|

市場調查報告書

商品編碼

1693531

歐洲控制釋放肥料:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Europe Controlled Release Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

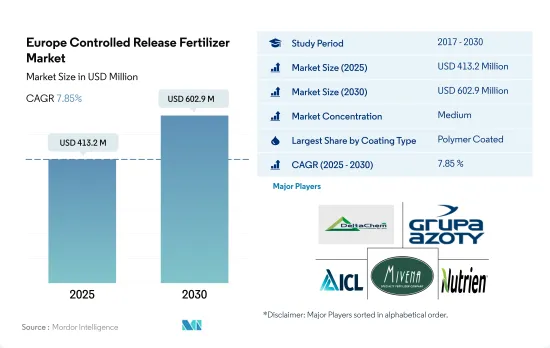

歐洲控制釋放肥料市場規模預計在 2025 年為 4.132 億美元,預計到 2030 年將達到 6.029 億美元,預測期內(2025-2030 年)的複合年成長率為 7.85%。

日益嚴重的環境污染和地下水污染導致該地區擴大採用CRF

- 2017 年至 2021 年間,歐洲控制釋放肥料市場大幅成長了 142.4%。在其他包衣類型中,聚合物包衣控釋肥料在 2022 年佔據了 76.4% 的較大佔有率。

- 2017年至2021年間,聚合物包膜控制釋放肥料的銷售額顯著成長了143.9%,但產量僅成長了24.3%。經歐洲化學管理局鑑定,這些肥料表面塗有該地區不同類型的聚合物,包括聚氨酯、聚乙烯醋酸乙烯酯、乙烯丙烯酸共聚物、甲醛磺酸鹽磺酸縮合物鈉鹽以及植物油基醇酸樹脂。市場規模的成長主要得益於產品價格的上漲,2022年與2017年相比大幅成長了96.3%。

- 歐盟 (EU) 對控制釋放肥料(包括聚合物封裝系統)有規則和法規,目前正處於未來監管階段,直到 2026 年開發出生物分解性肥料。這些因素限制了該地區的市場成長。

- 人們對農業領域污染和水污染的日益擔憂促使農民採用永續的耕作方法和環保肥料。 CRF減少養分的淋失和揮發,並根據作物需求釋放養分,使作物在需要時獲得所需的養分,並降低養分流失的風險。

- 因此,控制釋放肥料的其他包衣類型,尤其是生物分解性和聚合物基包衣類型,在 2023 年至 2030 年期間具有最高的市場潛力。

法國水果種植面積擴大,導致控釋肥使用量增加

- 2022年歐洲控制釋放肥市場中,法國將佔最大的市場佔有率,為22.4%,緊隨其後的是英國。

- 對水果和蔬菜(尤其是葡萄和洋蔥)的需求是西班牙生產活動的重要驅動力。因此,控制釋放包膜肥料的需求預計會上升。這些肥料的使用對葡萄產量有顯著的影響,使用控制釋放肥料每公頃可達到 70 噸,而使用傳統肥料每公頃僅能達到 30-40 噸。這導致聚合物包膜控制釋放肥料的採用率增加,從而提高了西班牙的市場收益。

- 聚合物包膜性肥料佔據市場主導地位,到 2022 年將佔 76.4% 的佔有率。

- 英國整體市場大幅上漲74.4%。這種激增很可能在很大程度上是由於 2022 年初開始的俄羅斯和烏克蘭之間的衝突,導致該國供不應求,隨後價格上漲。

- 法國是世界主要農業生產國之一,2021年收穫了520萬噸水果,成為繼西班牙之後歐洲第四大水果生產國。由於法國高度重視作物品質和產量,並考慮到控制釋放肥料具有減少淋失、減少蒸發和最佳化施用頻率等優點,預計未來幾年對這些肥料的需求將會增加。

