設100多個5G基地台。擴展的中波頻譜和新建的Apricot海底光纜將使國際容量提升33%,使菲律賓成為超大規模流量的冗餘樞紐。 5G專用網路正在擴展到物流、採礦和精密農業等光纖鋪設難度較高的領域。同時,新資料中心邊緣節點的延遲已低於10毫秒,這對於智慧工廠分析至關重要。通訊業者也嘗試開放式無線接取網路(Open RAN),以降低無線成本並實現供應商多元化,從而提高長期資本效率。這些努力共同深化並增強了菲律賓的互聯互通,支援低延遲應用,並提升了菲律賓ICT市場對全球雲端服務供應商的吸引力。

政府電子政府總體規劃加速公共部門數位化

資訊通訊技術部 (DICT) 已著手實現其電子化政府目標,目前已將 70% 的公共服務上線,發放了超過一百萬份數位數位簽章,並在偏遠村鎮(政府轄區)安裝了 438 個 VSAT 終端。隨著政府機構將其資料庫遷移到主權雲,對安全可靠的 IaaS、SaaS 和整合服務的需求也在穩步成長。基於區塊鏈的土地所有權證書發放和補貼分配採購平台也已開始試點,這預示著專業系統整合商未來將迎來商機。同時,由法國、新加坡和多邊合作夥伴支持的「數位互助」計畫為地方政府官員提供技能培訓,從而加強了技術的長期應用。這些舉措加深了菲律賓資訊通訊技術市場在農村地區的滲透,並為供應商創造了可靠的公共部門收入來源。

IT人才持續短缺限制了市場成長。

在人工智慧、數據分析和網路安全領域,只有十分之一的科技求職者符合招募標準,導致約20萬個職缺。儘管菲律賓技術教育與技能發展署(TESDA)的線上註冊人數自2023年以來成長了兩倍,但在主要大學之外,人們仍然缺乏工業4.0設備的實際操作經驗。企業學徒制培訓僅佔所有培訓的不到4%,這阻礙了菲律賓資訊通訊技術(ICT)市場吸收高附加價值計劃的能力。菲律賓半導體和電子工業基金會已提出獎勵方案和一個5億美元的技能基金,以遏制該地區的人才流失,但預計要到2027年才能看到成效。

細分市場分析

到2025年,IT服務將佔菲律賓ICT市場佔有率的27.42%,這主要得益於企業將資本預算轉向以結果為導向的管理解決方案,例如雲端遷移、人工智慧試點和流程自動化。預計到2031年,隨著國際超大規模資料中心業者與本地整合商深化合作,以及通訊業者將5G邊緣解決方案打包銷售,該領域的成長速度將超過硬體支出。同時, IT安全將成為營收成長最快的領域,年複合成長率將達到11.65%,這主要受勒索軟體攻擊事件增加和新的資料隱私法規的推動。

同時,硬體板塊依然疲軟,預計2023年至2024年半導體組裝基地營收成長將較上季萎縮,2025年僅成長1-2%。然而,來自中國的近岸外包以及電動車零件的優惠待遇有望提振印刷電路基板和基板製造設施的投資,從2027年起改善硬體板塊的貢獻。由於各方競相部署光纖和衛星通訊以滿足頻寬需求,通訊服務支出將保持強勁,這將鞏固菲律賓ICT市場頂級軟體和平台收入的基礎。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速部署5G

- 加速中小企業採用雲端運算

- 政府電子政府政府總體規劃 2022-2028

- 超大規模資料中心投資激增

- 電子錢包等數位支付方式的快速成長

- 馬尼拉大都會區以外正在蓬勃發展的科技Start-Ups生態系統

- 市場限制

- 農村地區最後一公里連接缺口

- 資訊科技人員持續短缺

- 電費上漲影響資料中心

- 網路威脅與勒索軟體事件

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

- 宏觀經濟因素的影響

- 產業相關人員分析

第5章 市場規模與成長預測

- 依產品類型

- IT硬體

- 電腦硬體

- 網路裝置

- 周邊設備

- IT軟體

- IT服務

- IT諮詢與實施支持

- IT外包(ITO)

- 業務流程外包(BPO)

- 資安管理服務

- 雲端和平台服務

- IT基礎設施

- IT安全/網路安全

- 通訊服務

- IT硬體

- 按公司規模

- 小型企業

- 主要企業

- 按最終用戶行業分類

- 政府和公共機構

- BFSI

- 資訊科技和電信

- 能源與公共產業

- 零售、電子商務與物流

- 製造業和工業4.0

- 醫療保健和生命科學

- 石油和天然氣

- 遊戲和電子競技

- 其他行業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- Amazon.com Inc.

