|

市場調查報告書

商品編碼

1693530

歐洲微量營養素肥料市場佔有率分析、產業趨勢與成長預測(2025-2030年)Europe Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

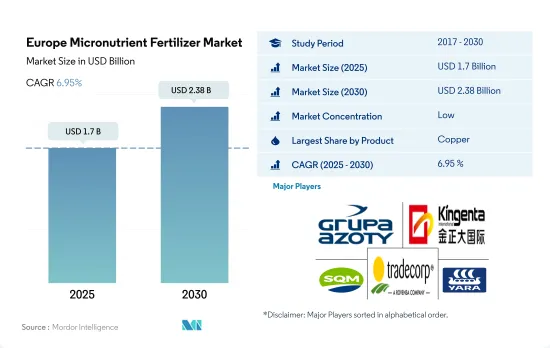

歐洲微量營養素肥料市場規模預計在 2025 年為 17 億美元,預計到 2030 年將達到 23.8 億美元,預測期內(2025-2030 年)的複合年成長率為 6.95%。

鋅在該地區微量營養素肥料市場佔據主導地位

- 俄羅斯在歐洲微量營養素肥料領域佔據主導地位,佔歐洲微量營養素肥料市場的24.2%。此外,預計 2023 年至 2030 年間複合年成長率將達到 7.0%。

- 從形式來看,特種微量營養素市場將在2022年達到最大佔有率,佔市場佔有率的62.6%,其中87.0%主要用於田間作物。隨著科技的不斷進步,專用肥料的使用主要用於田間作物。常規肥料微量營養素市場佔37.3%,田間作物佔88.8%。

- 根據營養類型,鋅在該地區微量營養素肥料市場中佔據主導地位,佔2022年市場價值的29.2%。鋅是植物酵素系統的關鍵組成部分。鋅有助於活化各種酶,促進碳水化合物代謝,其次是銅(26.4%)和鉬(15.7%)。葉面噴布微量營養素肥料是該地區的主流,佔2022年市值的65.0%,其次是施肥,佔34.9%。

- 植物和土壤中的微量營養素缺乏現象正在穩步增加,並成為歐盟的焦點。預計在 2023-2030 年期間,土壤健康狀況惡化、高價值作物種植面積穩步增加、對更高生產率的需求、對先進肥料的認知不斷提高及其採用率不斷提高等因素將推動區域微量營養素肥料市場的發展。

法國是歐洲最大的微量營養素肥料市場。

- 2022 年,法國在歐洲微量營養素肥料市場佔據首位,佔 14.1% 的顯著價值佔有率,相當於 2.184 億美元。法國農民越來越意識到土壤中微量營養素缺乏的重要性,導致對微量營養素肥料的需求激增。

- 俄羅斯已成為歐洲領先的微量營養素肥料市場,2022 年的市場佔有率為 1.493 億美元,佔 9.6%。在微量營養素中,鋅基肥料佔據俄羅斯市場的主導地位,佔總量的28.2%。

- 烏克蘭佔歐洲微量營養素肥料市場的13.8%,2022年市場規模為2.141億美元。同年該國微量營養素肥料消費量為61,200噸。值得注意的是,儘管面臨新冠疫情的挑戰,烏克蘭市場仍維持持續成長。

- 歐洲微量營養素肥料的消費可能會面臨熱浪和持續的能源危機的阻力。然而,隨著農民對先進技術和肥料(尤其是專用微量營養素)的接受度不斷提高,市場也有望持續成長。

- 預計歐洲微量營養素肥料市場將受到土壤健康惡化、高價值作物種植擴張、追求提高生產力和增加肥料供應等因素的推動。

歐洲微量營養素肥料市場趨勢

田間作物的種植面積一直在穩步增加,以滿足國內和出口的需求。

- 在歐洲,油菜、小麥、黑麥、小黑小麥等田間作物是主要的冬季作物,而玉米、向日葵、水稻和大豆則是夏季作物。大麥有冬季和春季兩種品種,分佈廣泛。歐洲主糧作物的種植面積一直在穩定增加,主要原因是人口成長和糧食需求增加。 2017年田間作物將達78,500公頃,2022年將增加至108,000公頃。

- 2022年歐盟普通小麥產量預估為2.827億噸,相當於穀物總產量的54.0%。這比2020年增加了1,100萬噸,成長了9.3%。這一成長反映了收穫面積的增加(成長 5.6%,達到 2,180 萬公頃)以及表觀產量的提高。

- 2019年至2022年,該地區的收穫面積減少了34%。儘管整體種植面積下降,但玉米種植面積增加了 11%,小麥種植面積增加了 2%,而同期其他田間作物的種植面積則減少。 2023年至2030年間,預計農民將增加化肥使用量,以提高產量並減輕近年來收穫面積整體下降的影響。

- 因此,農民面臨越來越大的壓力,需要提高產量和作物產量以滿足日益成長的需求,而且隨著田間作物總種植面積的增加,預計肥料市場將在 2023 年至 2030 年間大幅成長。