歐洲控制釋放肥料的市場趨勢。

田間作物的種植面積一直在擴大,以滿足國內消費和不斷成長的出口需求。

- 在歐洲,油菜、小麥、黑麥和黑小麥等田間作物主要為冬季作物,而玉米、向日葵、水稻和大豆則在夏季種植。大麥是廣泛種植的冬季作物和春季作物。受人口成長和糧食需求增加的推動,歐洲主糧作物種植面積正在穩步擴大。 2017年田間作物收穫面積將達78,500公頃,到2022年將增加至108,000公頃。

- 2021年,歐盟將收穫1.299億噸普通小麥和斯佩耳特小麥,佔穀物總產量的43.7%。這比2020年增加了1,100萬噸,增幅達9.3%。產量增加的原因是收穫面積增加 5.6% 至 2,180 萬公頃,且表觀產量提高。

- 2021年,歐盟玉米和玉米穗混合穀物產量達7,300萬噸,比2020年增加600萬噸。整體成長主要得益於羅馬尼亞(成長46.8%,增產470萬噸)和法國(成長14.5%,增產190萬噸)的強勁復甦。

- 2019年至2022年,該地區的採伐面積下降了34%。儘管如此,玉米和小麥的種植面積分別增加了11%和2%,而其他田間作物則有所下降。預計農民將在 2023 年至 2030 年間增加化肥使用量,以提高產量並抵消近年來收穫面積的下降。

該地區大部分土壤缺氮,因此氮是田間作物消耗的主要養分。

- 2022年,田間作物佔據歐洲養分消耗的大部分,佔總量的85%,利用量為4,700萬噸。這種高需求是由於田間作物的大規模種植及其大量的營養需求所造成的。

- 歐洲主要的田間作物包括小麥、油菜籽、黑麥、大豆和玉米,這些作物都嚴重依賴化肥。 2022年,這些作物氮、磷、鉀平均施用量為每公頃187.3公斤。

- 氮肥成為歐洲田間作物最需要的主要營養肥料,2022 年平均施用量為 130.64 公斤/公頃。氮缺乏是最大的產量限制因素,該地區大多數農業土壤缺乏這種營養,因此必須廣泛施用。

- 鉀是繼氮之後第二消費量的肥料,2022 年的平均施用率為 103.75 公斤/公頃。瑞典、西班牙、波蘭和拉脫維亞等土壤以沙質為主的國家,鉀缺乏問題尤其明顯。其次是磷肥,2022 年施用量為 56.93 公斤/公頃。

- 主要營養肥料對作物起著至關重要的作用,因為它們對於代謝過程以及細胞、細胞膜和葉綠素等重要植物組織的形成至關重要。磷在種植優質作物方面起著至關重要的作用,而鉀則能激活植物生長發育所必需的酵素。

歐洲控制釋放肥料產業概況

歐洲控制釋放肥市場適度整合,前五大企業佔51.97%。該市場的主要企業包括 Ekompany International BV (DeltaChem)、Grupa Azoty SA (Compo Expert)、ICL Group Ltd、Mivena BV、Nutrien Ltd. 等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 主要作物種植面積

- 田間作物

- 園藝作物

- 平均養分施用量

- 主要營養素

- 田間作物

- 園藝作物

- 主要營養素

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 塗層類型

- 聚合物塗層

- 聚合物硫塗層

- 其他

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

- 原產地

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 烏克蘭

- 英國

- 其他歐洲國家

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Ekompany International BV(DeltaChem)

- Grupa Azoty SA(Compo Expert)

- Haifa Group

- ICL Group Ltd

- Mivena BV

- Nutrien Ltd.

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

The Europe Controlled Release Fertilizer Market size is estimated at 413.2 million USD in 2025, and is expected to reach 602.9 million USD by 2030, growing at a CAGR of 7.85% during the forecast period (2025-2030).

Increasing environmental and groundwater contamination lead to higher adoption of CRFs in the region

- The European controlled-release fertilizer market grew significantly by 142.4% from 2017 to 2021. Polymer-coated CRF, among all the other coating types, held the major share, 76.4%, in 2022.

