|

市場調查報告書

商品編碼

1910586

日本貨運物流市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Japan Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

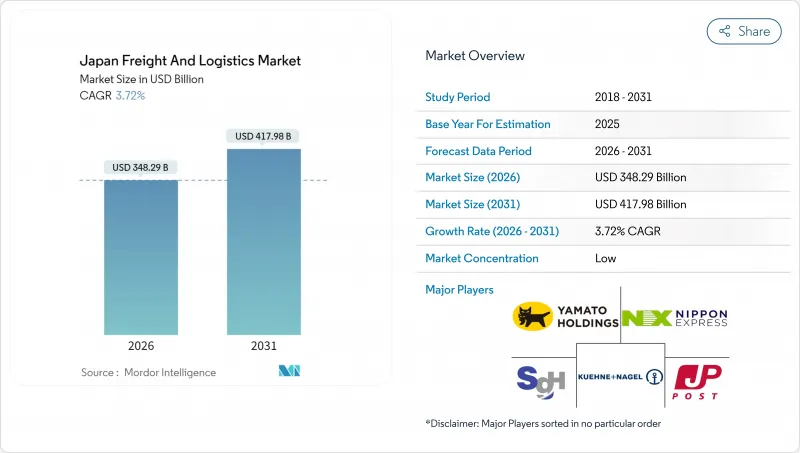

預計到 2026 年,日本貨物和物流市場規模將達到 3,482.9 億美元,高於 2025 年的 3,358 億美元。

預計到 2031 年,該市場規模將達到 4,179.8 億美元,2026 年至 2031 年的複合年成長率為 3.72%。

電子商務訂單量的成長、製造地對第三方物流(3PL)的日益普及以及政府對智慧物流平台的新支持,正在拓展運輸、倉儲和附加價值服務領域的收入來源。內閣府「社會5.0」計畫下的平台互通性要求正在加速數位化融合,而氫燃料電池走廊計劃則為長途運輸車輛的脫碳和緩解日益嚴重的司機短缺問題鋪平了道路。同時,都市區倉儲空間長期短缺以及公路貨運燃料成本的上漲加劇了運輸能力的競爭,迫使營運商轉向自動化、多層倉儲設施和網路重構。高調的勒索軟體攻擊事件顯著增加了網路風險,促使營運商在推進供應鏈數位化的同時,採用零信任架構和冗餘資料中心。

日本貨運和物流市場的趨勢和洞察

電子商務小包裹熱潮

跨境和國內線上零售的擴張推動小包裹量創下歷史新高,使CEP(宅配)成為成長最快的物流功能領域。國內業者正在部署自動化分類機、人工智慧路線規劃和多層配送中心,以滿足人口密集都市區的配送需求。國際專業營運商正在簡化清關流程以縮短配送時間。大和控股與DHL的「GoGreen Plus」服務等合作案例表明,永續性目標與面向注重碳排放消費者的優質小包裹服務正在融合。溫控微型倉配排放的增設旨在支援生鮮食品和藥品的電商業務,這反映出物流模式正從通用處理轉向專業的最後一公里配送解決方案。政府的數位商務政策正在簡化跨境支付和資料共用,減少小規模出口商的行政障礙。小包裹密度的不斷提高同時也給司機招募、加強對自動駕駛機器人的獎勵以及在人口密集城市部署環保配送中心帶來了挑戰。

製造商的第三方物流外包

製造商正在重新定義第三方物流 (3PL) 關係,將其從單純的成本節約協議轉變為創造價值的夥伴關係關係。日本新的價值鏈實質審查法要求二氧化碳排放可追溯性和監管認證,而許多企業內部物流部門難以滿足這些要求。像日立運輸系統這樣的供應商正在整合人工智慧規劃套件和區塊鏈可追溯性,以滿足合規性審核的要求,這使得技術成為一項新的必要條件。三井物產收購一家餐飲物流企業的併購交易趨勢表明,行業正朝著垂直專業化方向發展,將行業洞察與數位化能力相結合。製造商可以獲得動態路線規劃、即時可視性和嵌入式的永續性評分,而第三方物流運營商則可以獲得包含數據分析和監管諮詢等長期契約,這些服務不僅限於實體運輸。這一趨勢使日本的貨運和物流市場成為全球互聯生產網路韌性的關鍵基礎。