鋅是該地區使用最廣泛的微量營養素肥料。

- 歐洲土壤微量營養素缺乏症是由於淋溶流失、過多降雨和土壤剖面較淺等因素造成的。 2022年,歐洲田間作物微量營養素的平均施用率為3.85公斤/公頃。 2022年,鋅、銅、鐵、錳、硼將佔最大的市場規模,佔有率分別為38.28%、25.09%、13.68%、11.68%、4.168%、0.021%。錳的平均施用量為9.33公斤/公頃,佔該地區微量營養素肥料總消費量的11.68%。錳缺乏嚴重阻礙了大豆、小麥、甘蔗和玉米等主要田間作物的生產。

- 在作物中,小麥、高粱、大豆和棉花是微量營養素肥料的主要消耗作物,玉米和水稻比例較小。 2022年,小麥位居榜首,消耗錳11.54公斤/公頃,鋅5.87公斤/公頃,銅6.60公斤/公頃。鋅成為該地區使用最廣泛的微量營養素肥料,佔2022年總消費量的38.28%,平均施用率為5.72公斤/公頃。其次是銅、鐵和硼,平均施用量分別為6.31公斤/公頃、3.70公斤/公頃和1.50公斤/公頃。

- 微量營養素在為作物提供均衡營養方面發揮重要作用,其缺乏會影響作物的生長。因此,歐洲微量營養素肥料市場正在成長,這在很大程度上是由於土壤中微量營養素缺乏現象的日益普遍。

歐洲微量營養素肥料產業概況

歐洲微量營養素肥料市場細分,前五大公司佔21.44%。市場的主要企業包括 Grupa Azoty SA(Compo Expert)、Kingenta Ecoological Engineering Group、Sociedad Quimica y Minera de Chile SA、Trade Corporation International 和 Yara International ASA。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 主要作物種植面積

- 田間作物

- 園藝作物

- 平均養分施用量

- 微量營養素

- 田間作物

- 園藝作物

- 微量營養素

- 灌溉農田

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 產品

- 硼

- 銅

- 鐵

- 錳

- 鉬

- 鋅

- 其他

- 如何申請

- 受精

- 葉面噴布

- 土壤

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

- 原產地

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 烏克蘭

- 英國

- 其他歐洲國家

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- AGLUKON Spezialduenger GmbH & Co.

- Fertiberia

- Grupa Azoty SA(Compo Expert)

- Haifa Group

- Kingenta Ecological Engineering Group Co., Ltd.

- Sociedad Quimica y Minera de Chile SA

- Trade Corporation International

- Valagro

- Verdesian Life Sciences

- Yara International ASA

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

The Europe Micronutrient Fertilizer Market size is estimated at 1.7 billion USD in 2025, and is expected to reach 2.38 billion USD by 2030, growing at a CAGR of 6.95% during the forecast period (2025-2030).

Zinc dominates the micronutrient fertilizers market in the region

- In Europe, Russia accounted for the majority of micronutrient fertilizers, holding 24.2% of the value of Europe's micronutrient fertilizer market. Moreover, it is anticipated to register a CAGR of 7.0% between 2023 and 2030.

- By form, the specialty type micronutrient market was the largest in 2022, accounting for 62.6% of the market value, and was majorly applied to field crops at 87.0%. With increased technological and scientific advancements, specialty fertilizer applications are primarily used for field crops. The conventional type fertilizer micronutrient market accounted for 37.3%, and this fertilizer application was majorly applied to field crops at 88.8%.

- By nutrient type, zinc dominated the micronutrient fertilizers market in the region, accounting for 29.2% of the market value in 2022. Zinc is a major component of plant enzyme systems. Zinc aids in the activation of various types of enzymes, boosting carbohydrate metabolism, followed by copper at 26.4%, and molybdenum accounting for 15.7%. Micronutrient fertilizers are mostly applied through foliar application in the region, accounting for 65.0% of the market value in 2022, followed by fertigation at 34.9%.

- Micronutrient deficiency in plants and soil has been steadily increasing and has become a major cause of concern in the European Union. Factors such as depleting soil health, steadily increasing area under high-value crops, the requirement for higher productivity, and improved awareness about advanced fertilizers and their increasing adoption are expected to drive the regional market for micronutrient fertilizers between 2023 and 2030.

France is the largest micronutrient fertilizer market in the European region.

- In 2022, France held the top spot in the Europe's micronutrient fertilizer market, commanding a significant 14.1% value share, equivalent to USD 218.4 million. French farmers are increasingly recognizing the significance of micronutrient deficiencies in their soils, leading to a surge in demand for these fertilizers.

- Russia emerged as the leading micronutrient fertilizer market in Europe, capturing a market share of 9.6% and a value of USD 149.3 million in 2022. Among the micronutrients, zinc-based fertilizers dominated the Russian market, comprising 28.2% of the total volume.

- Ukraine accounted for 13.8% of the European micronutrient fertilizer market, valued at USD 214.1 million in 2022. The country consumed 61.2 thousand metric tons of these fertilizers in the same year. Notably, the Ukrainian market has exhibited consistent growth, even amidst the challenges posed by the COVID-19 pandemic.