- Between 2017 and 2021, there was a striking increase of 143.9% in the value of polymer-coated controlled-release fertilizers, while the volume increased by only 24.3%. These fertilizers are coated with various types of polymers in the region, including polyurethanes, polyethylene co vinyl acetate, ethylene acrylic acid copolymer, formaldehyde-naphthalene sulfonic acid condensate sodium salts, and alkyds based on vegetable oils, as identified by the ECHA. The rise in market value can be mainly attributed to the surge in product prices, which rose by a significant 96.3% in 2022, compared to 2017.

- The European Union has set rules and regulations for controlled-release fertilizers, including polymer encapsulation systems, which are currently under the scope of future restrictions until they are developed to be biodegradable by 2026. These factors restrict the market growth in the region.

- Growing concerns over agricultural sector pollution and water contamination have led farmers to adopt sustainable agricultural practices and environmentally friendly fertilizers. CRFs reduce nutrient leaching and volatilization and release nutrients based on crop requirements, which will provide necessary nutrients to the crops when required and reduce the risk of nutrient losses.

- Hence, the other coating types segment of controlled-release fertilizers, particularly biodegradable and polymer-based ones, has the highest market potential from 2023 to 2030.

Expansion of fruit cultivation in France increases the CRFs' use

- France held the largest market share of 22.4% in the European controlled release fertilizer market in 2022, with the United Kingdom following closely behind.

- The demand for fruits and vegetables, particularly grapes and onions, is a key driver of production activity in Spain. This, in turn, is expected to boost the demand for controlled release coated fertilizers. The use of these fertilizers has shown a significant impact on grape yields, with controlled release fertilizers delivering 70 metric tons per hectare compared to the 30-40 metric tons achieved with conventional fertilizers. Consequently, the increased adoption of polymer-coated controlled release fertilizers has bolstered the market revenue in Spain.

- Polymer-coated fertilizers dominated the market, accounting for a substantial 76.4% share in 2022.

- The United Kingdom witnessed a significant 74.4% surge in the overall market value. This surge can be largely attributed to the Russia-Ukraine conflict that commenced in early 2022, leading to a supply shortage and subsequent price hikes in the country.

- France, a prominent global agricultural producer, harvested 5.2 million metric tons of fruit in 2021, ranking it as the fourth-largest fruit producer in Europe, trailing behind Spain. Given France's emphasis on crop quality, production, and the advantages of controlled release fertilizers, such as minimizing leaching losses, reducing vaporization, and optimizing application frequency, the demand for these fertilizers is projected to rise in the coming years.

Europe Controlled Release Fertilizer Market Trends

The cultivation area for field crops is consistently expanding to cater to both domestic consumption and the growing export demand

- In Europe, field crops like rapeseed, wheat, rye, and triticale are predominantly winter crops, while maize, sunflowers, rice, and soybean are grown in the summer. Barley, in both winter and spring varieties, is widely cultivated. The area dedicated to major food crops in Europe has been steadily expanding, driven by population growth and rising food grain demand. In 2017, the harvested area for field crops stood at 78.5 thousand ha, which climbed to 108 thousand ha by 2022.

- In 2021, the European Union harvested 129.9 million tonnes of common wheat and spelled, accounting for 43.7% of all cereal grains. This marked an 11.0 million tonne increase from 2020, reflecting a 9.3% surge. The rise was propelled by a 5.6% expansion in the harvested area, reaching 21.8 million hectares, and improved apparent yields.

- In 2021, the European Union's production of grain maize and corn cob mix reached 73.0 million tonnes, up by 6.0 million tonnes from 2020. This overall increase was primarily driven by significant rebounds in Romania (a 46.8% increase, adding 4.7 million tonnes) and France (a 14.5% increase, adding 1.9 million tonnes).

- From 2019 to 2022, the region witnessed a notable 34% decline in harvested area. Despite this, corn/maize and wheat saw respective increases of 11% and 2% in their cultivation areas, while other field crops saw reductions. Farmers are expected to boost fertilizer usage during 2023-2030 to bolster yields and counterbalance the declining harvested areas of recent years.