司機短缺和工時限制

2024年修訂的加班限制規定將年工作時長限制在960小時以內,這抑制了車輛生產率,並加劇了工資壓力。營運商正在加速併購以整合駕駛人隊伍,例如名鐵運輸在2025年2月進行的區域整合。托運人要么接受更高的現貨貨運附加費,要么將不那麼緊急的貨物改走鐵路或沿海運輸以確保運力。這些限制擴大了自動駕駛卡車和轉運樞紐模式的商業價值,這些模式可以減少每位駕駛者的駕駛時間。政府的燃料電池運輸路線支援措施旨在提高中小型運輸業者建造零排放設施的經濟可行性,並減輕過度勞累員工的負擔。目前,網路重新設計策略的特點是選擇性地最佳化服務並提高載貨率目標。

細分市場分析

到2025年,製造業將佔日本貨運物流市場的37.41%,這反映了該地區以出口為導向的汽車、電子和精密機械產業的集中度。嚴峻的生產週期迫使物流供應商投資於零件同步、保稅倉庫和供應商管理庫存(VMI)專案。九州和東北地區的半導體製造工廠對無塵室級空運解決方案的需求不斷成長,貨運代理商也積極推廣符合濕度和振動控制標準的托盤認證。為了確保價值鏈的韌性,製造商正在尋求港口路線和雙源承運商的多元化,這增加了日本貨運物流市場中第三方物流(3PL)協調的複雜性和價值。

批發和零售雖然規模較小,但預計將成為成長最快的客戶群,2026年至2031年的複合年成長率將達到3.98%。全通路模式要求在門市、暗倉和線上平台實現近乎即時的SKU可見性,這迫使物流合作夥伴將庫存管理API直接整合到客戶的企業計畫系統中。零售商正與承運商共同資金籌措區域配送中心,以確保大型促銷活動的運力,並透過跳區配送降低最後一公里成本。微型倉配機器人和人工智慧需求預測減少了拆分訂單的罰款,提高了托運人和服務供應商的盈利。隨著日本貨運和物流市場的成熟,零售商的物流支出預計將接近製造業水平,這將為第三方物流公司(3PL)向這些領域多元化發展奠定基礎。

截至2025年,貨運代理業務佔日本貨運和物流市場的70.52%。這得歸功於日本密集的工業供應鏈,該供應鏈依賴卡車運輸和沿海支線運輸服務來實現準時制生產週期。該領域受益於綜合多模態服務,這些服務在國內和出口運輸中平衡了成本、可靠性和碳排放指標。儘管基礎貨運量依然強勁,但不斷上漲的柴油額外費用和人事費用正給利潤率帶來越來越大的壓力。為此,主要航運公司正在實施人工智慧驅動的動態定價和自動化轉運場,以提高周轉率並履行合約規定的服務水準協議。因此,日本貨運和物流市場正在經歷一場價值創造的轉變,向數據驅動的貨運協調和預測性維護計劃轉型。

同時,受生鮮食品和醫療保健領域向直接面對消費者的履約模式以及新型訂閱模式的結構性轉變的推動,宅配(CEP)正以4.27%的複合年成長率(2026-2031年)加速成長。機器人服務(RoaS)正在分類中心擴展,使營運商能夠在季節性高峰期靈活調整運力,而無需擁有過多的資產。農村地區的無人機配送試辦計畫正在填補因司機短缺造成的服務缺口。同時,都市區的當日達服務依賴微型配送中心的電動貨運自行車。隨著小包裹密度的持續增加,輕資產網路平台正與實體店合作,擴大宅配櫃和退貨點的數量。競爭格局正從單純的成本優勢轉向生態系統範圍內的協調,這為技術型企業永續地擴大其在日本貨運和物流市場的佔有率創造了平台。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 人口統計數據