- Europe's micronutrient fertilizer consumption might face headwinds from heatwaves and an ongoing energy crisis. However, the market is poised for growth, driven by farmers' increasing embrace of advanced technologies and fertilizers, particularly specialty micronutrient variants.

- The European micronutrient fertilizer market is set to be propelled by factors such as deteriorating soil health, expanding cultivation of high-value crops, the pursuit of enhanced productivity, and the growing availability of fertilizers.

Europe Micronutrient Fertilizer Market Trends

The cultivation area of field crops is steadily rising to meet domestic needs and export demand

- Field crops, such as rapeseed, wheat, rye, and triticale, are the main winter crops in Europe, while maize, sunflowers, rice, and soybean are summer crops. Both winter and spring types of barley are widely available. The area harvested under major food crops in Europe has been steadily increasing, primarily due to the growing population and increasing demand for food grains. Field crops accounted for 78.5 thousand ha in 2017, which increased to 108 thousand ha in 2022.

- The European Union harvested 282.7 million tons of common wheat in 2022, the equivalent of 54.0% of all cereal grains harvested. This was 11.0 million tons more than in 2020, an increase of 9.3%. This upturn reflected a rise in the area harvested (up 5.6% to 21.8 million hectares) and improved apparent yields.

- Between 2019 and 2022, there was a notable 34% decline in the harvested area within the region. Despite this overall reduction, the areas dedicated to corn/maize and wheat cultivation experienced increases of 11% and 2%, respectively, while the acreages for other field crops decreased during the same period. It is anticipated that farmers will augment their fertilizer usage during the 2023-2030 period, aiming to enhance yields and mitigate the impact of the overall decrease in harvested areas observed in recent years.

- Therefore, with rising pressure on farmers to improve yield and grain production to meet the growing demand and with the overall field crop cultivation area increasing, the fertilizer market is expected to grow significantly during the 2023-2030.

Zinc has become the most used micronutrient fertilizer in the region

- Micronutrient deficiencies in European soils stem from factors such as leaching losses, excessive rainfall, and shallow soil profiles. In 2022, the average application of micronutrients for field crops in Europe stood at 3.85 kg/hectare. In 2022, zinc, copper, iron, manganese, and boron commanded the highest market values, with shares of 38.28%, 25.09%, 13.68%, 11.68%, 4.168%, and 0.021%, respectively. Manganese, with an average application rate of 9.33 kg/ha, led the pack, accounting for 11.68% of the total micronutrient fertilizer consumption in the region. Its scarcity severely hampers the production of key field crops like soy, wheat, sugarcane, and maize.

- Among the crops, wheat, sorghum, soybean, and cotton were the major consumers of micronutrient fertilizers, while corn and rice had a smaller share. In 2022, wheat topped the charts, consuming 11.54 kg/ha of manganese, 5.87 kg/ha of zinc, and 6.60 kg/ha of copper. Zinc emerged as the most widely used micronutrient fertilizer in the region, accounting for 38.28% of the total consumption in 2022, with an average application rate of 5.72 kg/ha. Copper, iron, and boron followed with average application rates of 6.31, 3.70, and 1.50 kg/ha, respectively.

- Micronutrients play a crucial role in providing balanced nutrition to crops, and their deficiency can hinder crop growth. As a result, the market for micronutrient fertilizers in Europe is witnessing growth, significantly fueled by the escalating prevalence of soil micronutrient deficiencies.

Europe Micronutrient Fertilizer Industry Overview

The Europe Micronutrient Fertilizer Market is fragmented, with the top five companies occupying 21.44%. The major players in this market are Grupa Azoty S.A. (Compo Expert), Kingenta Ecological Engineering Group Co., Ltd., Sociedad Quimica y Minera de Chile SA, Trade Corporation International and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Country

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Italy

- 5.4.4 Netherlands

- 5.4.5 Russia

- 5.4.6 Spain

- 5.4.7 Ukraine

- 5.4.8 United Kingdom

- 5.4.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 AGLUKON Spezialduenger GmbH & Co.

- 6.4.2 Fertiberia

- 6.4.3 Grupa Azoty S.A. (Compo Expert)

- 6.4.4 Haifa Group

- 6.4.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.6 Sociedad Quimica y Minera de Chile SA

- 6.4.7 Trade Corporation International

- 6.4.8 Valagro

- 6.4.9 Verdesian Life Sciences

- 6.4.10 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

2026年全球微量元素肥料市場報告

2026年全球微量元素肥料市場報告 微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年)

微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年) 中國微量營養素肥料市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)中東和非洲微量營養素肥料:市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030 年)亞太地區微量營養素肥料:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)北美微量營養素肥料:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美微量營養素肥料:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印度微量營養素肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)微量營養素肥料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國微量營養素肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)

中國微量營養素肥料市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)中東和非洲微量營養素肥料:市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030 年)亞太地區微量營養素肥料:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)北美微量營養素肥料:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美微量營養素肥料:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印度微量營養素肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)微量營養素肥料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國微量營養素肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)