- Alphabet Inc.(Google)

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- International Business Machines Corporation

- Microsoft Corporation

- Oracle Corporation

- Cognizant Technology Solutions Corporation

- PLDT Inc.

- Globe Telecom Inc.

- Total Information Management Corporation

- Doa Alejandra Inc.

- CTO Phils Inc.

- P-Tech People and Technology Inc.

- Trend Micro Inc.

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Lenovo Group Limited

- SAP SE

- Vendor Positioning Analysis

第7章 市場機會與未來展望

The Philippines ICT market was valued at USD 27.2 billion in 2025 and estimated to grow from USD 30.16 billion in 2026 to reach USD 50.53 billion by 2031, at a CAGR of 10.88% during the forecast period (2026-2031).

This strong trajectory reflects the archipelago's liberalized foreign-investment regime, large-scale 5G roll-outs, more than USD 10 billion in hyperscale data-center commitments, and a government digitalization plan that is migrating over 70% of public services online. Intensifying demand for cloud, edge, and cybersecurity solutions is reinforcing spending momentum, while tower-sharing policies and new common-tower companies are widening network reach to underserved provinces.Simultaneously, the Philippines ICT market is benefiting from ASEAN supply-chain diversification, which is drawing semiconductor assembly, data-analytics, and AI workloads toward the country's growing pool of skilled talent. Heightened competition among fixed and mobile operators is compressing tariffs but stimulating investment in fiber backhaul, private 5G, and satellite links that collectively lift service quality and geographic coverage.

Philippines ICT Market Trends and Insights

Rapid 5G Rollout Drives Infrastructure Modernization

The commercial Philippines ICT market is accelerating network modernization as Globe and PLDT jointly surpassed 100 additional Geo-Isolated and Disadvantaged Area (GIDA) 5G sites in 2025. Expanded mid-band spectrum and the new Apricot subsea cable now lift international capacity 33%, positioning the country as a redundancy hub for hyperscale traffic. 5G private networks are extending to logistics, mining, and precision agriculture where fiber remains impractical, while edge nodes colocated within new data centers deliver sub-10 ms latency critical for smart-factory analytics. Carriers are also experimenting with open-RAN to drive down radio costs and diversify vendors, reinforcing long-run capital efficiency. Collectively, these activities are adding depth and resilience to national connectivity, enabling low-latency applications and boosting the Philippines ICT market's attractiveness to global cloud providers.

Government e-Gov Masterplan Accelerates Public-Sector Digitalization

The Department of Information and Communications Technology has already taken 70% of public services online, issued more than 1 million digital signatures, and deployed 438 VSAT terminals in remote barangays to fulfill e-Gov targets. As ministries migrate databases into sovereign clouds, demand for secure IaaS, SaaS, and integration services grows steadily. Procurement platforms leveraging blockchain for land titling and grant disbursement are being piloted, signaling future opportunities for specialist system integrators. Meanwhile, the Digital Bayanihan program backed by France, Singapore, and multilateral partners supplies skills training for local officials, thus reinforcing long-term adoption. These initiatives deepen the Philippines ICT market penetration into rural regions and produce a reliable public-sector revenue stream for vendors.

Persistent IT-Talent Shortage Constrains Market Growth

Only 1 in 10 technical applicants meets AI, data-analytics, or cybersecurity hiring thresholds, leaving an estimated 200,000 vacancies unfille. Although TESDA has tripled online enrollments since 2023, hands-on exposure to Industry 4.0 equipment remains scarce outside flagship universities. Enterprise-based apprenticeships account for less than 4% of total training, dampening the Philippines ICT market's ability to absorb high-value projects. The Semiconductor and Electronics Industries in the Philippines Foundation is lobbying for incentive packages and a USD 500 million skills fund to stave off regional talent leakage, but any impact is unlikely before 2027.

Other drivers and restraints analyzed in the detailed report include:

- Hyperscale Data-Center Investment Transforms Digital Infrastructure

- Digital-Payments Boom Reshapes Financial-Services ICT

- Rising Electricity Costs Threaten Data-Center Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IT services controlled 27.42% of Philippines ICT market share in 2025 as enterprises shifted capital budgets toward outcome-based managed solutions for cloud migration, AI pilots, and process automation. The segment is forecast to outpace hardware spending through 2031 as international hyperscalers deepen partnerships with local integrators and telcos bundle 5G-enabled edge solutions. At the same time, IT security contributes the fastest incremental revenue, rising at an 11.65% CAGR thanks to ransomware frequency and new data-privacy directives.

The hardware slice remains subdued because the semiconductor assembly base posted just 1-2% top-line growth in 2025 after back-to-back contractions in 2023-2024. Nonetheless, near-shoring from China and incentives for electric-vehicle components are renewing investment in printed-circuit and substrate facilities that could lift hardware contributions after 2027. Communication-services spend is resilient as fiber and satellite deployments race to meet bandwidth demand, strengthening the Philippines ICT market's foundation for higher-layer software and platform revenues.