- 按經濟活動分類的GDP分配

- 按經濟活動分類的GDP成長

- 通貨膨脹

- 經濟表現及概覽

- 電子商務產業的趨勢

- 製造業趨勢

- 運輸和倉儲業GDP

- 出口趨勢

- 進口趨勢

- 燃油價格

- 卡車運輸營運成本

- 卡車運輸車隊規模(按類型)

- 主要卡車供應商

- 物流績效

- 按交通方式分享

- 海運船隊運力

- 班輪運輸連接

- 停靠港口及航行記錄

- 貨運費率趨勢

- 貨物運輸量趨勢

- 基礎設施

- 法規結構(公路和鐵路)

- 法規結構(海事和航空)

- 價值鍊和通路分析

- 市場促進因素

- 電子商務小包裹熱潮

- 製造商將物流外包給第三方物流(3PL)

- 政府推動智慧物流平台

- 加速自動駕駛卡車試營運(針對老年駕駛的措施)

- 半導體出口激增(準時)

- 氫燃料電池走廊計劃

- 市場限制

- 駕駛人和工時限制

- 燃油和通行費上漲

- 都市區倉儲空間短缺

- 與快速數位化相關的網路風險

- 市場創新

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 終端用戶產業

- 農業、漁業、林業

- 建設業

- 製造業

- 石油天然氣、採礦和採石

- 批發和零售

- 其他

- 物流職能

- 宅配、快捷郵件和小包裹(CEP)

- 按目的地

- 國內的

- 國際的

- 按目的地

- 貨物運輸

- 透過交通工具

- 航空

- 海路和內河航道

- 其他

- 透過交通工具

- 貨物運輸安排

- 透過交通工具

- 航空

- 管道

- 鐵路

- 路

- 海路和內河航道

- 透過交通工具

- 倉儲

- 透過溫度控制

- 非溫控型

- 溫度控制

- 透過溫度控制

- 其他服務

- 宅配、快捷郵件和小包裹(CEP)

第6章 競爭情勢

- 市場集中度

- 關鍵策略舉措

- 市佔率分析

- 公司簡介

- DHL Group

- DSV A/S(Including DB Schenker)

- FedEx

- Hitachi Transport System

- Japan Post Holdings Co., Ltd.

- Kintetsu Group Holdings Co., Ltd.

- Kuehne+Nagel

- Meitetsu World Transport

- Mitsubishi Logistics Corporation

- Mitsui OSK Lines

- Nippon Express Holdings

- Nissin Corporation

- NYK(Nippon Yusen Kaisha)Line

- Sankyu Inc.

- SBS Holdings, Inc.

- Seino Holdings Co., Ltd.

- Senko Group Holdings Co., Ltd.

- SG Holdings Co., Ltd.

- United Parcel Service of America, Inc.(UPS)

- Yamato Transport Co., Ltd.

第7章 市場機會與未來展望

The Japan freight and logistics market size in 2026 is estimated at USD 348.29 billion, growing from 2025 value of USD 335.80 billion with 2031 projections showing USD 417.98 billion, growing at 3.72% CAGR over 2026-2031.

Rising e-commerce order volumes, greater third-party logistics (3PL) adoption in manufacturing hubs, and new government incentives for smart-logistics platforms are widening revenue streams across transport, warehousing, and value-added services. Platform interoperability mandates under the Cabinet Office's Society 5.0 framework are accelerating digital integration, while hydrogen fuel-cell corridor projects create pathways to decarbonize long-haul fleets and mitigate mounting driver shortages. At the same time, persistent urban warehouse land scarcity and higher road freight fuel costs intensify competition for capacity and push operators toward automation, multistory facilities, and network redesign. Cyber-risk exposure climbed sharply after high-profile ransomware attacks, prompting operators to embed zero-trust architectures and redundant data centers into supply-chain-wide digital rollouts.