Nitrogen is the primary nutrient consumed more in field crops as most of the soil in the region is deficient in nitrogen

- In 2022, field crops dominated nutrient consumption in Europe, accounting for 85% of the total and utilizing 47 million metric tons. This high demand can be attributed to both the extensive cultivation of field crops and their significant nutrient requirements.

- The primary field crops in Europe include wheat, rapeseed, rye, soybean, and corn, all of which have a substantial reliance on fertilizers. In 2022, the average application rate of nitrogen, phosphorous, and potassium in these crops stood at 187.3 kg per hectare.

- Nitrogen emerged as the most in-demand primary nutrient fertilizer for European field crops, with an average application rate of 130.64 kg/hectare in 2022. Nitrogen deficiency poses the most significant yield constraint, with a majority of agricultural soils in the region lacking this nutrient, necessitating its widespread application.

- Following nitrogen, potassium took the second spot in fertilizer consumption, with an average application rate of 103.75 kg/hectare in 2022. Notably, countries like Sweden, Spain, Poland, and Latvia face more pronounced potassium deficiencies, primarily due to the prevalence of sandy soils. Phosphatic fertilizers followed with an application rate of 56.93 kg/hectare in 2022.

- Primary nutrient fertilizers hold immense significance for crops, as they are integral to metabolic processes and the formation of crucial plant tissues such as cells, cell membranes, and chlorophyll. Phosphorous plays a vital role in cultivating high-quality crops, while potassium activates enzymes essential for plant growth and development.

Europe Controlled Release Fertilizer Industry Overview

The Europe Controlled Release Fertilizer Market is moderately consolidated, with the top five companies occupying 51.97%. The major players in this market are Ekompany International BV (DeltaChem), Grupa Azoty S.A. (Compo Expert), ICL Group Ltd, Mivena BV and Nutrien Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Ukraine

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ekompany International BV (DeltaChem)

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 ICL Group Ltd

- 6.4.5 Mivena BV

- 6.4.6 Nutrien Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

控釋肥料市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用途、應用方式、地區和競爭格局分類,2020-2030年預測

控釋肥料市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用途、應用方式、地區和競爭格局分類,2020-2030年預測 全球控釋肥料(CRF)市場按類型、功能、產品等級、應用方法、最終用途和地區分類-預測至2030年

全球控釋肥料(CRF)市場按類型、功能、產品等級、應用方法、最終用途和地區分類-預測至2030年 緩釋性肥市場按包覆類型、作物類型、釋放期、養分類型、應用、最終用途和銷售管道分類-2025-2032 年全球預測包衣肥料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、作物類型、地區和競爭情況分類,2020-2030 年)控制釋放液態氮市場按產品類型、包衣類型、形態、釋放機制、施用方法、作物類型、最終用戶和分銷管道分類 - 全球預測 2025-2030

緩釋性肥市場按包覆類型、作物類型、釋放期、養分類型、應用、最終用途和銷售管道分類-2025-2032 年全球預測包衣肥料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、作物類型、地區和競爭情況分類,2020-2030 年)控制釋放液態氮市場按產品類型、包衣類型、形態、釋放機制、施用方法、作物類型、最終用戶和分銷管道分類 - 全球預測 2025-2030 全球硝化抑制劑及尿素酶抑制劑市場分析及預測(至2032年):依產品類型、營養類型、作物類型、施用方法、通路、最終用戶及地區分類

全球硝化抑制劑及尿素酶抑制劑市場分析及預測(至2032年):依產品類型、營養類型、作物類型、施用方法、通路、最終用戶及地區分類 2025年全球控制釋放肥市場報告

2025年全球控制釋放肥市場報告 2025-2033年控釋肥料市場(按類型、形式、應用和地區)報告

2025-2033年控釋肥料市場(按類型、形式、應用和地區)報告 硝化抑制劑及脲酶抑制劑市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測2032 年控制釋放和緩釋性肥市場預測:按類型、作物類型、應用類型和地區分類的全球分析

硝化抑制劑及脲酶抑制劑市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測2032 年控制釋放和緩釋性肥市場預測:按類型、作物類型、應用類型和地區分類的全球分析