The Philippines ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security, Communication Services), Enterprise Size (Small and Medium Enterprises, Large Enterprises), and End-User Industry Vertical (Government and Public Administration, BFSI, Energy and Utilities, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture plc

- Amazon.com Inc.

- Alphabet Inc. (Google)

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- International Business Machines Corporation

- Microsoft Corporation

- Oracle Corporation

- Cognizant Technology Solutions Corporation

- PLDT Inc.

- Globe Telecom Inc.

- Total Information Management Corporation

- Doa Alejandra Inc.

- CTO Phils Inc.

- P-Tech People and Technology Inc.

- Trend Micro Inc.

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Lenovo Group Limited

- SAP SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid 5G roll out

- 4.2.2 Accelerated cloud adoption by SMEs

- 4.2.3 Government's e-Gov Masterplan 2022-2028

- 4.2.4 Surge in hyperscale data center investments

- 4.2.5 Digital payments boom via e-wallets

- 4.2.6 Growing tech startup ecosystem outside Metro Manila

- 4.3 Market Restraints

- 4.3.1 Last-mile connectivity gaps in rural provinces

- 4.3.2 Persistent IT talent shortage

- 4.3.3 Rising electricity costs impacting data centers

- 4.3.4 Cyber-extortion and ransomware incidents

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Impact of Macroeconomic Factors

- 4.10 Industry Stakeholder Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 IT Hardware

- 5.1.1.1 Computer Hardware

- 5.1.1.2 Networking Equipment

- 5.1.1.3 Peripherals

- 5.1.2 IT Software

- 5.1.3 IT Services

- 5.1.3.1 IT Consulting and Implementation

- 5.1.3.2 IT Outsourcing (ITO)

- 5.1.3.3 Business Process Outsourcing (BPO)

- 5.1.3.4 Managed Security Services

- 5.1.3.5 Cloud and Platform Services

- 5.1.4 IT Infrastructure

- 5.1.5 IT Security/Cybersecurity

- 5.1.6 Communication Services

- 5.1.1 IT Hardware

- 5.2 By Enterprise Size

- 5.2.1 Small and Medium-sized Enterprises

- 5.2.2 Large Enterprises

- 5.3 By End-user Industry Vertical

- 5.3.1 Government and Public Administration

- 5.3.2 BFSI

- 5.3.3 IT and Telecom

- 5.3.4 Energy and Utilities

- 5.3.5 Retail, E-commerce, and Logistics

- 5.3.6 Manufacturing and Industry 4.0

- 5.3.7 Healthcare and Life Sciences

- 5.3.8 Oil and Gas

- 5.3.9 Gaming and Esports

- 5.3.10 Other Verticals

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Amazon.com Inc.

- 6.4.3 Alphabet Inc. (Google)

- 6.4.4 Cisco Systems Inc.

- 6.4.5 Huawei Technologies Co. Ltd.

- 6.4.6 International Business Machines Corporation

- 6.4.7 Microsoft Corporation

- 6.4.8 Oracle Corporation

- 6.4.9 Cognizant Technology Solutions Corporation

- 6.4.10 PLDT Inc.

- 6.4.11 Globe Telecom Inc.

- 6.4.12 Total Information Management Corporation

- 6.4.13 Doa Alejandra Inc.

- 6.4.14 CTO Phils Inc.

- 6.4.15 P-Tech People and Technology Inc.

- 6.4.16 Trend Micro Inc.

- 6.4.17 Hewlett Packard Enterprise Company

- 6.4.18 Dell Technologies Inc.

- 6.4.19 Lenovo Group Limited

- 6.4.20 SAP SE

- 6.5 Vendor Positioning Analysis

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

日本資訊通訊技術市場:按支出、技術和地區分類,2026-2034年

日本資訊通訊技術市場:按支出、技術和地區分類,2026-2034年 2026年針對政策制定者的全球數位主權市場報告

2026年針對政策制定者的全球數位主權市場報告 新加坡資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

新加坡資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 全球資訊與通訊技術(ICT)市場規模、佔有率、趨勢及成長分析報告(2026-2034)印度資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利資訊通訊技術市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)零售業先進資訊與通訊解決方案的成長機遇資訊通訊科技(ICT)產業客戶經驗(CX)成長機會,2025-2026年

全球資訊與通訊技術(ICT)市場規模、佔有率、趨勢及成長分析報告(2026-2034)印度資訊通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利資訊通訊技術市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)零售業先進資訊與通訊解決方案的成長機遇資訊通訊科技(ICT)產業客戶經驗(CX)成長機會,2025-2026年