Japan Freight And Logistics Market Trends and Insights

E-commerce Parcel Boom

Cross-border and domestic online retail have lifted parcel volumes to record highs, making CEP the fastest-growing logistics function segment. Domestic operators deploy automated sorters, AI route planning, and multistory depots to handle dense urban drop-offs, while international specialists streamline customs clearance to compress delivery windows. Partnerships such as Yamato Holdings and DHL's GoGreen Plus service show convergence between sustainability goals and premium parcel offerings that appeal to carbon-conscious consumers. Temperature-controlled micro-fulfillment nodes are being added to support fresh food and pharma e-commerce, reflecting a shift from generic handling to specialized last-mile solutions. Government digital-commerce policies simplify cross-border settlement and data sharing, reducing administrative frictions for small exporters. Accelerating parcel density simultaneously stresses driver availability, thereby reinforcing incentives for autonomous sidewalk robots and eco-depot rollouts in dense cities.

3PL Outsourcing by Manufacturers

Manufacturers are redefining 3PL relationships as value-creation partnerships rather than cost-reduction contracts. New Japanese supply-chain due-diligence laws demand CO2 traceability and regulatory proof points that most in-house logistics departments cannot maintain. Providers like Hitachi Transport System integrate AI planning suites and blockchain traceability to satisfy compliance audits, elevating technology as the new table stakes. Deal activity, typified by Mitsui's bolt-on acquisitions in food-service logistics, signals a pivot toward vertical expertise that blends sector know-how with digital capabilities. Manufacturers gain dynamic routing, real-time visibility, and embedded sustainability scores, while 3PLs secure stickier, multiyear contracts that grow beyond physical transport into data analytics and regulatory advisory. The trend positions the Japan freight and logistics market as a critical resilience lever for globally linked production networks.

Driver Shortage and Work-Hour Caps

Revised 2024 overtime limits capped annual hours at 960, curbing fleet productivity and adding upward wage pressure. Operators accelerate M&A to pool driver rosters, as seen in Meitetsu Transport's February 2025 regional consolidation. Shippers accept higher spot-rate surcharges or shift non-urgent volumes to rail and coastal shipping to secure capacity. The constraint magnifies the business case for autonomous trucks and relay-hub models that cut on-road hours per driver. Government fuel-cell corridor incentives seek to make zero-emission equipment economically viable for smaller carriers, easing compliance for over-worked staff. In the interim, selective service rationalization and higher load-factor targets characterize network redesign strategies.

Other drivers and restraints analyzed in the detailed report include:

- Government Push for Smart-Logistics Platforms

- Autonomous-Truck Pilot Acceleration (Ageing Drivers)

- Urban Warehouse Land Scarcity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing accounted for 37.41% of the Japan freight and logistics market size in 2025, reflecting the country's export-oriented automotive, electronics, and precision machinery complexes. Tight production cycles force logistics providers to invest in synchronized parts-sequencing, bonded warehousing, and vendor-managed inventory programs. Semiconductor fabs in Kyushu and Tohoku elevate demand for clean-room grade air cargo solutions, pushing forwarders to certify pallets for controlled humidity and vibration thresholds. Supply-chain resiliency mandates drive manufacturers to diversify port routings and dual-source carriers, increasing the complexity-and value-of 3PL orchestration roles inside the Japan freight and logistics market.

Wholesale and Retail Trade, though smaller, is the fastest-expanding customer group, projected at a 3.98% CAGR between 2026-2031. Omnichannel models require near-real-time stock-keeping-unit visibility across stores, dark warehouses, and online platforms, compelling logistics partners to integrate inventory APIs directly with client enterprise planning systems. Retailers are co-financing regional fulfillment centers with carriers to secure capacity during mega sale events while lowering last-mile costs through zone skipping. Micro-fulfillment robotics and AI demand forecasting reduce split-order penalties, enhancing profitability for both shippers and service providers. As the Japan freight and logistics market matures, retail players are expected to approach manufacturing levels of logistics spend, underpinning segment diversification for 3PLs.

Freight Transport captured 70.52% of the Japan freight and logistics market share in 2025, anchored by dense industrial supply chains that rely on truck and coastal feeder services for just-in-time production cycles. The segment benefits from integrated multimodal offerings that balance cost, reliability, and carbon metrics across domestic and export flows. Although base volumes remain strong, margin pressure intensifies as diesel surcharges rise and labor costs climb. In response, leading carriers roll out AI-derived dynamic pricing and automated trans-shipment yards that elevate asset turns and support contractual service-level agreements. The Japan freight and logistics market is therefore witnessing a shift in value creation toward data-driven freight orchestration and predictive maintenance programs.

Conversely, CEP is accelerating at a 4.27% CAGR (2026-2031), supported by a structural pivot toward direct-to-consumer fulfillment and new subscription models in groceries and healthcare. Robotics-as-a-Service is scaling inside sortation hubs, allowing operators to flex capacity during seasonal peaks without owning surplus assets. Drone pilot deliveries in rural prefectures fill service gaps left by shrinking driver pools, while same-day urban cycles depend on electric cargo bikes operating from micro-depots. As parcel density further increases, asset-light network platforms partner with brick-and-mortar stores to extend parcel lockers and returns drop-off points. The competitive balance is moving from linear cost advantages to ecosystem orchestration, positioning tech-savvy players for lasting share gains in the Japan freight and logistics market.

The Japan Freight and Logistics Market Report is Segmented by Logistics Function (Courier Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services), and by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL Group

- DSV A/S (Including DB Schenker)

- FedEx

- Hitachi Transport System

- Japan Post Holdings Co., Ltd.

- Kintetsu Group Holdings Co., Ltd.

- Kuehne+Nagel

- Meitetsu World Transport

- Mitsubishi Logistics Corporation

- Mitsui O.S.K. Lines

- Nippon Express Holdings

- Nissin Corporation

- NYK (Nippon Yusen Kaisha) Line

- Sankyu Inc.

- SBS Holdings, Inc.

- Seino Holdings Co., Ltd.

- Senko Group Holdings Co., Ltd.

- SG Holdings Co., Ltd.

- United Parcel Service of America, Inc. (UPS)

- Yamato Transport Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.23 Regulatory Framework (Sea and Air)

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 E-Commerce Parcel Boom

- 4.25.2 3PL Outsourcing by Manufacturers

- 4.25.3 Government Push for Smart-Logistics Platforms

- 4.25.4 Autonomous-Truck Pilot Acceleration (Ageing Drivers)

- 4.25.5 Semiconductor Export Surge (Time-Critical)

- 4.25.6 Hydrogen Fuel-Cell Corridor Projects

- 4.26 Market Restraints

- 4.26.1 Driver Shortage and Work-Hour Caps

- 4.26.2 Escalating Fuel and Toll Charges

- 4.26.3 Urban Warehouse Land Scarcity

- 4.26.4 Cyber-Risk From Rapid Digitalisation

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Buyers

- 4.28.3 Bargaining Power of Suppliers

- 4.28.4 Threat of Substitutes

- 4.28.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 DSV A/S (Including DB Schenker)

- 6.4.3 FedEx

- 6.4.4 Hitachi Transport System

- 6.4.5 Japan Post Holdings Co., Ltd.

- 6.4.6 Kintetsu Group Holdings Co., Ltd.

- 6.4.7 Kuehne+Nagel

- 6.4.8 Meitetsu World Transport

- 6.4.9 Mitsubishi Logistics Corporation

- 6.4.10 Mitsui O.S.K. Lines

- 6.4.11 Nippon Express Holdings

- 6.4.12 Nissin Corporation

- 6.4.13 NYK (Nippon Yusen Kaisha) Line

- 6.4.14 Sankyu Inc.

- 6.4.15 SBS Holdings, Inc.

- 6.4.16 Seino Holdings Co., Ltd.

- 6.4.17 Senko Group Holdings Co., Ltd.

- 6.4.18 SG Holdings Co., Ltd.

- 6.4.19 United Parcel Service of America, Inc. (UPS)

- 6.4.20 Yamato Transport Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026年全球貨車市場報告2026年全球貨運和物流市場報告2026年全球零碳運輸市場報告

2026年全球貨車市場報告2026年全球貨運和物流市場報告2026年全球零碳運輸市場報告 貨運及物流市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、最終使用者及運輸方式分類

貨運及物流市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、最終使用者及運輸方式分類 2026-2030年全球貨物審核與支付市場

2026-2030年全球貨物審核與支付市場 中東歐貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)亞太地區貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)南美貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東歐貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)亞太地區貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)南美貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)